The future of fresh Patterns from the pandemic

8 minute read

13 October 2020

It is more important than ever that items be at their freshest when purchased.

A year unlike any other

Learn more

Explore the Consumer products & retail collection

Read more about the Future of fresh

This article is featured in Deloitte Insights Magazine

Learn about Deloitte’s services

Go straight to smart. Get the Deloitte Insights app

Good news! The fresh food category is as important and valued as ever. Sales are up.1 According to our Deloitte fresh food consumer survey 2020, nine out of 10 people say fresh food makes them happy. One of life’s great pleasures, food is also an essential product provided by essential workers. Despite early struggles, the industry rose to meet the challenges posed by COVID-19.

Yet beneath the top-level success, it is a category left changed by the pandemic. The entwined forces of the health and financial crises have significantly affected consumer behavior and posed new challenges for businesses. The industry now confronts disrupted consumer buying patterns and accelerated trends as well as a rise of new concerns and a recalibration of priorities.

Consequently, grocers and fresh food producers should be posing some key questions:

- How has the behavior of fresh food consumers changed relative to more normal times and which changes will continue to persist after the pandemic?

- Does consumer behavior during the pandemic indicate that it is time to redefine consumer segments? If so, how can the new segments be best served?

The Deloitte fresh food consumer survey 2020 provides a view into the new phenomena as well as the changed profile of consumers—both products of the pandemic. It revisits topics from The Deloitte fresh food consumer study conducted in 2019 to contrast how the prepandemic consumer compares to the consumer today. We also pose several new questions unique to this moment in time.

Survey methodology

- We interviewed 2,000 adults (aged 18 to 70) in the United States, who influenced fresh food purchases in their household.

- The interviews were conducted in July 2020.

- This sample was mapped to the US census to attain a representative view of the average US consumer.

- The findings were overlaid with our insights from ongoing State of the Consumer Tracker.2

The pandemic altered purchasing behaviors and value drivers

COVID-19 changed who we invite into our lives, what we do for entertainment, how we teach our children, and where we work, for those who are fortunate enough to still have stable employment and work from home. It isn’t a surprise that consumers also changed their habits and shifted their priorities when it comes to fresh food. Our survey reveals three major change themes in terms of how often consumers shop, what they buy, and what they value in their fresh food purchases.

