News

Tax Newsflash

EU begins anti-subsidy investigation on China's new battery electric vehicles

Published date: 6 October 2023

On 4 October 2023, the European Commission self-initiated (i.e., independent of any particular complaint from any third party) an anti-subsidy proceeding concerning imports of new battery electric vehicles (BEVs) originating in China that are designed for the transport of persons. The products under investigation are new BEVs principally designed for the transport of nine or fewer people (including the driver) propelled solely by one or more electric motors. Motorcycles are excluded from the investigation.

The investigation will look into whether BEV value chains in China benefit from illegal subsidization (under EU law/WTO rules), and whether this subsidization does, or could, cause economic injury to EU BEV producers. The investigation into potential illegal subsidization covers the period from 1 October 2022 to 30 September 2023 (the investigation period). The examination of trends relevant for the assessment of any economic injury covers the period from 1 January 2020 to the end of the investigation period.

Background

Amidst global decarbonization efforts, China's automotive industry has rapidly expanded its international presence, driven by the electrification trend. According to statistics from the China Association of Automobile Manufacturers, in 2022 BEV exports from China have continued to increase rapidly, becoming a significant player in China’s foreign trade exports, alongside lithium batteries and solar photovoltaics. According to the statistics from China’s General Administration of Customs, China exported 679,000 BEVs in 2022. The EU has emerged as a significant growth market for these BEV exports from China.

The rapid growth of China's BEV industry has sparked concerns within the EU. In the past few months, there has been widespread and persistent discussions around potential EU anti-dumping and countervailing duty investigations (AD/CVD investigations) on China's new energy vehicles. On 13 September 2023, Ursula von der Leyen, the president of the European Commission, announced that “the Commission is launching an anti-subsidy investigation into electric vehicles coming from China,” which was followed by the publication of a notice on 4 October 2023 to initiate the anti-subsidy investigation.

EU anti-subsidy overview

Authority in charge

The European Commission is the authority responsible for conducting AD/CVD investigations regarding dumped and/or subsidized products causing material economic injury to EU industry, and for imposing measures related to such products.

Legal framework

The current effective EU anti-subsidy regulation is Regulation (EU) 2016/1037 on protection against subsidized imports from countries not members of the EU (the basic anti-subsidy regulation). This regulation was amended in 2017, 2018, and 2020.

EU anti-subsidy investigations

Anti-subsidy investigations refer to the European Commission's actions to counteract subsidy practices that are found to cause economic injury to EU industries. Key considerations for such anti-subsidy investigations include:

- Determination of subsidy: This refers to financial assistance provided by the government or any public entity of the exporting country (region) that benefits the recipient, as well as any form of income or price support.

- Specificity: Specificity refers to whether the subsidy is targeted at certain enterprises, industries, or specific regions.

- Economic injury: Even if there are subsidized products imported into the EU, anti-subsidy measures can only be taken if it is also determined that the subsidy products cause material economic injury, the threat of economic injury, or material retardation of the establishment of such industry in the EU.

- Causality: After determining subsidy, specificity, and economic injury, the European Commission will then assess the causal link between subsidized imports and economic injury to EU industries, i.e., whether the economic injury suffered by EU industries is a result of the subsidized imports.

- EU interest: In deciding whether to implement provisional or final anti-subsidy measures, the European Commission is obliged to conduct an EU interest test to determine whether implementing anti-subsidy measures would not be against the interest of the EU.

Procedures for EU anti-subsidy investigations:

