Birmingham Crane Survey 2024

Still open for business

Key findings

Market summary

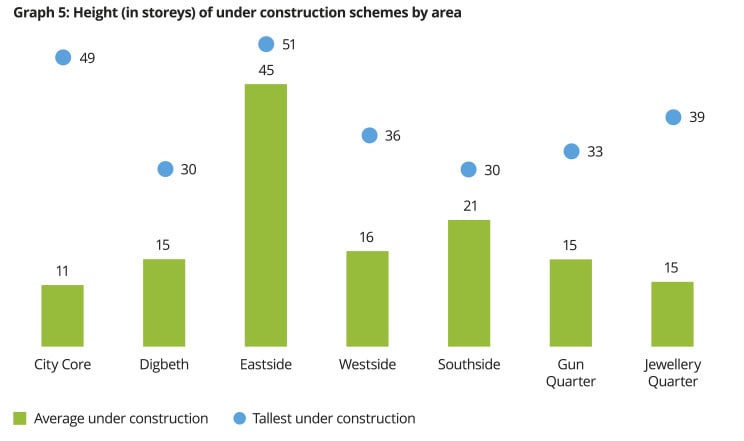

It has been an excellent year for Birmingham despite some of the challenges it has faced. The city is a hive of activity, with construction at historically high levels, building on the success of 2022. Development in Birmingham continues to stand tall, reaching new record heights at 51 storeys.

It is important to acknowledge the economic conditions that have cast a shadow over the construction industry in 2023. At the close of the year, the outlook for geopolitics, oil prices, inflation, and interest rates remained uncertain.1 This uncertainty is compounded by important national elections due in 2024, in the US, some EU member states, and in all likelihood, the UK.

Birmingham also faced challenges at a local scale in 2023. In September, the City Council served a Section 114 notice, effectively declaring bankruptcy. Following the issue of the Section 114 notice,2 Prime Minister Rishi Sunak also announced in October 2023 that the High Speed 2 railway project would no longer run from Birmingham to Manchester.3

However, our survey data indicates that this has not impacted the construction industry in 2023 and that Birmingham is continuing to show resilience and adaptability in the face of adversity. The city has demonstrated its adaptability in the past. Birmingham’s rich urban tapestry is testament to that. Despite the headwinds, 2023 has been another strong year for the construction industry in Birmingham, with 20 new starts across 19 schemes and with 44 total schemes under construction across 46 sectors, one more in each category than in 2022.

Construction activity in Birmingham continues to be led by the residential sector, with 31 residential-led schemes currently under construction, far outpacing other sectors, where nine office, three student residential, one hotel, one healthcare, and one education development are also underway. This signals that, despite the financial and economic challenges facing the city, investor confidence remains strong.

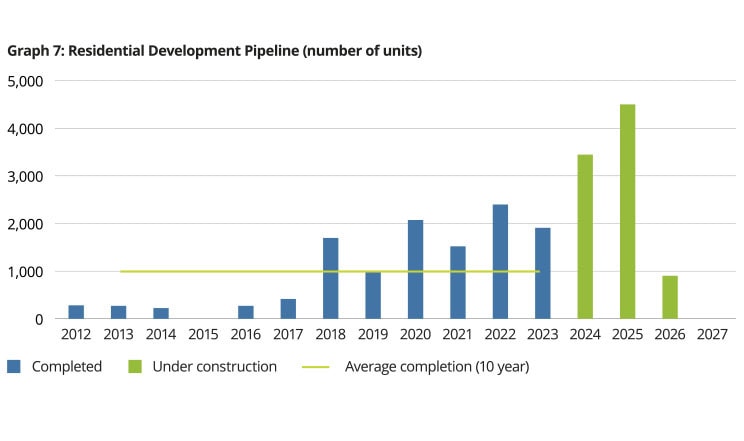

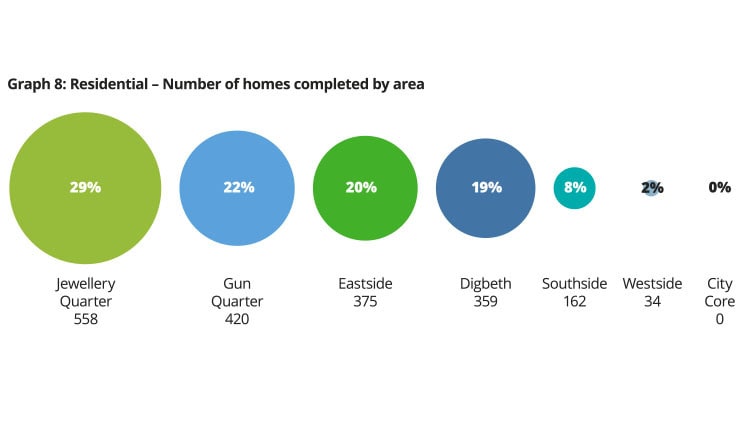

1,908 homes were completed in 2023, down from 2022’s record-breaking total of 2,398. The Jewellery Quarter delivered the most homes in 2023. The 558 homes completed here made up 29% of all homes completed in the Crane Survey area.

