Deloitte in the News

RAB is on the Wire

Why Ukraine Needs Incentive Based Regulation in the Energy Sector, and What Tariff Disparities it is Able to Correct

Almost a year has passed since the free electricity market has been formally launched in Ukraine. Since then, discussions about its operation have become increasingly heated. One of the most pressing issues is the tariff one. The national regulator and other ‘involved’ government agencies are trying to please all the big players at once, as a result, the industry is suffering from price distortions. And recently also from disequilibrium caused by the unbalanced power flow from RES. Against this background, we can’t but mention the so-called incentive based regulation in the energy market. Artur Ohadzhanyan, Corporate Finance Advisory Partner, Energy and Resources Group Leader at Deloitte Ukraine, explained to Mind what such regulation is all about and why it is currenty topical.

From time to time, the idea of the so-called RAB regulation in the electricity sector appears in the Ukrainian public space and soon disappears again.

To begin with, let's clarify: RAB is an abbreviation of the English ‘Regulatory Asset Base’, which in Ukrainian is ‘регуляторна база активів’. So the correct abbreviation in Ukrainian is ‘РБА’ not ‘РАБ’ as it is often mistakenly transliterated from English.

The fact that this issue has been unresolved in Ukraine for many years shows that it is not perceived as urgent. Even more, when discussing the incentive based tariff regulation in electricity transmission and distribution systems (precisely such a term is correct), the emphasis is quickly shifted from the economic to purely political plane. To some extent, this is explained by the fact that from the technical point of view issue is quite difficult to understand correctly, and the result of the implementation of such pricing policy is perceived by the majority unequivocally: tariffs will be increased.

Before we move to the issue of price setting in the electricity transmission and distribution sector, let's try to understand why the existing system in Ukraine is inefficient.

The incentive based regulation policy in this industry has long been in place in the vast majority of Western and Central European countries. Should our country change its pricing policy, too?

Why it is necessary to regulate the prices

Let's start with the question why pricing in the electricity transmission sector should be regulated at all. Why market principles weren’t used? The answer is quite simple: electricity can only be transmitted via electrical networks. And networks as the only means of electricity transmission belong to the companies that provide these services, and there is no alternative. Thus, all known oblenergo companies, as well as NPC Ukrenergo, which transmits electricity via high-voltage networks, are natural monopolists. And in such conditions, of course, there can be no competition and market principles of pricing.

That is why the procedure for setting tariffs for such companies should be established by an independent state regulatory body.

What are the downsides of ‘Cost plus’ system

The approach to the regulation of tariffs for electricity transmission and distribution services, which is currently applied in Ukraine and was formerly used in European countries, is the so-called ‘Cost plus’ system. It stipulates that the income of a monopoly company is set by the regulator (in Ukraine – NEURC) as the sum of allowed costs (not all costs may be allowed by the regulator to be included in the tariff) of such a company plus the regulatory rate of return. This amount in Ukraine is set by the regulator separately for each operator company on an annual basis and, therefore, determines the tariffs for consumers. As for capital expenditures, in Ukraine they mostly represent the amounts of annual investment programmes approved by the regulator for each company, and the source for covering such expenditures is also cash receipts from consumers.

Under such conditions, the regulator and the monopolist have diametrically opposed interests: the regulator tries to curb the tariff growth, and the company is interested in raising costs. One cannot speak of any incentives for operational efficiency in such conditions.

Even more negative impact on power grids is made by the consequences of the ‘Costs plus’ policy related to capital expenditures. The company has no incentives and opportunities to invest in maintaining its networks and improving the quality of services above the approved investment programme. The consequences of underfunding investments in this industry are not simply a reduction in the quality of services. To some extent, this is about security of the energy sector. Electrical networks are a very expensive and complex engineering infrastructure that permeates the whole country and requires constant funds to maintain its serviceability.

Another factor that is often underestimated is the fact that the architecture of our networks were created at a time when both the generating capacities and the consumption structure were significantly different. It is worth mentioning at least the active development of renewable energy in Ukraine. Connection to the electricity grid of a huge amount of generating capacities, which has not even thought of 20 years ago, is a very difficult technical task for transmission and distribution companies. And it also involves the costs that most such businesses have to plan and bear.

And, under the ‘Cost plus’ system, there are no incentives for them to act flexibly, solving complicated technical tasks and trying to achieve greater efficiency. ‘Cost plus’ pushes the companies in another direction – to increase their costs. From the point of view of a market economy, this is, of course, absurd.

