European football scores $30 billion Foi salvo

Previsões

European football scores $30 billion

TMT Predictions 2016

Executive summary

Deloitte Global predicts that the European football market may generate $30 billion (€27 billion) in revenues in 2016/2017, an $8 billion (€7 billion) increase relative to 2011/2012, and a compound annual growth rate of seven percent. Most of this growth will likely be driven by the five largest leagues: England’s Premier League, France’s Ligue 1, the German Bundesliga, Italy’s Serie A and La Liga in Spain.

Football’s revenues have been increasing consistently and impressively over the past few decades; but it is only recently that revenue growth has stayed ahead of costs, with improved cost discipline being implemented across the game. This improved cost management, combined with continuing broadcast and commercial growth, looks likely to make football clubs increasingly profitable. They are therefore attractive to investors looking for a consistent financial return, as well as those interested in building profile or business opportunities through acquiring a trophy asset football club.

Football and pay television have had an increasingly symbiotic relationship over the past two decades, and forecast 2016/2017 revenues attest to this. Football’s revenues are predominantly made up of matchday (admissions and hospitality), commercial income and broadcast revenues, and it is this latter source which is forecast to generate both the majority of total revenues and the increase in revenues in 2016/17.

The 2016/2017 season will see new broadcast deals for both the English Premier League (EPL) and Spain’s La Liga come into effect. Domestic live broadcast rights is expected to generate an average of $2.6 billion for the EPL for the three seasons from 2016/2017, a 71 percent increase on the prior agreement. Spain’s La Liga, which has recently moved to a collective broadcast rights selling model, is expected to earn approximately $1.1 billion per season from domestic live rights. These are the two biggest drivers of revenue growth in the European football market.

It is not just from domestic markets that Europe’s top leagues are achieving substantial growth in broadcast rights fees. The EPL and La Liga’s international rights fees have been climbing fast too. In the 2016/2017 season the EPL is expected to generate over $1.5 billion from overseas broadcast rights, a gain of at least 40 percent compared to the previous rights cycle. La Liga generates less than half this amount, but has achieved substantial recent growth, and generates the second-highest broadcast revenues from non-domestic markets of any sports league.

In the long run, there is a virtuous circle within football. The more revenues a club can generate, the more money it has to invest in talent, increasing the chances of on-pitch success, with the associated financial rewards allowing it to reinvest. This creates an imperative for clubs, and the leagues of which they are a part, to maximize their revenues. More revenue should enable clubs to recruit not just the best talent and coaches on the field, but also the best commercial staff, access to the best technology, and also the ability to invest for the long term, for example by investing in youth academies. The more popular football becomes, the more brands will likely want to be associated with it.

European football scores $30 billion

1 For a complete list of references and footnotes, please download the full PDF version of the TMT Predictions 2016 report.

Deloitte Global predicts that the European football market may generate $30 billion (€27 billion) in revenues in 2016/2017, an $8 billion (€7 billion) increase relative to 2011/2012, and a compound annual growth rate of seven percent.