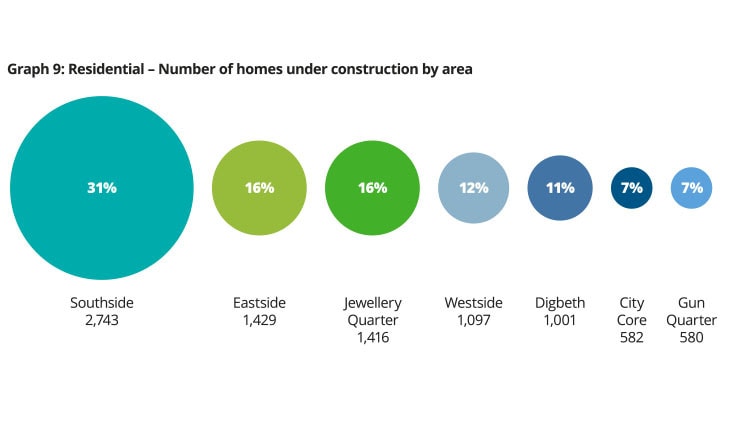

Birmingham's impressive track record of delivering homes may not have been exceeded in 2023, but the city's pipeline of homes is at the highest ever level recorded by our Crane Surveys. With 8,848 homes currently under construction and set to be delivered over the next three years, the demand for city-centre living in Birmingham shows no signs of slowing down. In fact, projections suggest that 2024 and 2025 are poised to outperform 2023. Southside is the hub of this activity, as the area with the most homes under construction, at 2,743.