Implications for the power grids’ condition and the country’s economy

We may look into the problems of oblenergos even more deeply, but speaking about the feasibility of changing the pricing system, we should analyse the implications of their activity for consumers and, consequently, for the economy in general.

Usually, when it comes to the condition of the electricity distribution system, analysts mention a high level of depreciation of oblenergos’ assets. But this figure is taken neutrally by the majority and looks unconvincing.

Really, what kind of depreciation are we talking about: physical or economic one? If physical, how is it measured? If economic (which is typically referred to, often without any specification), then, based on what value is it calculated? Based on accounting records? But, depending on the accounting policy, which differs from company to company, both the cost and depreciation may vary significantly. On top of that, many critics do not link the rate of depreciation of assets with their actual performance, as it is known that a huge number of the infrastructure and energy companies’ assets having a high level of depreciation are used for a long time.

We do not deny the importance of the rate of depreciation, but still let’s pay attention to the industry specific, widely used indicators:

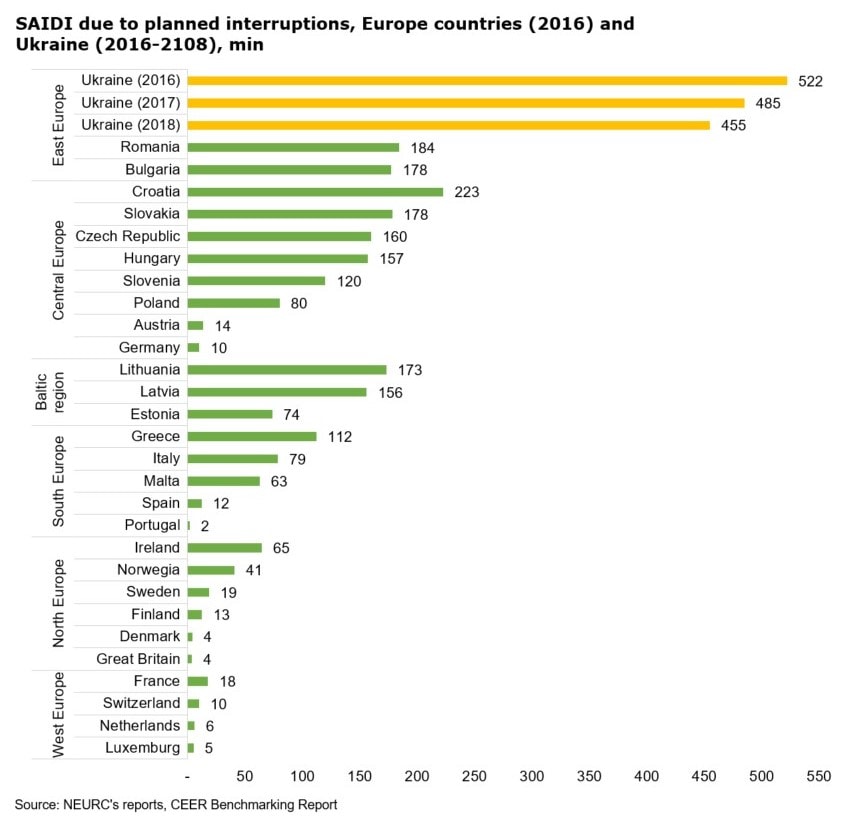

- SAIDI – System Average Interruption Duration Index per consumer;

- SAIFI – System Average Interruption Frequency Index per consumer;

