OECD Pillar One and Pillar Two tax advisory service

An integrated approach to help you evaluate potential impact

What is Pillar One and Pillar Two?

The OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (BEPS) recently endorsed the key components of the two-pillar approach to international tax reform. The agreement has set an ambitious and challenging timeline for both Pillars and whatever the final rules, most global businesses of any scale are likely to be impacted.

Pillar One: Nexus and profit allocation rules

Pillar One targets the largest multinational groups focusing initially on those with at least EUR 20 billion of consolidated revenue and net profits of over 10% (i.e., profits before tax to revenue) and will require them to pay tax in the locations where their customers and users are located. A formulaic approach will be used to allocate a percentage of profits between each jurisdiction. Pillar One should effectively require in scope multinationals to pay at least some tax in the markets they interact with.

Pillar Two: Global minimum tax

Pillar Two, the key components of which are commonly referred to as the "global minimum tax" or "GloBE", introduces a minimum effective tax rate of at least 15%, calculated based on a specific ruleset. Groups with an effective tax rate below the minimum in any particular jurisdiction would be required to pay top-up tax in their head office location or in the location of other affiliates. The tax would be applied to groups with revenue of at least EUR 750 million, making it far more widely applicable than Pillar One.

What is Deloitte's OECD Pillar One and Pillar Two modeling service offering?

Deloitte’s OECD Pillar One and Pillar Two modeling service offering combines the deep expertise of Deloitte tax specialists with the analytical power of our technology solution to help companies assess and evaluate the potential implications of Pillar One and Pillar Two on their tax profile.

Benefits

Evaluate the impact of the OECD’s Pillar One and Pillar Two proposals

Perform accurate compliance calculations post-enactment

Identify data limitations that may need to be considered for compliance

Customize to your fact pattern and data sources

How it works

Assess the impact of Pillar One and Pillar Two

Use the inbuilt calculator to calculate the tax impact of Amount A and relocate a share of residential profit to your market jurisdictions.

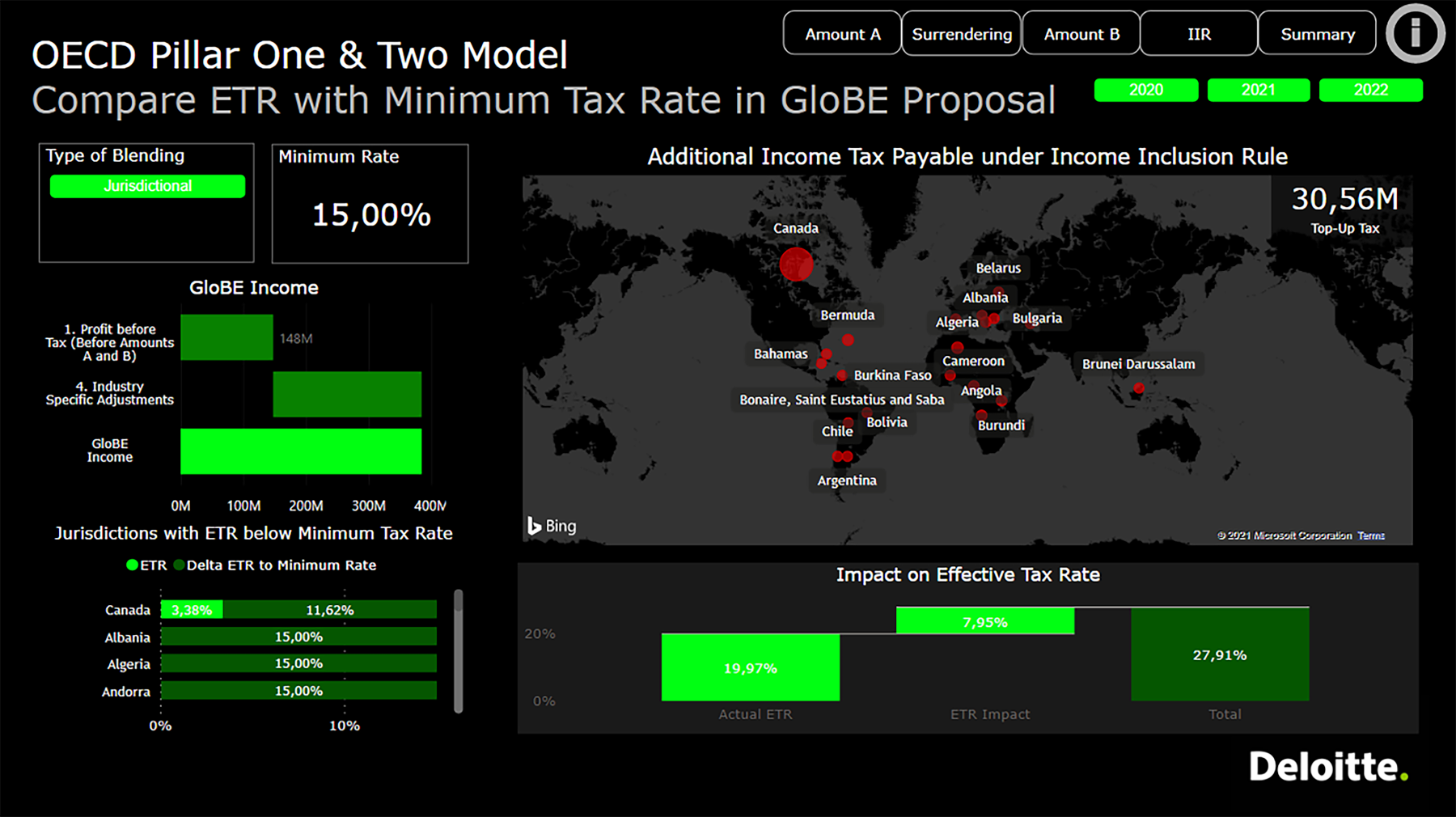

Calculate GloBE income

Quickly compare effective tax rate (ETR) with Minimum Tax Rate in GloBE Proposal.

Customize your data set

Evaluate the impact of different scenarios by customizing your data set.

Easy scenario planning

Save and compare various scenarios and datasets.

Fluid branded contact