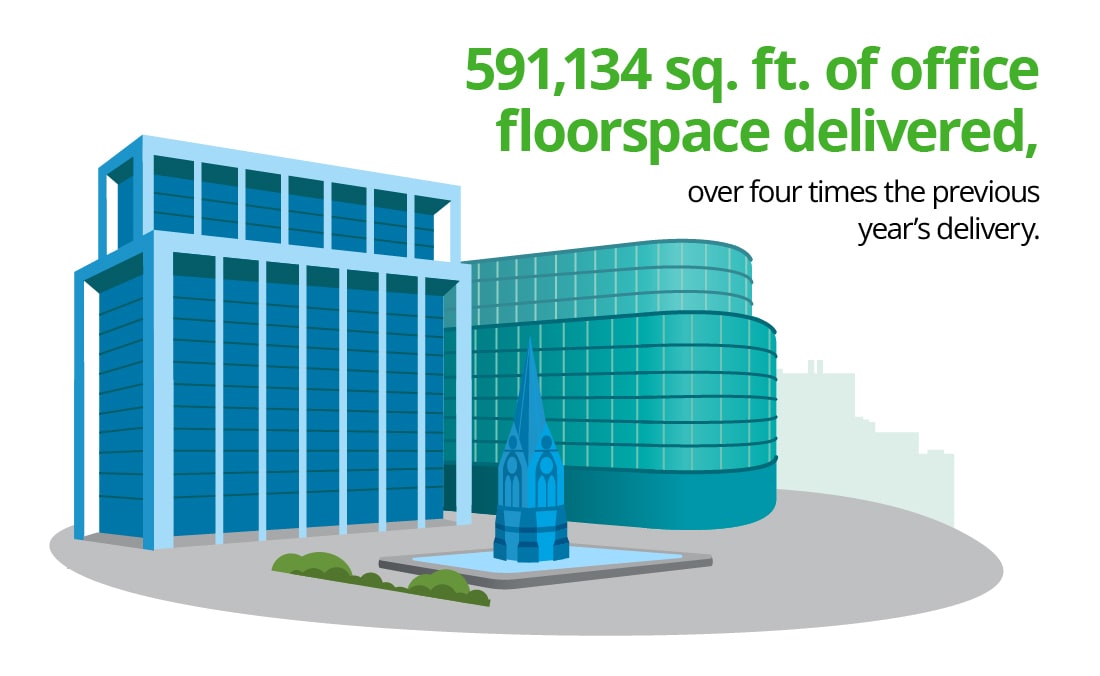

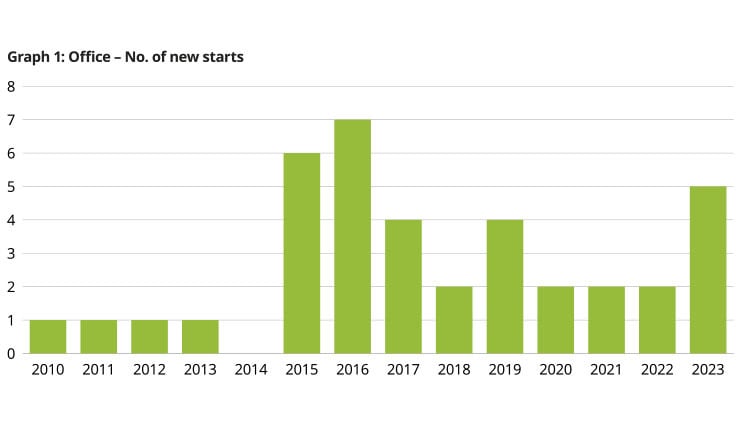

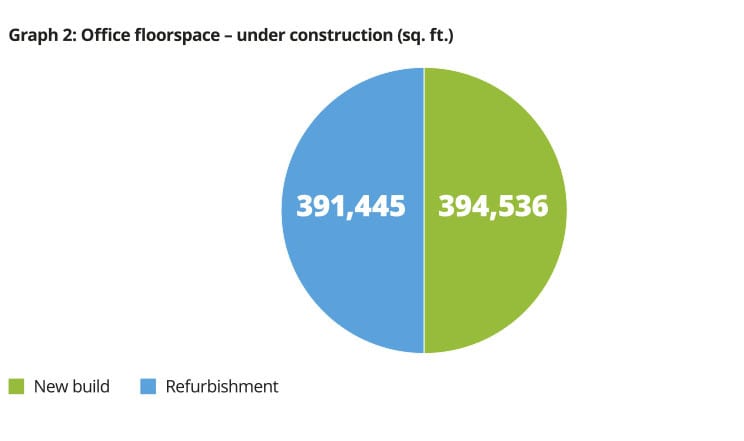

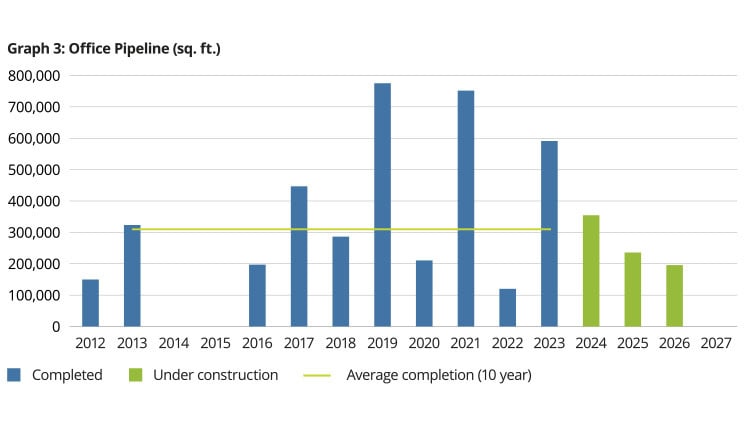

591,134 sq. ft. of office floorspace completed in 2023, over four times the total recorded in 2022. 785,981 sq. ft. of office floorspace is under construction across nine schemes, including major refurbishments. This represents a decrease of just nine per cent from the 866,969 sq. ft. under construction the previous year. No year since the outbreak of the COVID-19 pandemic has reached the 2020 level of over 1 million sq. ft. under construction. Notably, six of the nine office schemes are major refurbishments. This could represent the market’s continuing adaption to post-pandemic working practices.

Last year, we predicted that we would soon have a 50+ storey building under construction. New start, One Eastside, will top out at 51 storeys, surpassing the 2022 record for the tallest building under construction, previously set by the Octagon at 49 storeys. Back down at ground level, however, and retail-led new starts were absent for the fifth consecutive year, although 120,258 sq. ft. of retail floorspace will be delivered as part of mixed-use developments, an increase over 2022.

The city captured the world's attention as host to the 2022 Commonwealth Games and is now executing its legacy game plan. However, attracting investment since the Games is a marathon, not a sprint. Birmingham has secured its role as host to several new major sporting events, such as the European Football Championship in 2028 and the city continues to deliver the legacy through funds and grants.4

The hotel industry will be playing its part by providing hospitality to visitors: 409 hotel rooms were completed in 2023 across two schemes and 229 rooms are currently under construction. Eight additional schemes with the potential to deliver a further 1,070 rooms are also in the running, either at planning stage, with planning permission, or undergoing demolition.

