Key operational challenges of IFRS 16 has been saved

Analysis

Key operational challenges of IFRS 16

Are you prepared?

Following the new leasing standard, which came into effect at the start of 2019, what are the main challenges and key points to consider?

Explore Content

- Introduction

- IFRS 16 at a glance

- How will lessees be affected by IFRS 16?

- Transition to the IFRS 16

- Simple worked example

Introduction

A company’s lease obligations, previously lost in the small print of financial statements, are finally being given prominence on the balance sheet, as the new leasing standard became effective 1st January 2019, for both IFRS and US GAAP reporting companies.

Companies that issue interim financial statements should have already transitioned to the new leasing standard, whilst all IFRS reporting companies will soon have to complete their transition, in time for their 2019 annual financial statements to be issued in the first few months of next year.

Ultimately, previously invisible leverage from unrecognised lease obligations will now become visible on the balance sheet, as all lease obligations will be recognised and presented as a liability.

These new liabilities will be offset by a corresponding “right-of-use” asset, representing the value of the lessee’s right to use the leased asset. Furthermore, the subsequent accounting for these new lease liabilities and right-of-use assets will fundamentally change how leases have been accounted for under the old standard.

Therefore, financial statements’ users need to understand how the new leasing standard will affect the financial statements and their resulting financial key performance indicators (KPIs), especially since most companies will not restate prior periods. In addition, banks and regulators would need to understand these changes in KPIs especially when monitoring compliance with debt covenants and other regulatory requirements.

IFRS 16 at a glance

International Financial Reporting Standard 16 (IFRS 16) Leases must be applied by every IFRS-reporting entity, for financial years starting on or after 1st January 2019.

This Standard replaced its predecessor, International Accounting Standard (IAS) 17 Leases. The fundamental change brought about by IFRS 16 affects the majority of lessees. Whereas the previous Standard (IAS 17) required lessees to classify leases as either finance leases (recognised on balance sheet) or operating leases (off balance sheet), IFRS 16 removed this distinction and requires lessees to recognise almost all their leases on balance sheet.

Only certain short-term leases having a lease term of 12 months or less and leases of low-value assets (in the region of USD 5,000 or less, irrespective of how many such leases there are), such as laptops, office printers, mobile phones etc, can be kept off the balance sheet by applying their respective practical expedient in IFRS 16. In these limited instances, their accounting treatment would remain the same as it was under IAS 17.

Therefore, lessees that had operating leases under IAS 17 must bring those leases on the balance sheet upon transitioning to IFRS 16 and this could have a significant impact on their financial statements, compared to what was previously reported under IAS 17.

In contrast, IFRS 16 accounting for lessors remains largely unchanged. The revised definition of a lease may change those contracts considered to be a lease, but otherwise for lessors the finance / operating lease distinctions will remain and IFRS 16 also contains a specific exemption for lessors which value investment properties at fair value, in line with IAS 40. Consequently, the proposed IFRS is not expected to have an impact on the majority of lessors. There are some new requirements for sale and lease back transactions, with the lease back giving rise to an asset, and only a portion of the sale gain reflected. There is also additional guidance for lessees that sublease: the head-lease will give rise to a right of use asset and lease liability, and the sublease will be assessed as finance or operating and the right of use asset retained or derecognised based on the extent to which risks and rewards of the right of use asset have been transferred.

In addition, IFRS 16 adds significantly more disclosures for both lessees and lessors.

How will lessees be affected by IFRS 16?

From a lessee’s perspective, every operating lease existing under IAS 17 must be recognised on the balance sheet as from the date of initial application of IFRS 16. This is achieved by recognising a right-of-use asset and a corresponding lease liability for each such lease. New leases, entered into by lessees after the date of initial application of IFRS 16, must also be recognised on the balance sheet in the same manner upon their commencement date.

Although lessees can opt for the modified retrospective approach and recognise right-of-use assets and lease liabilities initially at equal amounts, KPIs would still be affected, both upon initial application and subsequently.

In fact, following the calculation and recognition of a right-of-use asset (attracting depreciation), and a lease liability (attracting interest), lessees will become more asset-rich as well as more heavily indebted. For individual leases that were previously operating leases, the expense profile will typically shift from being straight-line to front-loaded and boost performance metrics such as Earnings Before Interest Tax Depreciation and Amortisation (EBITDA). This could have a knock-on impact on debt covenants, remuneration schemes, earn-out clauses, regulatory capital and various KPIs.

