Analysis

China automotive consumer study

Consumer opinions on advanced vehicle technology

Published date: 25 July 2023

In the extended automotive ecosystem, consumers will ultimately choose the winners and losers among the companies and brands vying to deliver convenient, low-cost and customized mobility solutions. In the new automotive consumer study on, Deloitte surveyed over 22,000

consumers in 17 countries around the world, and focused on six countries (the

United States, Germany, Japan, South Korea, China and India) to explore

consumers' attitude towards self-driving technologies, their preference in

advanced vehicle technologies and their choice among various mobility services etc. Following are the key findings from the study:

Consumer's attitude towards autonomous vehicles

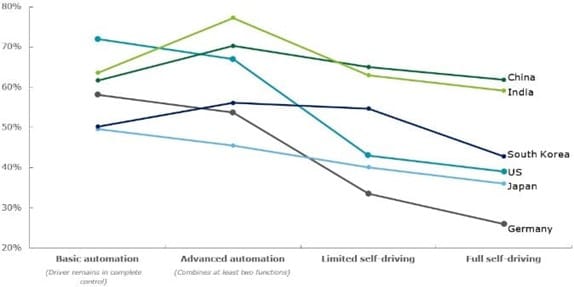

- Interest in different levels of autonomous vehicle technology varies across global markets. Consumers in China and India appear most interested in vehicle automation, while German consumers are more conservative in autonomous driving. (Figure 1)

- Although interest in full self-driving capabilities has risen in both China and the US since 2014, the same cannot be said for other global markets, where interest has remained flat or declined. In terms of generation, Gen Y/Z consumers are generally more interested in fully autonomous vehicles.

- Consumers at present appear consistent in their concerns regarding the safety of fully autonomous vehicle. While having an established track record of fully

self-driving vehicles operating safely on public roads, or if it were offered

by a brand they trust would encourage consumer support for autonomous vehicles. - Consumer opinion appears to diverge on whom they trust to bring self-driving cars to market, consumers in Japan, Germany and the U.S. believe traditional car manufacturers will play the role, while consumers in China and South Korea trust more on new autonomous companies.

Figure 1: Percentage of consumers who prefer different levels of vehicle automation

There is significant opportunity for automakers to capitalize on the success of individual self-driving features such as self-parking and lane control.

Consumer's preference on advanced technology features

- Compared to a variety of advanced technology features, we found technologies that deliver advanced, predictive safety capabilities were ranked as the most preferred, while features that provide customized entertainment, notification of places of interest and technologies that manage daily activities are viewed as least useful. (Figure 2)

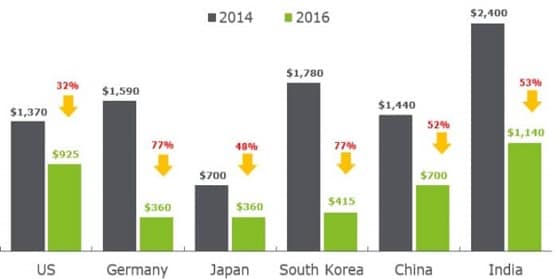

- Consumers are generally willing to pay a little extra for access to advanced tech features, but the amount consumers willing to pay has declined significantly since 2014. (Figure 3)

Figure 2: Advanced technology features that consumer say are most and least useful (rank order by country)

Most useful technology feature |

Category |

CN |

US |

DE |

JP |

KR |

IN |

Recognizes |

Safety |

1 |

1 |

1 |

1 |

2 |

1 |

Blocks |

Safety |

2 |

3 |

2 |

2 |

1 |

2 |

Informs |

Safety |

3 |

2 |

3 |

2 |

3 |

4 |

Takes |

Safety |

4 |

4 |

4 |

3 |

4 |

3 |

Enables |

Connectivity |

5 |

8 |

10 |

5 |

9 |

11 |

Least |

Category |

CN |

US |

DE |

JP |

KR |

IN |

Empowers |

Miscellaneous |

28 |

29 |

30 |

28 |

22 |

27 |

Enables |

Convenience |

29 |

16 |

23 |

26 |

30 |

24 |

Provides |

Convenience |

30 |

26 |

32 |

30 |

28 |

28 |

Enables |

Connectivity |

31 |

19 |

25 |

24 |

21 |

22 |

Helps |

Convenience |

32 |

32 |

31 |

27 |

32 |

31 |

Figure 3: Overall expected price which consumers are willing to pay for advanced automotive technologies (2014 and 2016)*

* The dollar value for each country represents the average of overall weighted prices across the five technology categories (safety, connectivity, cockpit/convenience, self-drive, and alternative powertrain). The non-USD currency has been converted into USD by using the average exchange rates in 2016.

Consumers expect advanced technology features that were once considered premium options to become standard features that do not increase the price of the vehicle.

Consumer's option for mobility services

- In terms of consumer's option for mobility, almost half of consumers in emerging markets like China and India use ride-hailing services at least once a week, eclipsing the U.S. and South Korea, and well ahead of Germany. But the adoption of ride-hailing services in urban and non-urban settings varies between countries.

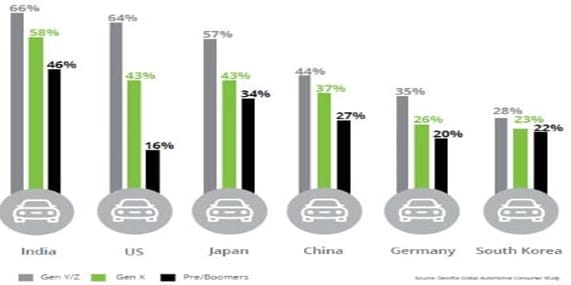

- By generation, Gen Y/Z consumers are more likely to use ride-hailing services. In addition, those young consumers who regularly use ride-hailing are also more likely to question their need to own a vehicle than older consumers. (Figure 4)

Figure 4: Percentage of consumers who use

ride-hailing services that question whether they need to own a vehicle in the future, by generation

Ride-on-demand, folded more broadly into shared mobility and transportation services, will disrupt car ownership.