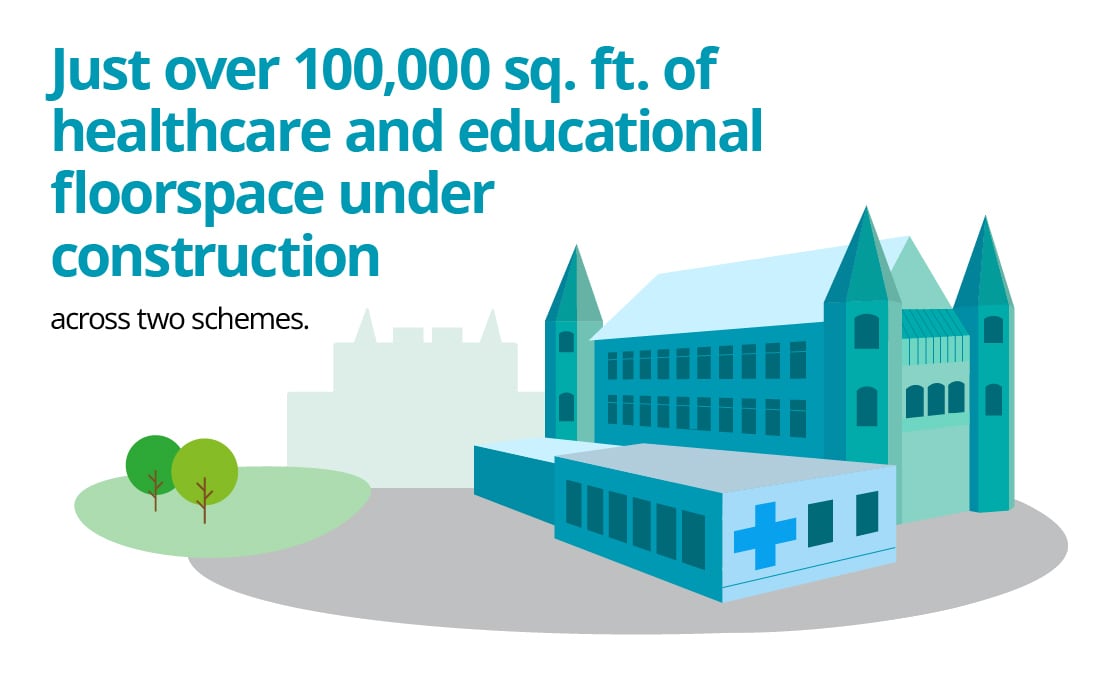

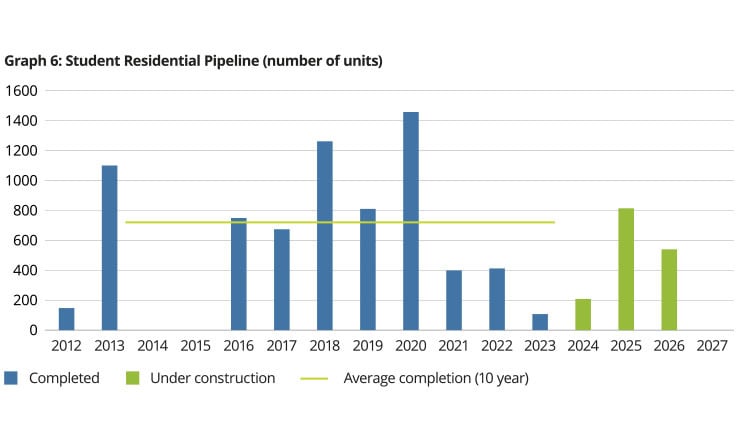

It is not just visitors that Birmingham is attracting from across the world, it is firmly established as a leader in world-class education, with three leading universities located within the city centre and the boundary of our survey. University College Birmingham and Birmingham Children’s Hospital are upgrading their facilities, with a combined 102,223 sq. ft. of education and healthcare floorspace currently under construction. Provision of accommodation for the growing number of students in the city is also on the increase. Three new student residential schemes started construction in 2023, bringing the total number of units under construction to 1,562 – 15 times more than in 2022.

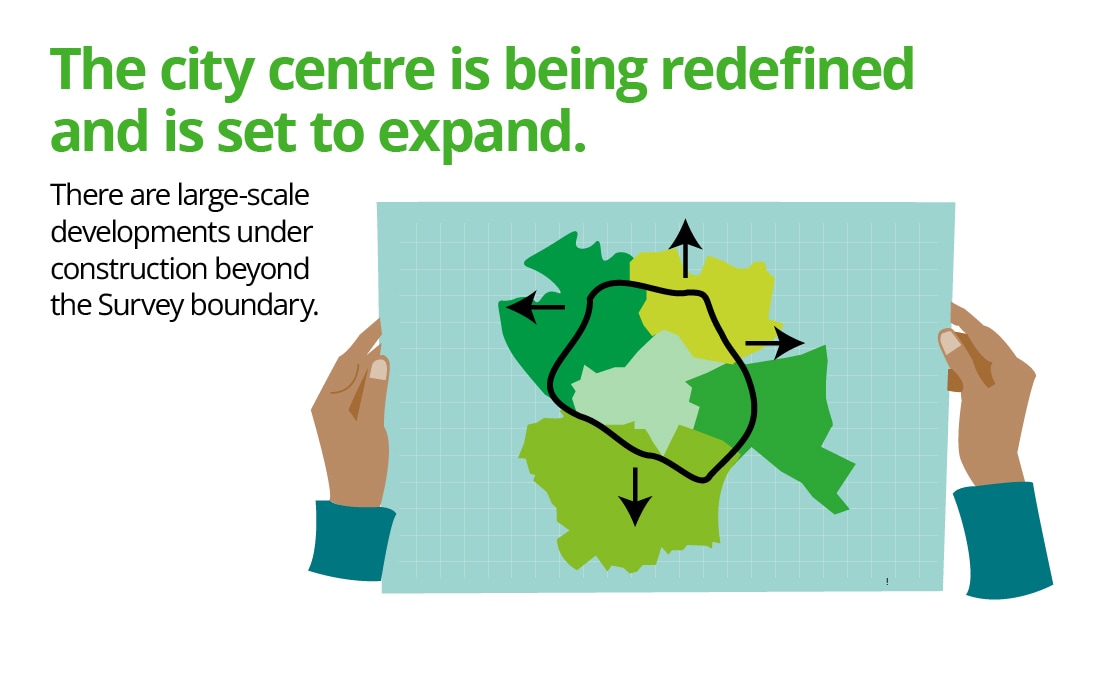

Despite some economic adversity during 2023 and despite the limits of our survey boundary, our data is showing that Birmingham is still very much open for business. What we have not captured in our data, are the developments under construction outside the geographical boundary of our survey, which focuses on developments within the city centre, as currently defined by the Middleway ring road. But, with Birmingham City Council’s publication of the draft Our Future City Framework for consultation in 2023, the city centre is being redefined and is set to be extended. The developments both within our survey boundary and beyond demonstrate growth and resilience in the construction sector across the city.

Still open for business

Although the city faces challenges and obstacles must be navigated moving forward, our Crane Survey reveals that Birmingham is still very much open for business. The city is successfully attracting and retaining new office occupiers, proving its status as a thriving commercial hub.

Central to success

Office floorspace is performing well in established central locations, including Westside and the City Core. 591,134 sq. ft. of office floorspace was completed in 2023, across three schemes in the City Core and Westside. This is over four times the quantum delivered in 2022. Unsurprisingly, the phased Paradise development continues to add to the office floorspace figures in the City Core, with the completion of One Centenary Way contributing 335,134 sq. ft. The building has attracted high-profile tenants, including Goldman Sachs, commercial property firm JLL5 and consultancy Arup.6

Delivery of Paradise Phase 2 continues. Three Chamberlain Square was a new start in 2023 and is set to contribute a further 189,000 sq. ft. of office floorspace to the market. It will be the first net-zero carbon development within the Paradise Masterplan and is the first building in the West Midlands to earn a BREEAM Outstanding rating at design stage for its sustainability credentials.7

Three Chamberlain Square is one of five new starts for office developments in 2023, an impressive increase from the two new starts in each of the three previous years 2020-2022.