Shopping less frequently

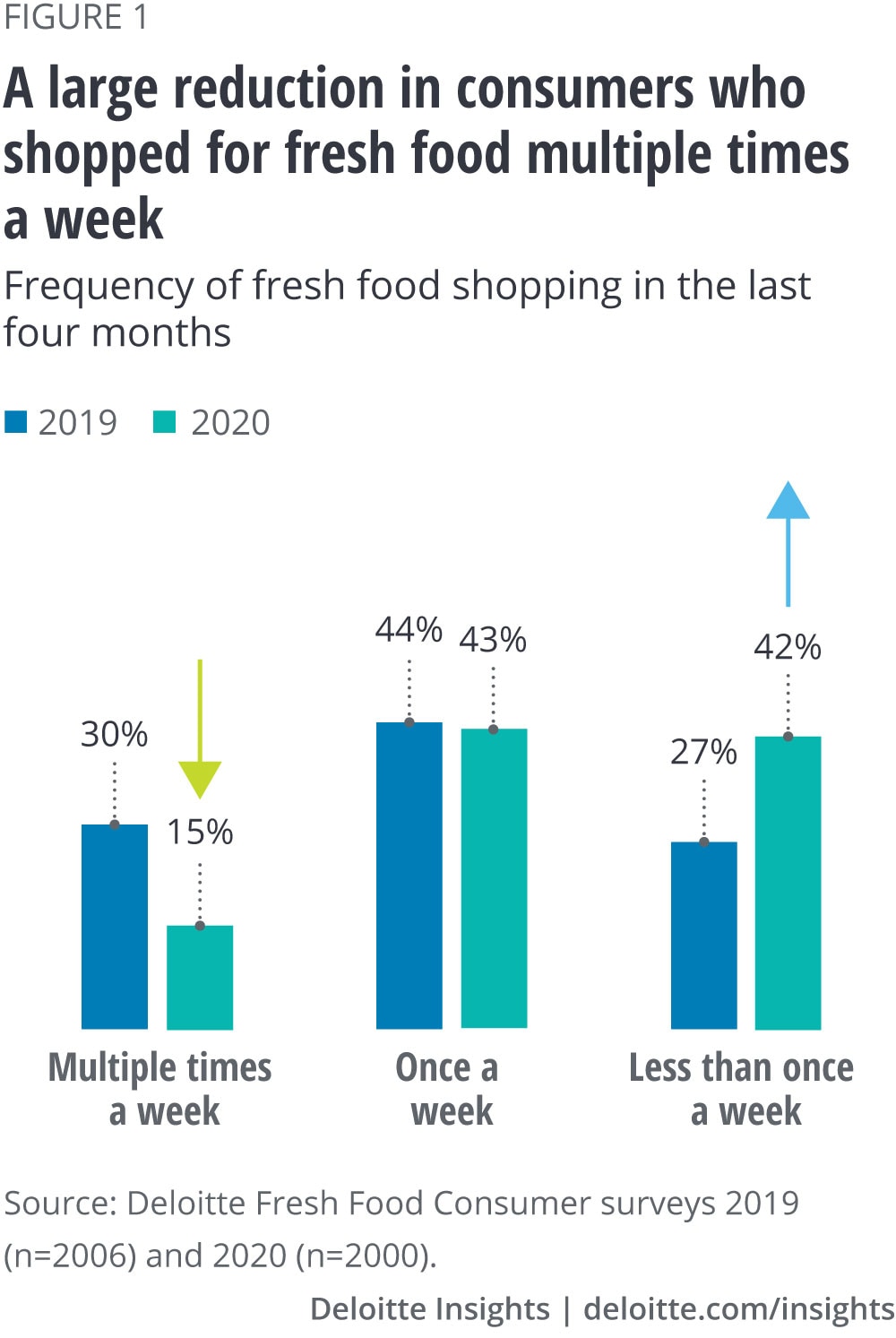

More than half of consumers (54%) in our survey say they feel stressed by shopping in stores. Stress is driving them to avoid stores and to shop less frequently. The number of respondents who said they shopped for fresh food multiple times a week dropped by half from 2019 to 2020 (figure 1). Those consumers who broke with their multiple-times-a-week practice now shop only once every two weeks, on average. This is troubling change for fresh, a category that is perishable by definition. And perishable means it is not possible for consumers to just stock up in equal amounts and keep fresh food for weeks on end at home. Not only that but frequent shoppers are also the grocery store’s best customers. Our analysis of grocery receipt data shows consumers who shop for fresh food at least once a week made up about 80% of fresh sales.3 A reduction in these frequent shoppers can’t be good news for the traditional channel.

The less frequent in-store shopping trend may stick for some time. Half of shoppers globally still don’t feel safe going to the store, even in countries that have the virus well under control.4

Changing what they buy

At the onset of the pandemic, consumers stockpiled food at a frenzied pace. To some degree the stocking up trend is still taking place, with consumers indicating they are still keeping more food on hand than they need.5 This surge in demand and other strains on supply chains translated into many food categories, including fresh food, experiencing stockouts. Two-thirds or 65% of consumers in our study were at least sometimes unable to buy the fresh food they wanted because it was out of stock; one in four say this happened often or almost always. One can assume that if a consumer experienced too many stockouts they would switch their shopping to another store entirely—translating to an all-or-nothing situation for the retailer. Switching costs are lower than ever now that there are good digital options that remove proximity to home as a barrier.

