Regulatory posture on social media advertising and finfluencers has been saved

Article

Regulatory posture on social media advertising and finfluencers

28 June 2022

In our previous blog of the New Market Entrants series, we discussed the risks that social media and finfluencers pose to consumers and financial stability. In this instalment, we will zoom in on social media content relating to financial products and services, the concerns shared by regulators across the region regarding such content, and how regulators are taking actions to protect consumers from risks arising from ‘finfluencers’.

Social media content containing advertisements for financial products, including crypto-assets

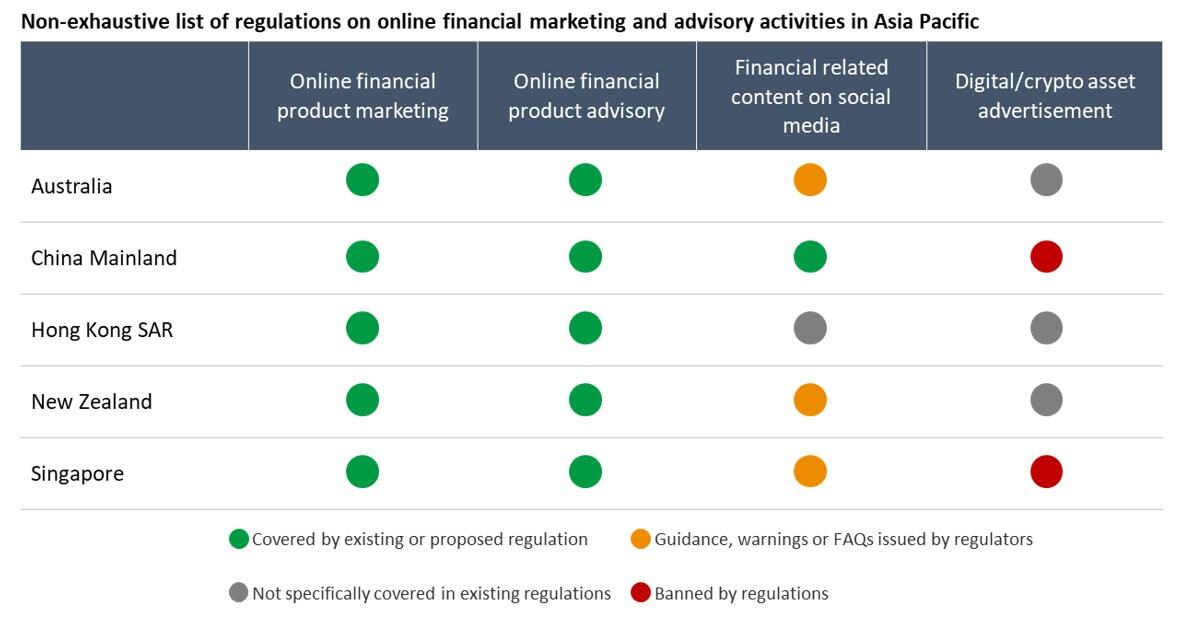

Existing laws on customer protection, advertisement, and intellectual property rights protection are generally applicable to marketing activities on social media. Violations of these laws could potentially lead to civil and even criminal charges against the individual or company that posted the advertisement.

Social media content will generally be considered a commercial advertisement if the content mentions specific product names and features, or the content creator receives a commission from the product provider. As financial products can pose risks to the financial well-being of consumers, most regulators believe they should be advertised with prudence and clarity. To that effect, some AP regulators have taken the initiative to develop and implement regulations targeting the online promotion of financial products. On 31 December 2021, seven regulators from various sectors in China Mainland jointly issued a consultation on the online marketing of financial products, laying out detailed regulatory requirements for online marketing of financial products through all online channels including social media.i This is a major step taken by the Chinese regulators to tackle key concerns around online financial product marketing, including illegal financial product marketing, misleading consumers, and unfair competition. This is also an example of cross-sectoral collaboration in regulating online financial product marketing activities.

Promotion of complex financial products or high-risk products through online distribution and advertising channels is more closely scrutinized by regulators given the potential for large financial loss they may cause the investing public. In some cases, advertisement of investment products bearing high risks can be subject to stricter limitation. For example, in January 2022, the Monetary Authority of Singapore (MAS) banned digital token providers from advertising their products in public and on media, as a means to protect the general public from risks associated with cryptocurrency trading.ii

Social media content containing financial or investment ‘advice’ to viewers/followers

This form of social media content does not fall under the advertisement category as the content creator is generally not receiving any commission directly from the product provider. Instead, the content creators discuss financial products to share their knowledge on finance and investment or simply share their personal experience with certain financial products.