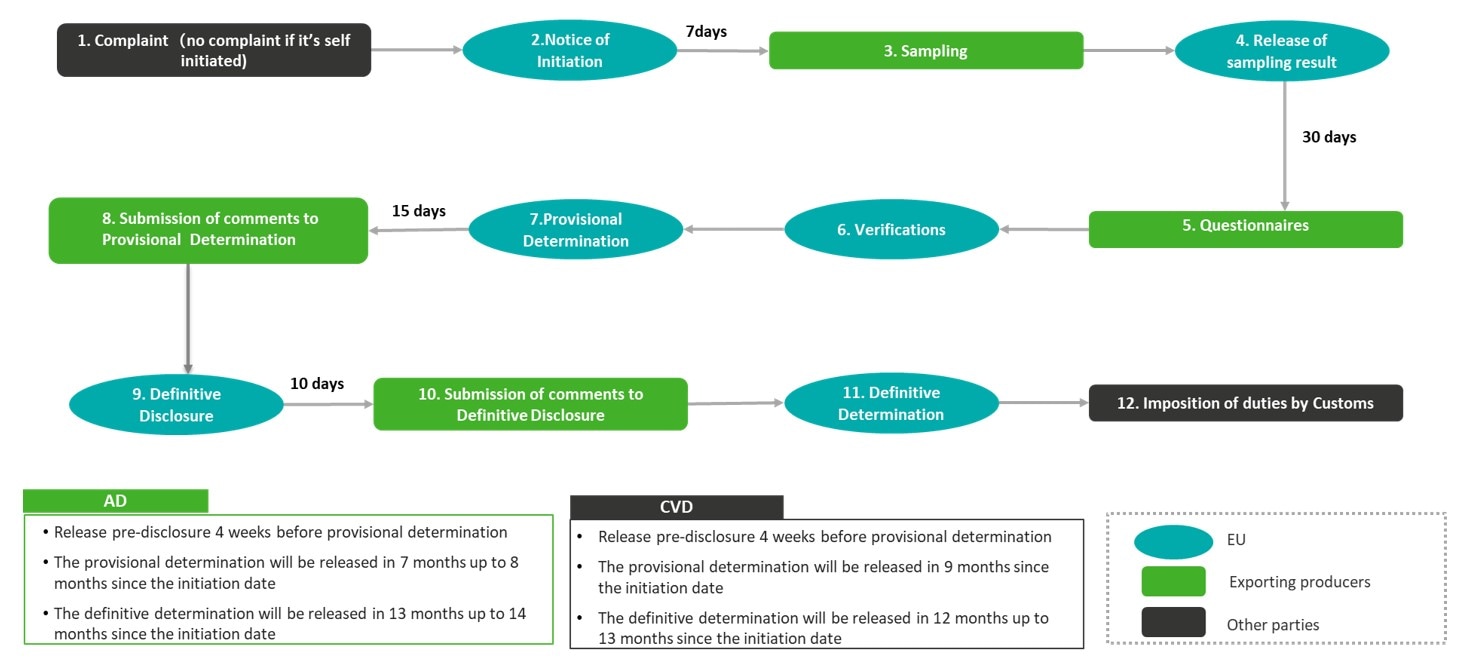

The main investigation processes and timelines for EU AD/CVD investigations are summarized below:

Pursuant to the EU anti-subsidy rules, when the investigation involves a large number of “exporting producers,” the European Commission may conduct a sampling procedure to limit the number of exporting producers under investigation to a reasonable scope. An exporting producer is any company in the country concerned that produces and exports the product under investigation to the EU market, either directly or via a third party, including any of its related companies involved in the production, domestic sales, or exports of the product under investigation.

Affected exporting producers are required to submit sampling responses within seven days of the date of publication of the EU notice of initiation. Exporting producers with the largest representative volume of exports to the EU may be included in the sample and subject to separate anti-subsidy duty rates. Other exporting producers that have submitted sampling responses but have not been included in the sample will be considered as non-sampled cooperating exporting producers, and the anti-subsidy duty that may be applied to imports from them will not exceed the weighted average subsidy amount of the sampled exporting producers. Exporting producers that do not submit a sample response will be considered non-cooperative and will be subject to the highest anti-subsidy duty rate.

Comments

Previous AD/CVD investigations by the EU against China have often resulted in a positive determination and subsequent imposition of high anti-subsidy duties. However, the EU's AD/CVD investigations against China may also have a demonstrative effect, such that after the EU initiates investigations into Chinese products, other countries may follow suit and also initiate their own AD/CVD investigations into similar Chinese products. Once any such measures are implemented, there could be a significant impact on the strategic planning and business activities of Chinese exporting companies. Therefore, it is essential for potentially affected Chinese exporting companies to fully understand the potential EU trade remedy measures and market regulations and proactively respond to them.