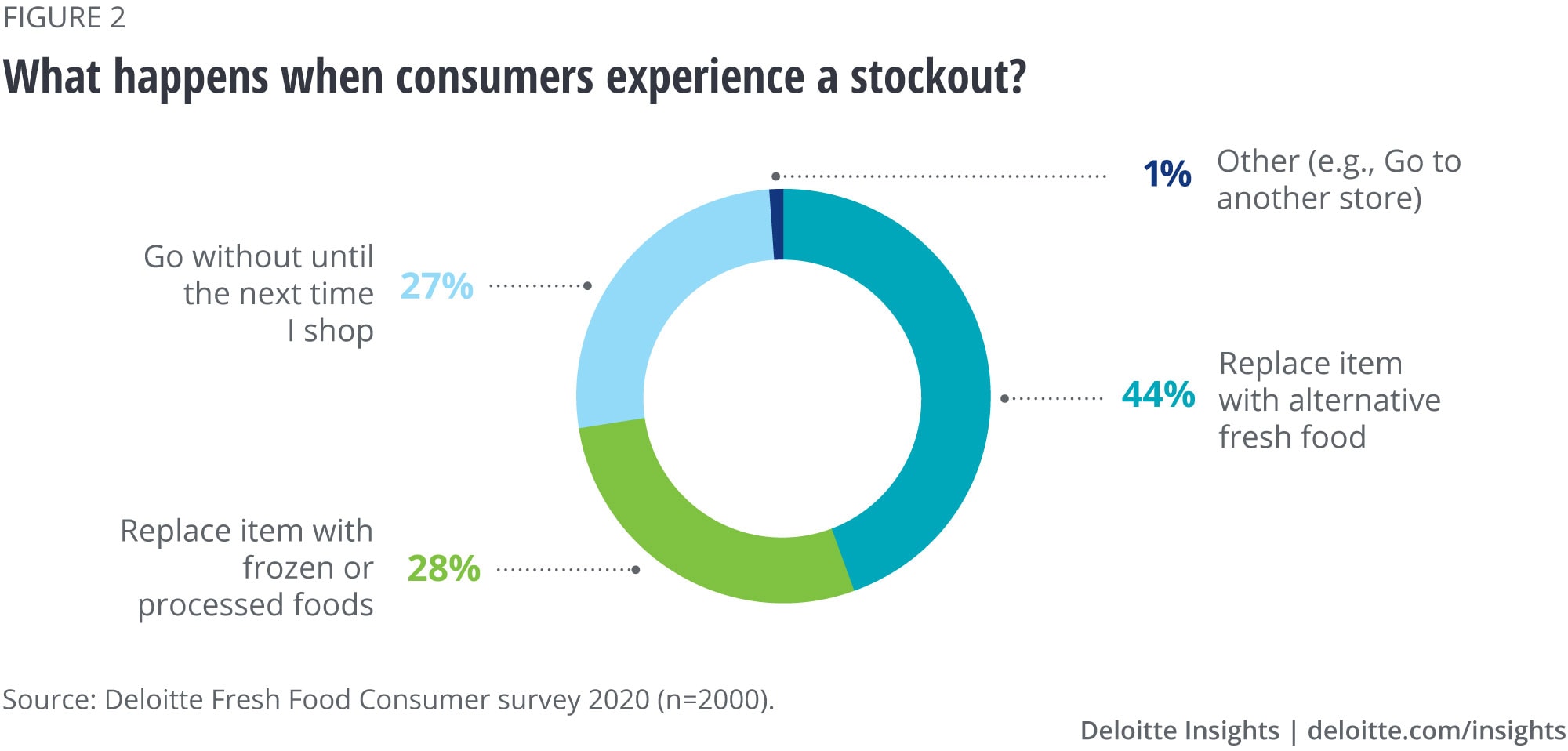

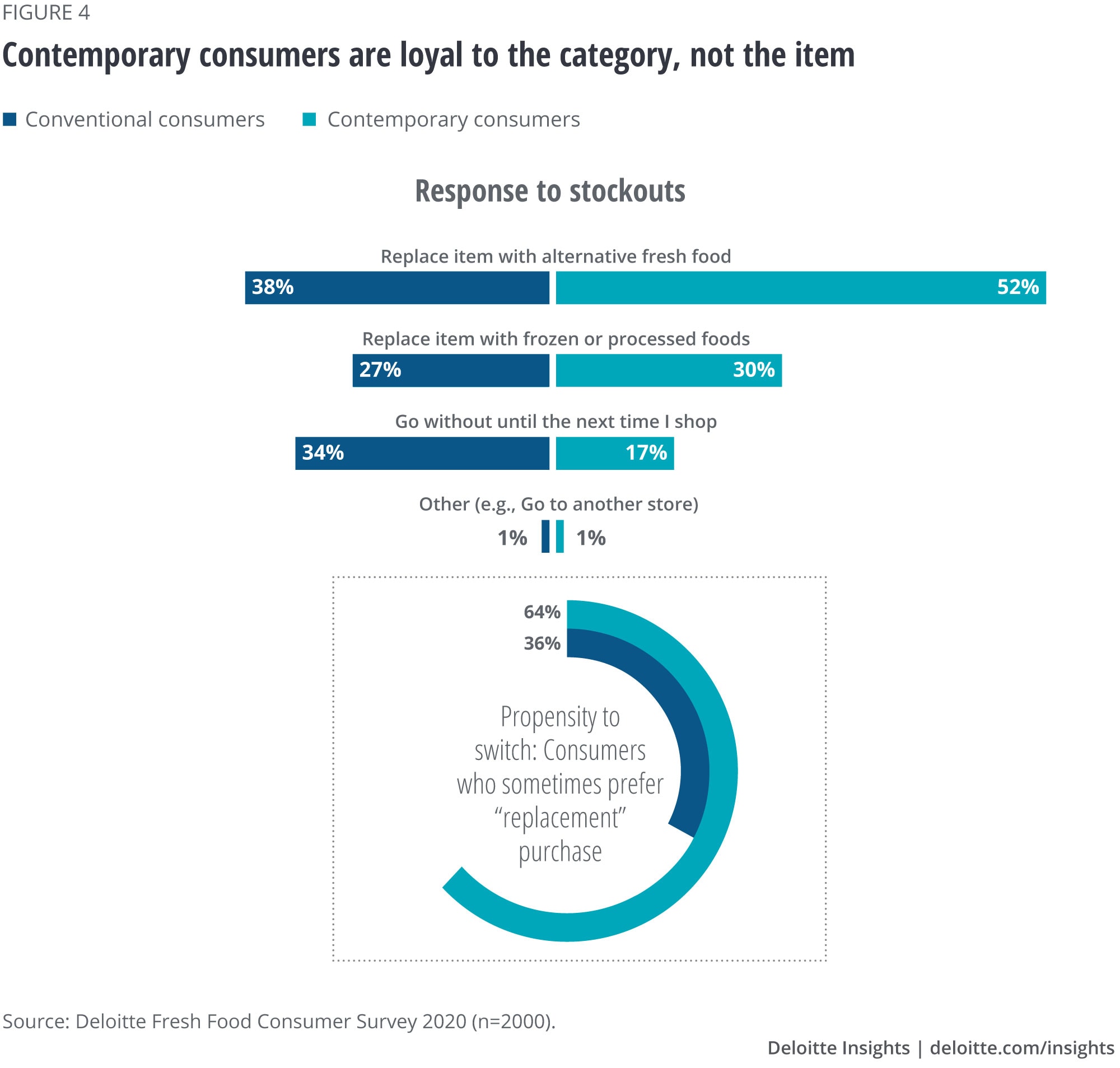

Through both stocking up and stockouts, consumers bought different brands and types of food than they normally would have purchased. Figure 2 breaks down what respondents did when confronted with a stockout of a desired fresh food item. One surprising takeaway is that more than half of respondents left the fresh food category entirely through buying a frozen or processed replacement or going without a substitute. One thing they did not report doing is seeking the item out in another store during this same shopping trip. After all, they are keeping their store visits to a minimum.

Predicting what consumers are likely to purchase is essential to keeping food in stock. Sales data from this unusual period could point to “phantom trends” when there isn’t a good sense of the underlying causes and consumer preferences. When we asked consumers about their stockout replacements, about half said they sometimes prefer the replacement item. So, these new preferences could stick even when the originally preferred fresh product is again available. Without taking these propensities into account and building a more complete view that includes external data for context, analytics systems may point in the wrong direction.

Predicting what consumers are likely to purchase is essential to keeping food in stock.

Changing what they value

Price is still king when it comes to consumer purchase drivers—90% of respondents in both 2019 and 2020 indicated that this traditional purchase driver was important. However, a new factor safety—that until now was just expected and not part of consumer concerns—has essentially tied with price for first place. Safety has multiple dimensions based