From monopoly to competition has been saved

From monopoly to competition How the three rules shaped the telecommunications industry

07 November 2014

A historical view of the telecommunications industry suggests that companies that persisted with an approach consistent with the three rules were the ones that turned in exceptional performance.

A historical perspective

The telecommunications industry has undergone dramatic shifts in its evolution. Since the end of the long-distance monopolies in the early 1980s and local monopolies in 1996, the industry has seen deregulation, technological innovation, and new market entrants. With each change in industry structure and technology, telecom companies have had opportunities for differentiation—opportunities exceptional performers took advantage of by creating and capturing value.

Telecom companies today continue to face challenges, including significant intermodal competition (cable, wireline, cellular) and competition from adjacent businesses, for example, from over-the-top (OTT)-based service providers such as Google and Apple. They are once again confronted with shifting business models and face several strategic choices:

- How can top telecom companies manage intermodal competition between cellular, traditional landline, and cable TV services?

- How should leading telecommunication companies move from a time division multiplexing (TDM)-based network to an Internet protocol (IP)-based one? This question is especially critical for wireless and traditional wireline players.

- How can incumbent telecommunications companies adapt their strategy to the new reality of competing in a global market with rapidly evolving competitors such as Google, Amazon, and Facebook?

- How can telecom companies best manage a complex and increasingly obsolete regulatory environment that was designed around the industry and technology of the past?

To understand these strategic choices, we must first look briefly at the industry’s development and how leading telecommunications companies met earlier challenges. Historian David Thelen said, “The challenge of history is to recover the past and introduce it to the present.” The history of the telecom industry and, in particular, two of its largest players tells the story of outcomes that resulted from strategic choices. This history is important because it created a set of deeply ingrained institutional beliefs and behaviors that were not appropriate in the context of new competitive realities. As a result, companies struggled, and some made poor decisions about how to approach new business realities.

Viewed from the perspective of the three rules described by Michael Raynor and Mumtaz Ahmed, these historical outcomes provide useful lessons for current industry participants. Companies that learned from these mistakes and persisted with an approach consistent with the three rules were the ones that turned in exceptional performance.

The Three Rules: How Exceptional Companies Think

Research conducted across industries, described in The Three Rules: How Exceptional Companies Think, shows that the most successful enterprises are those that continually search for and find ways to create new value—that is, value that is not price-driven—and in the process, pursue growth.1 Examining the study’s most consistently successful businesses, the researchers distilled three rules that drive long-term superior performance (see the sidebar “About The Three Rules”). The three rules are:

1) Better before cheaper: Don’t compete on price; compete on value.

2) Revenue before cost: Drive profitability with higher volume and price, not lower cost.

3) There are no other rules: Do whatever you have to in order to remain aligned with the first two rules.

About The Three Rules

More than five years ago, Deloitte launched the Exceptional Company research project to determine what enabled companies to deliver exceptional performance over the long term. Adopting a uniquely rigorous combination of statistical and case-based research, this project has led to over a dozen publications in academic and management journals, including the Strategic Management Journal, Harvard Business Review, and Deloitte Review.2 The fullest expression of this work to date is in The Three Rules: How Exceptional Companies Think (www.thethreerules.com).3

The project studied the full population of all publicly traded companies based in the United States at any time between 1966 and 2010, encompassing more than 25,000 individual companies and more than 300,000 company-years of data. Performance was measured using return on assets (ROA) in order to isolate the impact of managerial choices: Measures such as shareholder returns often confound company-level behaviors with changes in investor expectations.

Using a simulation model, the researchers estimated how well each company “should” have done given its industry, size, life span, and a variety of other characteristics. They then compared this theoretical performance with how well each company actually did. A company qualified as “exceptional” if it surpassed its expected performance by more than population-level variability would predict.

Not all exceptional companies are equally exceptional, however. The researchers identified “Miracle Workers,” or the best of the best, and “Long Runners,” companies that did slightly less well but still better than anyone had a right to expect. In the entire database, there were 174 Miracle Workers and 170 Long Runners.

To uncover what enabled these companies to turn in this standout performance over their lifetimes, the researchers compared the behaviors of Miracle Workers and Long Runners with each other and with “Average Joes,” companies with average lifespan, performance level, and performance volatility.

First, to understand the financial structure of exceptional companies’ performance advantages, the researchers pulled apart their income statements and balance sheets. This provided invaluable clues: Miracle Workers systematically rely on gross margin advantages, and very often tolerate cost and asset turnover disadvantages. In contrast, Long Runners tended to rely on cost advantages and lean on gross margin to a far lesser extent.

Then, detailed case study comparisons of trios—a Miracle Worker, Long Runner, and Average Joe—in nine different sectors revealed the causal mechanisms behind these financial results. Specifically, exceptional performance hinged on superior non-price differentiation and higher revenue, typically driven by higher prices. Nothing else seemed to systematically matter; in fact, exceptional companies seemed willing to change anything, and sometimes just about everything, about their businesses in order to sustain their differentiation and revenue leads.

Hence, the three rules:

- Better before cheaper: Don’t compete on price, compete on value.

- Revenue before cost: Drive profitability with higher volume and price, not lower cost.

- There are no other rules: Do whatever you have to in order to remain aligned with the first two rules.

Telecom Miracle Workers and Long Runners

It is well established that industry effects have a material impact on corporate-level performance. Any attempt to compare the performance of companies, and understand the impact of behavior on performance, must therefore control for these effects. In large-scale research, industry categorization schemes such as the Standard Industrial Classification (SIC) or the Global Industry Classification Standards (GICS) are often used. The findings reported in The Three Rules relies on the SIC system.

