News

Hong Kong Tax Newsflash

Newly published advance ruling and updated guidance on single family office tax concession

Published date: 9 February 2024

The Inland Revenue Department (IRD) recently published an advance ruling case no. 73 and updated guidance on tax concessions for family-owned investment holding vehicles (FIHVs)1 on its website. It is the first advance ruling on tax concessions for FIHVs published by the IRD. The IRD ruled that the applicants are eligible for the tax concessions and their foreign-sourced interest, dividend or disposal gain will not be regarded as a specified foreign-sourced income under the Foreign-sourced Income Exemption (FSIE) regime or will not be chargeable to profits tax as the economic substance requirement is met.

Concurrently, the IRD updated its guidance on tax concessions for FIHVs concerning the substantial activities requirement and information required for application of an advance ruling.

In this article, we summarize the advance ruling and highlight the IRD’s comments, as well as set out the IRD’s updated guidance.

Advance ruling

Background

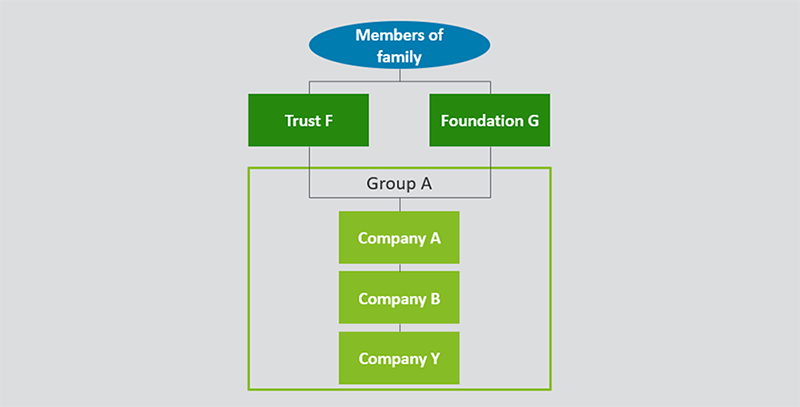

- Before restructuring, the assets of the family were mainly held by Company A and Company B (both incorporated in Hong Kong) within Group A.

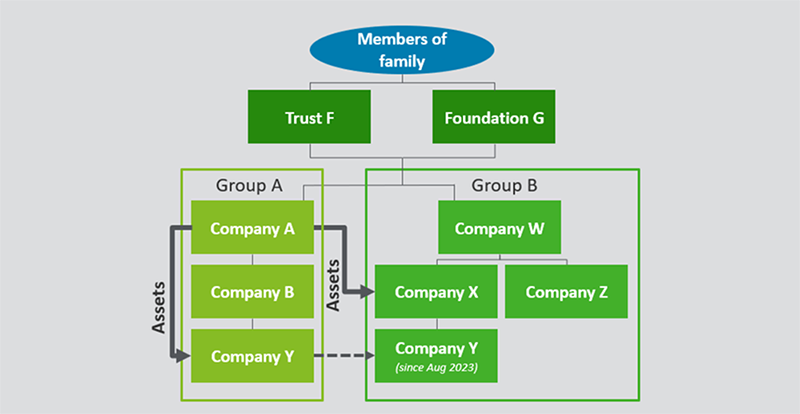

- In a restructuring exercise, certain assets of the family held within Group A were transferred to Company X and Company Y (the applicants) within Group B for arm's length considerations during 2022 and 2023. Any assessable profits of the transferors arising from the transfers will be chargeable to profits tax in Hong Kong.

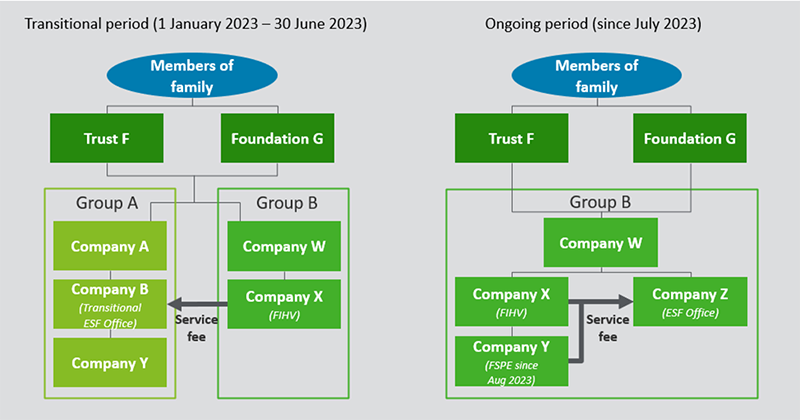

- After the restructuring, the applicants have been managed in Hong Kong by Company B during the period from 1 January 2023 to 30 June 2023 (transitional period) and Company Z during the period from 1 July 2023 and onwards (ongoing period).