on strength of response to several questions in the survey. It includes safety for self, others, and the workers who produce food, as well as safety in terms of packaging to prevent contamination—each of these drivers scored 85% or higher in importance to consumers.

A few other drivers—time-saving convenience, clarity in food labeling, availability of locally grown foods, concerns about sustainability, and concerns about food wastage—that were trending up in pre–COVID-19 times seem deprioritized, at least for the short term. While a wide majority of respondents still value them, respondents scored them lower and with lesser intensity (meaning, more people selected “somewhat important” instead of “very important” relative to last year). A recalibration of priorities on consumers’ part seems in tune with the present times. However, our message to the fresh foods producers is don’t be fooled. These drivers may not be as urgent as price and safety right now, but still are important to 70% or more of consumers surveyed.

Consumer personas remade by COVID-19

So far, we have covered aggregate-level findings. But all consumers are not alike, and the unique characteristics of specific consumer groups still should be addressed. In 2019, our study identified three distinct buyer personas based on consumers’ commitment to the fresh category: Forwards, Followers, and Neutrals.6 The world has changed since. The virus accelerated some patterns nascent in the Forward and Follower personas described at the time and brought forth others that could not have been anticipated. The Forward consumer especially provided some hints about the consumer we see today but, as we revisit the data from 2019, we do not see the same patterns and groupings that we see now.