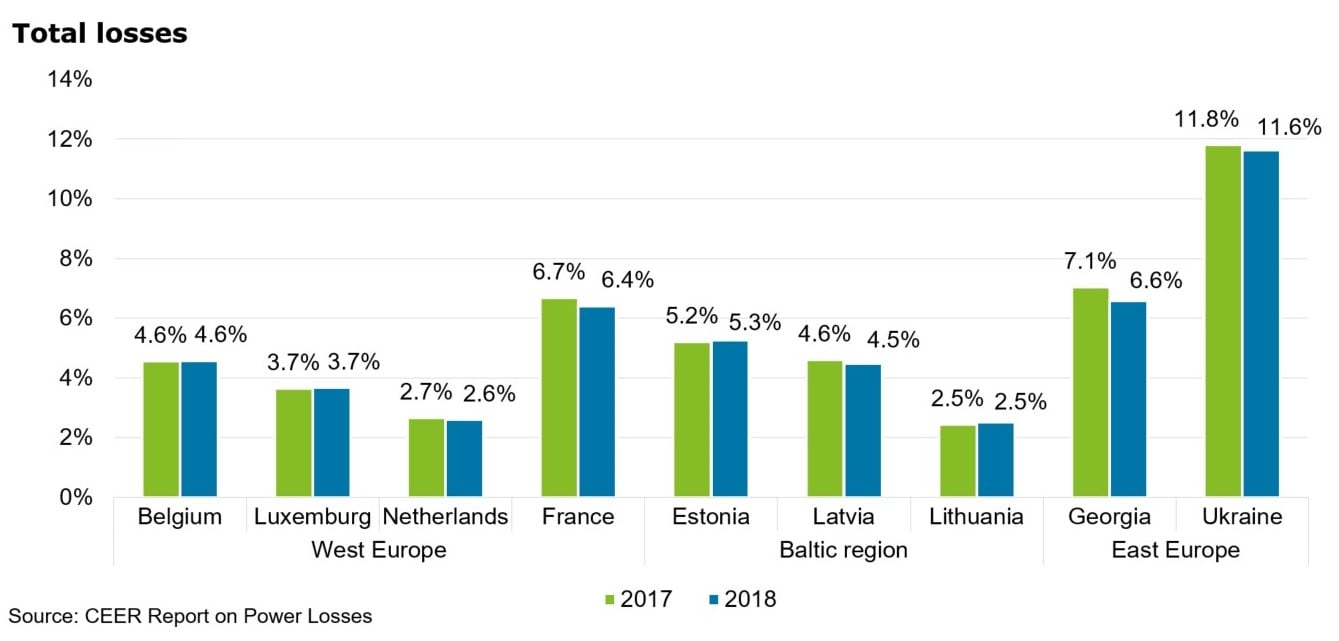

- Losses – electricity losses, a difference between the amount of electricity fed to the grid and the amount of electricity actually supplied from the grid to consumers.

Let's compare SAIDI and losses in Ukraine with those of different EU countries.

First of all it should be noted that there are several methods for calculating these indicators, that is why here we use equally calculated indicators for correct comparison.

To understand the impact of electricity losses on the economy of Ukraine, note that the amount of electricity lost was:

- 2017 – 16,786 GWh;

- 2018 – 16,995 GWh.

The specified data clearly demonstrates the position of Ukraine among the European countries. Obviously, we are not just in a bad situation in terms of quality of electricity distribution services. As one of the largest countries in Europe with a much branched electricity supply network, we are the worst among the specified countries, including the states, which are not economically much more powerful than us.

Moreover, the indicators do not just differ. The remarkable difference demonstrates that the state of electricity networks, system of their service and operation in Ukraine are incomparably worse than the ones of the majority of the European countries. Only systemic fundamental problems can be the reason of such a huge gap.

After reviewing these indicators, the reader may ask a question: if everything is so bad, why do not we feel it in everyday life, for instance?

The answer is quite simple. The indicators specified above are average across Ukraine. On the top of that, they are relevant for the entire network. However, the indicators are better for the capital and metropolises, where the majority participating in discussion of the issue concerned inhabits. After a closer look at the statistics of the NEURC and conversations with other consumers, including large enterprises, residents of villages and small towns, we will get a broader picture.

The SAIDI indicator in some regions exceeds 1,000 minutes (i.e. more than 16 hours per year per an average consumer in the relevant region). Disconnections during peak loads, accidents, current frequency drops, property thefts create not only inconveniences, but actual losses and emergency situations. If we add electricity losses due to demolition of network equipment, flawed metering system and ordinary electricity thefts, we may be able to see the actual picture. According to the industry experts, the most dangerous issue is the low reliability of the distribution system, which may unexpectedly cause large-scale accidents.

Such situation was mostly caused by the system for regulation of electricity distribution companies in Ukraine aimed not at the development of network infrastructure but at the minimum support of its working capacity.

The European countries understood that the regulation of electricity transmission and distribution systems needed to be changed in the 1990s, and, as of now, the majority of the countries have already changed it.

Incentive-based regulation system: key features

What is the difference between the "Costs Plus" system and the incentive-based regulation system, which has been formally in place in Ukraine in electricity transmission and distribution since 2013, but has not been implemented yet?

The key features of incentive-based regulation system related to the tariffs are as follows:

- the tariffs are calculated based on transparent economic rationale;

- the tariffs are set for the specific period of several years;

- the tariffs include components of stimulation for achievement of planned indicators known beforehand and sanctions for the failure to achieve them. This is a fundamental difference from the "Costs Plus".