Within our survey area, 785,981 sq. ft. of office space is currently under construction, largely in the City Core but reaching out to new office hotspots such as Digbeth. This is close to the 866,969 sq. ft. of office space under construction at the time in 2022, representing a drop of just nine per cent. Looking ahead, several schemes are on track to complete in 2024, with the potential to deliver an additional 354,493 sq. ft.

Succeeding with creativity

Digbeth, already an established creative industry hotspot, is now attracting media industry attention. In 2023, the vision of renowned director and Peaky Blinders creator, Stephen Knight, for the Digbeth Loc Studios8 masterplan started to be realised. It was lights, camera, action for the former Banana Warehouse, a new start which will provide a hub for the Shine TV and BBC produced MasterChef relocating from London.9

We are likely to see further activity in the media sector in next year’s survey with the forthcoming Typhoo Wharf refurbishment, which was granted planning permission in 2023. The BBC will be the anchor for the scheme and is set to move production to the historic refurbished industrial building in about 2027. Typhoo Wharf will house several editorial teams, including those for The Archers, BBC Asian Network, BBC Newsbeat, BBC Radio WM and Midlands Today. These developments will cement Digbeth’s identity as a dynamic hub for the creative industries and the growing media sector in Birmingham.

The ongoing Eastside Metro extension is adding to the construction activity in Digbeth, increasing the connectivity of the area. This is likely to give developers and potential occupiers the confidence to commit to investing in Digbeth.

Making connections to succeed

Underlying the stimulus for growth in commerce and business in Birmingham is investor confidence in its plans for public transport expansion. This will increase connectivity not only across the metropolitan area, but also regionally and nationally.

In October 2023, it was announced that the West Midlands will receive £9.7 billion in investment through the government’s Network North plan, designed to redistribute the costs saved from shortening the route of HS2. £1.75 billion of this money will go to delivering the Midlands Rail Hub to improve rail service and capacity.10 Coupled with this ambition, £60 million in funding has been awarded to Transport for West Midlands to deliver an extension of the metro from Wednesbury to Brierley Hill on the outskirts of the city.11 This is part of the Deeper Devolution Deal funding, intended to expand connectivity across the city region.

Looking ahead, and beyond our current survey boundary, we are starting to see hotspots of activity in the office sector in areas of improved connectivity. For example, Calthorpe Estate’s New Garden Square in Edgbaston benefits from the new Westside Metro extension and could deliver over 600,000 sq. ft. of office floorspace.

The performance of Birmingham’s office sector is not just about connectivity, but is also about making connections. In 2023, several major partnerships were announced. In May, the West Midlands Combined Authority announced a strategic partnership with SEGRO, with the aim of delivering 14,000 new jobs and 13.5 million sq. ft. of employment space throughout the West Midlands. In October, the central government announced Birmingham’s selection as the location for a future civil service hub for the Department for Transport and National Highways and others.12 The hub will house up to 4,000 civil servants and will open by 2028 as part of the Places for Growth initiative to relocate civil servants outside London.

2023 has therefore demonstrated that the city continues to leverage its central geographical location, connectivity and creativity to attract both the public and private sectors, including the creative industries.

Renew, not new!

In addition to new buildings, 2023 was also a year for office refurbishments, with six of the nine schemes under construction in our survey a refurbishment rather than a new build. This partly reflects a continuing post pandemic trend, where the office sector is striving to adapt to new ways of working and occupier demands for collaborative and flexible spaces. It also reflects growing industry recognition of the value of carbon capture in development. Of the refurbishments in our survey, a common theme is the aim to minimise embodied and operational carbon use and to embed green technology. These initiatives will support Birmingham City Council’s objective of achieving net-zero carbon emissions by 2050 to combat the effects of climate change.

Grosvenor’s refurbishment of 134-138 Edmund Street in the City Core is currently underway and will retain the Grade II-Listed façade and deliver 121,094 sq. ft. of Grade A office space. This refurbishment focuses on increasing biodiversity on the site and bolstering the sustainability credentials of the structure through measures such as enhanced heating and cooling systems.13

Looking ahead to the pipeline of office schemes that are not yet under construction, another notable refurbishment will be 125 Colmore Row, where Lloyds Banking Group has plans to refurbish its headquarters, boosting its sustainability credentials through implementation of new heat pump and water use monitoring systems designed to reduce carbon emissions, as well as electric vehicle charging points and enhanced cycle parking space.14 In the interim, the firm has taken up nearly 60,000 sq. ft. of flexible office space at The Foundry in the existing office hub Brindleyplace, in the largest flexible office market transaction for 2023 outside London.15

Looking not just at refurbishment, but also at change of use, another major scheme is The Drum, located within the former John Lewis department store at New Street Station. This will deliver 198,454 sq. ft. of office space alongside a cinema, music venue and drinking establishments. Planning consent for this change of use from major department store to office was granted in 2023 and contributes to a national dialogue around the future of large floorplate retail assets. Could we see a future trend where department stores in city centre locations are converted from retail into more viable uses, such as office, in a post-pandemic world?

The current office developments in Birmingham and those in the development pipeline demonstrate Birmingham’s growing prominence as a national office hub. Two schemes in the City Core are awaiting planning permission, with the potential to deliver a further 422,841 sq. ft. of office space, if approved. Planning permission was granted in 2023 for an additional 539,453 sq. ft. of office floorspace in three schemes across the City Core, Digbeth and Westside. Central and connected locations, partnerships and the thriving creative sector are all contributing to the strong results in 2023 for office floorspace in the city.