As we revisit the data from 2019, we do not see the same patterns and groupings that we see now.

To discover our new consumer groupings, we conducted a statistical analysis based on responses relative to shopping frequency, amount of fresh food purchased, perceptions on price, channel usage, stress while shopping, and experience with stockouts. This uncovered two distinct consumer profiles—we call them Conventional and Contemporary.

How they shop and think, and what they value and buy are their most important attributes. But first let’s ground these two groups by the characteristic demographics associated with their patterns.

Two distinct consumer profiles

Conventional

- 60% of the survey group

- Tend to be older, lower-income, and more rural

Contemporary

- 40% of the survey group

- Tend to be younger families, more well-off, urban dwellers, and more ethnically diverse

While conventional consumers have a traditional approach to their fresh shopping, the contemporary consumers have a more novel approach. Industry veterans will already be familiar with many attributes of the Conventional consumer so here we focus on the Contemporary.

Understanding the Contemporary consumer

This group is a source of disruption and innovation for the fresh category. It is responsible for the much-discussed “accelerated trends” the industry is experiencing. Contemporary consumers are a younger group and, hence, personify the consumers of the future, and they already have more financial means at their disposal. Understanding the contemporary consumer and finding ways to specifically cater to them today can help hold off competition and unlock future growth.

Contemporary consumers value fresh more

The contemporary consumers’ outsized commitment to the fresh food category is evident in both tangible and intangible ways. Starting with the tangible, they are more willing to pay a premium for fresh food (75% versus 62% for conventional consumers). This appears to be a COVID-19–driven difference and not just a product of their being more well-off than conventional consumers—when compared to a like group of respondents with similar demographics from 2019, we see willingness to pay premium increased 6%. They also seem to be buying more. Contemporary consumers say they increased their fresh purchases in the last four months at a level almost double that of conventional consumers (50% versus 27%, respectively).

There are also less-tangible markers to how much they value fresh. We asked consumers if brand was important when buying fresh food. Sixty-four percent of contemporary consumers say it is important but only 44% of conventional consumers said so. This question was posed knowing that “brand” does not translate in the same way for a category such as fresh. For instance, it isn’t about whose sticker is on their apple or banana. Instead, it is a collection of attributes that define the brand of fresh. Or perhaps better said the idea of fresh or image of fresh. Looking at how contemporary consumers responded to other attitudinal questions, we see they value attributes, such as less pollution and waste, more than conventional consumers. They actively consider sustainability aspects such as local sourcing, recyclable packaging, and water neutrality while purchasing perishables (72% of Contemporary compared to only 51% of Conventional). Contemporary consumers seek out healthier alternatives and avoid preservatives at slightly higher rates. Sixty-six percent actively look for “non-GMO” labelling on the foods they purchase, relative to 46% of conventional consumers. Efficiently and effectively communicating these attributes to consumers is often a big challenge for the fresh foods industry.

Contemporary consumers are after a new kind of convenience

To the prepandemic consumer, convenience was primarily about saving time and effort. That has changed. Contemporary consumers seek a convenience that is less about time and more about stressfree availability. For them, the importance of quick meal prep and commute-related time savings has decreased. At present, many consumers have extra time at home and are not commuting. It is contemporary consumers who find shopping in-stores the most stressful and they are seeking out different ways to access fresh.

Contemporary consumers seek a convenience that is less about time and more about stress-free availability.

Where the conventional consumer is almost universally a grocery store shopper, contemporary consumers are using all channels (figure 3). Notably, 68% of this group bought at least some fresh food online versus only 9% of conventional consumers. Whether cause or effect, contemporary consumers ordering online place significantly higher trust in their assigned in-store shoppers to pick out the best quality fresh food items that are available in the store (68% of contemporary). That is a phenomenal development for a category such as fresh. This bodes well for overcoming what has typically been a major barrier to online adoption, as traditionally people like to select their own produce.

As further evidence of this desire for a new kind of convenience, contemporary consumers also show the most interest in subscription boxes (59% versus 26% for conventional consumers).

Contemporary consumers react differently to stockouts

When confronted with fresh food stockouts, contemporary consumers are more likely to stay in category (figure 4). Contemporary consumers value fresh more and this pattern further reflects that claim. When they do buy a fresh food alternative, they are still the least likely to go without purchasing something and are essentially just as likely as the conventional consumer to buy frozen or processed replacements.

