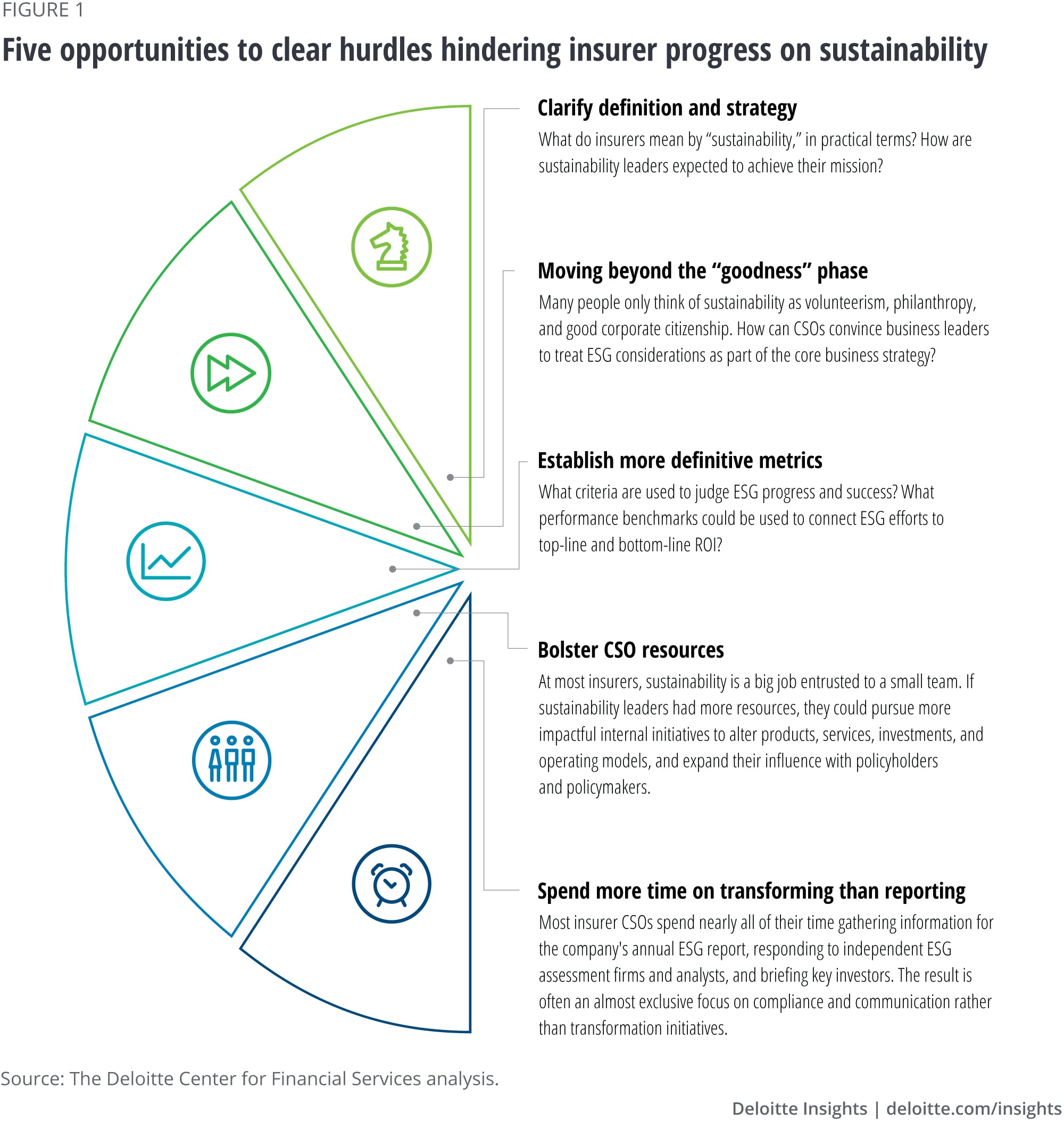

Opportunity No. 1: Clarify sustainability definition and strategy

How exactly should insurers define “sustainability,” and how might those leading such efforts go about realizing the concept strategically and in day-to-day operations?

Many of the ESG leaders interviewed said their companies lacked consistent messaging from senior management and board members about what sustainability means and how it relates to the company’s operational business plans and strategies. Definitions cited were frequently broad and aspirational, and sometimes, downright vague.

One described the effort simply as “positioning us to be a company that people can be proud and confident to work for, do business with, and invest in over the long term.” Another cited sustainability as “determining who we are, what we stand for, and what that means in terms of aspiration and vision.”

Most, however, acknowledged they are also expected to maintain a clear business focus and rationale for sustainability initiatives. “ESG fundamentally is about value and not values,” said one property-casualty CSO.

Several said they are making progress in keeping track of what their companies are doing in ESG as well as facilitating more public transparency. But most are still figuring out their longer-term strategy and execution plans to go beyond gathering and communicating information to stakeholders.

