Overcoming the hurdles to integrating sustainability into business strategy

Transforming to meet the demands of decarbonization takes more than ESG metrics: It takes governance. And it takes guts.

Simon Cleveland

Kristen Sullivan

Veronica Poole

Yasmine Chahed

It’s clear from the latest climate science that the world is not doing enough, fast enough to decarbonize. Without immediate and profound changes to how society lives and does business, the world is likely heading for a future marked by widespread changes to the climate with devastating consequences for every region across the globe.1

The business community is alert to the crisis and has started to make progress in foundational ways: They are working to understand what regulators and standard setters expect, they are gathering data to help measure their impact in society, and they are responding to their stakeholders through dialogue and disclosure. Importantly, they are also embracing a broader concept of sustainability, which looks at how actions today can impact people, the planet and prosperity in the future, as a strategy for business resilience and long-term success.

Spending priorities seem to reflect this, too. According to a recent Deloitte survey of C-level executives about their sustainability priorities2, 75% of the executives surveyed said their organizations have increased their sustainability investments over the past year; nearly 20% of whom have increased investments significantly.3

Still, there continues to be a worrying gap between most corporate actions-to-date and the deeper changes required to achieve net-zero and the United Nations (UN) Sustainable Development Goals (SDGs).

While most corporate leaders say they have taken actions to use more sustainable materials (59%) and increase the efficiency of energy use (59%), Deloitte research also shows that organizations are slower to implement the “needle-moving” actions that embed sustainability into the core of their strategies, operations, and cultures. For example, only 33% of C-level executives indicate their organizations are tying senior leader compensation to environmental sustainability performance, and 32% incorporate climate considerations into lobbying/political donations.4

If the business community is aware that every moment counts, and companies are starting to align themselves to a more sustainable world, then why hasn’t more progress been made to help address climate change?

In a word, uncertainty.

To learn more about some of the key barriers preventing deeper sustainability integration, Deloitte Global interviewed 25 leaders from around the globe in the investment community, business world, academia, and non-profit sector. The interviews revealed that even seasoned leaders are having trouble keeping up with the changes to the operating landscape over the last few years. There are now economic, social, ethical, and regulatory reasons for companies to change, but they face integration challenges at all levels, complex stakeholder environments, and ambiguity over their role as corporate citizens.

Few business leaders have experienced this level of change before and it’s taking place at a time of tremendous disruption—the Russia-Ukraine war, the energy crisis, geopolitical tensions, rapidly changing technologies, supply shortages, and the lingering effects of the COVID-19 pandemic.

That’s why there are companies that are looking at the different types of actions that society expects of businesses and saying, “Well, if I don’t have to report it, then we really don’t want to spend any time on it.” However, there can be serious risks to approaching sustainability reporting with a compliance mindset because transparency is designed to reflect the risks and opportunities that could affect business performance going forward.

Viewing a business model through a sustainability lens can help leaders better understand how they create value, gain a clarity of purpose, discover insights that can frame business problems in new terms, and prepare them to respond. This report outlines the challenges companies are facing in integrating sustainability into business strategy and offers a set of approaches leaders can use to clear the hurdles along the way.

Leaders are facing integration challenges on all levels

Integrating sustainability into the fabric of an organization can require fundamental shifts in how leaders think and make decisions. While the early movers had the benefit of time to experiment with solutions and to align their governance to the requirements of building an agile organization, for those embarking on this journey now, these changes are taking place all at once. And as Deloitte’s interviews with leading sustainability experts reflected, sustainability integration is a process often fought with complex questions, unclear expectations, and business risks.

Perceived lack of clear direction

The recent release of the International Sustainability Standards Board (ISSB) standards now provides the framework for a global shift from voluntary to mandatory sustainability reporting, but until now, the absence of an overarching framework left leaders feeling like they didn’t have a sense of what “good” looks like, especially when the emerging expectations are not consistently supported by incentives and rewards from the financial system. Many companies remain concerned about how these overarching standards will be interpreted in local jurisdictions.

Reporting itself can introduce risks. Offering greater transparency can expose companies to legal and reputational consequences if they misstep, or if they promise change faster than they are able to deliver. There are also countervailing matters to consider, including: impact on customer relationships, access to credit, impact on stock price, and even impact on long-term solvency for companies whose current business models may be incompatible with a low-carbon economy.