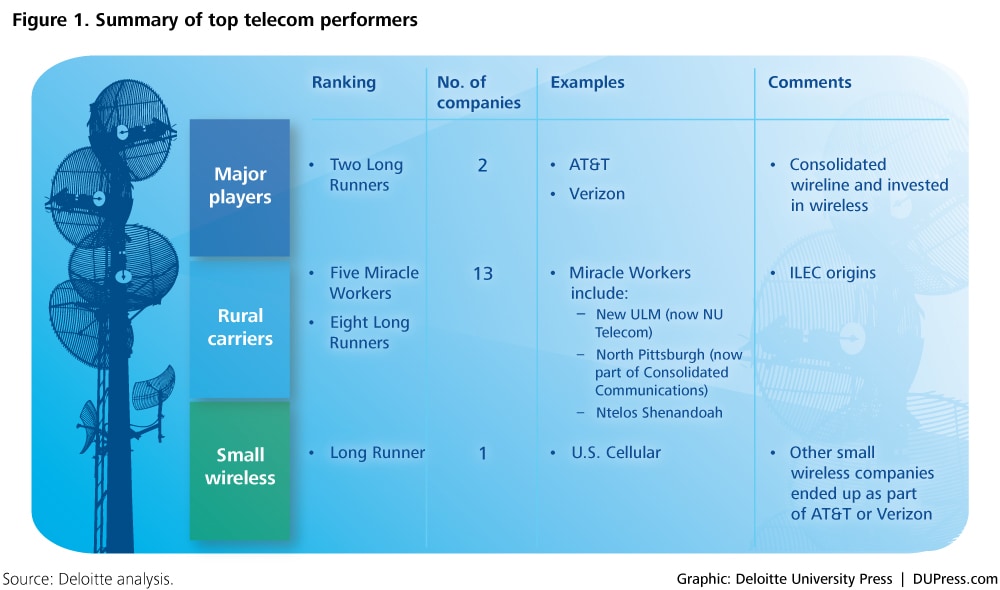

Finer-grained case study analysis of specific industries can sometimes require a qualitative analysis in order to capture material differences within these code-based industry categorizations. Such is the case for telecommunications. Based on what we believe to be the most relevant analysis of the industry’s major players, AT&T and Verizon appear to meet our criteria for Long Runners, while a number of smaller companies qualify as Miracle Workers and Long Runners—rural incumbent local exchange carriers (ILECs), smaller wireless companies, and niche players (see figure 1). This is probably because most superior performers have so far focused on only one of the rules—revenue before cost—paying limited attention until the last 10–15 years to establishing non-price differentiation (better before cheaper).

For the Three Rules analysis, companies are classified based on their time-varying four-digit SIC. A Miracle Worker is a company that has had enough 9th-decile ROA performances over its lifetime such that it would be statistically unlikely that the company would be able to achieve its performance profile through luck alone. A Long Runner is a company that has had enough 6th- to 8th-decile ROA performances over its lifetime such that it would be statistically unlikely that the company would be able to achieve its performance profile through luck alone. For example, a company with eight years of data would require eight 9th-decile performances to be considered a Miracle Worker, and a company with 42 years of data would require 17 9th-decile performances to be considered a Miracle Worker at a Miracle Worker probability threshold of 99.8 percent.

Other industries have seen many Miracle Workers derive their sustaining advantage from a significant difference in return on sales (ROS), but to date there has been relatively modest ROS spread in the telecom industry. This is changing, especially in the wireless business, where AT&T and Verizon, the two largest US carriers, clearly lead. Today, they are growing revenues, differentiating their products, investing heavily, and focusing on better before cheaper.4

Consistent with this research, we find that the dramatic shifts in the telecommunications firmament created opportunities for growth that only a few firms have been able to execute on over the long term. The history of the industry shows us that those that survived—and thrived—followed the three rules as they navigated two major transitions:

- The advent of competition

- The entry of cable and satellite plus the shifts from voice to data and wired to wireless

The advent of competition

For most of the first 100 years of their history, wireline and long-distance telecom companies could not apply the three rules. The highly regulated nature of the industry meant that, during this period, investors were guaranteed a return, the customer was guaranteed affordable service, and the telecom employee was provided with fairly secure employment. The process involved the industry submitting capital plans for services or service extension to the regulatory bodies, with the regulator generally choosing the lowest investment option and then setting the appropriate phone prices to deliver the regulated return. Thus, investment decisions and pricing were not under the control of the telecommunications provider.

Two major events changed this: the 1984 breakup of AT&T Corp. and the passage of the 1996 Telecommunications Act. The 1984 breakup of AT&T Corp. opened up competition in the long-distance (IXC) market. By the early 1980s, AT&T Corp. had grown into a vertically integrated telecom company providing local ILEC and long-distance wireline services. The company faced a US government antitrust suit, the resolution of which required the separation of the Bell System IXC from its Bell operating companies (BOCs).5 The breakup of AT&T formalized competition in the interstate and interexchange services. In its aftermath, IXCs moved from operating in a complex and heavily regulated environment to market-based competition and pricing, albeit with extensive rules. Three primary IXC players emerged: AT&T, MCI, and Sprint.

Even after the breakup of AT&T, the ILEC market remained monopoly-based, composed of two larger independents (GTE and Sprint/United Telecom); small, typically rural companies; and the seven former AT&T BOCs (the “Baby Bells”: Ameritech, Bell Atlantic, Pacific Telesis, Bell South, NYNEX, SBC, and US West). The 1996 Telecommunications Act allowed ILECs to enter the long-distance IXC market and compete with each other in exchange for removing their local monopolies.6

In just over a decade, companies in both the ILEC and IXC markets moved from operating in a complex and heavily regulated environment to market-based competition and pricing, though with extensive oversight.7 After a lengthy period of stable returns, these companies had to learn how to find and retain customers in a series of price-cutting battles that eroded margins. For most, the early days of deregulation were the antithesis of better before cheaper and revenue before cost. The move by ILECs into the IXC market based on low prices with a limited set of services can be described as cheaper before better. Customers benefited from the price-cutting, but as figure 1 shows, wireline industry revenues and profits collapsed. However, as we will discuss, two "Baby Bells", Bell Atlantic and SBC made sequential acquisitions—a revenue before cost strategy that positioned them for success in the coming wave of voice, data, and wireless innovations.8