It should be noted that every European country has an incentive-based regulation systems with their own features, that is why there are no two countries with identical rules for tariff-setting for services of electricity transmission or distribution companies. However, the general features of such system in those countries are principally similar, so we can outline several similar signs.

Income components

The income of electricity transmission or distribution companies permitted by the regulator in the majority of countries consists of the following components:

- operational expenses;

- income tax (in some countries);

- regulatory depreciation and amortisation, which are calculated with the use of the RAB, as a rule;

- regulatory income, which is calculated with the use of the RAB.

The rationale of such approach is clear: the company receives such amount of income, which allows to compensate the costs incurred and earn a certain profit. Even though the 'RAB' abbreviation is mentioned here, this rationale reminds us of the "Cost Pus". That would be true, but aside from the mentioned components, the system of incentive-based regulation envisages utilisation of rewards (stimulation, incentives) and penalties (sanctions) aimed at incentivising the companies to achieve the targets on efficiency and quality of services.

Let us briefly review the abovementioned income components of the company with incentive-based regulation system in place.

The operational expenses include expenses, which are directly related to implementation of the key activities of the company. The regulator may set specific rates of such expenses for each company, however the expense components for the companies of the same country are generally identical.

What is RAB?

Before getting to regulatory depreciation, amortisation and profit, it is worth explaining the RAB notion. In terms of its economic substance, the regulatory asset base is the value of assets, which are considered as such ensuring provision of services by the company according to the specific regulatory arrangement.

The variations of inclusion of specific assets into the RAB base and the methods for determination of their value are significantly different in different countries. The RAB components may include the following:

- fixed assets involved in operations of the company – usual practice for all countries;

- in-progress capital investments – according to the latest data of CEER these practices are utilised by a half of the European countries with incentive-based regulation system;

- working capital – utilised in just a third of the European countries with incentive-based regulation system;

- assets in the form of contributions of third parties and leased assets are included into the RAB in a restricted number of the European countries.

How is the RAB value determined?

The most common practice is to use the historical value of the assets. According to CEER, 72% of the electricity transmission companies and 65% of the electricity distribution companies utilise the historical value for the RAB.

Some countries calculate the RAB value using revaluation. The justification for using such method is high inflation level or processes of company consolidation. Only five countries use revaluation for the companies distributing electricity via high voltage networks. In most cases, the revaluation is used once during transition to the incentive-based regulation.

Important aspect: the RAB value in 75% of the European countries is identical to the fair value of the assets according to accounting records of the relevant companies.

But the RAB itself is a transitional indicator. The more important is that the RAB value of the company is used for calculation of the regulatory depreciation, amortisation and profit amounts, which is an important income component of natural monopolies.

How regulatory amortisation and profit are calculated?

The amortisation is calculated using a specific method with useful lives established by the regulator. Respectively, the amortisation calculated based on the value of asset creation (construction/acquisition) is the main source of capital expenditure incurred by the companies for modernisation and development of their assets.

The issue on method for profit calculation is equally important and very vital. The majority of the countries utilise the WACC method to determine the rate of return as a proportion of the RAB value. According to CEER, this method is not utilised only by four countries related to electricity transmission and two countries related to electricity distribution. This is the very method that is perceived by the majority of market operators as a fair one, because it essentially reflects the market rate of return on the invested capital, which is expected by a typical investor.

Therefore, the income of the monopoly is calculated so that:

- compensate for all justified operational expenses, including the income tax;

- enable the companies to modernise their assets on a permanent bases through supporting their operability and, respectively, the quality of services;

- enable the companies to earn the profit, which is approximate to the market level.

Regulatory periods

It is also important that the rules on regulations are set (and remain unchanged in basic aspects) throughout a specific, so-called regulatory period consisting of several years. It ensures that the companies plan their activities more efficiently, unlike other systems, which set the tariffs on an annual basis.

Moreover, transparent unchanged rules established for this period allow the companies to enhance the efficiency of their activities by reducing expenses and losses. The incentive for enhancing the efficiency is the fact that unlike the "Cost Plus", the material effect is an additional profit for these companies. That means that their incentives are totally opposite to the incentives of the companies operating under the "Cost Plus" system.

Now, let us find out what makes such pricing system to be incentive-based.

Incentives

The regulatory authorities in different European countries set different incentive-based systems for monopolies operating in energy industry. But, in general, they are aimed at setting of specific targets for the companies regarding reduction of general operational and/or capital expenditures.

Such targets may be based upon both the vision of the regulator and comparison with the operational indicators of other operators (benchmarking).