As discussed in the previous blog, financial or investment advice is strictly regulated across jurisdictions. When an activity is defined as providing financial advice, a license, registration, or exemption with the relevant regulator will be required. Such financial advisors will need to comply with regulations regardless of how the advisory service is being performed. For example, the Securities and Futures Commission of Hong Kong (SFC) Guidelines on Online Distribution and Advisory Platforms explicitly stated that any licensed financial advisor will be held accountable through all channels including social media.iii However a majority of the social media influencers are not licensed financial advisors, and are therefore not in compliance with these guidelines.

Financial regulators have started to provide guidance to social media content creators on how to produce content that is not "financial advice". The Financial Market Authority (FMA) of New Zealand issued a Guide to Talking About Money Online in January 2021, to provide tips for both consumers and social media influencers engaging in related activities to better manage the risks.iv On 28 October 2021, the European Securities and Markets Authority (ESMA) issued a Public Statement on Investment Recommendations Made on Social Media, clarifying the definition of investment recommendations, how to post them properly on social media, and laying out the consequences of breaching the EU Market Abuse Regulation.v In the AP region, some regulators are taking a similar approach. In March 2022, Australian Securities and Investments Commission (ASIC) issued an information sheet (INFO 269) for social media influencers who discuss financial products and services in their content. The information sheet focuses on relevant laws and requirements and provides case studies and examples of potential violations.vi This approach discourages finfluencers who are not licensed financial advisors from creating finance-focused posts by warning against the potential breaches of the Corporations Act 2001, which imposes severe imprisonment and financial penalties. Similarly, MAS has warned social media content creators against posting false or misleading statements and other activities that may constitute market abuse under securities laws.vii

Although action is being taken by regulators to tackle risks arising from the above-mentioned activities, several issues remain. Firstly, education on basic financial knowledge and typical frauds and scams is critical for the general public. While a number of financial regulators have already issued various warnings on suspicious activities, further educational efforts may be necessary to reach more consumers. Secondly, similar to other topics that emerged with the increased use of the internet such as cryptocurrency trading, activities of concern are usually not tied to jurisdictional boundaries. In this case, fragmented legal and regulatory requirements across jurisdictions could lead to regulatory arbitrage. For example, an influencer violating regulations in one jurisdiction could post the video from an IP address in another jurisdiction that has less stringent rules. In other cases, rules that are appropriate in one jurisdiction may be less appropriate, if relevant at all, in another jurisdiction. Last but not least, the algorithms used by social media platforms also come into play. For instance, someone who viewed one finance-related content post or searched finance-related keywords could get frequent recommendations for similar content. The information cocoon created by algorithms could reinforce social media’s influence on an individual’s financial decisions.

It is clear that social media and 'finfluencers' are having an increasing impact on the decision-making process of individuals. While finfluencers can play a positive role in improving the financial literacy of the general public to a certain degree, they also pose a number of risks to consumer protection and financial stability – two key focus areas of financial regulators. Although guidelines on finfluencers in different AP jurisdictions continue to evolve at different paces, a foreseeable common trend is that provision of financial advice in any shape or form will be limited to qualified professionals. Cross-sectoral collaboration will also be needed to mitigate risks to consumers and the financial market. We will explore this topic in more detail in future ACRS publications.

References:

i. People's Bank of China, Consultation on Measures to Regulate Online Marketing of Financial Products, 31 December 2021

ii. Monetary Authority of Singapore, Guidelines on Provision of Digital Payment Token Services to the Public [PS-G02], 17 January 2022

iii. "[…] The Securities and Futures Commission (SFC) will take into account activities targeting Hong Kong investors conducted by a licensed or registered person via all channels in their totality in considering the licensed or registered person’s compliance with the requirements in these Guidelines." Hong Kong Securities and Futures Commission, Guidelines on Online Distribution and Advisory Platforms, July 2019

iv. Financial Market Authority, A guide to talking money online, 28 June 2021

v. European Securities and Markets Authority, ESMA’s Statement on Investment Recommendations on Social Media, 28 October 2021

vi. Australian Securities and Investments Commission, Discussing Financial Products and Services Online, March 2022

vii. MAS and SGX: Beware of risks related to trading incited by online discussions

Back to the Main page.