Contemporary consumers often have an open mind for trying new products. They are much more likely to be satisfied with replacement items (64% versus 36% for conventional consumers), making them candidates for being nudged, inadvertently or otherwise, into forming new shopping patterns. As a result, their preferences may be more volatile, making predicting and planning more challenging if these tendencies aren’t properly taken into account.

Ideas for the way forward in fresh

Keep it fresh: With customers going longer between shopping trips, it is more important than ever that items be at their freshest when purchased. Collaborate more closely with your supply chain partners, consider intermittent deliveries and smaller shipment sizes, and use analytics to ensure that the least amount of time is consumed before the consumer takes the product home. That should aid in extending at-home shelf life as much as possible. In-store or online, actively guide customers to food that will last longest (relative to specific item expectations) past the day of purchase. This includes suggesting fresh food items to be consumed now and others that will still be good in “week number two.” The technology exists. If predictions are made accurate enough, one could imagine labels or signage indicating information such as “six days of freshness strawberries” or “10-day bananas.” Might customers also pay US$1/day instead of US$1/pound?

Avoid stockouts: This is somewhat obvious but more important than ever. For the consumer that is only going to shop in one store for the next two weeks, too many stockouts may cause them to take all their business somewhere else. Retailers and manufacturers alike are reducing stock-keeping units to focus on keeping core items in stock. But stockouts are inevitable, even if it is from just the turning over of the season. Knowing the patterns of both conventional and contemporary consumers, find ways to nudge them toward suitable replacements, even if that means a frozen or preserved alternative in some cases.

Build a fresh image: Find more ways to engage contemporary customers with the “brand” or “image” of fresh. Retailers might accomplish this by emphasizing fresh attribute messaging as a core part of their own brand. If done properly and backed by trusted and transparent supply chain management, customers may begin to feel that all fresh food bought in your store must have those attributes. Consumers can also be offered a capability to let them build digital profiles of their specific preferences around sustainability, local sourcing, etc. Phone apps can then help guide customers to items that have those qualities in-store and filters and recommendations can serve the same function when shopping online. Again, the technology already exists.

Innovate: Retailers are very good at promoting fresh food items that are in season and at the peak of quality to consumers shopping in-store through placement on endcaps, etc. Engaging online shoppers in similar ways is proving more difficult. For one thing, consumers often hit “buy again” and don’t consider additions. There could be an opportunity to leverage Contemporary consumers’ willingness to try and propensity to like new things, along with their trust of in-store assigned shoppers and interest in subscription boxes, to make purchase recommendations based on the grocer’s assessment of what is at the peak of quality on any given day. Like a virtual farm share box, online orders for select customers could be augmented with a selection of fresh food chosen by the retailer

Keep moving forward: As more people eventually feel safe shopping again, the industry’s first reaction may be to create promotions just to get customers back into stores. Instead, keep moving forward. The imperative should be to continue building the capabilities to connect with consumers in virtual settings. Whatever new models you wish to deploy, continue to invest in omnichannel access to better serve contemporary consumers. Manufacturers can help enabling these models by adapting supply chains as well as exploring their own direct-to-consumer models as another way of serving this demand for low stress, safe access. Contemporary consumers will likely pull the industry there eventually. It’s better to lead.

Supply Chain and Manufacturing Operations Consulting

Deloitte’s Supply Chain and Manufacturing Operations practice is a leader in helping companies integrate business strategy with supply chain initiatives to drive operational excellence. Our deep industry experience encompasses new product development, inventory strategy and integrated demand planning, sourcing and commodity management, manufacturing footprint strategy and operations, distribution network and logistics optimization, and sustainability. We employ programmatic approaches, leverage analytics capabilities, and offer managed services that can help improve top-line growth, lower costs, reduce response times, and increase productivity.

Learn more

Get in touch

- Barb Renner

- Partner

- Deloitte Tax LLP

- brenner@deloitte.com

- +1 612 397 4705

© 2021. See Terms of Use for more information.

Related content

More on the Future of Fresh

-

Solving the technology crossword in fresh foods Article4 years ago

Solving the technology crossword in fresh foods Article4 years ago -

Advancing the fresh campaign Article4 years ago

Advancing the fresh campaign Article4 years ago -

In an uncertain economy, does fresh produce spoil revenue growth? Article5 years ago

In an uncertain economy, does fresh produce spoil revenue growth? Article5 years ago -

The future of fresh Article5 years ago

The future of fresh Article5 years ago -

The future of fresh Collection

The future of fresh Collection