Implementing the legacy

The legacy of the Commonwealth Games in Birmingham in 2022 has left a definitive spirit of sport in the city. Over five million visitors to the city centre during the Games representing a twofold increase over 2021. These visitors spent £14.1 billion, 41% of which was on retail products.16

In light of these benefits from the visitor economy, the city has moved ahead to enhance its international reputation in sport. In the summer of 2023, Birmingham hosted the British Squash Open, as well as the International Blind Sport Federation (IBSF) World Games, which drew over 1,000 competitors from more than 70 nations to the city.17

The city will become the first UK location to host the European Athletics Championships in 2026, and Aston Villa Football Club was announced as a future host of the 2028 Euros football cup. The club is preparing with plans for a £100 million stadium expansion and new facilities for fans.18 To the south of the survey area, Edgbaston Cricket Stadium has progressed its masterplan which includes 160 Build to Rent units completed in 2023, and may include a hotel in the forthcoming Phase 3.19 The stadium will be looking to capitalise on the 2026 International Cricket Council (ICC) Women’s T20 World Cup and the 2030 ICC Men’s T20 World Cup, both being held in the UK. These major developments will deliver economic benefits, enhancements to infrastructure and community facilities, provide new commercial floorspace and, in some instances, new homes.

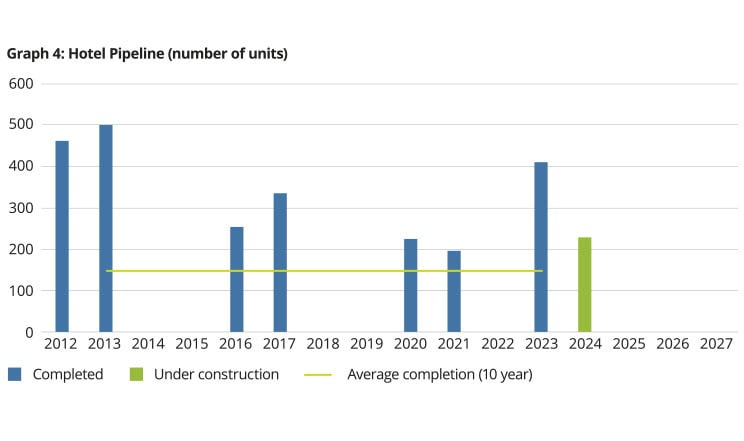

Sport has the potential to act as a catalyst for further development and economic uplift. Wider economic benefits of sports-led development are felt by the community over the longer term, but the economic benefits of a sporting event are felt in the short term by businesses serving the visitor economy. During the Commonwealth Games in 2022, hotel occupancy in Birmingham averaged 90% capacity.20 Our survey data suggests that Birmingham’s hotel market is expanding in preparation to host upcoming sporting events and accommodate visitors from around the world.

No new hotel schemes broke ground in 2023, but 409 hotel beds were completed during the year across two schemes: the Aparthotel on St. Chad’s Queensway in the Gun Quarter, and the Silveryard mixed-use scheme in Eastside. The pipeline remains strong, with 229 hotel beds currently under construction at the residential-led Cortland, Broad Street in Westside. In addition, a further 1,070 hotel beds within the survey area are either at demolition stage, planning stage, or have planning permission.

The legacy of the Commonwealth Games extends beyond its visitors, providing tangible benefits for Birmingham’s residents. In November 2023, the WMCA and several partners announced that £9 million of legacy funding from the Commonwealth Games would be distributed to funding grassroots projects across the West Midlands. Known as the Inclusive Communities Fund, this money will be granted to projects which promote a positive impact for mental and physical health and community cohesion.21 This circular investment back into the community could enhance public sentiment and support for hosting further events in the future, thereby increasing the appetite for development and the infrastructure (including hotels) necessary to facilitate their delivery.

The sky is the limit

Birmingham’s changing skyline is contributing to the city’s international profile. In 2022, the tallest building under construction in Birmingham was the Octagon at 49 storeys. A new record has now been set by Court Collaboration’s One Eastside, a 51-storey Build to Rent tower which broke ground in 2023. Eastside is a focus for tall buildings in Birmingham, with the average height of new builds under construction at 45 storeys. This race to the top is showing no signs of ending. Planning permission was granted in April 2023 for Woodbourne Group’s Curzon Wharf scheme in the Gun Quarter, which will provide 620 residential units in a 53-storey building, and a planning application has been submitted by Urban Vision for a 61-storey residential-led scheme at 100 Broad Street in Westside. The tower would deliver 294 Build to Rent units and, if approved and implemented, would become Birmingham’s tallest building.

These tall buildings are redefining Birmingham’s international profile as a major urban centre and destination.

Grassroots talent and innovation

It is not just the changing skyline, sports and sporting legacy that are raising Birmingham’s international profile. There are five universities in Birmingham, three of which are within the city centre, attracting talent in students and academics from the UK and beyond.

Only 107 student residential units were completed in 2023. However, three student residential developments started construction in 2023. Together these will deliver 1,562 student beds between 2024 and 2026 within the City Core and Gun Quarter, areas easily accessible to the city’s universities. The student population has increased in the city,22 and the market is responding. A further 4,846 units are either at the planning stage or have planning permission but these schemes are yet to be implemented. Looking beyond our survey boundaries, the pipeline figure becomes more impressive – with over 1,000 units in the ‘Central South’ area (which redefines and extends the city centre into Edgbaston).

The education, knowledge and healthcare sectors are also delivering.

