The Leisure Consumer 2021

Emerging from the pandemic

The COVID-19 pandemic triggered profound changes in consumer behaviour almost overnight. Not only did the lockdown restrictions lead to a significant increase in in-home leisure activities, they also accelerated the shift to online. In normal circumstances, these changes, most notably the growth of online leisure activities, would have taken years and would have been the result of more gradual social and technological innovations. Using data from a survey commissioned by Deloitte, we have looked at how UK consumers will emerge from the pandemic and what it means for the leisure sector.

Highlights

- A strong recovery in consumer confidence paves the way for a resurgence in leisure activities

- Improving expected levels of discretionary spending

- High levels of pent-up demand bode well for a recovery in the leisure sector

- How did consumers spend their leisure time during the pandemic?

- Consumers intend to continue pursuing healthier and more environmentally sustainable lifestyle choices beyond COVID-19

- Beyond COVID-19: Four leisure consumer profiles

A strong recovery in consumer confidence paves the way for a resurgence in leisure activities

In March 2021, consumer confidence saw its biggest jump in the ten-year history of the Deloitte Consumer Tracker following the announcement of a road map for lifting COVID-19 restrictions, renewed support for workers and the successful rollout of the vaccination programme.

Consumer confidence is often used as an indicator of prospects for the UK economy. Consumer expenditure represents the largest component of gross domestic product (GDP) and in recent years has been its main growth driver. As a result, how consumers spend will determine to a large degree how the UK emerges from the pandemic-induced recession and what sort of recovery we get. In the UK, 21 per cent of consumer spending is on ‘socially consumed’ services, such as meals out, holidays and other leisure activities – the areas most affected by lockdown measures. For consumers to spend on these, they need to be confident about their personal financial circumstances.

Improving expected levels of discretionary spending

For the first time since the Deloitte Consumer Tracker survey began, net spending on discretionary items is expected both to become positive and also to exceed net spending on essential categories.

