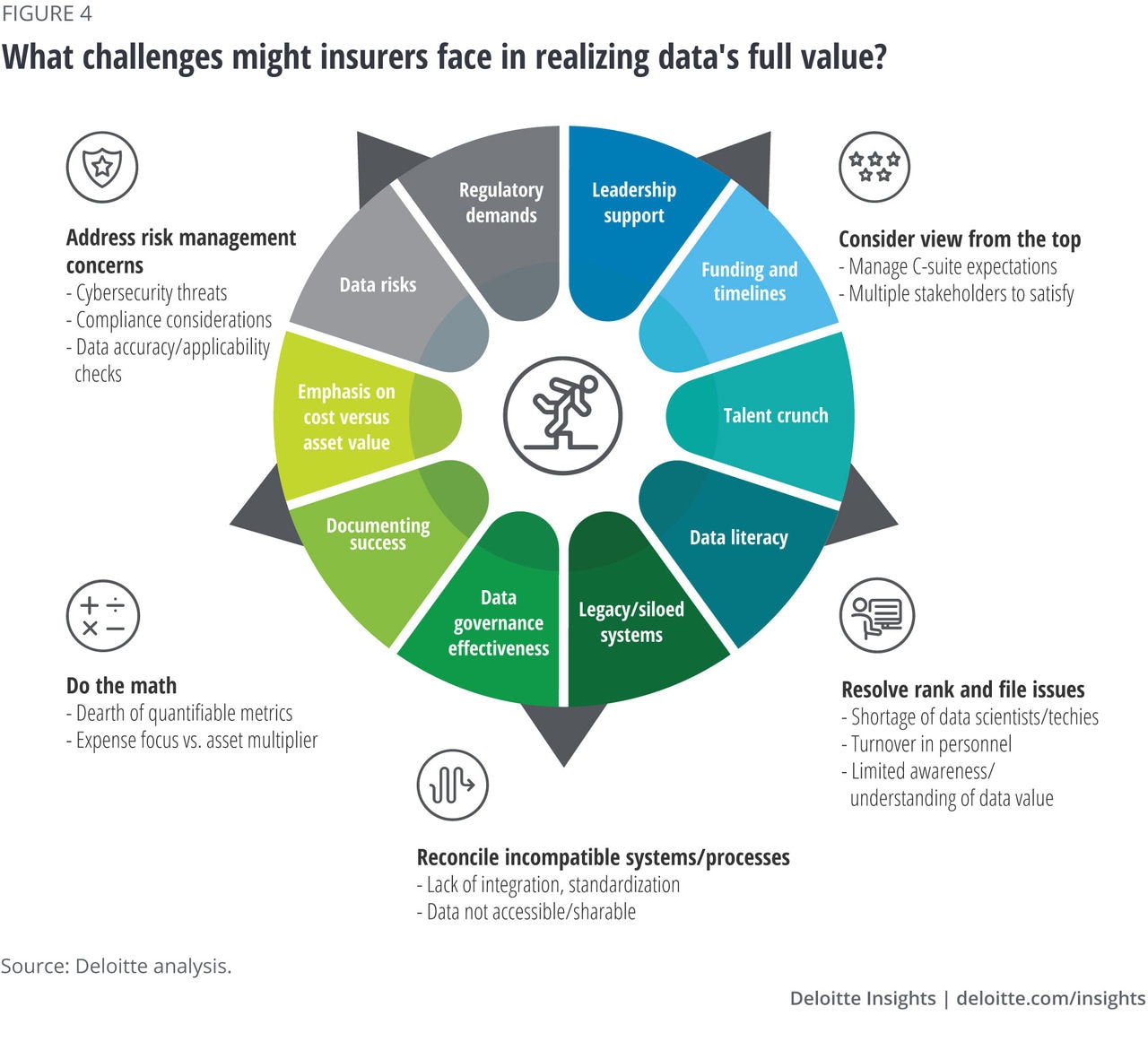

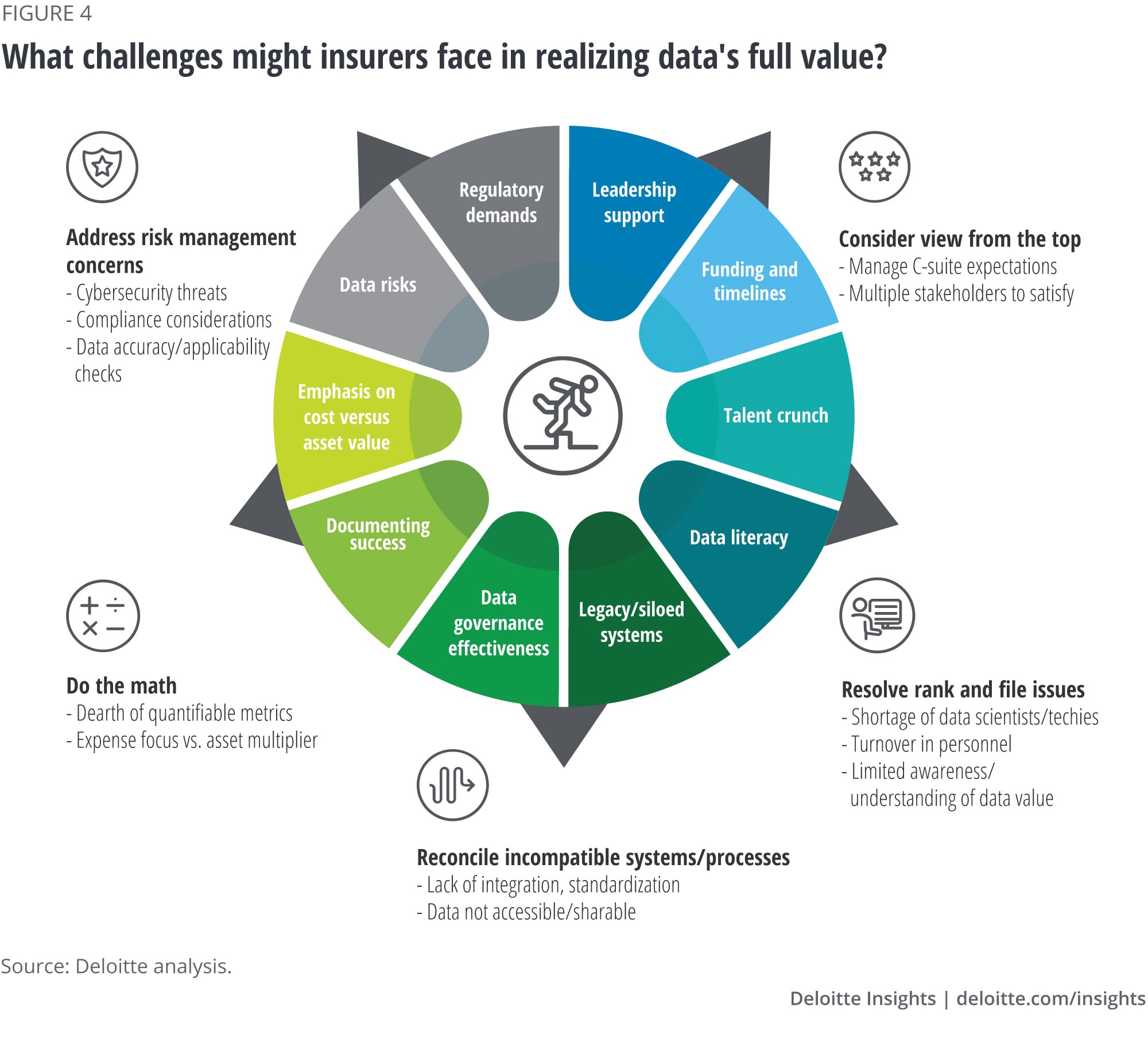

Do the math: Hard metrics may be hard to come by

Those interviewed often suggested that not all data and analytics spending can or should be expected to deliver quick or even easily measurable returns. This may be particularly true when they are part of broader transformation initiatives or are designed to help establish basic data management infrastructure—often necessary to overcome many of the challenges cited in figure 4. Sometimes it can be difficult to even provide a realistic estimate of the costs involved, let alone tie them quantitatively to outcomes, CDOs noted.

At the same time, interviewees conceded that expecting open-ended funding commitments from leadership may also be unrealistic without being able to provide some tangible proof of progress and improved outcomes. They often emphasized the importance of spotlighting periodic “wins” to maintain momentum and funding.

Use-case approaches were cited as a compelling way to retain leadership support, especially if they are tailored to a particular function and backed by a key performance indicator—such as cuts in processing time, improvements in closing rates, and reduction in fraudulent claims. These should suffice, at least in the Explorer stage of maturity, when insurers are focusing on improving the precision of pricing and effectiveness of claims handling—activities that can provide quicker, more quantifiable results.

However, it is also likely important for CDOs to keep leadership focused on a bigger-picture vision, or else the use case approach could lead to a continuation of fragmented architectures and siloed thinking.

Resolve rank and file issues

The “talent crunch” ranked high on the list of concerns among survey respondents—trailing only integration issues and data quality challenges. CDOs uniformly lamented their constant and worsening struggles to acquire the right talent, upskill existing employees, and retain those with the necessary capabilities to realize the true value of data and supporting analytical technologies.

Meanwhile, gaps in data literacy across the value chain were often cited for accentuating the disconnect between leadership expectations and execution of goals. Fragmented data management architectures, with information and responsibilities spread throughout the enterprise, can also present challenges in maintaining consistent standards and possibly hindering speed to market.

Reconcile incompatible systems/processes

One in five insurers surveyed characterized their data management governance process as “ineffective,” while one in four were only neutral on the question. A lot of that likely had to do with shortcomings cited in our one-on-one interviews, from the absence of holistic data governance to a lack of alignment between how data is generated versus how it might be used for advanced analytics. For example, the rapid influx of data from both internal and external sources is unlikely to deliver full value as long as information is stored in siloed and often incompatible legacy systems—making it tough to share, let alone scale for optimum value.