To enable sustainability leaders to formulate viable transformation strategies and gain widespread buy-in and commitment from leadership down through the rank and file, companies should make sure they specifically define each element of ESG. The “environmental” side tends to get a great deal of attention in insurance because of the billions in climate-related property-catastrophe claims generated in most years, along with increasing calls for data and accountability from regulators and advocacy groups.

But sustainability mission statements should also define an insurer’s “social” goals—for example, to improve economic equity by finding ways to increase coverage availability and affordability in underserved areas. The “governance” side should be defined not just in terms of transparency, but also by how effectively the company is enhancing diversity and inclusion in management, executive leadership, and the board.

Establishing and disclosing a clear sustainability strategy and execution plan might also help convince skeptical external and internal stakeholders that an insurer is firmly committed to fulfill impactful ESG goals. Deloitte’s recent report on Building credible climate commitments provides a possible road map for companies to follow to earn stakeholder trust, at least when it comes to environmental efforts.7

Opportunity No. 2: Moving beyond the “goodness phase”

Some interviewees cited frustration with colleagues who question the need for ESG initiatives and perhaps even seek to block or delay implementation, noting that such skepticism, if left unchallenged, could create credibility gaps, and undermine change management efforts.

One challenge is that many insurer sustainability programs may be “stuck in the ‘goodness’ phase,” according to a personal lines carrier’s CSO.

“We’re still trying to get beyond the cliché about how we can be a force for good and more about creating a company that’s sustainable not only in terms of dollars and cents, but in terms of what’s best for the long-term interests of all stakeholders,” said a CSO from a group benefits company.

A multiline insurer’s sustainability executive said that “too often our initiatives are conflated with good corporate citizenship, which implies a goal other than maximizing shareholder value, when, in fact, it’s all about how to reconcile the two.” CSOs therefore should strive to demonstrate and communicate a clear correlation between sustainability and enhancement of customer experience, stakeholder engagement, and ultimately, improved ROI and shareholder value to get senior leadership and functional leaders on board.

Many sustainability leaders interviewed cited following socially responsible business practices from a variety of ESG perspectives as a common goal. For example, several carriers are cutting back or even looking to “decarbonize” their underwriting and investment portfolios. Other interviewees seek to influence policyholders they cover and companies in which they’ve invested to transition to more sustainable energy sources, such as solar and wind power.

While none of the CSOs interviewed have direct responsibility for diversity and inclusion, all reported conferring regularly with human resource departments and, in some cases, those with another relatively new title—chief diversity officers. Together, they seek to reinforce the message that hiring, retaining, and promoting a more diverse workforce and leadership team is not being done for the sake of appearances, but to drive innovation,8 increase productivity,9 and boost profitability.10

Several interviewees stressed that CSOs should communicate how such efforts are justified from a bottom-line perspective. “It’s not the role of a CSO to effect change in the world-at-large. We’re not equipped for that,” said one ESG official at a multiline carrier. “My job is to define shareholder value in a sustainability context and help guide the company in a way that’s aligned with management’s duty to shareholders. Our duty is to take care of all our stakeholders—employees and customers—but within a business framework.”

Opportunity No. 3: Establish more definitive metrics

Some insurers have already begun setting big picture sustainability goals, particularly when it comes to managing climate risk—for example, by exploring ways to reduce their own carbon footprint.

However, most interviewees were striving to meet more basic, qualitative goals, such as publishing an annual report, creating and/or serving on cross-functional sustainability committees, and forging internal partnerships with colleagues who share ESG responsibilities. Some CSOs said management had set goals without providing benchmarks to manage expectations, quantify progress, or measure their status against peers.

The World Economic Forum (WEF) recommended firmer benchmarks in a September 2020 report prepared in collaboration with Deloitte LLP and other organizations.11 The WEF report’s 21 core and 34 expanded metrics and disclosures coalesced around four interdependent pillars: Planet, People, Principles of Governance, and Prosperity.

In terms of climate risk and its impact on the planet, for example, WEF called for companies to adopt the recommendations of the Task Force on Climate-Related Financial Disclosures, with a timeline of at most three years for full implementation. In addition, the WEF recommended disclosing whether the company has established or committed to set greenhouse gas emission targets to bring their business in line with the goals of the Paris Agreement.12

In terms of human capital, WEF suggested reporting the percentage of employees per category by age group, ethnicity, gender, and other diversity indicators, among other talent benchmarks.13

Many insurers have already begun thinking along these lines. One life insurer interviewed created a vendor code of conduct on sustainability to make sure the company’s goals are in sync across its value chain. Other carriers interviewed are aligning with the United Nations Sustainable Development Goals, which include taking action to lower carbon emissions, promoting the use of clean energy sources, as well as supporting efforts to achieve gender and economic equity.14

Opportunity No. 4: Bolster CSO resources

Sustainability is a big job for the relatively small teams assembled at many of the insurance companies we interviewed. While ESG activity and costs are spread across insurance organizations, most carriers have not yet committed much in the way of full-time personnel or dedicated funding. The biggest staff among those interviewed totaled nine people; most are getting by with only two or three full-time workers.