Consumer spending intentions in the next three months

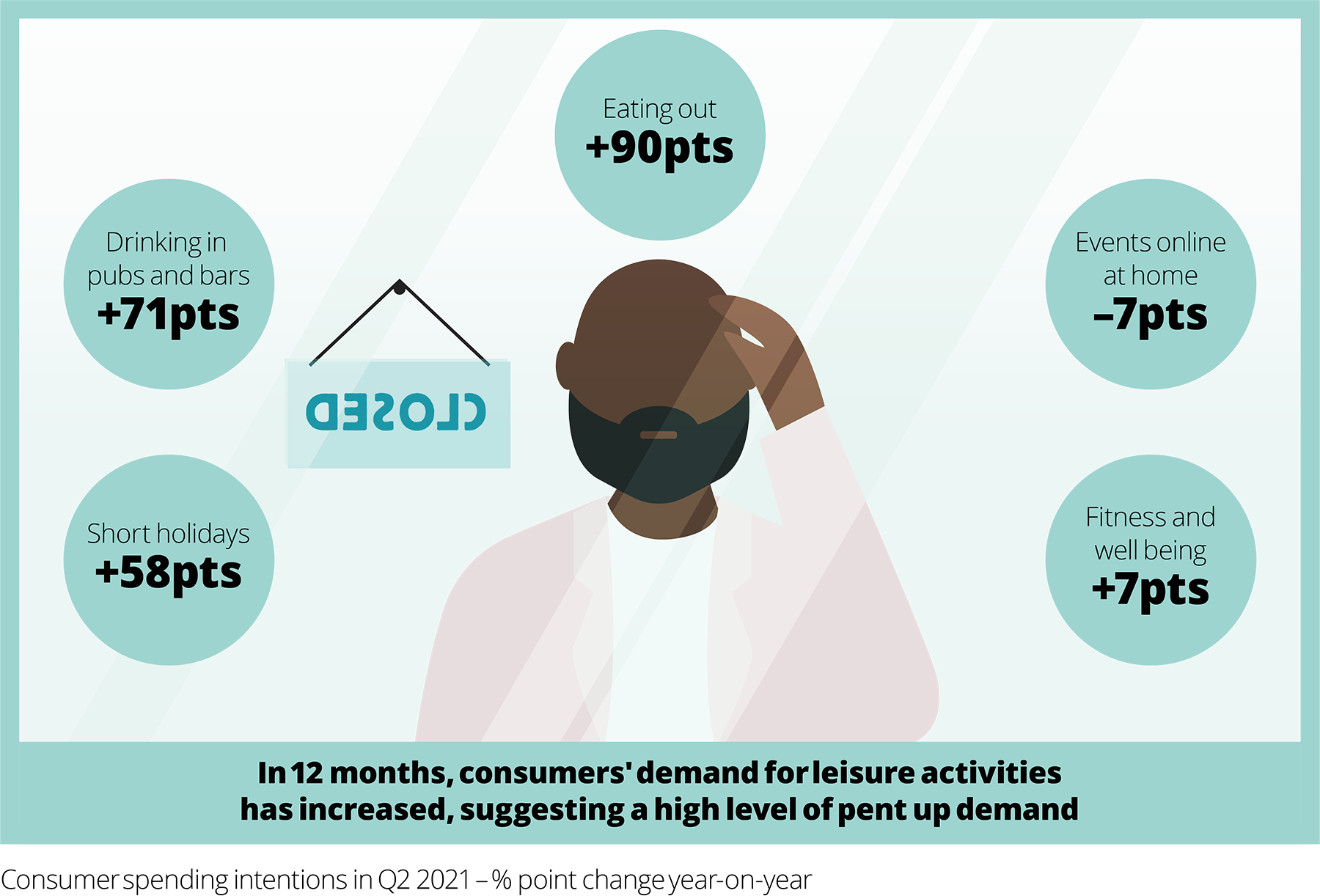

High levels of pent-up demand bode well for a recovery in the leisure sector

According to our data, intentions to spend on eating out in the next three months saw a 50 percentage point jump in Q1 2021 compared to Q4 2020 and a 90 percentage point increase compared to the same period in the previous year. Large increases were also seen in drinking out in cafes and pubs. Leisure activities, such as attending cultural events and going to the gym, also saw net spending climb.

How did consumers spend their leisure time during the pandemic?

While many found the new ways of socialising and spending their leisure time restrictive during the pandemic, others saw an opportunity to try out new things and do things differently.

Not surprisingly in the year since March 2020 people did one thing more than anything else − they socialised online. There was a 44 per cent net balance of consumers doing more socialising online compared to before the pandemic. While the majority of individuals will want to return to socialising in person, the possibility of staying in touch online has become more acceptable regardless of distance.

The home has also grown in importance, which is why the second highest growth activity in the past 12 months has been DIY projects, with a 24 per cent net balance of consumers doing more DIY than before the pandemic.

As people needed to find new ways of entertaining themselves at home, there was an increase in the total number of media subscription services with an 18 per cent net balance of consumers having subscribed to more entertainment services such as Netflix or Spotify.

With more time on their hands, people also reflected on their lifestyle before the pandemic. For a 17 per cent net balance of consumers, it meant making more environmentally sustainable lifestyle choices and for another 14 per cent net balance of consumers, it meant making healthier choices. Indeed, according to another recent survey by Deloitte, sustainability is now a key consideration for consumers, with 32 per cent of consumers adopting a more sustainable lifestyle.

Level of participation in leisure activities in the last 12 months compared to before COVID-19

Now thinking about the past 12 months (i.e. since March 2020), have you done more or less of each of the following activities compared to before COVID-19 (i.e. before March 2020), or have you done about the same amount?

Consumers intend to continue pursuing healthier and more environmentally sustainable lifestyle choices beyond COVID-19

When asked about their intended level of engagement with leisure activities in the year to March 2022 compared to the year before March 2020, a net balance of 19 per cent of consumers claim they will be making healthier lifestyle choices and a 14 per cent net balance aim to make more sustainable lifestyle choices. Throughout the pandemic, consumers were struck by two home truths: first that staying healthy is an important factor in fighting COVID-19 and second that the travel restrictions in place during the pandemic had a direct impact on improving air quality and reducing greenhouse gas emissions.

Consumers also plan to do more home improvement projects. According to our data, a net balance of 12 per cent of consumers expect to do more DIY projects in the year to March 2022. Respondents indicated that the reasons they wanted to take on more home improvement projects were that they enjoyed them and that they were better value.