The table below outlines the expected impact of IFRS 16 on commonly used KPIs for lessee entities that have significant operating leases being recognised on balance sheet upon transitioning to IFRS 16.

Key Performance Indicator (KPI) |

Impact |

Overview |

Interest expense |

Negative |

An interest expense will be incurred at the onset and will diminish over the lease term as it is directly dependant on the outstanding liability. |

Depreciation |

Negative |

Depreciation is charged over the period of the lease term, typically on a straight-line basis. |

Operating expense |

Positive |

The fixed yearly rental expense, previously charged under IAS 17, will no longer be charged. |

Profit Before Tax |

50/50 |

The final result on profit before tax, after taking into account the changes set out above, will result in a front-loaded expense profile in the early years compared to the current straight line approach. The magnitude of this front-loading effect increases if one or more of the following increase: discount rate, lease term and lease payments. |

EBITDA |

Positive |

IFRS 16 will result in an improved EBITDA measure over the life of the lease due to the fact that interest and depreciation charged under the new standard are excluded in this KPI, as opposed to being included within operating expenses under IAS 17. |

Net Assets |

Negative |

Negative impact on net assets due to net liability position over the life of the lease. Since the right-of-use asset is depreciated on a straight-line basis, whilst the lease liability is measured by charging interest on the outstanding balance, the right-of-use asset decreases faster than the lease liability, resulting in a net liability position over the life of the lease. |

Net debt / EBITDA ratios |

Negative |

The impact depends on the remaining duration of the lease (and current leverage ratio). The incremental net debt / EBITDA on the lease liability will generally be high at start of the lease term, gradually decreasing to zero at the end of the lease term. |

IFRS 16 will have no impact on net cash flows, but in the presentation of cash flow statements is likely to lead to an increase in operating cash inflows, with a matching increase in financing cash outflows. Principal payments on leases will be classified as financing activities, and under IAS 7 interest can be classified under operating, investing, or financing cash flows. Payments associated with short-term leases, leases of low-value assets and variable lease payments that are not included in the measurement of lease liabilities remain presented the within operating activities section.

For each lease being recognised on balance sheet, a Right-of-Use asset and a corresponding lease liability are recognised upon commencement of the lease and measured as follows:

Right-of-use asset |

Lease liability |

|

|

Transition to IFRS 16

Furthermore, IFRS 16 must be applied retrospectively i.e. as if it had always been applied. Since this requirement can be very costly to apply, IFRS 16 allows an entity to choose between either the full retrospective or the modified retrospective approach. Whereas under the full retrospective approach no transitional reliefs are available, the modified retrospective approach allows the entity to avail itself from several transitional reliefs. Examples of such reliefs include:

- Applying the definition of a lease under IFRS 16 only to leases entered into on or after the date of initial application of IFRS 16;

- Recognising a Right-of-Use asset equal to the lease liability on the date of initial application of IFRS 16, thus causing no initial impact on net assets; and

- Not restating prior year reported figures.

It is also worth noting that lessees using the modified retrospective approach are required to use the incremental borrowing rate at the date of initial application of IFRS 16 to measure lease liabilities. Therefore, in this case, even if the interest rate implicit in the lease is readily determinable, it should not be used.

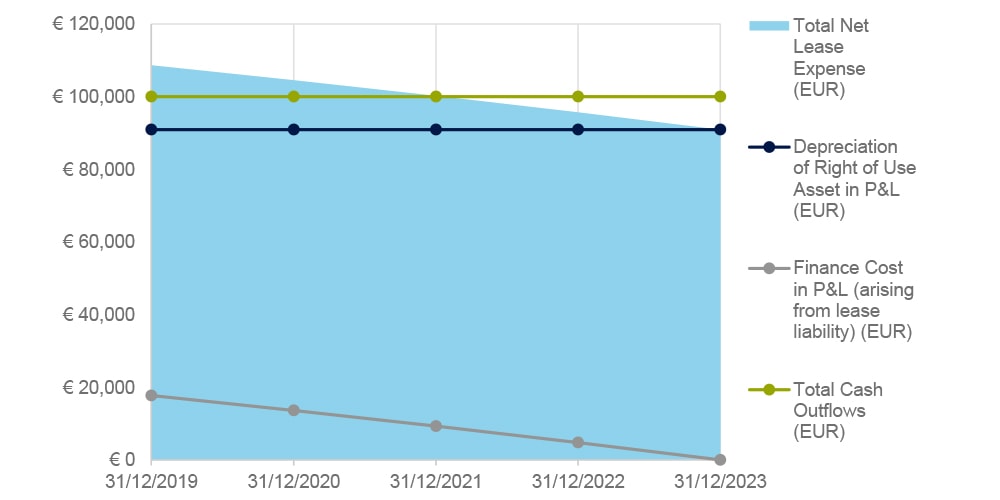

Simple worked example

A lessee enters into a five-year lease of a building, commencing on 1st January 2019. Lease payments are €100,000 per year and are payable in advance on 1st January of every year.