One carrier said that “if you want reusability and the efficiencies of scale across the organization, the walls between functions and business lines must be broken.” This is not likely to be an easy task for many insurers, noted one CDO, who observed that “in some cases, we’re erasing decades of significant legacy system obstacles.”

Address risk management challenges

As more personal data is collected and purchased by insurers, concerns over cybersecurity and privacy have multiplied. Yet only 32% of data leaders surveyed said they collaborated very closely with those in compliance. Meanwhile, the reliability, verifiability, timeliness, and relevance of data are among the many quality concerns that could undermine utility and value, while raising additional risk concerns.4

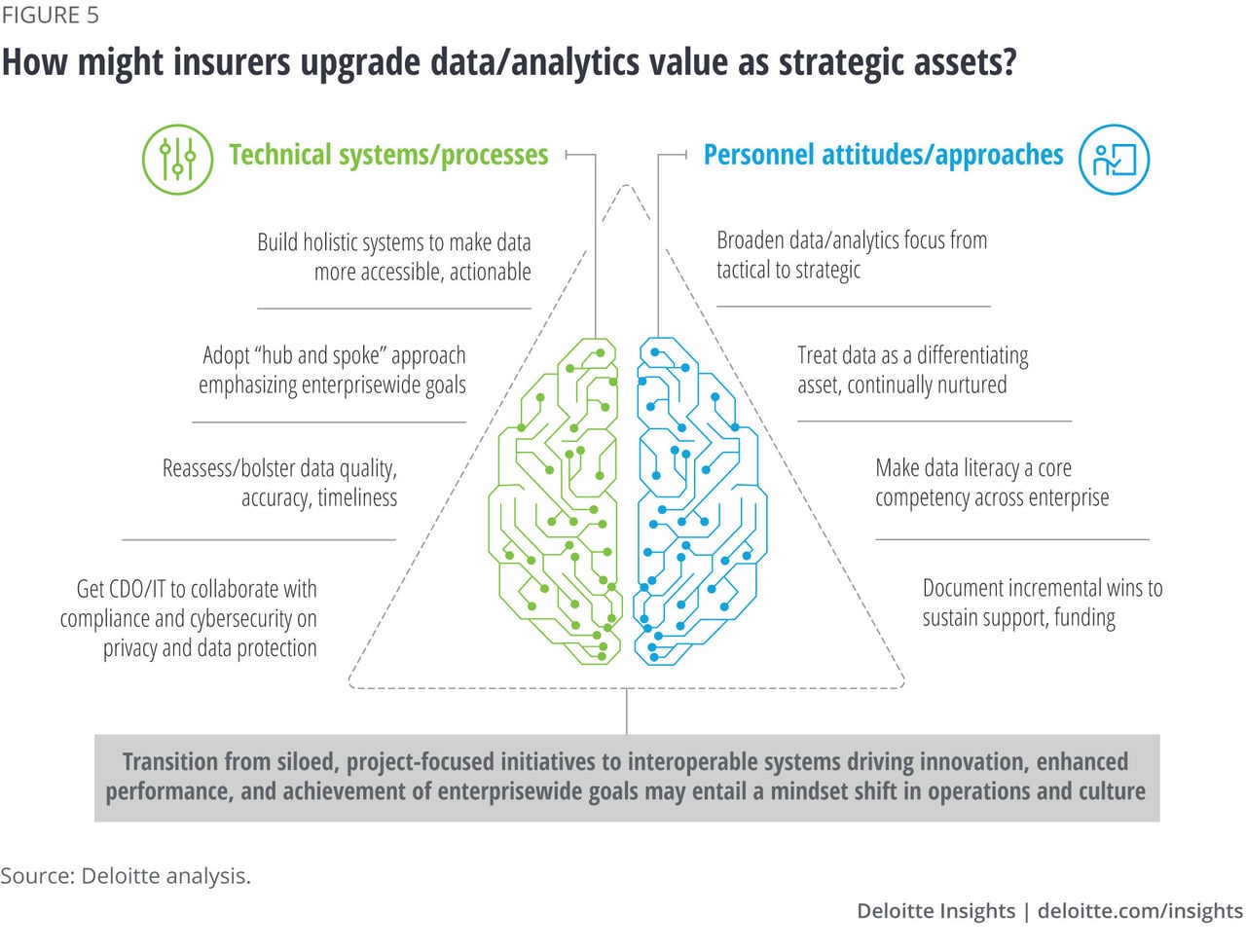

Next steps: Bending the maturity curve to bolster the value of data and analytics

An insurer’s ability to overcome obstacles and reach higher maturity stages so they may harness greater value from data and analytics investments will likely differentiate the leaders from laggards in an increasingly data-driven economy.

While “making a purposeful shift away from managing a mesh of siloed, inconsistent data,” as well as treating data as a strategic asset rather than an expense, are both important steps, according to the Deloitte AI Institute, “reaching the point of maturity where enterprise strategy and operations are data-driven can require a medley of phased actions.”5

Insurers might consider laying out a road map to establish a more holistic data management and analytics strategy linking the two sides of the organizational “brain”—technical systems and processes versus attitudes and approaches of the people executing the plan (figure 5).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}