Our survey also indicates that people are ready to return to face-to-face leisure activities. The net balances for many at-home activities were negative, meaning that on balance there are more people wanting to do fewer online leisure activities at home than those wanting to do more. These results point to a return to pre COVID-19 behaviours in the leisure sector.

Participation intention in leisure activities in the next 12 months compared to before COVID-19

And now thinking of the next 12 months (i.e. until March 2021), do you intend to do more or less of each of the following activities compared to before COVID-19 (i.e. before March 2020)?

Beyond COVID-19: Four leisure consumer profiles

To bring more clarity to the debate around which behaviours will stay beyond COVID-19 and how these will affect the leisure sector, we have developed a set of four profiles describing likely consumer behaviours, motivations and concerns.

The Reverter

Those who mainly want to return to pre-pandemic behaviours but seek to create a balance between the familiar and the new

Reverters look back at pre-pandemic times with nostalgia, and they miss the social and physical experiences of going to a cultural venue or restaurant. As a result, as soon as the restrictions are fully lifted, they expect to drop the behaviours they adopted since the onset of the pandemic and expect to take part in leisure activities as they used to before. Reverters will want to return to going out the way they used to but also recognise some of the benefits of the at home experiences and will want to enjoy a mix of both.

The Transformer

Those who are keen to maintain the lifestyle changes they have adopted and want more flexible options

Transformers want to continue with the lifestyle changes they adopted during the pandemic. Having changed their personal and work life experience in the past year, they have found more benefits than disadvantages to their new lifestyle. Transformers show greater focus on health and well-being and are likely to take part in activities such as fitness, yoga and sports. They have enjoyed the convenience of online platforms and the ability to build new virtual social networks. Environmentally sustainable and ethical practices will be increasingly important for them. Transformers want more choice and flexibility from businesses to maintain their new lifestyles.

The Whatever

Those who managed to maintain the status quo despite the COVID-19 restrictions and want to keep it that way

Whatevers have managed to maintain the status quo, not letting the pandemic affect them. They did not alter their lifestyle much beyond what the restrictions required. They see the pandemic as a temporary crisis that they must deal with, but not as something for which they should alter their habits drastically. They were less likely to have engaged in some of the at-home leisure activities in the past year and they do not intend to engage in such activities in the future either. They want to continue going about their lives with minimum disruption.

The Worrier

Those who have concerns about the future and seek reassurance, affordability and convenience

For Worriers, the fear of the unknown forces them to hedge against the perceived health and financial risks. They built a safety bubble around them using digital services to interact with other people and businesses, out of fear of contracting the virus. They are savers and will be reluctant to spend on larger purchases. Worriers are more likely as a result to experiment as a result. They want solutions that offer safety, support and protection, as well as affordability and convenience.

About this research

The consumer data featured in this report is based on a survey carried out by independent market research agency, YouGov, on Deloitte’s behalf. This survey was conducted online with a nationally representative sample of more than 3,000 UK adults aged 18+ between 19 and 23 March.

Some of the figures in this report show the results in the form of a net balance. This is calculated by subtracting the proportion of respondents that reported doing less of something from the proportion that reported doing more of the same thing. For instance, assume that 30 per cent of respondents reported they are spending more, 50 per cent reported no change and 20 per cent reported they are spending less. The net balance is calculated as 30 – 20 = 10. This means 10 per cent of consumers reported that they spent more rather than less.

Download the report

DownloadOther relevant research

The Deloitte Consumer Tracker

Consumer confidence saw its highest jump for ten years following the announcement of a road map for lifting COVID-19 restrictions, the chancellor’s renewed support for workers and the vaccination programme remaining on track.

Shifting sands: Are consumers still embracing sustainability?

How 2020 shaped consumers’ behaviours and attitudes to sustainability.

What next for the high street?

In 2014, Deloitte published research and analysis predicting it would be the high street rather than shopping centres or retail parks that would prove most resilient over the coming years. We revisit our optimistic prediction.

Contact us

If you would like to discuss any of the topics raised in this report, or find out more about our services, please contact our leisure sector team specialists:

Simon Oaten

Lead Partner, Leisure sector

Alistair Pritchard

Lead Partner, Travel & Aviation sector

Andreas Scriven

Lead Partner, Hospitality sector

James Yearsley

Lead Partner, Transport, Hospitality & Services sector

Céline Fenech

Research Manager

Anjusha Chemmanur

Insight Manager