Article

Buy Now Pay Later: the Regulatory Landscape in the Asia Pacific Region

05 May 2022

During the COVID-19 pandemic, the Buy Now Pay Later (BNPL) market grew significantly largely due to the boost in e-commerce and digital finance. However, despite the speed, the BNPL market has grown unevenly among Asia Pacific (AP) jurisdictions. According to the Australian Securities and Investments Commission (ASIC), BNPL transaction volumes in Australia increased by 43% during the first year of the COVID-19 pandemic (Figure 1).1 However, in other AP jurisdictions, BNPL transactions only make up a small portion of total consumer transactions.

Figure 1: BNPL Transaction Volume in Australia 2019 -2020

![]()

Source: ASIC

A recent Deloitte blog on the Rise and Evolution of Buy Now, Pay Later noted that the explosion in popularity of BNPL in Australia has seen 'traditional' financial services firms (like banks) rapidly move into the BNPL space, either by introducing their own BNPL offerings or partnering with established BNPL providers, despite initial hesitancy and scepticism about these types of arrangements – giving consumers greater access to a variety of payment methods.

In other AP jurisdictions, BNPL shows strong growth potential but remains at the nascent stage of development. For instance, the Monetary Authority of Singapore (MAS) indicated in its response to the parliament that, compared to other payment methods, BNPL is not yet widely used.2 Whether the Australian phenomenon in BNPL will be replicated in other AP markets remains unclear. Nevertheless, the topic has gained enough traction for regulators to start studying its implications for customer protection.

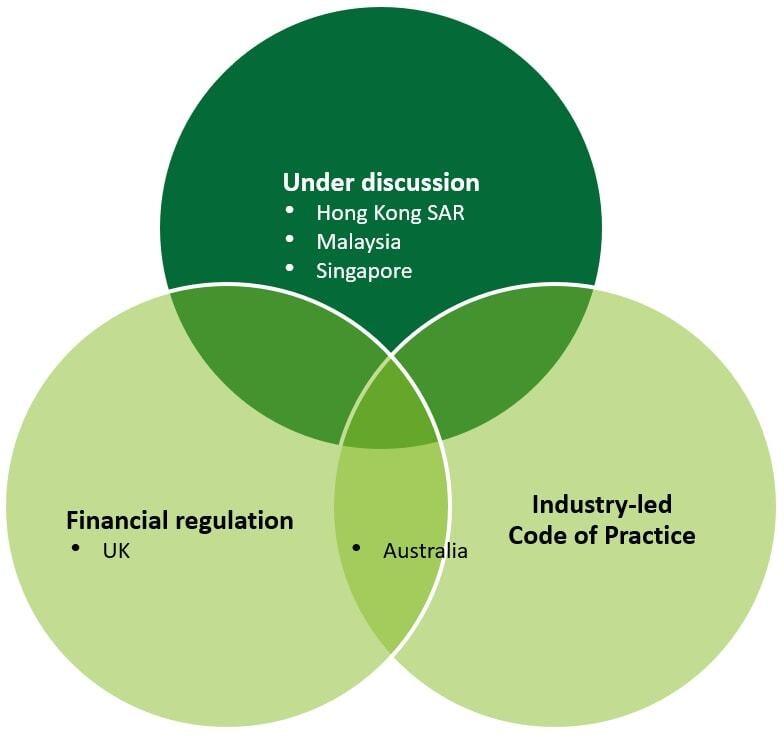

Figure 2: Regulatory landscape in BNPL

Currently, concerns shared by global regulators regarding BNPL primarily revolve around three issues:

- Fairness of BNPL contracts –consumers may not understand the contractual terms of unregulated BNPL products;

- Consumer leverage – the potential to put consumers overly in debt when using more than one BNPL product; and

- Product suitability – the compressed timeline when entering a BNPL contract hinders the BNPL provider's ability to conduct thorough creditworthiness and affordability assessment of the consumer.

Without proper regulation, the rapid evolution of BNPL business models and the fast expansion of the market could potentially create additional risks for consumers, such as misuse of customer data and the lack of support for vulnerable customers or customers experiencing financial difficulties. As a key part of the overall effort to strengthen retail payments regulation, regulators have started to study the BNPL business model and its customer protection implications.

Actions taken by regulators

Given the similarities between BNPL and products such as credit cards, a long-standing debate over BNPL regulation is whether it should be considered and regulated as consumer credit. Consumer Credit Regulations (CCR) usually require a thorough creditworthiness assessment to be conducted by the credit provider to prevent the consumer from over-indebtedness. CCR also protects consumers by providing guidelines on product suitability and treatment of customers in financial difficulty. As BNPL developments continue to gain momentum, whether BNPL providers and products should be subject to CCR is being considered by regulators in different jurisdictions, and different approaches are being taken.

