Solutions

Warning indicator in tax inspection – verification of the personal tax situation (VSFP)

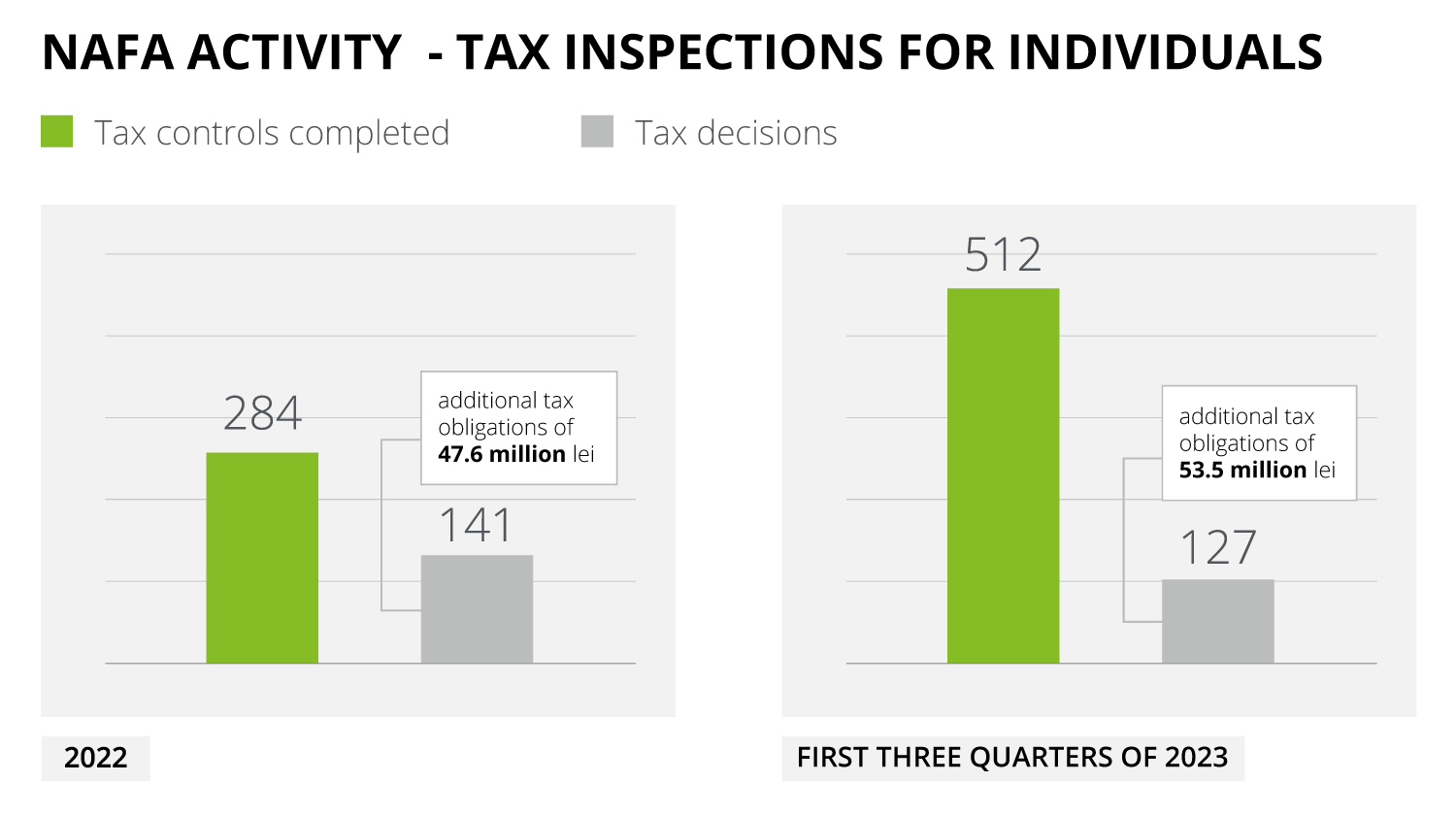

The increase in the control activity on individuals seems to have exceeded the stage of cyclical declarations and becomes reality, at least if we look at the tangible data published by the National Agency for Fiscal Administration (ANAF) and compare the activity in 2022 with the first three quarters of 2023.

What does the image of this amplification show us? Of course, a first answer would be that it is the natural mission of an institution such as ANAF to collect more revenues to the state budget and to use tax inspections as an essential tool in tax compliance, so important for ensuring equity. At the same time, this is probably also because there is a diversification of individuals' income sources (along with the lack of a dictionary to define them, from influencing income to crypto income) as well as because there have been increasingly pronounced inaccuracies between the declared income and those estimated by ANAF.

However, this image shows us something more if we place it on the background of a series of legislative changes and the noticeable change in the approach of tax inspection teams during controls. Namely, that ANAF's pronounced degree of intentionality regarding the increase of tax compliance at the level of individuals will become more visibly in the coming period.

In this context, we recall that, at present, individuals may be subject to:

- a check of the personal tax situation – the equivalent of a tax inspection for companies;

- a desk check – which may also be carried out by the Directorate-General for Tax Anti-Fraud.

However, the most recent changes made in 2023 targeting individuals cover:

- the express introduction in an ANAF Order of the criteria for classifying taxpayers as high net worth individuals subject to certain alternative treatments to increase voluntary tax compliance;

- increasing the tax rate on income obtained from unidentified source from 16% to 70%.

In this context, we believe that a high knowledge is needed not only of how to report income for individuals, but also of what a personal tax control entails in practice, how it should be addressed, what the implications are once subject to such an verification, what problems it can generate, but also how these can be prevented or remedied.

For details on this subject please contact us.

Contact:

- Raluca Bontaș - Tax Partner, Deloitte Romania

- Alex Slujitoru - Partner, Reff & Associates | Deloitte Legal

- Emanuel Bondalici - Senior Managing Associate, Reff & Associates | Deloitte Legal

- Cătălin Barbu - Manager, Global Employer Services

- Răzvan Brătilă - Managing Associate, Reff & Associates | Deloitte Legal