When asked about the emotions leaders associate with generative AI, excitement and fascination are common responses across regions. Still, European leaders report notably lower trust concerning the technology. This mistrust may stem from cultural differences and concerns about AI-associated risks like biases and copyright issues.4 European companies are focused on developing this new technology responsibly and ensuring its trustworthiness. They aim to balance the potential and advantages of generative AI with the need for it to be regulated. This means ensuring that AI systems are fair, impartial and accountable. They also want AI to be responsible, robust and dependable, while being safe and secure and protecting privacy and confidentiality. Emphasising ethical AI practices could help organisations avoid reputational risk and enhance trust among customers and employees.

High expectations for productivity amidst slow adoption of generative AI tools

European leaders in our study highlight efficiency, productivity, cost reduction, innovation and growth improvements as the benefits of generative AI, which mirrors global findings. These results are also consistent with previous reports such as the autumn 2023 edition of Deloitte’s European CFO Survey.5 A significant 91% of European respondents expect generative AI to increase productivity, aligning with global results. This is particularly significant for Europe, given the region’s recent productivity challenges, as highlighted by Deloitte Germany’s research into the economic effects of a shrinking workforce.6

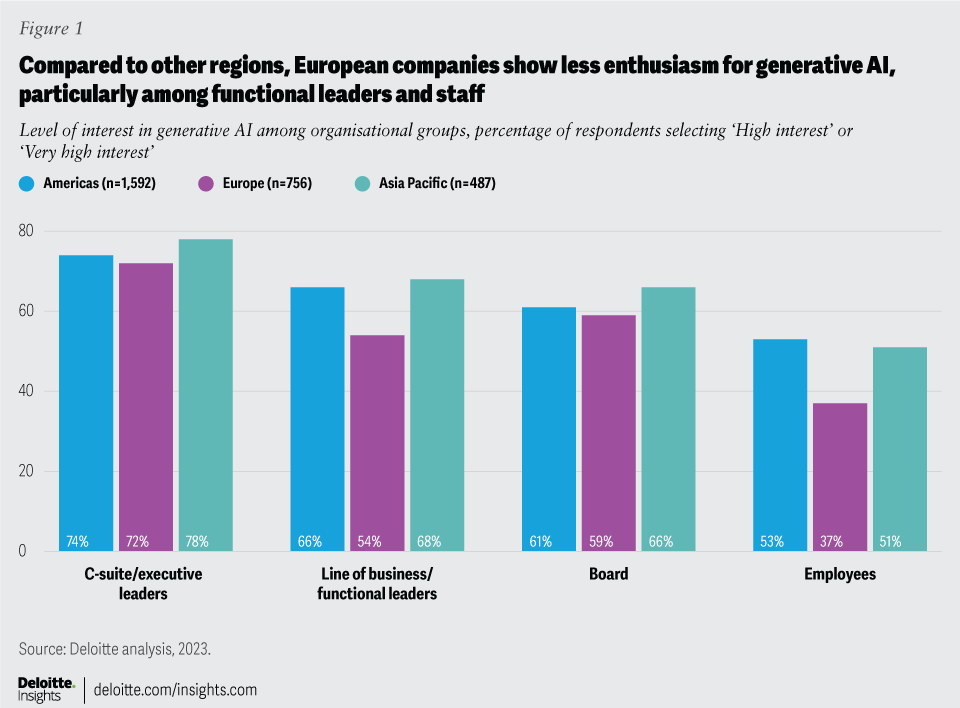

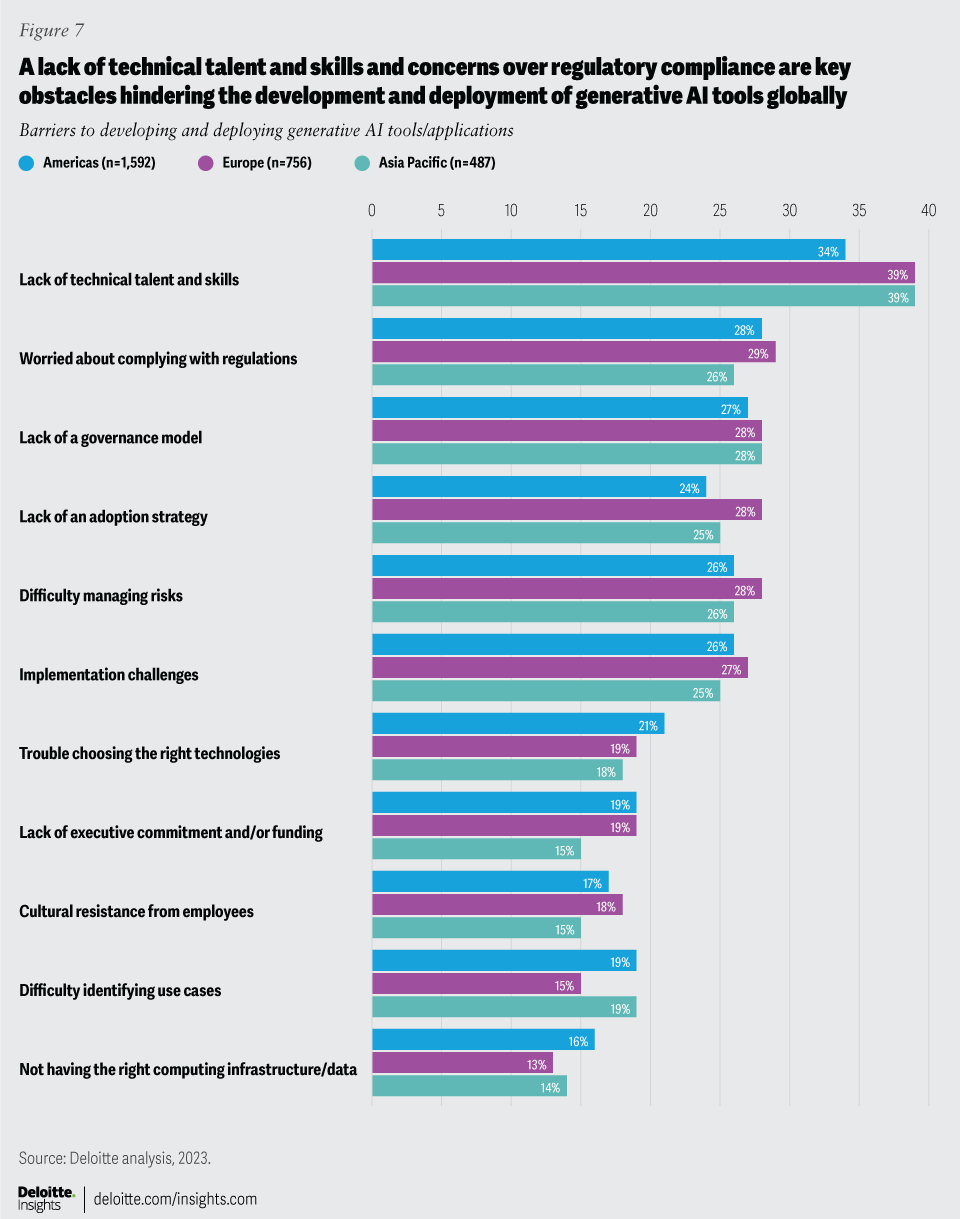