“Change is difficult because you don’t know what will happen,” one interviewee explained. “If you start to report on something you didn’t report on before, that can be scary. Responses may be uncertain. It’s a step in the unknown and it may demonstrate a negative impact.”

Deloitte’s research suggests that some companies have held back on making investments because they were waiting to see where climate policies and regulation would ultimately land. In some jurisdictions, there has even been some entrenched skepticism that governments will follow through on climate action: Only 28% of the executive leaders surveyed by Deloitte said that governments around the world are “very serious” about it.5

Feeling stuck between conflicting expectations

Complex stakeholder environments can make it challenging to prioritizing sustainability investments. The intense external interest in a company’s environmental, social and governance performance often results in overlapping information requests, which compete for limited resources, and raise questions about how to prioritize efforts when the audience and benefits are not always clear. “Many companies want to be responsive to all requests and as a result publish a lot of information,” one interviewee said. “But is this investment resulting in better decision-making by anyone?”

Those who open themselves up to scrutiny can also face litigation and political backlash. In the United States, the rhetoric from conservative politicians, for example, has already had a chilling effect on how companies are communicating with investors on environmental sustainability, and diversity, equity, and inclusion programs.6 As one interviewee explained, “Politics is the main issue. It is not the difficulty of calculating and communicating the value of impact".

Just getting the data can be harder than it looks. From the outside looking in, it might seem like a straightforward expectation that a company would know how its products are made and where its materials come from, but as an industry leader from the interview panel explained: “They didn’t set up their operations to gather this information […] They didn’t start projects expecting this data need, they don’t have the track record, they don’t have the systems, they don’t yet know how they will do it.”

And when each product involves dozens of materials, sourced from different geographies, producers, and suppliers, measuring environmental impact can get complicated quickly. The data companies need, in other words, just might not be available—yet.

Overwhelm and decision fatigue

Understandably, leaders are feeling overwhelmed. “I don’t think there’s a silver bullet to this, it’s kind of hard to see what the theory of change is, because there are all of these blocking factors before you’re out of the gate,” one interviewee explained. “As a result, it is seen as a compliance issue and there is no motivation to explore the potential business opportunities of the transformation the different sectors are in.”

Even companies that are willing to embrace an element of risk and uncertainty may find that they encounter too many ‘chicken-and-egg situations’ to know where to even start.This came through in the conversations with sustainability specialists, one of whom described the wait-and-see approach in organizations as “a lot of finger-pointing and disparate activities resulting in confusion and lack of process and ownership.”

So, at a time when uncertainty looms, it might seem rational to prioritize short-term security over long-term investments, but in fact, further climate delay comes at a great cost.

The problems we face require business transformation

If the world does not curb greenhouse gas emissions, modeling by the Deloitte Economics Institute indicates that the global economy will lose US$178 trillion in net present value terms by 2070 due to the escalating costs of dealing with climate-related events.7

Under such a scenario, the toll on human health and well-being, biodiversity, and the world’s ecosystems would be immeasurable, as the Intergovernmental Panel on Climate Change’s (IPCC’s) latest summary report notes: “There is a rapidly closing window of opportunity to secure a livable and sustainable future for all.”8

Given these tangible changes to the operating environment, global capital markets and regulators are seeking enhanced disclosure to help evaluate how companies are responding to climate and sustainability matters. Those companies that may have not yet looked at the full range of material matters or still perceive environmental, social, and governance (ESG) reporting as a compliance activity may be putting business continuity and future performance at risk.

They are also likely overlooking the true role of transparency as a catalyst for internal business transformation. “We can get lost in forgetting what we are doing this for,” one interviewee said. “The end goal is for companies to do their part in acting in ethical, responsible, meaningful ways that creates a future that is positive for everyone.”