New technologies: Cable, satellite, data, and wireless

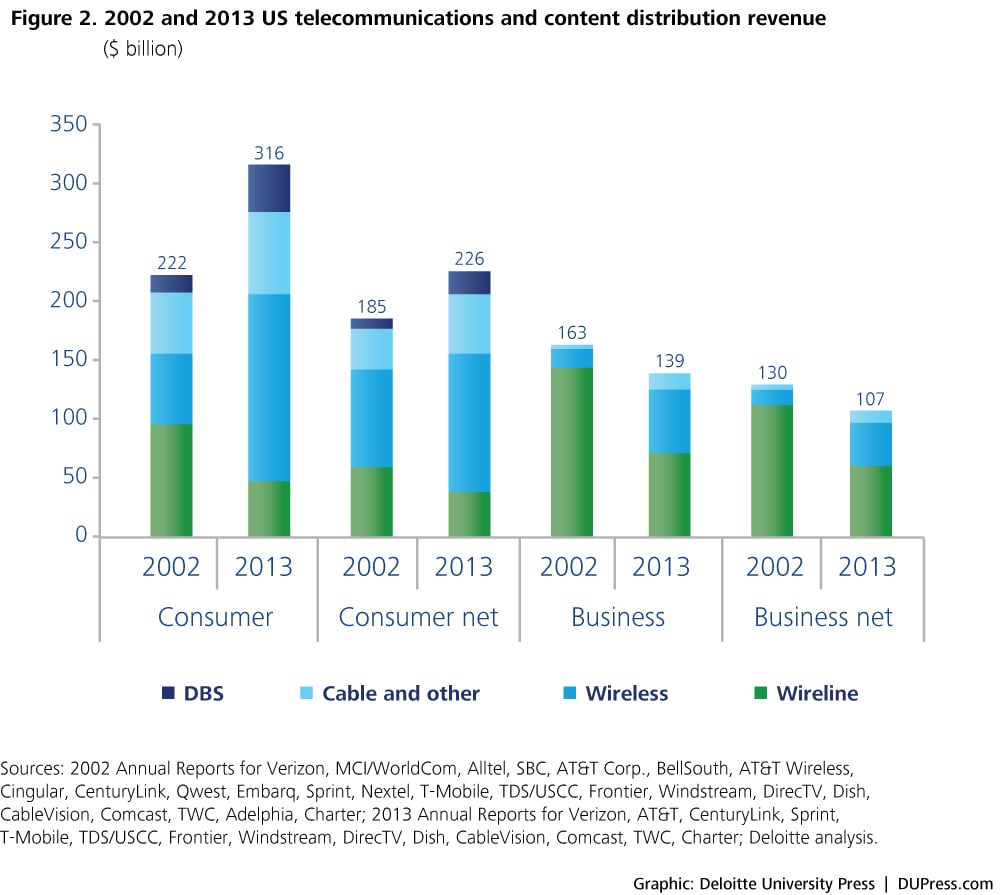

During the 11-year period between 2002 and 2013, the industry experienced a dramatic shift in technology from voice-oriented wired TDM (time-division multiplexing) services delivered over copper circuits to data-driven IP-based services delivered over wireless and fiber-rich networks.9 These new technologies captured ever-larger telecom revenue share. In 2002, the US telecommunications industry’s gross revenues were $385 billion (including cable and satellite TV), and its net revenues (after interconnection costs, program content, and handset subsidies) were $315 billion (see figure 2).

By 2013, wireline gross and net revenue both had fallen by more than 50 percent compared to 2002, declines that were more than offset by gains from wireless, cable, and DBS. It was during this period of growth that AT&T and Verizon began to pursue better before cheaper and revenue before cost strategies, particularly in the wireless segment and in TV distribution with new products such as Uverse (AT&T) and FiOS (Verizon). While these investments required both carriers to make extensive reinvestments in the network and products, the market results have been positive and their investments in fiber will have value for a long time.10 However, in the rest of the wireline consumer segment and the business market, the two companies have followed a more price-focused approach with limited new areas in the portfolio.

The rise of AT&T and Verizon

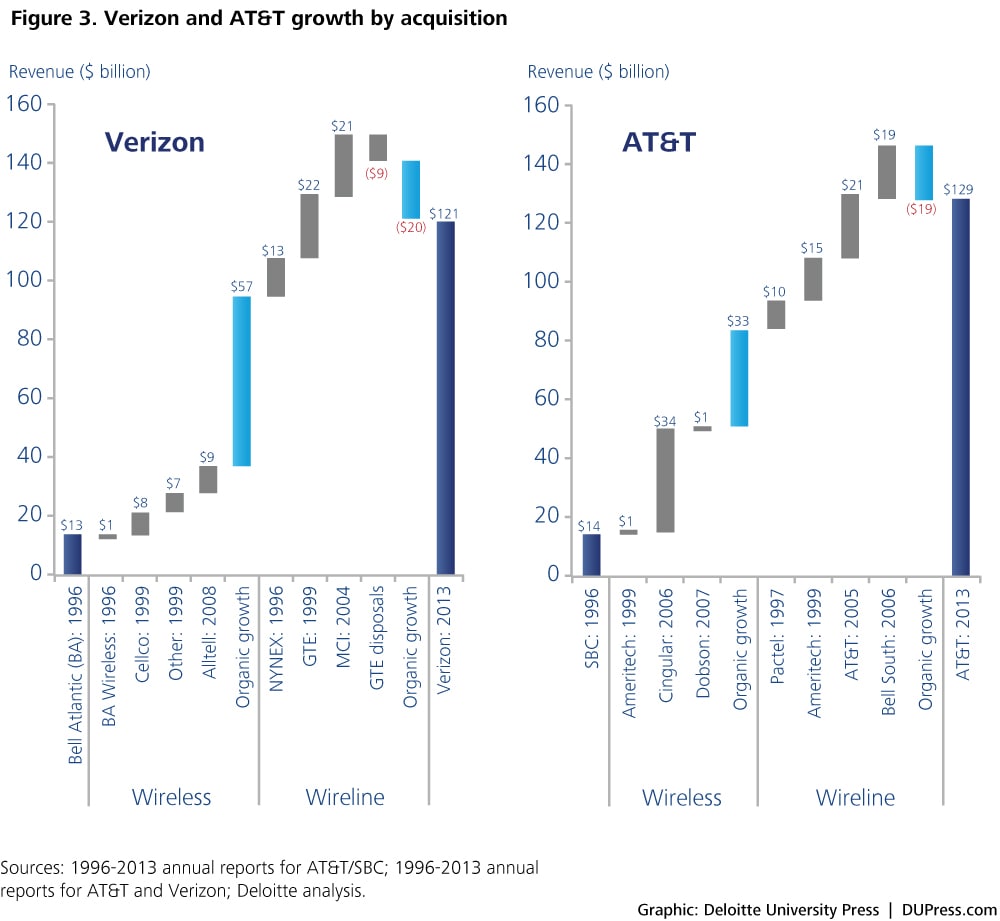

AT&T and Verizon made investments in wireless and new fiber networks, and moved from the voice-centric to the data-centric world. The progression of these two companies from medium-sized regional providers with a narrow product set to major industry players with a full range of telecom services was largely achieved by following the three rules. As the industry became competitive, the precursors of both companies (SBC and Bell Atlantic) initially used low prices to attract customers of the IXCs. But by the late 1990s, both companies adopted the revenue before cost strategy of expanding into new geographies. They also sought new technologies that helped create differentiated, value-based products—for example, in data and wireless. Using a revenue before cost acquisition strategy and organic growth, SBC (the predecessor of AT&T, Inc.) grew its revenue from $13 billion to $129 billion, and its enterprise value from $30 billion to $250–260 billion between 1993 and 2013.11 Between 1996 and 2003, SBC delivered top two-decile ROA performances.12 SBC was also in the top four deciles almost every year between 1985 and 2003. Even in more recent times, AT&T has delivered a much higher ROS than most of its peers (including Verizon), largely due to its wireline performance and business mix.13

About deciles

Decile values range from 0 to 9. A company’s decile rank is its relative performance in that year. A company with a rank of 0 is in the bottom 10 percent of all publicly traded companies, and one with a rank of 9 is in the top 10 percent. To calculate these ranks, we used a statistical technique called quantile regression and included controls for market share, size, industry, year, leverage, number of observations, and level of competition.