1. BNPL-related consumer credit regulation

The international regulatory framework for BNPL arrangements is not uniform. In most cases, BNPL remains outside of consumer credit laws. A few regulatory developments in consumer credit regulation are taking place in more developed BNPL markets, such as the UK and Australia. In Australia's case, BNPL is not regulated under the National Consumer Credit Protection Act 2009, as certain short term loans are exempt from credit licensing.3,4 However, it is regulated as consumer credit under the Australian Securities and Investments Commission Act 2001.5 This means that ASIC has product intervention powers that allow the regulator to intervene when concerns arise relating to significant consumer detriment. Looking outside the AP region, the UK’s Financial Conduct Authority (FCA) has made substantial progress in rule-making, by issuing a consultative version of Regulation of Buy-Now Pay-Later in October 2021. This consultative Regulation re-examined BNPL-related exemptions in the Consumer Credit Act 1974 (CCA). Additionally, in February 2022, the FCA drove changes to BNPL firms' contractual terms due to concerns relating to the fairness of BNPL contracts. By including BNPL products in the scope of CCR, regulators are asking BNPL providers to better manage the credit risk that comes with the borrower's lack of ability to repay, as well as protect consumers from the risks of over-indebtedness and unsuitable products.

2. Policy measures under discussion

Regulators in jurisdictions where the BNPL market has just started to take shape are at the beginning stage of policy discussion. The Hong Kong Monetary Authority (HKMA) announced in its 2022 Work Priorities that it will enhance consumer protection on innovative products, including BNPL products.6

In October 2021, the Monetary Authority of Singapore (MAS) addressed questions from the parliament regarding the regulatory framework on BNPL. MAS noted in the response that currently BNPL operators have instituted their own measures to prevent over-indebtedness, such as credit limits. However, given the growth potential of the BNPL market in Singapore, MAS will continue to evaluate the need for a tailored regulatory framework to mitigate potential risks. Under MAS’ guidance, the Singapore Fintech Association has launched a BNPL Working Group to develop a code of conduct for all BNPL operators.

Another example is Malaysia. The Malaysian Central Bank, Bank Negara Malaysia (BNM) announced that they will pass a consumer credit act in 2022 to strengthen consumer credit activities including BNPL.7

In some jurisdictions, regulation on BNPL products has not been discussed but can be expected down the road. For example, although BNPL products have not been widely used in Mainland China, regulators in recent years have started to strictly regulate digital finance platforms, some of which provide interest-free short-term financing similar to the BNPL model. It is reasonable to expect the same level of scrutiny to be applied to the BNPL products when they emerge in the Mainland China market.

Development of industry-led codes of practice

In the absence of laws and regulations in the BNPL space, certain jurisdictions have taken the initiative to explore self-regulation mechanisms to show their good faith in consumer protection, and to support the growth of the BNPL market. This approach aims to address the same risks as CCR, but on a voluntary basis. This approach to self-regulation has been adopted in Australia, and is now being explored by Singapore.

The Australia Finance Industry Association (AFIA) launched a voluntary Code of Practice, the AFIA Buy Now Pay Later Code of Practice,8 for BNPL product providers in March 2021. This Code of Practice sets out nine high-level customer commitments for signatories to make to ensure customer protection. Similarly, a voluntary code of practice is being developed by the industry in Singapore. Ongoing discussion on this code of practice includes the following considerations:

- Disclosure and fair marketing requirements, which will support customers to make informed decisions on whether to take on BNPL products;

- Introduction of age limits for taking up BNPL products, to prevent minors from taking on credit;

- Introduction of credit limit to prevent overleverage;

- Suspension of accounts following missed payments, to prevent accumulation of further;

- Credit information sharing to facilitate a holistic view of customers’ finances; and

- For interest charges and other fees, an option being considered is to ban interest charges and to put a cap on other fees, in order to keep the BNPL product simple and avoid the accumulation of fees and charges.

Both the AFIA BNPL Code of Practice and the Singapore Code of Practice initiative focus on ensuring the BNPL product is suitable, fair, and transparent for customers.

Whilst consumer credit has been available in many different forms, the emergence of BNPL has seen many regulators reconsider whether existing CCRs remain appropriate for this new breed of products, and how regulation may need to shift to ensure consumers remain protected against new risks arising from the rapid growth and uptake of BNPL. However, as noted above, certain jurisdictions are not waiting for the advent of new regulation, instead choosing to move forward with self-regulation through the adoption of voluntary codes of practice, which focus on consumer protection, whilst leaving enough flexibility for innovation.

It is an exciting time in financial services, and firms will need to ensure the desire to innovate and create new product offerings is balanced with, and appropriately considers regulator’s expectations relating to fair treatment of consumers, suitability of products, and credit risk management.

[1] Australian Securities and Investments Commission, ASIC tips for making the most of buy now pay later, 28 April 2021

[2] Monetary Authority of Singapore, Reply to Parliamentary Questions on Buy Now Pay Later Schemes, 5 October 2021

[3] According to the National Consumer Credit Protection Act 2009, short-term loans with fees charged up to 62 days do not exceed 5% of the loan amount and 24% per annum interest are exempt from credit licensing.

[4] Australian Securities and Investments Commission, 19-250MR ASIC makes product intervention order banning short term lending model to protect consumers from predatory lending, 12 September 2019

[5] Australian Securities and Investments Commission, BNPL: An industry Update, 16 November 2020

[6] Hong Kong Monetary Authority, Hong Kong Banking Sector 2021 Year-end Review and Priorities for 2022, 26 January 2022

[7] Ministry of Finance Malaysia, Bank Negara teams up with MoF, SC to regulate BNPL schemes, 30 March 2022

[8] Australian Finance Industry Association, Code of Practice for Buy Now Pay Later Providers, March 2021

Back to the Main page.