Indeed, responding to the climate crisis requires more than curbing greenhouse gas emissions alone: Businesses need to transform how they operate, in support of the system-level changes that can achieve carbon reduction at scale.9

Those who keep waiting until all the requirements are finalized are likely missing opportunities to build systems, gain capacity and counter the rising tide of climate litigation.10 And delaying these types of multidimensional changes is likely to make it more difficult and more costly to play catch up later, as the pandemic recently demonstrated: When digital transformation suddenly became an imperative, those companies who had already started the process clearly had a competitive advantage over those who had not.11

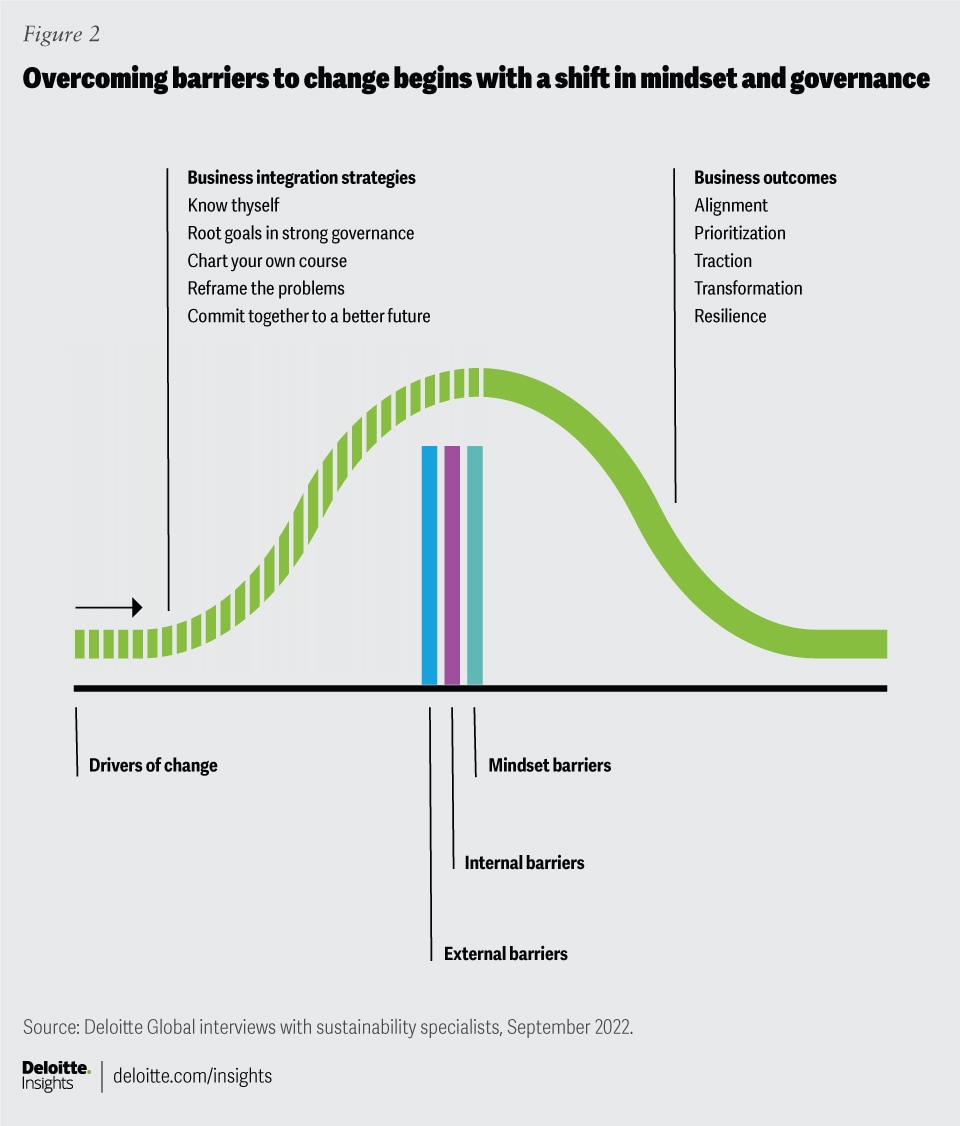

In the following sections, we outline a core set of approaches to help leaders gain clarity, align resources, prioritize goals and spending, and overcome the hurdles to progress on their sustainability transformation journey.

1. Know thy self

Invest in data quality and identify the material risks that align to purpose

Integrating sustainability into the core of the business begins with taking a 360-degree view of a company’s operational relationships with people and the planet. Done correctly, this process can often turn into a meaningful conversation about the overlooked risks, operational inefficiencies, and broader business realities that could affect business’ performance going forward.