Both companies’ wireless businesses are examples of better before cheaper—providing an increasing array of services and geographic coverage. AT&T and Verizon have also followed a revenue before cost approach, moving into new markets such as wireless, broadband data, and video distribution and therefore carving out leading market positions. Both companies have shifted to a better before cheaper approach with their wireless businesses and new consumer broadband investments (FiOS and Uverse) built around fiber-rich IP networks; these incorporate advanced IPTV capabilities that meet consumer demand for a feature-rich, multimedia TV, telephone, and Internet experience. Interestingly, in this case the two companies have taken similar approaches, focusing on the US market and investing heavily in new assets.

The first step: Revenue before cost

Expanding geographic footprint by acquiring competitors

Both AT&T and Verizon embraced a revenue before cost strategy early, expanding their footprints by acquiring other Baby Bells that were struggling due to wireless substitution, cable competition, and resale-based competition that squeezed margins. The companies started as local exchange carriers—SBC and Bell Atlantic (two of the seven Baby Bells)—after the 1984 breakup of the AT&T system. SBC acquired Pacific Telesis, Ameritech, SNET, Bell South, and the post-divestiture AT&T long-distance business. Bell Atlantic acquired NYNEX, then merged with GTE to form Verizon, then subsequently acquired MCI (see figure 3).14

All seven Baby Bells started at about the same size, but a combination of stronger market growth and a more generous regulatory environment in the south and southeast propelled SBC, Bell Atlantic, and Bell South to outperform the others; by the late 1990s, they were the strongest of the Baby Bells. Conversely, NYNEX (New York and New England) and Pacific Telesis (Nevada and California) were faring poorly in terms of financial performance, although this did not deter Bell Atlantic and SBC from acquiring them.

Both Bell Atlantic and SBC followed up with more expensive acquisitions of other ILECs. SBC bought Connecticut ILEC SNET15in 1998 and Ameritech (Midwest) in 1999.16 Bell Atlantic bought GTE the same year and re-named itself Verizon after the deal closed.17

Thus, in the early 2000s, two major telecom companies had emerged with significant footprints in regional wireline and wireless communications:

- Verizon: Verizon was the amalgamation of the two northeast Baby Bells with the largest independent (GTE), which also had a controlling interest in Verizon Wireless—a major cellular player with a strong base in the US northeast and west. In the wireless space, Bell Atlantic Mobile merged with Vodafone Airtouch (the wireless assets of Pacific Telesis and US West) and the wireless assets of GTE were added to create Verizon Wireless. Later, Alltel was acquired, and Verizon has recently bought out the Vodafone minority to take full ownership of the wireless company.18

- SBC: SBC was formed by the merger of three major Bell companies covering the central United States and the west coast. SBC also grew its wireless business by merging its own wireless assets (SBC and Ameritech) with those of Bell South to create Cingular.19

Acquiring new market segments and technologies

For both companies, the next step was to become national long-distance providers. Historically, the Bell companies had been shut out of much of the long-distance market—specifically, the interstate and inter-LATA (local access and transport area) business. Both SBC and Verizon developed a foothold in the consumer and small business long-distance markets, but were unable to grow organically in the enterprise market and in more complex services (for example, advanced voice and data). Ultimately, however, financial stress among the three main long-distance players—Sprint, MCI/WorldCom, and AT&T Corp.—provided acquisition opportunities. In January 2005, SBC acquired AT&T Corp. for $16 billion, and in October of the same year, the company changed its name to AT&T.20

After MCI emerged from bankruptcy protection, Verizon acquired it for $6.8 billion in February 2005.21 With these two large acquisitions, SBC and Verizon became major players in the enterprise communications business and gained a full range of advanced voice and data products.

The move into wireless

Today, the wireless industry is generally regarded as one of the telecom industry’s great successes over the last 25 years. That was not always the case, and even as late as 2000, many analysts thought that the wireless industry in the United States would not deliver any value, as investments were still larger than returns.