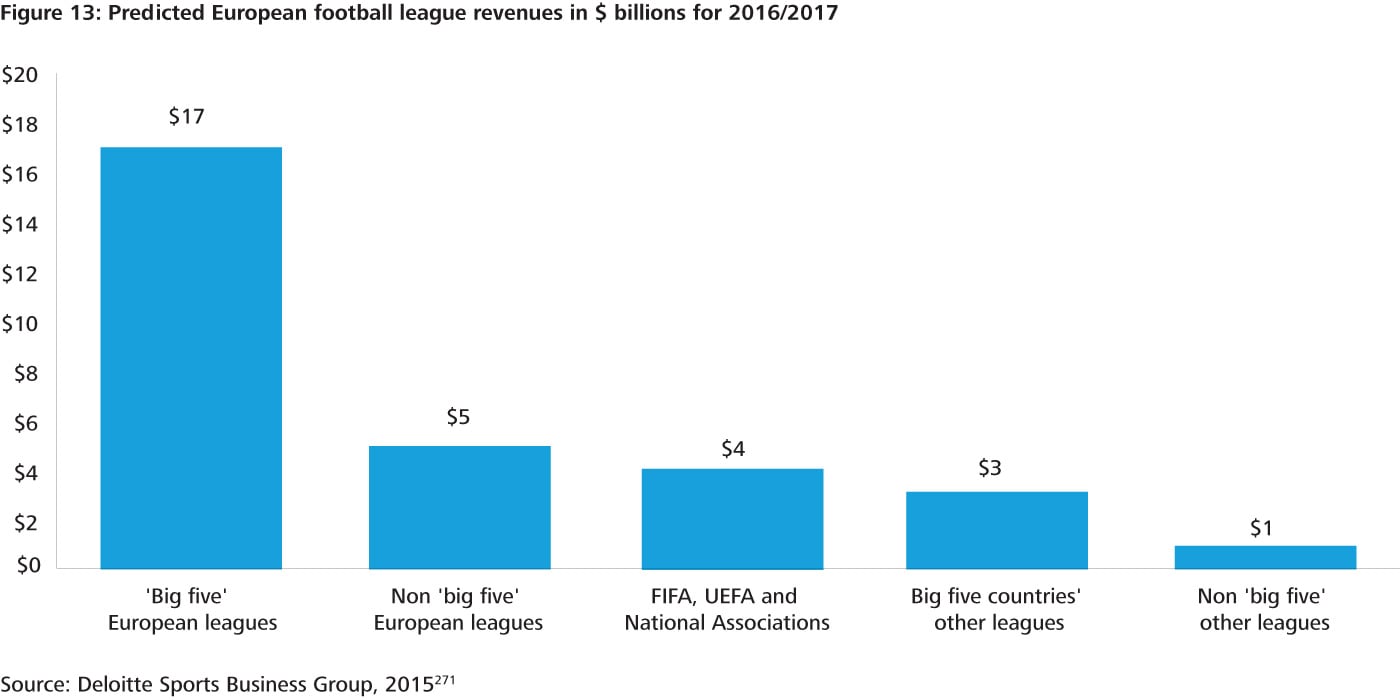

Most of this growth will likely be driven by the five largest leagues (England’s Premier League, France’s Ligue 1, the German Bundesliga, Italy’s Serie A and La Liga in Spain) whose share of revenues continues to rise. These leagues are expected to generate approximately $17 billion (58 percent) of total revenues in 2016/17.

Football and pay television have had an increasingly symbiotic relationship over the past two decades, and forecast 2016/2017 revenues attest to this. Football’s revenues are predominantly made up of matchday (admissions and hospitality), commercial income and broadcast revenues, and it is this latter source which is forecast to generate both the majority of total revenues and the increase in revenues in 2016/17.

The 2016/2017 season will see new broadcast deals for both the English Premier League (EPL) and Spain’s La Liga come into effect. Domestic live broadcast rights is expected to generate an average of $2.6 billion for the EPL for the three seasons from 2016/2017, a 71 percent increase on the prior agreement. Spain’s La Liga, which has recently moved to a collective broadcast rights selling model, is expected to earn approximately $1.1 billion per season from domestic live rights. These are the two biggest drivers of revenue growth in the European football market.

Source: Deloitte Sports Business Group, 2015

Both the UK and Spain are now relatively mature pay-TV markets for football, with 17.4 million pay-TV homes in the UK (65 percent of all households) and 5.4 million (29 percent) in Spain. Live rights to premium content such as top-tier domestic league football provides regular content through most months of the year, and hence is highly attractive to pay-TV operators in driving subscriptions.

It is not just from domestic markets that Europe’s top leagues are achieving substantial growth in broadcast rights fees. The EPL and La Liga’s international rights fees have been climbing fast too. In the 2016/2017 season the EPL is expected to generate over $1.5 billion from overseas broadcast rights, a gain of at least 40 percent compared to the previous rights cycle. La Liga generates less than half this amount, but has achieved substantial recent growth, and generates the second-highest broadcast revenues from non-domestic markets of any sports league.

There is global interest in football’s top leagues and clubs at many levels, from broadcast interest to shirt sponsorship and ownership. In the EPL, over half of the 20 clubs have non-UK owners and the principal sponsor of three-quarters’ of the teams is headquartered abroad, with many based in Asia Pacific and the Middle East.

Combined revenues of the 20 EPL clubs are predicted to surpass $6.5 billion in 2016/17, more than double that of the next-highest European league. The EPL has for many years delivered strong matchday, commercial and broadcast revenues and the core reasons for the EPL’s continued revenue leadership are: its substantial broadcast revenue advantage, aided by highly successful centralized sales and marketing; global talent; competitive matches throughout the league; full stadia; and strong history and heritage. The EPL has for many years delivered strong matchday, commercial and broadcast revenues.

EPL clubs are reaping the returns from heavy investment in venues and facilities over the last 20 years. League attendance averages over 95 percent of stadium capacity. Commercial revenues are now the highest of any European league, driven particularly by lucrative deals secured by the league’s largest clubs, which have global appeal and resonance. For example, Manchester United’s ten-year kit deal with Adidas is worth a minimum of $114 million (£75 million) per season.