Despite such acknowledged benefits, European leaders face implementation challenges. Lower interest levels, trust gaps, slow implementation of governing regulation and expectations of longer timelines for generative AI–driven change hinder organisational investment in and readiness for these technologies. Compared to other regions, European leaders report less preparedness for adopting generative AI in business areas like risk management, strategy, talent development and technology infrastructure.

Similarly, generative AI adoption in Europe is lower across all business functions compared to other regions (figure 3). Alongside regulatory considerations, this may stem from Europe’s challenging economic conditions and ongoing geopolitical tensions impacting interest and slow adoption. The survey took place against a backdrop of a US economy that had outperformed expectations and in which growth had accelerated. In contrast, European growth had slowed sharply and Germany, although not the euro area as a whole, had fallen into recession. The US has also enacted policies to enhance economic competitiveness, such as the Inflation Reduction Act and the CHIPS and Science Act. However, this does not necessarily explain the higher levels of adoption in the Americas as the NextGenerationEU programme could provide similar incentives for European organisations to adopt generative AI.7

Lower levels of generative AI adoption are certainly a result of European companies operating in a more complex and regulated environment than their counterparts in the Americas and Asia-Pacific regions. In December 2023, the EU provisionally agreed on the EU AI Act, its landmark, world-first AI regulation, which will introduce a comprehensive, legally binding, cross-sectoral framework for the technology to regulate its use and development.