Sprint PCS: creating value with the first nationwide network

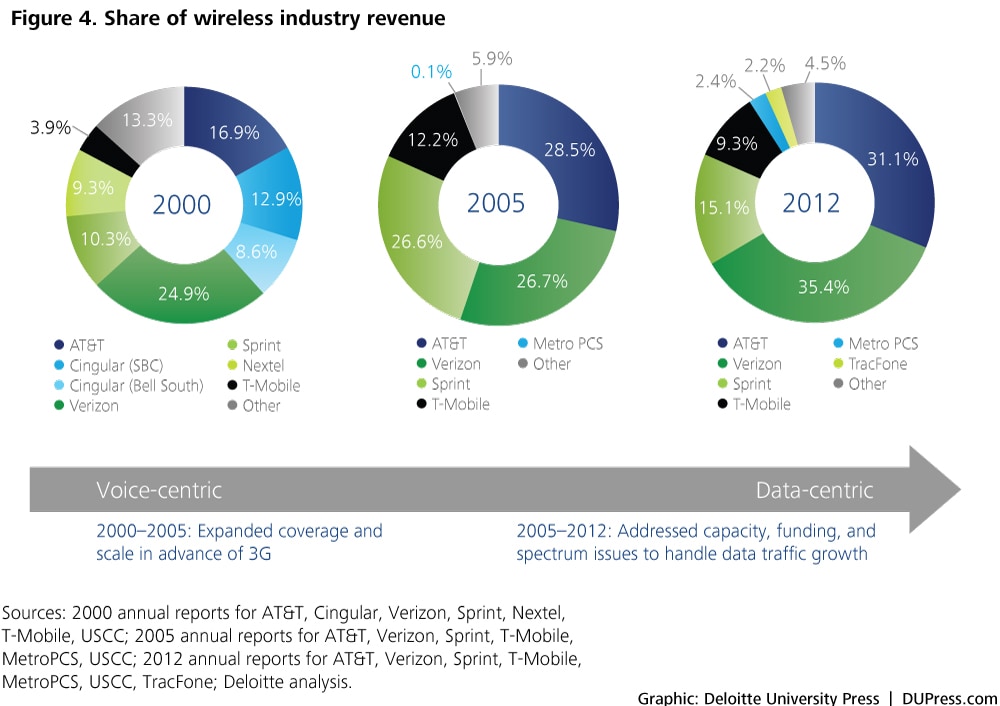

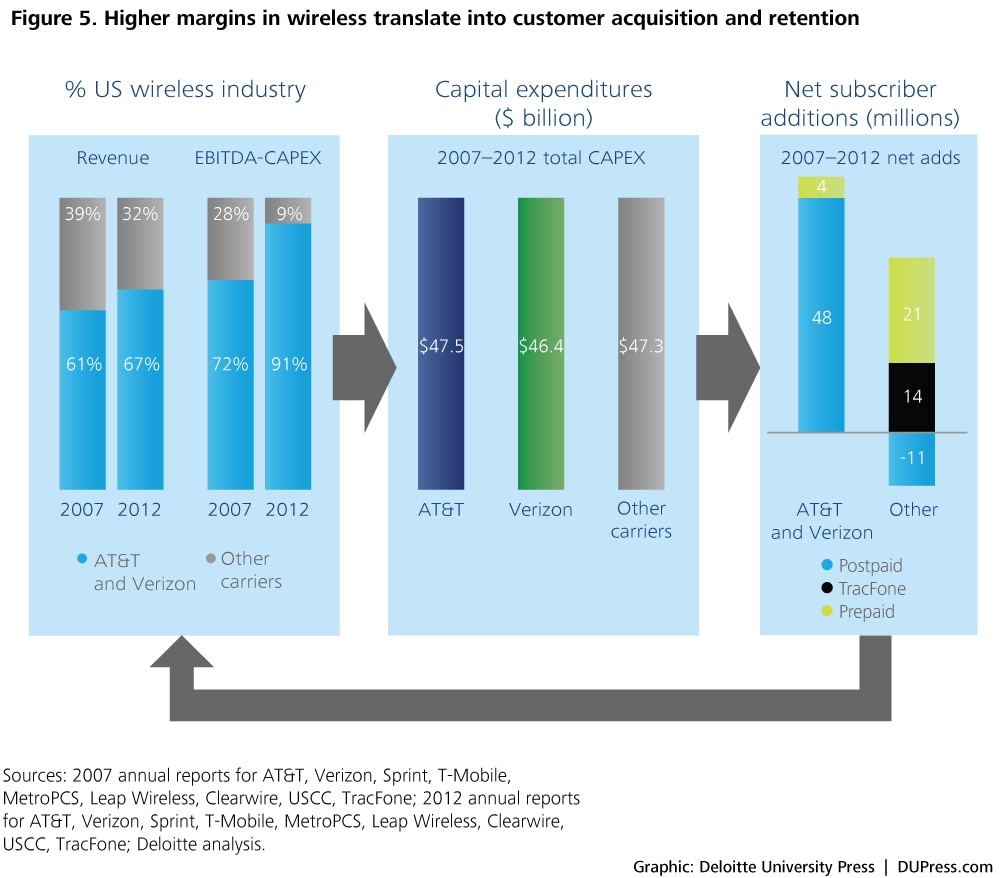

Even companies that did not reach the threshold of superior performance have delivered value by following the three rules. For example, in 1996, Sprint moved from being a regional cellular player to a national PCS operator. It acquired national PCS licenses in 1994 and 1995, and spun off its cellular business into 360° Communications in 1996. It created the first national network without roaming charges and seamless connection. This better before cheaper approach created significant shareholder value, with enterprise value rising from $18 billion in 1994 to around $100 billion in 1999–2000. At the same time, Sprint delivered industry-leading asset turnover but rather low ROS because it was investing heavily in growth. By 2005, other industry players had also evolved into national operations and were investing heavily in network performance. From the mid-2000s, AT&T and Verizon had gone national. They also pursued a better before cheaper approach, with Verizon building on network quality and AT&T on a superior device (the iPhone®).22Figure 4 shows the changing market share in the wireless industry between 2000 and 2012.

AT&T and Verizon continue to follow Sprint’s lead by investing in their networks to such an extent that they have attracted and retained the majority of postpaid customers, as shown in figure 5.

The wisdom of revenue before cost can be seen by contrasting the history of AT&T Corp. with that of Verizon near the turn of the 21st century. At the end of 1999, AT&T Corp.—before its acquisition by SBC—was much larger than Verizon (then Bell Atlantic), with revenues of $62.4 billion versus Verizon’s $33.2 billion. But AT&T Corp. pursued a cost-reduction strategy and broke the company into a number of business units in pursuit of efficiency. Its 1999 annual report states: “In order to become truly competitive, we must become the low-cost provider in the industry, and therefore, we are continuing our efforts to reduce our cost structure.”23

In 1999, AT&T Wireless earned $7.6 billion in revenue from 12 million subscribers, compared to Verizon’s $4.6 billion from 12 million wireless subscribers. However, in contrast to AT&T, Verizon pursued a revenue before cost strategy and merged with GTE and Airtouch, while AT&T Corp. separated itself into divisions that were publicly traded or had tracking stocks. By 2000, Verizon’s revenue of $65 billion almost matched AT&T’s $66 billion, and Verizon had created a much bigger wireless business with 27.5 million subscribers and $14.2 billion in revenue versus AT&T Corp.’s 15.2 million subscribers and $10.5 billion in revenue.24

Faced with a number of challenges, including ILEC entry and massive price reductions in the long-distance business, technology migration challenges in the wireless business (from TDMA to GSM), international challenges such as the losses in AT&T Canada, and limited ability to invest in 2004, AT&T Wireless put itself up for sale and was acquired by Cingular in October 2004.25 Meanwhile, AT&T Corp. itself—the long-distance and business services parent company—was sold to SBC in 2005, with SBC subsequently adopting the AT&T name.