For many companies, getting this level of insight may require deep investments. This may include introducing new data collection tools, improved data sharing with suppliers and customers, developing a data quality assurance process, and establishing internal governance for tracking the firm’s progress against stated goals and identified risks. Organizations that are doing this well build connectivity. They pull together strands of data from various systems and make it easily digestible for different audiences.

Having access to more data is not the same thing as having the right data, though. The key is to have data that reflects the sustainability risks and opportunities that are material to the business. Instead, the specialists Deloitte Global interviewed recommend that companies look closely at the resources and relationships that make them successful to identify the opportunities for making the value creation process more sustainable.

In turn, understanding the ESG matters that are relevant to the business can create a new rubric for evaluating and monitoring enterprise risks, prioritizing spending and making decisions that integrate sustainability aspects into the company’s DNA: “The definition of corporate success is changing, as is the role of business in society and corporate measurement systems (e.g., impact thinking, double materiality). To be successful in the new business reality, companies need to understand if they are leaders or laggards in their sector transition paths and how they manage trade-offs between financial and non-financial targets.”

Aligning the data collection efforts to the company’s key risk and opportunities is a good starting point: “There is a world in which companies could stick to 20 metrics that were deemed material for their sector,” one interviewee said. “This would serve as a reasonable proxy for performance along the most important and meaningful dimensions for sector peers.”

For those who are overwhelmed by the number of metrics, another interviewee recommended that companies leverage the emerging set of International Financial Reporting Standards (IFRS) Sustainability Disclosure Standards to focus on climate-related risks. “Starting with one reporting topic --climate --will ease the burden for companies, and allow them time to prepare themselves organizationally, establish systems and processes, determine the kind of data needed and how to gather it.”

2. Root goals in strong governance

Embedding sustainability into business operations requires accountability

Regardless of the industry or the sustainability matters a company faces, good governance should be an essential part of the internal business transformation. “If you don’t have governance, you can’t talk about having environmental or social disclosures,” one interviewee said. “To be transparent, you need governance. It’s the foundation and the base.”

To help elevate accountability for sustainability integration, some companies are assigning responsibility to the senior leaders of the organization, including: the board of directors, the chief financial officer, or a cross-functional sustainability steering committee, as one interviewee described: “This is a major challenge for boards,” one interviewee said. “The focus of the board has typically been company strategy, reporting, investor engagement. Now you’re folding in a new suite of information that will require a diverse set of skills not traditionally required.”

To help drive governance over sustainability data and accounting, some companies are assigning sustainability information disclosure to the chief financial officer. "The finance teams have the capabilities to put strong controls in place, build systems that capture data once and reuse it for multiple purpose,” one interviewee explained. “They are also the teams responsible for management reporting and the information systems that support internal strategy and business decision making. Thus, they are uniquely positioned to ensure that sustainability information is integrated into management and board decision making.”

Just as having the right tone at the top is an important part of changing organizational culture, so too is empowering employees to contribute to the effort by embedding the work into day-to-day responsibilities.

“Companies will soon begin setting up teams consisting of sustainability, strategy, investor relations, and finance. Leading companies have already integrated sustainability directly into standard operations and decision-making processes.”

3. Chart your own course

Organizations can find traction through authentic stakeholder dialogue about what the future holds and where a company is on the sustainability journey

Because each company has a unique business model, structure, and culture, no two sustainability transformations are alike. Even within the same organization, the integration process may require different strategies for different business units, depending on such factors as industry segment, workforce composition, geography, and management structure.

Factors that can influence sustainability integration

- Privately held versus publicly owned (The market it is listed on also matters.)

- Industry sector

- Business model

- Organizational design

- Internal culture

- The availability/lack of talent to support sustainability efforts

- Macro-economic factors, supply chain disruptions, etc.

- The pace of broader, nested system integrations

That’s why it’s important to be honest about where your business is on the transformation journey. “Quality of dialogue is critical here,” one interviewee said. “We are at a tipping point where investors, auditors, business, and others need to collaborate to find solutions and address challenges. It is okay to disagree, but we need to have dialogue.”

Directly engaging with stakeholders can be a chance to understand their needs and improve connections that can support the business transformation in important ways. Some companies formally incorporate stakeholder dialogue into the goal-setting process, while others find that these dialogues can open the aperture for bigger shifts in the business. In talking to stakeholders, they must identify the most significant voices, not simply the loudest, and take ownership of responding to what is most important.