The diagrams below illustrate the group structure before and after the restructuring exercise.

Before restructuring

Restructuring exercise

After restructuring

Ruling

- Company X is an FIHV.

- Company X is a wholly owned subsidiary of Company W, whose beneficial interest is at least 95% held by members of the family through a specified trust and a foundation. The IRD made this ruling on the grounds that the members of the family are the specified beneficiaries of Trust F who are entitled to the benefit from the entire trust estate, as well as the only beneficiaries of Foundation G.

- Company X is not a business undertaking for general commercial or industrial purposes.

- Company Y is a family-owned special purpose entity (FSPE).

- Company Y is a wholly owned subsidiary of Company X which is an FIHV.

- Company Y is engaged in investment holding principally holding Schedule 16C assets and does not carry on any other trade or activity.

- Company B and Company Z are eligible single family offices (ESF Offices).

- Company B and Company Z are wholly owned subsidiaries of Company A and Company W respectively, whose beneficial interests are at least 95% held by members of the family through a specified trust and a foundation.

- Company B and Company Z are private companies normally managed or controlled in Hong Kong. In particular, Company X, Company B and Company Z share the same business address in Hong Kong and have common directors. The investment activities were/have been carried out by the employees of Company B and Company Z in Hong Kong.

- At least 75% of the assessable profits of Company B and Company Z were derived from the investment services2 provided to Company X and/or Company Y and were chargeable to profits tax.

- Company X satisfies the conditions for the tax concessions for FIHVs.

- Company X is normally managed or controlled in Hong Kong.

- As at 30 September 2023, the aggregate amount of net asset value of the Schedule 16C assets of Company X and Company Y managed by Company Z amounted to a few billion Hong Kong dollars (i.e. not less than the minimum asset threshold of HK$240 million).

- Company B and Company Z had adequate employees and operating expenditures in Hong Kong.

Number of qualified full-time employees Amount of operating expenditures Company B 3 HKD3 million Company Z 4 HKD10 million

In considering whether the adequacy test is satisfied, the IRD has considered the following:- The number of FIHVs managed by the ESF Office;

- The investment strategies of Company X and Company Y;

- Asset types held by Company X and Company Y;

- Investment activities undertaken by the ESF Office;

- Details of employees employed in Hong Kong (e.g. experience, qualifications, position held and duties performed);

- Amount and types of the operating expenditures (e.g. fixed or variable costs) incurred in Hong Kong.

- The anti-round tripping provisions4 would not apply to Company W as it is regarded as a specified entity.

- Company W is not a business undertaking for general commercial or industrial purposes and does not carry on any trade or business.

- Members of the family have a direct or indirect beneficial interest in Company W which in turn has a 100% direct beneficial interest in Company X.

- The anti avoidance provisions5 would not apply as the purpose of the restructuring exercise is to distinguish the family wealth from the family business of Group A such that the assets of the family can be well-managed by a family office within Group B. Also, the transfers of assets were carried out on an arm’s length basis while the transferors are chargeable to tax in respect of the assessable profits arising from the transfers.

- Any foreign-sourced interest, dividend or disposal gain derived by Company X and Company Y from the qualifying transactions and incidental transactions to which the profits tax concessions apply will not be regarded as specified foreign-sourced income under the FSIE regime.

- In case Company X and Company Y derive any foreign-sourced interest, dividend or disposal gain that falls within the scope of specified foreign-sourced income under the FSIE regime, such income would not be chargeable to profits tax as the economic substance requirement is met.

Applicable period

- The ruling concerning the tax concessions for FIHVs will apply for the year of assessment 2023/24 and subsequent years of assessment.

- The ruling concerning the tax treatments of the specified foreign-sourced income will apply for the years of assessment 2023/24 to 2027/28.

