South Korea 2023 Tax Law Reform has been saved

Article

South Korea 2023 Tax Law Reform

Highlights for Korean Tax Reform 2023 for financial service companies

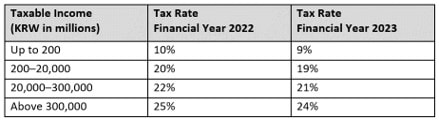

1. Overall reduction in corporate tax rates of 1% per tax bracket (highest rate is 26% now)

Under the Korean Tax Reform for 2023, corporate tax rates have been reduced by 1% for each taxable income bracket, effective for fiscal years beginning on or after 1 January 2023. The initial proposal was to target and remove the highest 25% tax rate bracket. However, the National Assembly renegotiated the terms to benefit a broader income spectrum.

2. Elimination of Accumulated/Undistributed Earnings Tax (with exception of Korean conglomerates with cross-shareholding)

The Accumulated/Undistributed Earnings Tax applies to two types of companies: (1) domestic corporations with a net asset value of more than KRW50 billion on their balance sheets at the end of their fiscal year (excluding qualified small and medium-sized enterprises [SME]); and (2) corporations affiliated with cross-shareholding-restricted business groups as per current Anti-Monopoly and Fair Trade regulations. However, as of 1 January 2023, condition (1) has been excluded, therefore this tax will generally no longer apply to Korean subsidiaries of foreign national groups.

3. Dividend income exclusion of 95% of dividends received from a foreign subsidiary

Prior to 1 January 2023, a domestic corporation that received dividends from a foreign subsidiary was required to include the received dividend in its taxable income while claiming a foreign tax credit. However, the Korean Tax Reform for 2023 enables domestic corporations with at least a 10% ownership interest and a six-month holding period in a foreign subsidiary to exclude 95% of the dividends received from that subsidiary.

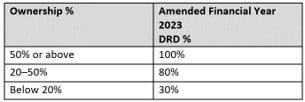

4. Revised Dividend Received Deduction (DRD)

Prior to 2023, the Korean Tax Law used to have a complicated system for calculating the domestic dividend received deduction ratio, which included variables such as the type of company (e.g., public or private), in addition to the ownership percentage. However, these variables have been eliminated now, and only the ownership percentage is considered. Furthermore, the DRD requirement for the ownership percentage has been lowered for dividends received on or after 1 January 2023.

5. Lower ownership threshold for filing consolidated tax returns from 100% to 90% ownership requirement

Prior to the 2023 Korean Tax Reform, a corporation was required to wholly own its domestic subsidiary to be eligible to file a consolidated tax return. However, starting from business year 2024, the ownership threshold for tax consolidation has been reduced from 100% to 90% or more.

6. Increase of limit for use of carried forward net operating losses (NOL) from 60% to 80%

The 2023 Korean Tax Reform increased the cap on the deductibility of NOL from taxable income from 60% to 80%. The 100% NOL cap for SMEs remains unchanged under the reform.

For further information, please contact Scott Oleson.