Stakeholder mapping can also help companies target communications, based on the needs and uses of the various audiences. The interviewees recommended that companies take a “multidimensional” approach.

“I think companies need to think about ESG disclosure in the same way they think about communications strategy broadly – tailoring information to the needs of the user,” one interviewee said. “You don’t use the same communication vehicles that you use internally with your employees with your clients. You tailor information to people’s needs and companies need to view ESG information through that same lens.”

As companies learn more about their sustainability impacts, risks, and opportunities they might become fearful of backlash from making related disclosures. It is helpful to remember that most companies are still in the early phases of building their programs and stakeholders seem to understand that perfection should not be the enemy of moving towards good practice.

4. Reframe the problems

Managing uncertainty requires business leaders to get comfortable with making decisions without a perfect answer

While most corporate leaders have grown up in a business culture that expects answers to come from accurate and timely information, sustainability will likely require business leaders to make decisions when they simply might not have the information, when choices are ambiguous, and the business outcomes vague.

"The differences with financial reporting are not trivial,” one interviewee explained. “The fact that ESG reporting will be forward-looking is quite an important distinction. There is also the timeframe, [which] is significantly longer than for traditional financial reporting. The data challenge gets compounded, and further compounded if you want that data to be verifiable. You need data based on science-based metrics. You need data on Scope 3. Those challenges are there. You are more likely to get qualitative than quantitative information."

It may be uncomfortable for leaders to admit what they don’t know, but it’s more accurate to present information in terms of ranges, scenarios, and confidence intervals and with explanatory narrative if the pace or direction of change may shift over time. "The ones who know they don’t know are the smartest," one interviewee said.

When it comes to setting goals and reporting progress, leaders should be authentic. This may mean limiting the scope at the outset to focus efforts and build internal capabilities. “Figure out a couple of things [that] have impact and make progress on those,” one interviewee recommended. “This has been the most effective way to break through the noise and be a part of the conversation." Over time, "companies will mature in setting more practical goals, will become bolder in what they do and how they share it will stakeholders,” another interviewee observed.

Because sustainability programs require long-term thinking, leaders may also have to make the business case for spending on programs with much longer payback periods. Although fiduciary duties sometimes keep business leaders and investors focused on the short-term, it's important to begin socializing with stakeholders the idea of making legacy investments in long-term risk reduction, resiliency, and business continuity. “It will take time, effort, and investment for these systems to develop and mature and ensure reliable data. By allowing for a greater period of maturity, we will also likely see better alignment between financial and non-financial reporting and account for potential implications between the two,” one interviewee said.

On the positive side, sustainability investments can often bring a host of unexpected benefits, too. Once companies start changing processes to help reduce factors such as energy consumption, water use and waste, they often discover new opportunities to help reduce operating expenses, improve efficiency, and even to generate new revenue altogether.

Making progress with sustainability integration is not about having all the answers, but about having a process that can help you understand problems better, align decisions to the core purpose of the organization and create space to experiment with solutions.

5. Commit together to a better future

No organization or institution can address the sustainability challenge by themselves.

If the goal is to create a new economic system that operates within the planetary boundaries and ensures quality of life to all members of society, then every organization is being called to do its part—in partnership. This last (and often overlooked) goal in the list of 17 SDGs recognizes the importance of building multi-stakeholder partnerships and voluntary commitments to help mobilize resources, build capabilities, and drive innovation.

"Transformation can only happen if everyone works together. What’s missing is key players (financial market, regulators, corporates) working together. It is still occurring too much in siloes. We are seeing more collaboration, but the question is if it’s happening fast enough."

It’s time for concrete actions. Embracing transformation means investing in the capabilities, the capacity, the infrastructure, the technology, the enabling mechanisms that can help drive integration throughout the organization. It can also mean supporting experimentation for those who want to lead and help reduce costs and uncertainties for those who follow.

Although the scope of the challenges can be daunting, business leaders are in a position to make a significant impact, by focusing on the matters they effect and committing themselves to continuous improvement. Each internal change that takes place becomes another ripple that cascades outward, reshaping business ecosystems and eventually rewriting the rules of the road altogether.

{kind=link}

{kind=link}