The purpose of implementation of incentives may be the increase in efficiency in such areas as improvement of consumer access to the network, reduction of electricity losses, quality of consumer servicing, implementation of innovations, reliability of electricity supply (SAIDI, SAIFI indicators etc.) and reduction of service costs for end consumers.

The company is obliged to achieve the targets, as they are specific (determined in terms of quantity) and, as a rule, clearly determined in terms of time. The failure to achieve the targets result in relevant sanctions (losses).

What obstructs the implementation of the incentive-based regulation system in Ukraine

All the required legal frameworks for transition to the incentive-based regulation of electricity distribution companies in Ukraine (let us focus on this segment in particular) is already in place, but the system has not been implemented yet. In order to understand the probable reasons, it is necessary to analyse the main features of the proposed system and its perception by the society and officials.

Pursuant to the NEURC's Procedure , the components of the company income are identical to the ones that are the most commonly used in Europe: operational expenses, income tax, as well as amortisation and profit, which are calculated based on the RAB value. However, there are several important specifics. First of all, it is the procedure for determination of the regulatory asset base.

RAB in Ukraine

Value of RAB for the electricity transmission and distribution companies are determined based on the methodology approved by the State Property Fund of Ukraine , which is in charge of the state regulation of the valuation activities in accordance with the legislation. Methodology No. 293 is detailed and contains minimum possibilities for application of the subjective assumptions by the appraisers in their valuations. Additionally, the Methodology contains the collection of price indicators for a major part of the energy assets, which is mandatory for use in the assessment of the electricity distribution companies' assets.

The Methodology requires adjustment of the assets' value downwards using ratios, which calculation accounts for actual utilisation of the assets. Such approach is aimed at preventing the consumers from paying for additional unutilised capacities of the monopoly company.

The assessment is carried out once upon transition of the respective company to the incentive-based regulation system. Expenses for the new assets obtained by the company during further operation and expenses for reconstruction of the existing assets shall be then accounted for in the RAB pursuant to the amounts of such expenses without their further reassessment.

The assets of a large part of oblenergos were repeatedly assessed, accepted by these companies, reviewers of the State Property Fund and approved by the NEURC.

Nevertheless, the European experts who are ready to share their experience with Ukraine wonder: why the book value is not applied? For those who know the financial statements of many Ukrainian companies, the answer is obvious.

The accounting policy of the Ukrainian electricity distribution companies, which are over 30, is different. Some companies maintain accounting under the fair value (which shall be regularly reassessed), other - under historical value. Only this fact causes significant differences in the book value of the companies similar in form, age and condition with a different accounting policy.

The following factors cannot be ignored either. The companies have different quality of the asset accounting, accuracy in compliance with the accounting standards, and attitude to the audit of the financial statements. There is one more issue - accounting standards. Which standards (national accounting standards or IFRS) are to be used for accounting the value?

Based on the experience, even some electricity distribution companies of the same holding company and applying the same accounting policy with the same standards may have drastically different book values of the assets taking into account the objective differences (region, consumer structure, asset structure).

One of the reasons for this is different approaches appraisers used for the fair value assessment, as well as their different industry practice and qualification. In additional, such assessment is technically difficult. There is also an objective reason, which doubts eligibility of the fair value in the accounting for RAB calculation. The fair value shall account all factors, including economic, as well as existing tariff-setting system and its possible changes. As a result, the fair value of the assets within the financial reporting standards is much lower than their recoverable amount.

In the meanwhile, comparison of the valuation results under aforementioned Methodology No. 293 gives comparable results for the different companies, and strictly detailed assessment algorithm and obligation to use the collection of price indicators attached to the Methodology ensures this.

One final comment is that generally the company's shareholders and creditors are in charge of correctness of the fixed assets' value recording in the company's accounting.

However, if tariff for the electricity distribution for millions of consumers is calculated based on the assets' book value, then that becomes an issue of society.

Approaches of Methodology No. 293 may be disputed (professionally, without populism, of course), amendments thereto may be proposed, however, considering that the assessment is made for the regulatory purpose, it is to be transparent and objective that will result in fair and clear assessment results.

Depreciation and investments

In accordance with NEURC Procedure, all amount of the annual regulatory depreciation and a half of the annual profit calculated using RAB value are to be invested in accordance with the investment programmes annually approved for each company. That is the regulator's imperative requirement in Ukraine.

Neither European country has such practice of direct connection between the depreciation amount and the volume of CAPEX. The Western countries proceeds from the principle that volumes and the purpose of the CAPEX may depend on actual needs of the company. The same includes the requirement concerning application of the company's profit.