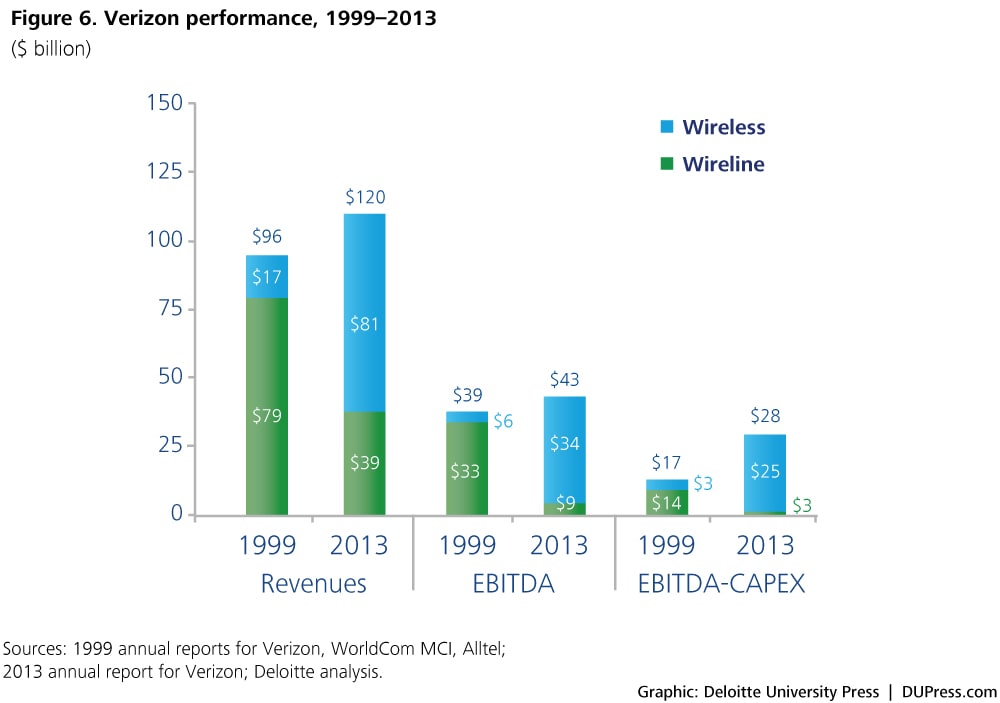

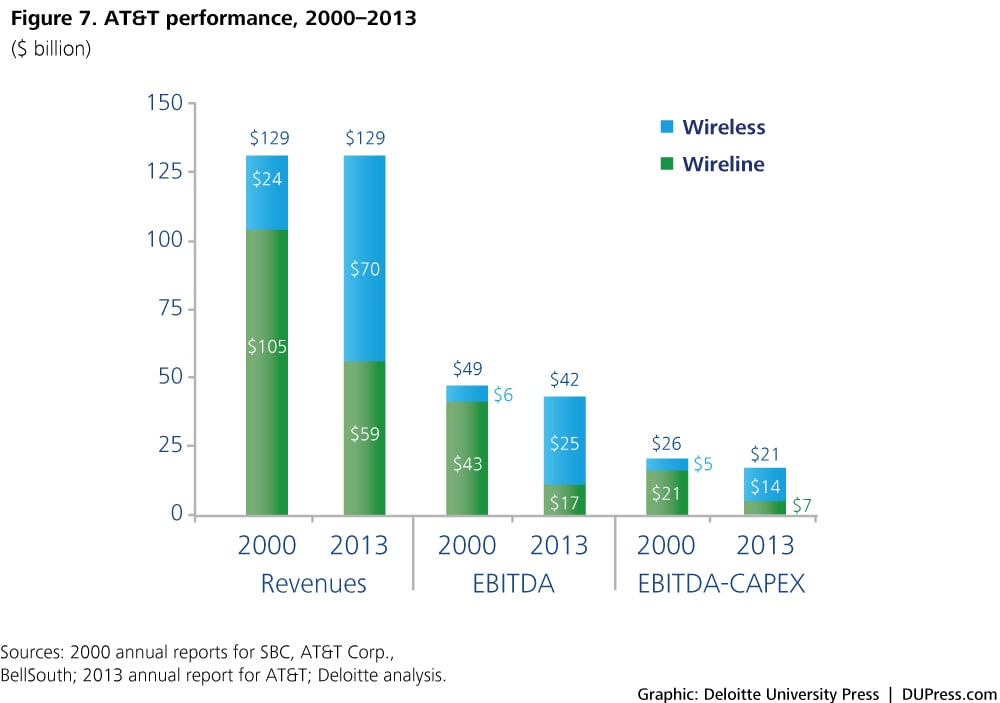

AT&T and Verizon were now in similar positions. They both owned significant local exchange assets, a major IXC/enterprise business, and a majority stake in one of the two largest wireless carriers. These changes coincided with the broader shift in the industry from wireline to wireless, evidence of which can be seen in the AT&T and Verizon results shown in figures 6 and 7, which recreate each company on a like basis (for example, data for 2000 covers the same set of businesses that each company had in 2013.)

The second step: Better before cheaper

Having followed Sprint in creating national wireless operations—with the benefits of a standard, seamless network with no roaming charges—AT&T and Verizon applied better before cheaper slightly differently. Verizon has focused on network quality—voice, text messaging, and data usage—and has received industry recognition for its efforts. In the J. D. Power 2013 US Wireless Network Quality Performance StudySM, Verizon Wireless was the first wireless provider since 2004 to rank highest across all six regions of the United States.26

AT&T chose to differentiate itself based on a combination of its data network and a new device—the iPhone, a product that clearly attempted to position itself as better before cheaper. When the iPhone was launched on June 29, 2007, it cost $499 or $599 depending on the model, compared with the $199 Blackberry Pearl (at that time one of the most expensive smartphones), but it added a whole new capability—the Internet experience on a mobile device.27 The iPhone’s availability created an environment where customers were willing to spend much more on wireless services to have access to mobile Internet. This additional spending allowed AT&T to invest heavily in network performance.28

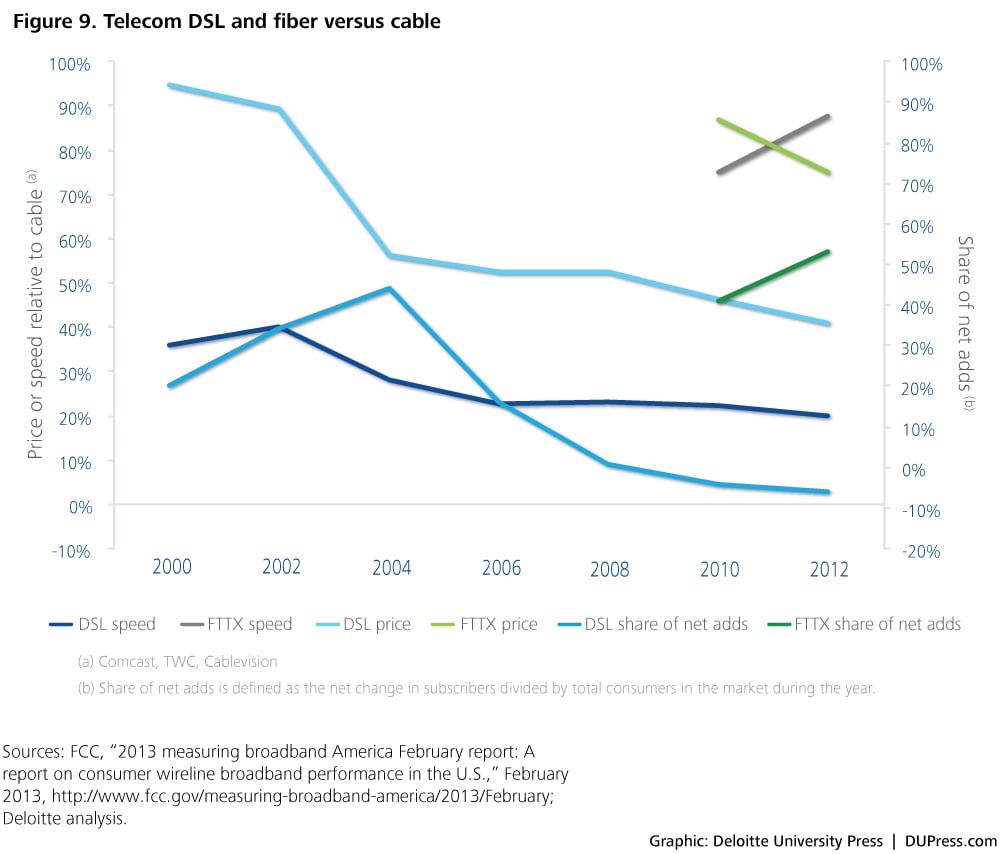

Lessons learned: Cheaper DSL

While AT&T and Verizon were successful in expanding their footprint and service mix, neither company followed the better before cheaper mantra in their attempts to offer cheaper inferior broadband with DSL. In 2000–2001, DSL was a competitive product with cable modems, but it was unable to keep up with the speed gains that cable could offer. Left with an inferior product, AT&T and Verizon responded by pricing it significantly below cable, a strategy that both companies eventually abandoned—underscoring the cost of deviating from the three rules.29