Establish an AD/CVD early warning and response mechanism

Potentially affected Chinese enterprises should first fully understand and familiarize themselves with the laws, regulations, and relevant procedures related to AD/CVD investigations. When establishing an international supply chain, it is advisable to set up risk control mechanisms in a timely manner. In general, during the early stages of investment, companies should conduct comprehensive research and due diligence to assess the risks of trade remedy investigations. During and after the investment period, companies should adjust their internal control systems, processes, and operations in response to the dynamics of AD/CVD investigations. Companies should also regularly monitor warning information released by relevant authorities and trade associations, and consider adjusting import and export models, product structures, and risk control plans accordingly.

Actively defend and strive for favourable investigation results

Historically, Chinese companies involved in EU AD/CVD investigations have tended to be conservative towards responding, with few actively participating in the defense procedure, which in turn has led to unfavorable results. It is vital to note that if a company does not respond to the investigation, it will be subject to the highest duties applied to “all other companies,” facing increased duty costs for entry into the EU market for at least five years and may continue to face restrictions after the sunset/expiry review.

When an AD/CVD investigation is initiated, prompt and thorough responses are expected by the authorities. Cooperation and disclosure of accurate and complete data will help towards obtaining a favorable decision in terms of the subsequent duty rate on imports to the EU market. Chinese companies involved in such cases should consider the necessity of participating in the defense based on factors such as the market share and capacity in the EU market and the company's future development direction. In addition, factors such as whether the relevant financial information can be readily available to support the entire value chain analysis should be taken into consideration in order to properly plan the defense strategy.

Specifically, companies should strategically allocate resources by:

- Identifying key leaders who are responsible for the defense work and appropriately engaged to actively motivate employees in the defense efforts, and to coordinate with external stakeholders (e.g., Ministry of Commerce, industry associations); and

- Appointing key personnel who are responsible for working in coordination with external advisors.

In addition, companies should properly respond to the investigation and submit comments by:

- Actively responding to questionnaires and deficiency letters from the European Commission and assessing and submiting data and supporting documents;

- Maintaining consistency in responses across all questionnaires and documents;

- Preparing for the on-site verification, with the assistance of professional consultants where deemed necessary; and

- Actively explore solutions (e.g., applying for product exclusions) to protect the company’s interest during the European Commission's hearing.

Reconstruct global supply chains

Regardless of whether the investigation result is positive, the investigation can have a far-reaching impact on the enterprise's global supply chain. Where the investigation determines that the Chinese enterprise will suffer additional CVD duties, these will last for at least five years. EU importers may therefore choose to discontinue trading with such enterprises due to the impact of the tariff costs, and the enterprises may have to withdraw from the original market.

Where the investigation results in no additional CVD duties for the Chinese enterprise or where the relevant enterprises are not within the scope of the investigation, it may still be appropriate to consider a review (and possible restructuring) of the global supply chain so as to reduce the likelihood of similar investigations in the future.

Authors:

Dolly Zhang

Partner

+86 21 6141 1113

dozhang@deloitte.com.cn

Roger Chen

Partner

+86 21 2316 6922

rogechen@deloitt.com.cn

Michael Wu

Senior Manager

+86 21 2312 7198

michaelzwu@deloitte.com.cn

Allen Lyu

Manager

+86 10 8534 2079

alllyu@deloitte.com.cn

Should you have any questions, please contact:

Tax and Business Advisory

Indirect Tax Services

National Leader

Lily Li

Partner

+86 21 6141 1099

lilyxcli@deloitte.com.cn

Deputy National Leader

Shu Tian

Partner

+86 10 8534 2338

shutian@deloitte.com.cn

Northern China

Betty Mu

Director

+86 10 8512 5698

bemu@deloitte.com.cn

Eastern China

Li Qun Gao

Partner

+86 21 6141 1053

ligao@deloitte.com.cn

Southern China

Janet Zhang

Partner

+86 20 2831 1212

jazhang@deloitte.com.cn

Western China

Frank Tang

Partner

+86 23 8823 1208

ftang@deloitte.com.cn