The masterplan for the Birmingham Knowledge Quarter, released in May 2023, proposes a new ‘innovation cluster’ of educational, office, and other venues delivered by a partnership of Bruntwood SciTech, Aston University and Birmingham City Council, near to Aston University.23 In his Autumn Statement delivered in November 2023, Chancellor Jeremy Hunt recognised the Birmingham Knowledge Quarter as a key driver for growth within the proposed West Midlands Investment Zone. It is anticipated that this Investment Zone could bring £3.5 billion of additional investment to the region.24

This is matched by other initiatives designed to establish the city as a leader in health research and technology. The Birmingham Health Innovation Campus in Selly Oak is being delivered through a partnership which includes the University of Birmingham, Birmingham City Council, the NHS in Birmingham, and Bruntwood SciTech. The first phase of the development is set to open in Spring 2024 and offers 130,000 sq. ft. of research and development and office floorspace. It is intended that this campus will attract start-ups and global corporations alike in the areas of medicine, healthcare, and medical research.25

Currently underway in the Jewellery Quarter, the new Engineering and Sustainable Construction Centre for the University College Birmingham is set to deliver 54,712 sq. ft. of educational floorspace by 2024. Meanwhile, in the city core, construction began in late 2023 on a major redevelopment of Birmingham Children’s Hospital to deliver 47,511 sq. ft. of improved healthcare facilities.

Housing delivery continues to break records and boundaries

In the residential sector, 2023 has been another record-breaking year, as well as a boundary breaking year, signalling continued strong performance in this market which we expect to continue into 2024.

Breaking records

In 2022, Birmingham broke the record for the highest number of homes completed. Completions were down by 20% in 2023, but despite this dip, the city has put in an impressive performance, with a record-breaking number of homes under construction. 8,848 homes are under construction, an uptick of 36% from the 6,487 homes under construction in the survey area in 2022.

This pipeline of homes is being brought forward across 31 residential-led schemes currently under construction, down from 32 in 2022. There were 11 residential-led development new starts, as against 13 in 2022. However, with the city reaching for new heights, higher density development is helping to deliver more homes over fewer schemes in the city centre.

The Jewellery Quarter recorded the highest number of residential completions for 2023, at 558 homes. The majority of these were delivered through Blackswan Development’s The Goods Yard, which brought 395 Build to Rent homes to market. Tracking slightly behind, the Gun Quarter delivered 420 homes, and Eastside 375 homes.

Southside saw the most construction activity in the residential sector in 2023 with 2,743 homes under construction. Tracking behind is Eastside and the Jewellery Quarter, with 1,429 and 1,416 homes under construction respectively.

The largest scheme under construction is in Eastside: this is Glasswater Locks from St. Joseph Homes, due to deliver 762 homes once complete. The second largest scheme under construction is Moda Living’s Great Charles Square in the Jewellery Quarter. Located on the site of the former Ludgate Hill Car Park, this scheme started on site in 2023 and will provide 722 Build to Rent homes once complete.

The housing pipeline is further bolstered by five sites undergoing active demolition and seven already cleared sites which are ready to break ground. Additionally, 20 residential schemes have been granted planning permission in the survey area but have not yet started on site. The three largest schemes to be granted planning permission have the potential to deliver a total of 3,873 homes once completed. Although not yet under construction, stay tuned for the potential delivery of 1,680 homes at the former Ringway Centre along Smallbrook Queensway in the City Core, 1,250 units at Digbeth Bus Garage, and 943 units at Upper Trinity Street in Digbeth.

Residential development in Birmingham continues to outpace other types of use in terms of quantum of delivery and the pipeline of schemes.

Digbeth, named by The Times as one of the ‘best places to live in the Midlands’ in 2023,26 is reinventing itself as a post-industrial hub for creatives and nightlife, with residential developments supporting its vibrancy. 1,001 homes are under construction in the area, 50% of which comprise Build to Rent homes as part of Goodstone Living’s Smiths Gardens in Camp Hill, where construction began in 2023.

The City Core remained relatively quiet, with no completions and 582 homes under construction in 2023. However, subject to planning approval, the proposals for the Smithfield Masterplan would provide a significant boost to the creation of a vibrant, sustainable and mixed-use city core. The proposals include 3,547 mixed-tenure homes, 0.8 million sq. ft. of supporting retail and leisure floorspace, nearly two million sq. ft. of office space, and over one million sq. ft. of education and healthcare uses. If approved, the delivery will take place in phases over eleven years. It will be a major regeneration project that redefines the character of Birmingham city centre.

Breaking boundaries

Birmingham is breaking the mould for delivering new homes. The city is exploring alternative routes to delivering homes to help it meet its ambitious housing targets, which include a commitment to deliver 51,100 new homes by 2031, 19,400 of which will be affordable.27 With significant population growth expected (150,000 more inhabitants by 2031), the future housing need is evident.

The Spring Budget in March 2023 has unlocked another new route to delivering much needed housing in the city. With up to £500 million awarded to the WMCA as part of the Deeper Devolution Deal, six growth zones were identified across Birmingham and the wider West Midlands.28 The funding will be used to accelerate growth in these zones through investment and regeneration.29 The WMCA will become the first metropolitan combined authority other than London with fully devolved powers to build affordable homes for residents.30

The region is also investing in partnerships, with the aim of encouraging innovation in routes to delivering homes. In July 2023, the WMCA announced that it had established a strategic relationship with housing developer Keepmoat to deliver a target of 4,000 new homes across the West Midlands. Sustainability is a core principle of this agreement, with Keepmoat targeting net zero emissions on brownfield developments.31

The private sector also has a role to play in breaking the mould. Macroeconomic forces have influenced the way that people want to live and experience living in the city centre, creating growing demand in the Build to Rent sector, to which the market has responded. The Build to Rent sector is no longer an alternative tenure in the city, but is the lead tenure in the market. In 2023, 61% of residential units delivered in the survey area were Build to Rent, whilst Build to Rent now represents 63% of units under construction.