While anticipating additional resources over time, no one interviewed expects a major influx of budget or staff at the moment. Most are compensating by enhancing collaboration with other ESG players to extend their reach. Insurers could help facilitate a sustainability support network by assigning responsibility for ESG or appointing sustainability liaisons throughout operating units and business lines. This should be supported by a clear governance structure that includes accountability measures.

Indeed, one personal lines insurer CSO cautioned against having a standalone operation and taking a siloed approach. This could discourage people outside the department from taking an active role or owning the ESG mission themselves, they suggested. Instead, sustainability should be the responsibility of all operating functions and business lines. CSOs, at least in the short term, may therefore be best served broadening their outreach so ESG considerations are widely represented across the company and are front of mind for business leaders.

“We want that conscious choice mindset embedded in our people’s brains,” said one insurer’s senior manager for sustainability. “We need to make ESG an organic component of our everyday business operations.”

One commercial lines carrier’s CSO depends on employee engagement to help spread the word. The company names “sustainability champions,” who take part in deep-dive brainstorming sessions about ways to better satisfy customer and investor ESG expectations. They also share ideas and success stories over the company’s intranet and social media platforms. Another multiline carrier holds sustainability "town halls" to raise awareness.

Some of those interviewed also called for more industrywide collaboration to benefit from collective experience and bolster ESG efforts. One carrier established an informal peer exchange to discuss disclosure challenges and ways to expedite net-zero carbon programs. Their sustainability leader hoped that one day, more formal gatherings would be hosted by an independent insurance sustainability association. Such a group could offer sustainability leaders networking opportunities and a neutral forum to regularly share war stories, cautionary tales, and best practices.

Opportunity No. 5: Spend more time on transforming than reporting

Most insurer CSOs serve primarily as information clearinghouses, spending the vast majority of their time collecting and communicating details about existing ESG-related activities for internal and external consumption.

Publishing an annual sustainability disclosure document alone can be a “monumental task,” noted one interviewee, whose report required the help of 150 subject matter specialists across the company. The leader said they had had handled 55 inquiries last year from independent ESG assessment firms to either complete a survey or verify information. Among those, one response, particularly important to investors, took 30 people the equivalent of 45 workdays to complete. And reporting demands are likely to increase, given ESG’s rising profile around the world among legislators and regulators.

Meanwhile, independent ESG assessment firms are now evaluating insurers’ diversity and inclusion activities, while some advocacy groups are calling for regulators to take economic equity considerations into account for underwriting. For example, they are looking at whether credit scores should be a permissible pricing factor if they might have a disparate impact on underserved segments.

These reporting functions are critical components to maintain and enhance an insurer’s competitive position among key stakeholders. In addition, those interviewed said engagement with ESG monitors is particularly important to avoid a low rating that might raise a red flag for investors, regulators, and customers, who are all increasingly asking insurers to document their sustainability efforts.

Indeed, a good rating from an ESG firm can help independently confirm that an insurer’s efforts amount to meaningful initiatives achieving significant progress, rather than simply “green washing”—merely appearing to address issues to maintain a company’s public image.

While those interviewed cited issues with how such ratings are determined, most agreed the assessment process can provide useful competitive information and keen insights into how insurers might up their game. One life insurer created a leader board comparing their company’s ratings with those of competitors. “We can’t afford to lose business or be screened out in seeking new business because of our efforts in ESG,” this interviewee said.

Some use these ratings as a yardstick to share with their executive team and board, identifying shortcomings that need to be addressed. For instance, after being downgraded by an ESG assessment firm for not having philanthropy aligned with their business purpose, one life insurer launched financial wellness programs in their headquarters community.

Meanwhile, as reporting responsibilities keep growing, the sheer volume may overwhelm small sustainability teams, leaving them neither time nor resources to devote to much else. This will likely prevent CSOs from taking on more strategic roles facilitating transformation in product development, underwriting, investment policies, and public affairs, where their expertise and influence might be productively deployed.

Consolidation and standardization of the many sustainability assessment templates in the market would help ease the CSO’s reporting burden. One CSO characterized the cacophony of demands as a “Tower of Babel,” because ESG firms and government entities are asking for much the same information, but in different ways.

To free up valuable time, companies could deploy technology tools to improve data collection and reporting efficiency. One insurance services CSO hoped to develop or purchase a comprehensive sustainability management system that could automate many routine information gathering, monitoring, and reporting tasks.

Empowering the CSO to drive ESG transformation

Insurers are in a unique position to influence policyholders and policymakers on sustainability, given their front-line role in helping mitigate these risks and compensating those who’ve suffered ESG-related losses. Yet many are struggling to keep up with clarion calls to bolster ESG commitments in-house, as well as press a more aggressive sustainability agenda among customers, investment recipients, lawmakers, and society-at-large.

Insurers that have already appointed a CSO or an equivalent position are off to a good start. Those that have not yet named a point person should seriously consider doing so.

But among carriers that have appointed an ESG executive, many have not yet empowered them to go beyond basic reporting and communication responsibilities. To enhance the capacity and capabilities of sustainability leaders, insurers should be enabling them to drive overall strategy and integration of ESG considerations into everyday business decisions and operations (figure 2).

{kind=link}

{kind=link}

{kind=link}