The interest rate implicit in the lease is not readily determinable. The lessee’s incremental borrowing rate is 5% per annum, which reflects the fixed rate at which the lessee could borrow an amount similar to the value of the right of use asset, in the same currency, for the five-year term, and with similar collateral.

The accounting journal entries that would need to be posted to account for this lease on transition to IFRS 16 and at 31st December 2019, are as follows:

IFRS 16 Journal Entries |

|||

Date |

Details |

Debit (EUR) |

Credit (EUR) |

01/01/2019 |

Right-of-use asset a/c |

454,595 |

|

01/01/2019 |

Lease liability a/c |

454,595 |

|

Being journal entry to recognise the right-of-use asset and lease liability upon commencement of the lease. |

|||

01/01/2019 |

Lease liability a/c |

100,000 |

|

01/01/2019 |

Bank a/c |

100,000 |

|

Being journal entry to recognise the first lease payment on 1st January 2019. |

|||

31/12/2019 |

Depreciation expense a/c |

90,919 |

|

31/12/2019 |

Right-of-use asset a/c |

90,919 |

|

Being the first year straight-line depreciation of the right-of-use asset. |

|||

31/12/2019 |

Interest expense a/c |

17,730 |

|

31/12/2019 |

Lease liability a/c |

17,730 |

|

Being journal entry to charge interest on the lease liability for the first year of the lease. |

|||

01/01/2020 |

Lease liability a/c |

100,000 |

|

01/01/2020 |

Bank a/c |

100,000 |

|

Being journal entry to recognise the second lease payment on 1st January 2020. |

|||

The effect of this lease on the Statement of Financial Position and Statement of Comprehensive Income is illustrated below.

The above chart shows that the total expense that ends up being recognised in profit or loss is initially higher and subsequently lower than the straight-lined lease expense, which in this simple example is EUR 100,000 per year.

Key operational challenges in 4 steps

Inevitably, the rather complex lessee accounting requirements introduced by IFRS 16, together with multiple simplification options and practical expedients available, pose significant challenges to the vast majority of entities that are lessees. Furthermore, the added disclosure requirements will affect both lessees and lessors. The list of questions below outline the key operational challenges of IFRS 16.

Step 1: Lease identification

- Do you know which of your contracts are, or contain, a lease?

- Are your systems and processes capturing all the required information?

Step 2: Assess accounting judgements

- Have you considered the impact of changes on financial results and position?

- Do you know what discount rates will you be using for your different leases, and how they should be determined?

- Have you considered the potential use of IFRS 16’s recognition exemptions and practical expedients?

- Do you know what transitional reliefs are available, and whether you will apply any of them?

- Have you planned when you will consider any tax impacts?

Step 3: Communication with stakeholders, technology and leasing strategy

- Are systems and processes capable of monitoring leases and keeping track of the required ongoing assessments?

- Have you assessed the impact of IFRS 16 on your KPIs, compliance with gearing and debt covenants, compliance with other regulations and management compensation?

- Have you assessed the impact of IFRS 16 on business valuations that use the discounted cash flow (DCF) and/or the market approach? Both approaches rely on KPIs that will be affected by IFRS 16, such as Enterprise Value divided by EBITDA, which in the vast majority of cases is expected to decrease.

- Have you considered whether your leasing strategy requires revision?

- How will you communicate this impact to affected stakeholders?

Step 4: Implementation of your IFRS 16 transition project and subsequent maintenance

- Do you have sufficient human resources with the required skills to perform all of the above?

- Have you considered the ongoing maintenance work that will be required after successfully transitioning to IFRS 16?

- Will you be able to successfully transition to IFRS 16 whilst meeting all of your financial reporting deadlines?

How can Deloitte help?

Deloitte Malta Assurance has the necessary skills and experience to assist you in overcoming all the above challenges, leading you to a successful transition to IFRS 16. Some of the services we already provided are training sessions to senior and middle management, development of a complete lease register, impact assessments on primary statements and/or KPI’s, determination of right of use assets and lease liabilities on day one together with journal entries required over the period of the lease, and Excel-based accounting solutions tailored to specific business needs.