IRD’s guidance

Substantial activities requirement

FIHVs are required to have an adequate number of employees in Hong Kong and operating expenditures incurred in Hong Kong for carrying out their core income generating activities (CIGAs). Outsourcing of CIGAs to the ESF Office is permitted.

The IRD updated its guidance to clarify that it will not apply a mechanical multiplication or division exercise in determining whether the substantial activities requirement is met or specify the exact levels of qualified employees and operating expenditures that are considered adequate for meeting the substantial activities requirement as such levels would depend on the extent and complexity of the investment activities that the outsourced entity needs to carry out for the FIHVs. Instead, it will consider the totality of facts and circumstances of each case. In any event, the minimum thresholds of 2 qualified full-time employees and operating expenditures of HKD2 million should be met.

Information required for advance ruling

The IRD also listed out the information required for application of an advance ruling on the eligibility for tax concessions for FIHVs. Please refer to the guidance on the IRD’s website for details.

Our comments

This is the first advance ruling to confirm the eligibility for tax concessions for FIHVs and is a good reference for those who are planning to apply for such an advance ruling. In particular, the IRD provided detailed comments on how the conditions could be satisfied and the IRD’s considerations.

In this case, the IRD accepted that a restructuring exercise conducted for genuine business purposes, e.g. to distinguish the family wealth from the family business of one group such that the assets of the family can be well-managed by a family office within another group, would not trigger the anti-avoidance provisions. It is helpful as it is of general concern as to how the anti-avoidance provisions would be triggered. This case also provides useful guidance on the interaction between the FSIE regime and the tax concessions for FIHVs.

Applicants planning to apply for an advance ruling for tax concessions for FIHVs should also refer to the IRD’s latest guidance for the information required and seek professional advice where appropriate.

As a side note, we are pleased to share that Hong Kong’s tax concessions for FIHVs were found to be not harmful according to an OECD report newly released on 6 February 2024.

1 For the features of the family office tax concessions, please refer to our Hong Kong Tax Newsflash Issue 166 and Hong Kong Tax Newsflash Issue 179.

2 The investment activities carried out by Company B and Company Z include:

- Conducting research and advising on any potential investments to be made by Company X;

- Acquiring, holding, managing or disposing of property for Company X; and

- Establishing or administering Company Y for holding and administering one or more underlying investments of Company X.

3 The immovable property test, holding period test, control test and short-term asset test.

4 The anti-round tripping provisions provide that the assessable profits of an FIHV or an FSPE are deemed as assessable profits of the resident person if the resident person: (1) has (either alone or jointly with its associate) not less than 30% of the beneficial interest in the FIHV or (2) has any beneficial interest in the FIHV and the FIHV is an associate of the resident person. The anti-round tripping provision does not apply to a resident person which is a resident individual, an ESF Office or a specified entity.

5 The anti-avoidance provisions provide that if the Commissioner is satisfied that (i) the main purpose, or one of the main purposes of an FIHV or FSPE in entering into an arrangement, or (ii) the main purpose, or one of the main purposes of a person making a transfer of any asset/business to the FIHV or FSPE is to obtain a tax benefit, whether for the FIHV or FSPE or another person/entity, the tax concession will not apply to the FIHV or FSPE concerned.

Tax Newsflash is published for the clients and professionals of Deloitte Touche Tohmatsu. The contents are of a general nature only. Readers are advised to consult their tax advisors before acting on any information contained in this newsletter.

If you have any questions, please contact our professionals:

Authors

Roy Phan

Tax Partner

+852 2238 7689

rphan@deloitte.com.hk

Doris Chik

Tax Partner

+852 2852 6608

dchik@deloitte.com.hk

Carmen Cheung

Senior Tax Manager

+852 2740 8660

carmcheung@deloitte.com.hk

International and M&A Tax

National Leader

Vicky Wang

Tax Partner

+86 21 6141 1035

vicwang@deloitte.com.cn

Hong Kong

Anthony Lau

Tax Partner

+852 2852 1082

antlau@deloitte.com.hk

Recommendations

Hong Kong Tax Newsflash

Passage of stamp duty adjustments for residential properties

Hong Kong Tax Newsflash

Hong Kong-Croatia tax treaty signed