While the EPL’s financial prowess may not have been matched by its on-pitch success in European club competitions, in recent seasons their widening revenue advantage has given clubs the clout to bid for the top global playing talent, possibly squeezing out other European clubs.

Football has long been about supporters at every level, and owning a football club has to some extent been the ultimate collectable. The game’s rising revenues, and its universal appeal, make it highly attractive to investors.

The game changer is the recent trend for top clubs, in the EPL in particular, to be able to generate a profit. Historically, revenue growth has been outstripped by cost increases, with football’s greatest challenge being its ability to balance the books. Recent years have seen the development, implementation and subsequent benefits of cost control regulations within the game, indicating that this could be the most significant football business development since the Bosman ruling on player transfers. The early signs are that this is the case, with Premier League clubs returning collective pre-tax profits in 2013/14 for the first time since 1998/99. This has made the sport and its clubs an increasingly attractive investment, both for individuals seeking prestige and for financial buyers looking for a return on their investment.

Further purchases of leading European football teams, in part or whole, are likely in 2016 and beyond. In late 2015, Chinese investors paid $400m for a 13 percent shareholding in City Football Group, which owns EPL club Manchester City and football clubs in Melbourne and New York, as well as a shareholding in a club in Yokohama. As of end-2015, only one Premier League club, Leicester City, was majority-owned by Asia Pacific-based investors: we expect this to increase.

Chinese investors have been building their football investments within their home country and abroad. One investor in Manchester City, China Media Capital (CMC) also spent $1.3 billion to secure global broadcasting rights for the Chinese Super League for five years from 2016. Earlier in 2015 Dalian Wanda, a Chinese conglomerate, bought a $50million (€45million) stake in Atlético de Madrid, as well as acquiring global sports marketing company Infront Sports & Media, which holds commercial rights to the Chinese Super League. Full ownership of a Premier League club by a Chinese investor may only be a matter of time.

A quarter of EPL club owners are from North America and the EPL has secured a six-year $1 billion broadcast deal with NBC from 2016/17, highlighting its growing prominence in the US. Further evidence of football’s growing value in the US market are the sell-out crowds for pre-season matches involving European clubs, and also the carefully-managed development of the MLS. The US generates the highest individual broadcast rights fee for the World Cup of any territory, and US fans were the largest contingent of travelling fans for the last World Cup.

Bottom line

Football’s revenues have been increasing consistently and impressively over the past few decades; but it is only recently that revenue growth has stayed ahead of costs, with improved cost discipline being implemented across the game. This improved cost management, combined with continuing broadcast and commercial growth, looks likely to make football clubs increasingly profitable. They are therefore attractive to investors looking for a consistent financial return, as well as those interested in building profile or business opportunities through acquiring a trophy asset football club.

In the long run, there is a virtuous circle within football. The more revenues a club can generate, the more it has to invest in talent, increasing the chances of on-pitch success, with the associated financial rewards allowing it to reinvest. This creates an imperative for clubs, and the leagues of which they are a part, to maximize their revenues. More revenue should enable clubs to recruit not just the best talent and coaches on the field, but also the best commercial staff, access to the best technology, and the ability to invest for the long term, for example by investing in youth academies. The more popular football becomes, the more brands will likely want to be associated with it.

Europe is currently football’s financial powerbase, with leagues and clubs continuing to explore how to capitalize on their global appeal through a variety of strategies – broadcasting and distribution of content, sponsorship, other commercial partnerships, shareholdings, talent development and matches abroad. It is established practice for top European clubs to play pre-season matches in non-European markets. This trend is likely to increase, and it seems only a matter of time before a European League stages regular season matches outside of the continent, in a similar manner to how the NFL has staged matches in London and the NBA in Europe.

As long as imported European content retains popularity, leagues and clubs outside of Europe face the challenge of developing their own competition structures. This challenge should be embraced, with these leagues and clubs building strong governance and administration structures, facilities, youth development and community engagement in their local markets, while leveraging best practice from Europe.

Commentators may question whether football’s revenues can continue to grow. We would not expect the 2016/2017 revenue growth rate to continue in 2017/2018: there are no major new broadcast or sponsorship deals likely to start in that period which would generate the same uplift as the new EPL and La Liga deals will do in 2016/2017.

But in the long term, prospects look favorable as long as football maintains its ability to remain a spectacle that can attract a large proportion of the population, almost every week of the year, and which plays out not just on our television screens, but also through online news sites on the web, on social networks, on video games, in the back pages of newspapers, over breakfast, in school break times, and indeed in almost every other medium.

@DeloitteTMT