Is such requirement justified in Ukraine? The answer to this question requires reviewing a range of aspects of the company activities and regulatory condition, in particular:

- actual needs of the company for investment to replace and develop the assets;

- correlation of the amounts with compulsory investment costs to be borne by the company in accordance with the calculated depreciation and profit;

- ability of the company to disburse these compulsory costs within one year taking into account all procedural, technical and financial issues related thereto;

- whether this requirement is unlimited or is to be revised when the situation with the assets improves due to such investments.

Unfortunately, at present, there is no information about carrying out such analysis, thus, we can hardly get acquainted with its results.

Regulatory base return

Currently, the regulatory framework envisages that the Ministry of Economic Development sets the marginal (maximum) rate of return as a percentage of the regulatory framework, and the NEURC, determines a specific percentage of return that should not exceed such a marginal rate.

The issue of the regulatory base return is the most acute in Ukraine. In addition, the controversy over this issue is almost a major obstacle to introduction of the incentive regulation in the country.

The value of the return rate and the fact that the NEURC proposes to set a separate return rate on the so-called "old base" (i.e. estimated by the RBA Methodology on the date of transition to incentive regulation) and the "new base" (i.e. the value of assets created during functioning in the incentive regulation mode). At the time of this material preparation, the NEURC has a project that proposes a rate for the "old base" at 1% and for the "new base" – 15%.

The main argument of the regulator and a significant part of the Ukrainian politics is that the rate of return is the return on invested funds. If the RBA value revalued according to the Methodology No. 293 significantly exceeds the funds actually invested by the owners of regional power distribution companies (oblenergos) in their acquisition, then the rate of return cannot be equal to the market rate and should be lower than it.

The main arguments of the single RBA return rate supporters are as follows:

- different rates of return in other countries are not applied (this is not the case, there are a few examples in Europe);

- companies were acquired in different years, so a direct comparison of investment amounts with the RBA value is not correct;

- there is a high probability that in the nearest future the regulator will still abandon the difficulties associated with the differentiated calculation of regulatory returns, and will establish a single rate.

Incentives

The system of incentives provided by the NEURC Procedure is complex. In general, it includes monitoring operating costs and service quality.

The Procedure provides for the establishment of operating costs as part of efficiency indicators defined by the NEURC, which affect the company’s required income amount. The required income can also be adjusted according to the target for achieving quality indicators. Quality indicators are based on a system average interruption duration index (SAIDI).

At present, it is difficult to assess the effectiveness of the incentives and sanctions established by the Procedure, because they have never been applied in practice.

Instead of conclusions

To some extent, repeating the above, it is worth highlighting several important theses.The system of incentive regulation of natural monopolists’ prices always includes the political will and compromise components. It is useless to try to create an ideal system – there is no absolutely correct unified system, because there are no absolute market conditions for the natural monopolist functioning.That is why, for example, the question "Which way to determine a rate of return – a single rate or two separate ones – is correct?" does not seem very consistent. There are approaches that work, suit the service provider and consumers and incite the efficiency and quality of services. Yet, there are those that either contradict the very logic of the incentive regulation, or ultimately deplete it.

Unfortunately, since 2013, no model of tariff calculation has been presented in Ukraine, although, the entire legal framework for this is available. Yes, it is a plenty of work, but not so much that it cannot be done independently and objectively in a reasonably short time. The lack of such a transparent calculation publishing creates grounds for manipulation and baseless allegations by the discussion participants, including those who may have their own calculations and those who do not have a full understanding of the subject but have influence or authority.

It is also worth recalling that all European countries that have implemented a system of incentive regulation have come to it through trials and errors, taking into account both their own experience and the experience of neighbors. By the way, this is why in all countries the first regulatory period is set short enough to analyze the results from the beginning and make adjustments if necessary. In Ukraine, where the first regulatory period is three years and the next ones are five, there are also appropriate conditions for this.

In the first stage, the transition to incentive regulation will lead to an increase in electricity distribution tariffs (and possibly transmission, if this applies to Ukrenergo). Therefore, it is important that all parties involved in the process are guided by one approach: more money – more investments, more investments – better efficiency and quality of services, better efficiency and quality of services – a tendency to restrain and reduce the tariffs.

It is important for all of us to remember that any good idea can be distorted, and the only way to avoid this when implementing a new system is its transparency and willingness of all parties to compromise in order to achieve a goal that should benefit both consumers and companies providing services.

Contacts