Will India be insulated against global heat waves? has been saved

Article

Will India be insulated against global heat waves?

India’s growth is now expected to follow an upward trajectory in the year ahead.

The success of the liberalization policy and wide ranging economic reforms that were introduced during the early 1990s put India on an unprecedented growth path. What’s important to acknowledge is that the growth story was built around services rather than manufacturing as had happened in other Asian countries. Another distinctive aspect of the Indian growth story has been its foremost reliance on domestic factors, thereby also helping to limit adversial impact of global developments like the last global financial crisis. The signals of a difficult global environment are visible again and it is important to analyse if India can continue to minimize the impact from global uncertainty, key among them include tightening of global financial conditions, rising protectionist sentiments, increasing trend in commodity especially crude prices, volatile currency markets and fiscal slippages.

After a year of slowdown on account of market disruptive policies, India’s growth is now expected to follow an upward trajectory in the year ahead. Consumption remains the engine of growth and the lead indicators seem to suggest that domestic conditions are showing signs of re-vitality. The policy agenda continues to focus on building domestic infrastructure with more emphasis on increasing the formalization and inclusion within the economy. While externally, protectionism appears to be on the rise, there are strong indications of global demand picking up as well. In an environment of global headwinds to increasing trade, the world economic growth is expected to be 3.9% for both 2018 and 2019, which marks a 0.2 percentage point increase from its last update in October.

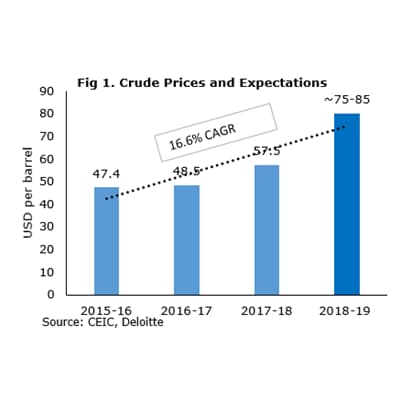

Having said this, India is by no means immune to global risks. A big concern for the economy and all future policy plans is the winding down of era of “low” crude prices. As the chart shows, the crude prices have risen by almost 17% from a level of approx. USD 48 to now in the range of USD 75-80. Such increase in crude prices, where India imports more than 80% of its crude requirement, can likely lead to a general price rise. While India has embarked on a long term vision of shifting to renewable energy sources, in the immediate and short term, imports of oil can be optimized and not minimized. Hence, high inflation is a fear that growing economies cannot ignore. India has won a hard battle to stabilize its macro-economic fundamentals. Therefore, if the crude prices remain elevated, the policymakers may have to make difficult choices wherein short term fiscal expansion may have to be curtailed to keep this hard won macroeconomic stability intact. RBI, recognizing the change, has already increased the repo rate by 25 points and may increase it further during the year if inflationary environment persists.

Separately, factors like the US trade and monetary policy are likely to have a substantial effect. Trade policies that can lead to a full scale tariff war can create disruptions especially for exporters. Coming immediately after the recent regulatory changes in India, the impact, even if it is for the short term, may limit the ability of the Indian exporters to take advanatage of a buoyant global demand. Even if India is not directly involved, any significant trade disputes are likely to have spill over effects on other economies as well.

In terms of the monetary policy, US Fed projections of at least two more rate hikes this year and three next year together with currency weakening can lead to capital being diverted away from emerging economies like India, a scenario which has already started playing out, reflective of global incentives to reroute investments. However to some extent a weakening rupee may help in boosting exports as in real terms, Indian currency is still overvalued as compared to some of its competitors. As can be seen from the chart, the Real Effective Exchange Rate (REER) for India continues to be more than 100.

Given the risks, it should be safe to account for certain domestic and external challenges in advance which can help policymakers, investors, and businesses to better prepare for strategies to mitigate any incoming impact. Important would be to appropriately set fiscal and monetary policy perspectives keeping in mind the fiscal limits while maintaining growth-inflation balance. In this backdrop, it can be rightly argued that India is likely more vulnerable to domestic variations while global uncertainty is likely to largely arise from tightening financial conditions and rising protectionist sentiments. Overall, a lot will depend on the time management with respect to effective implementation of economic schemes.

Information for the editor for reference purposes only

The authors are Anis Chakravarty, Lead Economist and Partner, Deloitte India and Umang Aggarwal, Economist, Deloitte India

Authors