The third step: There are no other rules

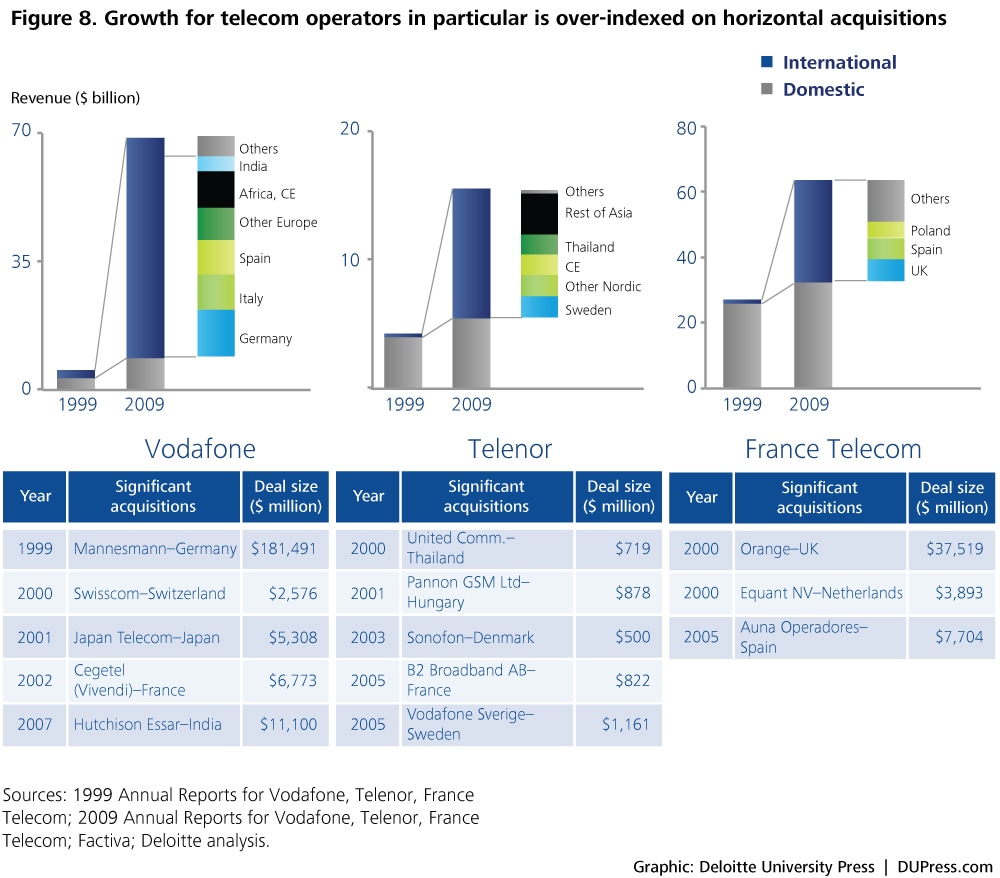

The wide range of approaches explored by telecom companies—and the decidedly mixed results—highlights both the promise and limitation of the third rule: There are no other rules. Telecom companies have been willing to explore many new avenues, but unless their actions are in the service of the first two rules, they are more likely than not to result in inferior performance. The sector has seen forays into international expansion (Bell South and others) and diversification (the legacy AT&T long-distance company getting into cable TV, equipment manufacturing with Lucent and NCR, and other businesses), but these efforts have failed to yield statistically significant improvements. Thus, horizontal acquisitions have been the main focus of telecommunications players, as shown in figure 8.

But increasingly, companies in the industry appear to be applying the rules. AT&T and Verizon are investing in replacing their landline product sets with fiber-based IP products, substantially changing their positions in the consumer market. While these shifts face significant regulatory hurdles, both companies appear committed to this approach. Their consumer products have evolved from the cheaper before better approach of offering consumer broadband through DSL to the better before cheaper offerings of IP-based FiOS and Uverse. FiOS (Verizon) and Uverse (AT&T) seek to provide the next generation of television, telecommunications, and high-speed Internet. Their aim is to win customers from cable and satellite providers by providing a multimedia TV, telephone, and Internet experience. The key product is high-speed Internet access, although the nature of household purchasing means that a bundle of three services (voice, data, and video) needs to be provided. Conversely, their investments in better before cheaper, such as IPTV, have stemmed revenue decline in their consumer businesses, even though deployment is limited.30AT&T is in the process of acquiring DirecTV, which will allow the company to add national video services to its national wireless services and gives it a stronger line-up of unique video content.31

The difference in results between AT&T and Verizon’s copper-based DSL services and their fiber-based Uverse and FiOS services can be seen in figure 9.

