Perspectives

Digital Banking Maturity 2024

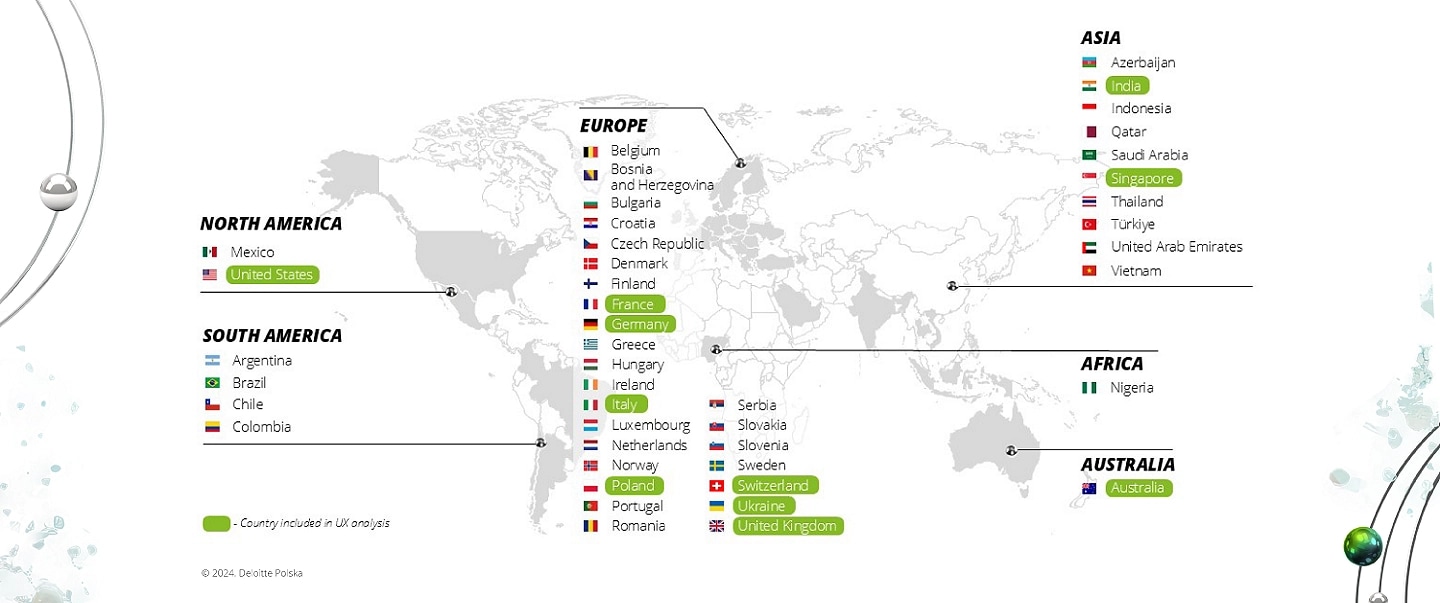

The biggest global digital banking study

We have analysed 1,005 functionalities divided into six paths:

