Property and casualty insurance industry remade

Scenarios for resilient leaders in a post-COVID-19 world

Uncertainties related to COVID-19 make it difficult to predict the future for property and casualty (P&C) insurance leaders. These scenarios explore how the US property and casualty insurance industry landscape may develop over the next one to three years to help spark insight and spot future opportunity.

In the wake of COVID-19, Deloitte and Salesforce hosted a dialogue among some of the world's best-known scenario thinkers to consider the societal and business impact of the pandemic. The results of this collaboration can be found in The world remade: Scenarios for resilient leaders.

The P&C insurance industry remade

Humanity is facing a crisis unlike any known to our generation—and as a result, insurers must prepare for an uncertain future. We explore how the insurance sector might evolve over the next one to three years in our latest perspective so you can:

- Understand how trends we see during the pandemic could shape what insurance may look like in the medium term.

- Have productive conversations around the lasting implications and impacts of the crisis.

- Identify decisions and actions that will improve resilience in this rapidly changing landscape.

- Move beyond responding to the crisis and towards recovering in the near term.

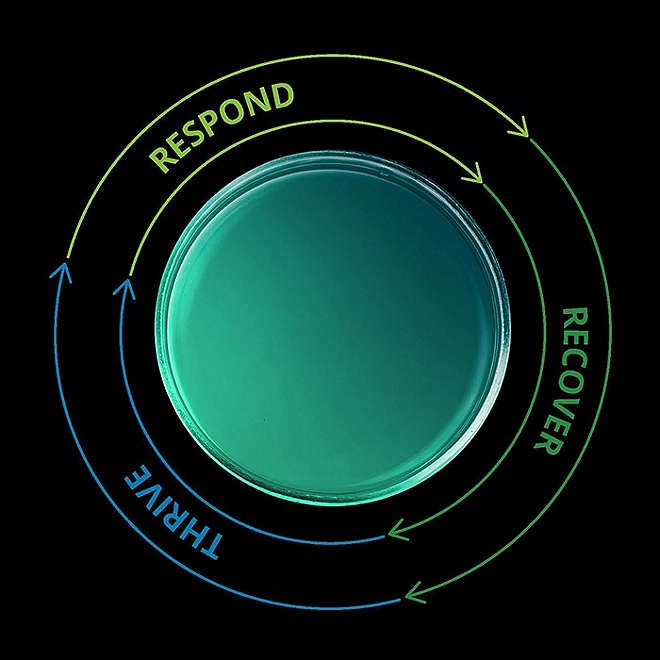

Deloitte’s Resilient Leadership framework defines three time frames of the crisis.

Four COVID-19 property and casualty insurance scenarios

The current crisis could unfold in four ways over the next one to three years.

Five critical uncertainties will drive the overall impact of COVID-19:

- The overall severity of the pandemic and pattern of disease progression.

- The level of collaboration within and between countries.

- The health care system response to the crisis.

- The economic consequences of the crisis.

- The level of social cohesion in response to the crisis.

The passing storm

- The pandemic is managed due to effective responses from governments and health providers.

- Lasting economic repercussions, which disproportionately affect small and midsized businesses and lower- and middle-income individuals and communities.

Property and casualty industry impact

- Strong regulatory and policy response helps prevent structural industry damage.

- Most insurers weather the storm due to both strong capital reserves, quick revert of customer expectations, and a hard rate environment.

- Market consolidation slightly above the precrisis rate as a few small or mid-tier insurers realize they lack resources to invest as required.

- Private equity–fueled channel consolidation continues.

Good company

- Governments globally struggle to handle the crisis alone, with large companies filling the gap.

- Acceleration of trends toward “stakeholder capitalism.”

- Companies become more purpose-driven; rise in partnerships and pop-up ecosystems.

Property and casualty industry impact

- Demand for insurance products recovers slowly and trust in insurers increases; leads to higher demand, at higher prices, postcrisis, engaging less price-sensitive customers.

- Increased trust in “good companies” results in customers willing to share data more broadly, which gives players who are able to drive insights and value an advantage over competitors.

- Prolonged pandemic leads to a fundamental shift in the balance of power toward larger incumbents as M&A activity starts to become more attractive.

Sunrise in the east

- China and other East Asian nations are more effective in managing the virus and take the reins as primary powers on the world stage.

- Centralized government response becomes the “gold standard.”

Property and casualty industry impact

- Slow recovery and long-term near-zero interest rates result in muted balance sheets and a smaller profit pool, driving increased market consolidation, particularly among small and midsized insurers.

- The largest Asian insurance and technology ecosystem players make plans to penetrate US markets, resulting in exit opportunities for small and midsized insurers.

- Incumbents are forced to adopt digital tech to drive automation and efficiency (roll up and purchase small-to-midsized insurers) to stay competitive in a more global market.

Lone wolves

- Prolonged pandemic period spurring governments to adopt isolationist policies, shorten supply chains, and increase surveillance.

- Economic free fall and social unrest due to prolonged periods of isolation.

Property and casualty industry impact

- Customer loyalty to insurers significantly decreases as customers switch insurers often in search of the best prices and coverage.

- As global trade suffers, commercial exposures flatten and eventually shrink—exacerbating prolonged top-line challenges for carriers; some offset from hardening rates.

- Migration of work to lower-cost locations stalls as trade barriers rise, putting additional pressure on carrier cost profiles.

For an in-depth discussion of scenario planning for leaders, potential implications across three dimensions, and various opportunities and risks.