Applying the three rules today

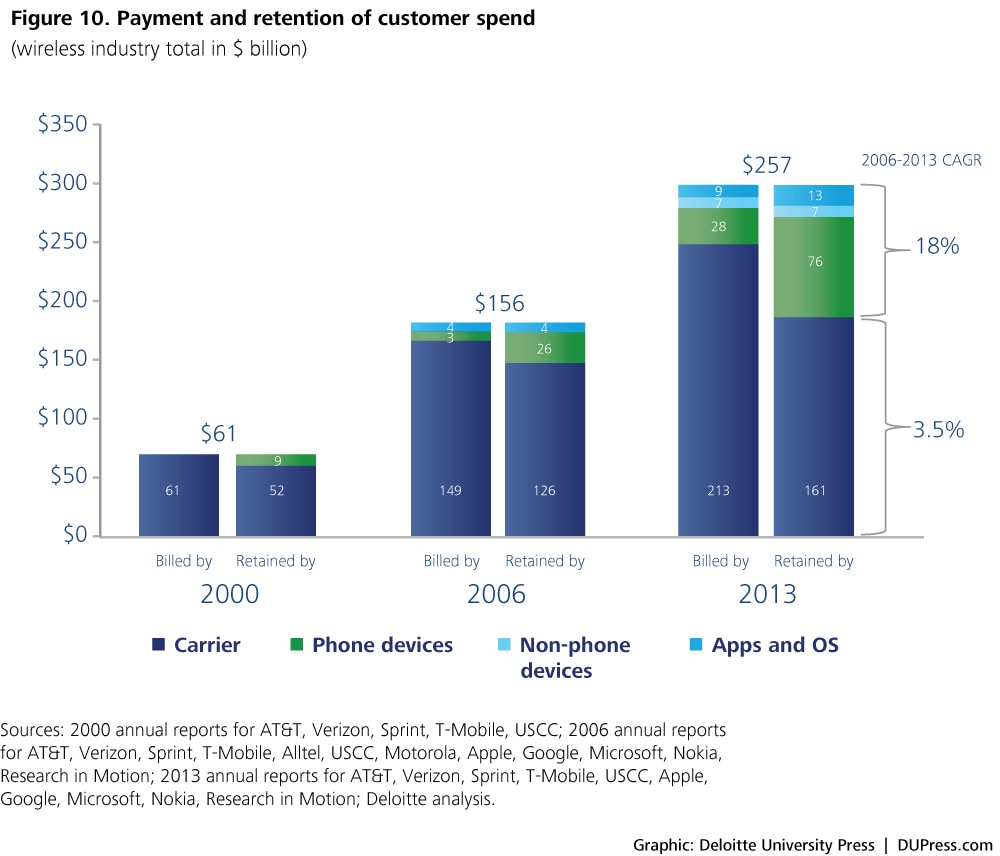

Going forward, a new form of competition is emerging, with adjacent players vying for carriers’ revenues. This is evident in the wireless industry, where handset and other ecosystem players are capturing an increasing share of revenue (figure 10). Companies such as Amazon and Google have invested heavily in infrastructure; Amazon Web Services is a clear competitor for many telecom offerings, and Google is even building fiber to the home (in Austin and Kansas) using newer and faster architectures.32

Google and Amazon are using new technologies and approaches to enter the market. Amazon is working in the adjacent cloud infrastructure space, while Google is building cloud capabilities and new applications that are network-agnostic. Telecommunications carriers are fighting back with a three-pronged strategy:

- Building superior network capabilities

- Investing in select end-user areas (such as telematics and video)

- Enabling companies in adjacent spaces to gain

The competitive environment in the landline segment is similar, with systems integrators and cloud service players competing for business using a better before cheaper strategy. These over-the-top types of services are using new IP data access services to create new service sets and value-added solutions (for example, corporate 1-800 solutions) that were traditionally the preserve of telecommunications carriers and built into the fabric of the network. Traditional telecom companies are responding by making investments in new areas. Verizon, AT&T, and others are creating a series of network APIs (application program interfaces) and investing in cloud services, system integration, outsourcing, and content distribution.33 At first glance, this looks like a pure revenue before cost approach because they are investing in new areas with emerging business models. However, these companies are also evolving their wireless networks from a best-efforts approach (where the subscriber received whatever performance the network had available) to a managed radio interface (where subscribers can pay for minimum performance levels), a clear better before cheaper approach.

In response to competition from traditional landline services, cable TV and wireless telecom companies are upgrading their wireline networks to an all-IP capability, replacing the older TDM technologies. Similarly, they are accelerating the pace of investment in wireless network technologies. Telecom companies are also shifting to software-defined networks that allow for flexibility, lower operating costs, and customer-specific configuration. Finally, they have shifted from focusing on a single technology (for example, wireless or copper) to an approach that is based on multiple technologies.

In moving from TDM to IP, telecom companies should also follow a “three rules” approach, switching to IP quickly and then rapidly removing TDM assets. This is a revenue before cost strategy and should be achieved by reengineering the business around IP capabilities rather than adding them to the existing TDM processes and systems. If the IP business is designed around a new operating model, the switch to IP can also constitute a better before cheaper approach that can differentiate these providers. This approach will require substantial investment, but if implemented correctly, changing the operating model for sales, provisioning, and customer care could enable much lower operating costs, as many tasks currently performed by company staff can be done online by customers. Doing this, however, will require a completely different approach; standardization will be important, and high predictability, low variance, and low error rates will need to be the norm.

Finally, telecom companies need to manage the current complex—and increasingly obsolete—regulatory environment to facilitate the change to a multi-technology approach and a new IP-based business model. While regulators see the need to move to the new networks, they have been slow to remove reporting requirements, regulations, and terms and conditions that are more appropriate for the old networks and processes. While telecom companies are working to educate regulators, this shift may be the most difficult one.

In summary, two major players have emerged in the US telecommunications industry: AT&T and Verizon, which together represent around 75 percent of the total industry’s enterprise value ($485 billion of $660 billion).34 They have shifted from being regulated, single-technology, regional- and local-access providers to national, multi-technology telecommunications service providers. They have done so by pursuing growth in new technology areas (mainly wireless and fiber-rich broadband networks), and they have tried to take a better before cheaper approach in the delivery of these services. This has not been without pain, but since the late 1990s, these companies have transformed dramatically. In the future, they will need to continue tackling competition from other cable, wireless, and wireline providers as well as carve out new positions against adjacent (OTT-based) competitors, even as they transform their networks again from TDM to IP and move the regulatory framework.

In the next few years, we expect to see telecom companies win through a mixture of better before cheaper and revenue before cost approaches. Better before cheaper approaches are likely to center around superior bandwidth, latency, and throughput on broadband products, as well as the delivery of unique customer experiences through the aggregation of a company’s own capabilities and the integration/aggregation of capabilities of other firms. Revenue before cost approaches, on the other hand, will probably center on offering a broader scope of services in an integrated fashion and creating and selling new solutions to existing customers.

In the future, we expect to see companies win through a mixture of better before cheaper and revenue before cost approaches:

- Better before cheaper probably centering around:

- Superior bandwidth, latency, and throughput on broadband products

- Unique customer experiences through the aggregation of a firm’s own capabilities and the integration/aggregation of the capabilities of other firms

- Revenue before cost approach probably centering around:

- Offering a broader scope of services in an integrated fashion

- Creating and selling new solutions to existing customers

Deloitte’s telecommunications group is part of the Deloitte US organization’s Technology, Media, and Telecommunications practice. This practice includes more than 1,400 technology, media and entertainment, and telecommunications clients in the United States alone, including the vast majority of market category leaders across all sector segments, and serving companies across multiple sub-sectors including wireless, wireline, and equipment manufacturing. In the United States, we serve the top five wireline companies, the top five wireless companies, the top five equipment manufacturing companies, and four of the top five satellite companies.

© 2021. See Terms of Use for more information.