Estimates suggest that there is just shy of one billion square feet of available office space in search of tenants in the United States,1 nearly 1.5 times the amount from the end of 2019.2 With a shortage of nearly three million homes,3 the US housing sector has emerged as a likely recipient of the unused downtown office space. So far, the US commercial real estate industry has been slow to respond: Between 2016 and 2021, there were, on average, 31 housing conversions from office products per year, totaling 188 projects.4 And while many Americans are still working from home, at least part of the time—a trend that will likely continue—only 217 conversion projects are in the immediate pipeline for completion.5

Government and business leaders appear to be taking notice.6 Some political leaders at the local and state levels have put forward legislation or called for action specifically supporting office-to-housing initiatives. These actions could provide incentives for real estate developers to provide Americans with clean, affordable, and safe places to live. Here are some of the initiatives in the works so far:

- At the end of 2021, Chicago’s La Salle Central TIF district had a balance of US$197 million in tax increment financing that they planned to make available to developers, with a priority on underutilized space. These would include those prime for conversion from commercial to residential space.7

- Washington, D.C. launched a US$2.5 million, 20-year tax abatement program for owners who add at least 10 housing units and change a building’s use in the downtown D.C. area, and of those units, 15% must be set aside for affordable housing.8

- California set aside US$400 million in incentives for office-to-affordable housing conversions. The state already had more than 50 applicants and roughly US$105 million already allocated as of early March 2023.9

City governments have provided these types of incentives for conversion projects before. In the early 1990s, New York City passed the 421-g tax abatement program, incentivizing 13 million square feet of downtown Manhattan conversions. And Philadelphia passed its own abatement program in 1997, resulting in 180 building conversions.10

Could it pay off? Yes, but not right away

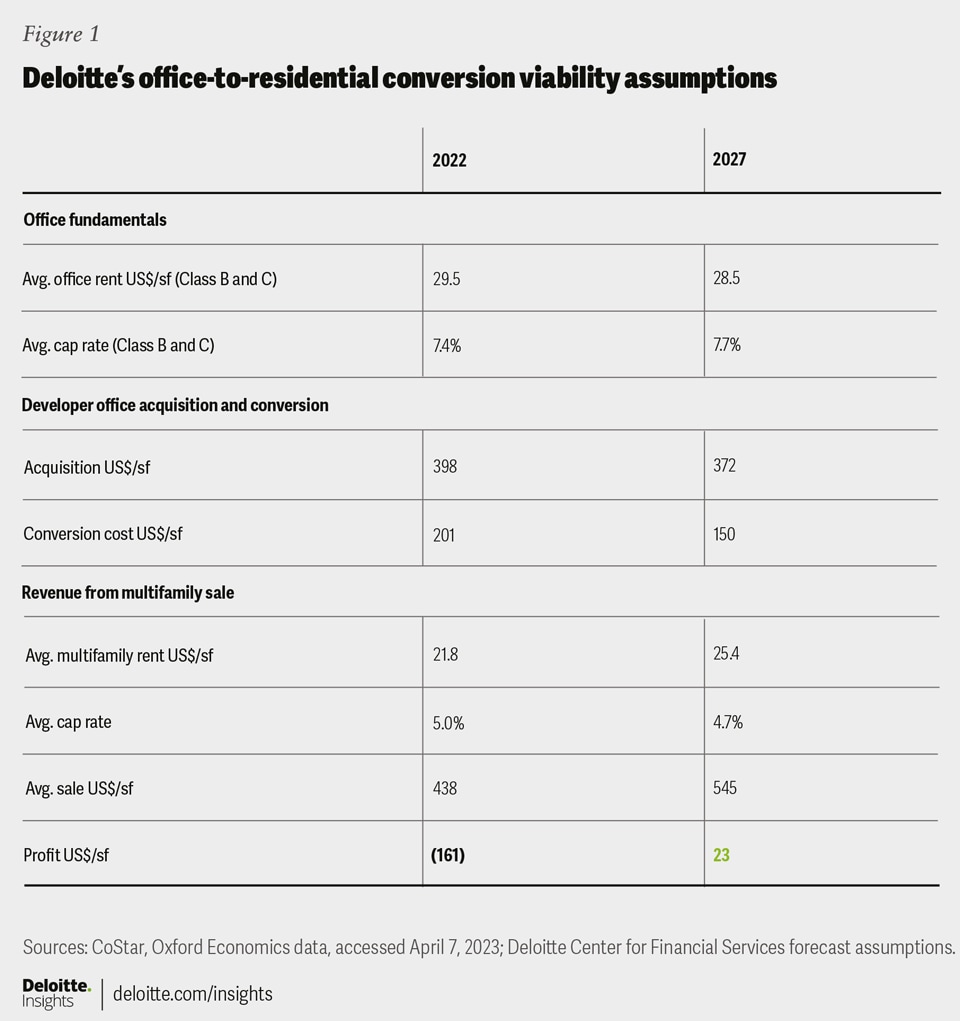

When considering these types of conversions, one of the biggest challenges owners and developers face is whether—and when—their investments will pay off. We anticipate that, by 2027, shifts in rents, valuations, acquisition costs, and conversion costs, in addition to added government-backed incentives, could allow developers to achieve a net profit on conversions of underutilized office space in favor of residential space (see sidebar for further information).

Layout aside, two valuation assumptions could deter developers in the near term: comparable rent and vacancy levels. The median asking rent for an apartment unit in the United States is around US$22 per square foot (psf). With US office rents still averaging US$37.38 psf,11 a 41% pricing concession in addition to an amortized cost of conversion is a tough pill to swallow. Additionally, developers would be unlikely to convert a building with a below-average vacancy that is still operating best as an office building.

{kind=link}