Using a risk-based but prescriptive approach, the law will regulate AI, including generative AI, based on the potential risks of specific models or applications. Certain AI use cases, such as behavioural manipulation, will be banned altogether. For AI systems and models deemed high-risk, organisations providing or deploying them will be subject to stringent requirements, including pre-deployment fundamental rights impact assessments, pre-market conformity assessments and transparency obligations, to name but a few.8 While the compliance implications are likely to be substantial, the Act will also bring more accountability and fairer distribution of responsibilities across the AI value chain, as well as increased consistency across sectors.

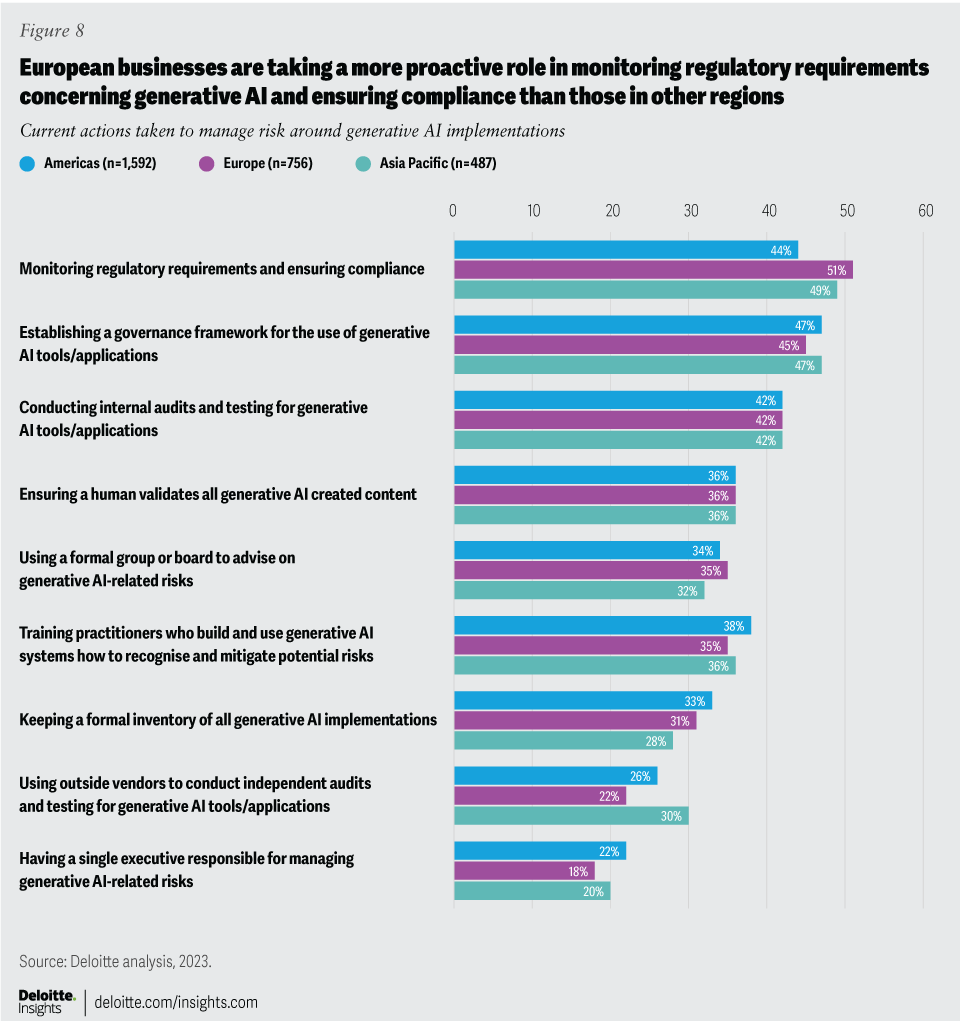

The Act will also have global implications, as it will apply to any AI providers or deployers whose systems are marketed or affect individuals residing in the EU, regardless of their location. The final legal text, expected in early 2024, will give organisations further details to fully assess the Act's operational and strategic impacts.9 It will be interesting to observe whether further clarity on the EU regulations will speed up the pace of implementation of generative AI in Europe.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}