- Availability of information

- Opening an account

- Introducing a customer

- Everyday banking

- Non-banking services

- Customer experience

- Closing an account

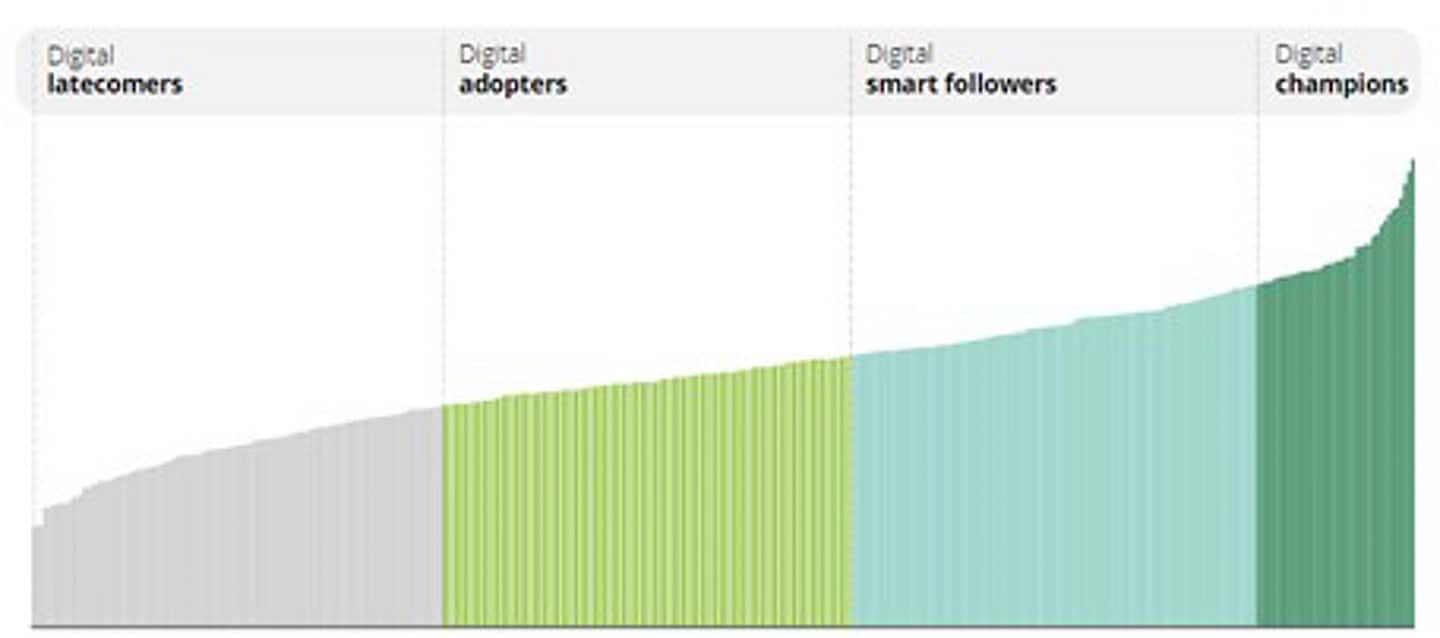

Each path has been evaluated and assigned a determined score. Based on the total scores, a global ranking of Global Digital Champions has been prepared. The group includes 10% of all banks that won the highest scores in our questionnaires.

Moreover, as we operate on the global level, we were able to determine key development directions of cyberbanking and global best practices.

What makes Digital Banking Maturity 2024 report special? We follow leading digital banking trends, focusing strongly on user experience, fully digitalised processes and banking as an auxiliary services platform. While the preceding edition, DBM 2022, focused on a material growth in the number of functionalities offered by banks in digital channels, with the pandemic acting as a strong trigger, the current one, Digital Banking Maturity 2024, indicates a significant trend observed among digital leaders to focus on key processes and functionalities, with significantly stronger emphasis on hyper personalisation and remodelling of digital channels to ensure best customer experience.

Key survey conclusions:

- When analysing the outcome of DBM 2022 and 2024, we notice that banks have shifted focus from developing new functionalities in digital channels to investing in personalised customer experience. COVID-19 pandemic with its frequent lockdowns increased banks’ motivation to provide customers with full service in digital channels. At present, however, we can observe a slowdown of this trend. Much more emphasis is put on the improvement of digital experience through redesigning channels used to reach customers, since most functionalities have been already implemented by banks, especially by the best ones. The strategic change indicates that the refinement of interfaces, simplification of processes and making digital banking more intuitive may significantly improve customer satisfaction and involvement. Thus, in the current banking landscape, customer experience is most important. Attention is focused on the upgrade and refinement of the existing functionalities; those less used or obsolete are withdrawn.

- The current edition of the report, Digital Banking Maturity 2024, indicates that banking leaders concentrate their activity on two key areas. The first group is involved in generating outstanding value for customers, offering them with a full range of key banking operations and fulfilling all financial needs, at the same time providing perfect user experience. The intuitive design and smooth interactions are prioritised in order to ensure customer satisfaction. The other group focuses on adding many new functionalities and to provide comprehensive “super applications” that meet a broad range of needs on a single platform. Both strategies aim at strengthening their positions as digital banking leaders.

- Currently banks apply a variety of methods to support, develop and educate their customers. Using Personal Finance Management tools, they help their clients to effectively manage their funds. Additionally, they utilise personalised content and messages to adjust banking experience to individual needs. Besides, banks provide their customers with valuable advice prompting well-balanced finance management. These initiatives are intended to increase customer awareness, competencies and satisfaction, enhance relations between banks and their customers, improve loyalty and increase the frequency of use of digital banking channels.

- Despite fast development of digital channels observed in the past, certain areas, such as digital mortgage, have not been addressed. Formerly ignored, now they are in the focus of current development initiatives. Although the process is often accompanied by manual analyses and real-world interactions, many supporting functionalities are introduced to digital channels throughout the customer journey, beginning from the development of the funding need, all the way through long-term post-sales support.

- While in the former edition of the report banks seemed to focus on the development of digital banking addressed to customers, now checking cost optimisation opportunities is of key importance. Although improved customer experience remains crucial, efficiency of operations and cost reduction are necessary for sustainable growth. Increasing efficiency and using new technologies, such as GenAI, to reduce costs, banks may remain competitive at the same time ensuring long-term financial health. Maintaining a good balance between innovation and cost management is the key to success in the changing financial landscape.

Contact

Recommendations

Deloitte Center for Regulatory Strategy

Our Center for Regulatory Strategy has the insights to help financial services leaders stay ahead of an active regulatory slate.

Banking and capital markets regulatory trends

Insights to guide your strategic decisions