Birmingham is also breaking its physical boundaries to support growth. The draft Our Future City Plan 2040 Framework, published by Birmingham City Council in 2023, redefines the city centre boundary. The Framework no longer sees the city centre as contained within the Middleway ring road. It extends the city centre beyond the Middleway ring road into four quadrants: Central North, Central East, Central South, and Central West, and we are seeing increasingly large schemes outside the ‘old’ city centre boundary.

The Central South area has several large-scale developments under construction, including Belgrave Village by developer Galliard Apsley, which will deliver 438 homes just south of the Middleway and Phase 1 of New Garden Square led by Moda Living which will deliver a further 392 homes in Edgbaston. In Central West, Soho Wharf, also from Galliard Apsley, completed this year and delivered 752 Build to Rent homes, and the multi-phase Icknield Port Loop regeneration area will deliver over 700 more homes.

Future outlook

In 2023, Birmingham proved itself resilient in face of political and economic challenges at both the local and national level.

Development activity maintained a strong upward trajectory, with growth led by the residential sector. Record-breaking housing numbers were under construction in 2023 and building density is increasing in the city centre. The pipeline for delivery of new housing remains strong, with the Build to Rent sector expected to continue to grow due to its popularity with investors.

The geographical reach of this residential development activity is expected to extend. Draft planning policy is proposing to re-organise the metropolis spatially, expanding it beyond its traditional boundary of the ring road into four quadrants. It is anticipated this will encourage regeneration beyond the boundary of the ring road, with development activity likely to pick up in inner city areas such as Bordesley Green, Edgbaston and Ladywood. These areas are also benefiting increasingly from investment in better public transport, enhancing local access to the city centre. Connectivity and regeneration go hand in hand. At the same time, major regeneration schemes such as the Smithfield Masterplan have the potential to activate the public realm in the heart of the traditional city centre, redefining its character and stimulating economic activity. Promises of central government funding announced in 2023, across transport, industry, homes, and community enhancement, could potentially redefine accessibility, urban form, and quality of life for residents in these strategic areas within the city.

The legacy of the Commonwealth Games is still being realised with Birmingham capitalising on its success with the Games to secure other major sporting events. Opportunities provided by the new facilities and regeneration areas carved out to host the Games are still being realised. There may be an uptick in hotel developments, responding to the need to house visitors to events that Birmingham will host. Sport-led regeneration and the hosting of future sporting events will deliver economic benefits to the city.

The city is redefining itself as a pioneer in knowledge and innovation. State-of-the-art facilities promoting health research, science and technology are cropping up around the city, which could stimulate growth and attract international interest. With the development of the knowledge industry in Birmingham, student housing may continue to be delivered steadily. As a result, education facilities associated with universities could be upgraded as the student population grows.

In the wake of the COVID-19 pandemic, and in the current stagnant economic conditions, retail-led schemes are muted, perhaps reflecting new consumer habits. Retail floorspace may continue a downward trajectory, and in future feature as a component of mixed-use, residential-led schemes.

However, the pandemic has not deterred Birmingham’s workforce from returning to the office. Office floorspace delivery and pipeline were strong in 2023, and Birmingham is demonstrating its national leadership in attracting key corporations and talent. The city’s offices are continuing to attract occupiers in the creative industries, clustered around the post-industrial hub of Digbeth.

There has been an increase in the number of office refurbishments, perhaps reflecting the post-pandemic office landscape, where employees have different expectations for the office environment. Office retrofits and new builds are demonstrating more ambitious sustainability credentials, reflecting the central government target of achieving net zero by 2050. It is likely that response to climate change, improved sustainability credentials and smart technologies will become desirable features in office developments in the coming years, and a feature expected by prospective occupiers and their employees.

In summary, Birmingham continues to chart an impressive path in the face of challenging economic conditions. Our Crane Survey 2024 data suggests that a bright future lies ahead for the city in 2024.

Data in Detail

A summary of all data across all development sectors can be accessed using the interactive Development map, Development activity and New start charts below, allowing you to explore all development projects, their location and what this means in terms of overall development activity.

The Report

Why?

A report that measures the amount of development taking place across Birmingham City Centre and its impact. Property types include residential, office, hotel, retail and leisure, student accommodation, education and research facilities.

Where?

Birmingham City Centre encompassing those areas within the outer ring road, including: City Core, Eastside, Westside, Southside, Digbeth, Jewellery Quarter and Gun Quarter.

What?

Developers building new schemes or undertaking significant refurbishments exceeding the following sizes: office – 10,000 sq ft; retail and leisure 10,000 sq ft; residential property – 25 units; education and research – 10,000 sq ft; hotel – 35 rooms. Mixed-use schemes with an equal split of uses will be counted against each sector within which the uses fall.

When?

Data for the Crane Survey recorded development activity between 3 January 2023 and 3 January 2024.

How?

Research for this report was undertaken by the regional Deloitte Real Assets team based in Birmingham which has monitored construction activity and planning permissions granted over a number of years, supplemented by rigorous field research. This research has been verified by industry contacts and an additional in-house research team.

Contacts

Zoe Davidson

Partner, Real Assets Advisory – Development

Eleanor Bird

Assistant Director, Real Assets Advisory - Planning

Jane Kistler

Associate, Real Assets Advisory - Planning