The Future of Health in Europe

How technology and prevention will drive more equitable and sustainable outcomes for all

The future of health in 2040

Europe is facing substantial challenges in continuing to deliver high-quality healthcare services to its citizens. Ageing populations, cultural shifts, rigid and complex financing models, increasing costs of innovation, a scarcity of skilled personnel, rising health inequalities and health complexities stemming from climate change are threatening the sustainability and affordability of healthcare services, and adversely affecting citizens’ health and productivity. To ensure citizens’ future health and well-being, Europe will need to chart a new, cost-effective and sustainable approach to healthcare.

Deloitte’s Global Future of Health campaign, launched in 2017, is based on a strongly held view that emergent technologies and digital transformation, artificial intelligence (AI) and open secure platforms will enable a shift from the current reactive-treatment model to a continuous, forward-looking, proactive health management model. This shift will be focused on prevention and earlier diagnosis, aimed at sustaining well-being and improving the cost-effectiveness of healthcare. Moreover, by 2040 care will be organised around the citizen rather than around the institutions that drive the existing healthcare systems.1 These changes will affect the businesses and operating models of all stakeholders, including new non-traditional companies entering the healthcare space.2

While the original future of health perspective was based predominantly on the US, the changes driving this future are also relevant to every healthcare system in Europe. With its 743 million residents spread across 44 countries, including the 27 nations within the EU, Europe is a significant player in the global economic landscape.3 Its economic stature and robust foundation in science and technology means Europe is well-poised to pioneer sustainable and innovative healthcare solutions. Considering this, we have explored how Deloitte’s global vision of the future of health could be used to chart Europe’s healthcare future.

Why Europe needs a new healthcare vision

Each European nation manages its own healthcare, resulting in a tapestry of distinct systems, each moulded by its specific cultural, economic and political environments. Healthcare financing comes primarily from three sources, namely, government schemes, social health insurance (SHI) and private health insurance (PHI). Some countries, like the Nordics and the UK, predominantly operate on a single-payer system. Comparatively, Germany, Switzerland and the Netherlands have systems of competing insurers, whereas out-of-pocket payments are the dominant source of finance in most Eastern European countries.4

Health spending is primarily dictated by political decisions and correlates with each country’s economic size (GDP). While nations aspire for universal health coverage (UHC), the range of services offered and cost-sharing varies substantially. For instance, the average European healthcare expenditure as a share of GDP was 8.8 per cent in 2019. However, the range was quite wide, from 11.7 per cent in Germany to less than 5.5 per cent in Romania. There is also a three-fold difference in average health expenditure per capita between high-spending countries in Western and Northern Europe and low-spending Eastern European countries.5

The COVID-19 pandemic caused a series of unprecedented health, economic and societal crises and compounded deep-seated structural issues that some countries managed better than others. The ensuing disruption resulted in all countries increasing healthcare spending by nearly one-third compared to 2019. The lessons emerging from the pandemic demonstrate that health is the foundation upon which resilient, productive economies and fair societies are built. They also highlight that emerging pathogens and other public health threats do not respect borders.6

Despite the differences, a unified ambition exists across European healthcare players to ensure accessibility, equity, quality and safety. While health spending is projected to continue rising, funding levels are anticipated to align more closely with the pre-pandemic growth rate of three per cent annually. Moreover, funding disparities among countries are likely to persist, albeit with a narrowing gap as consumerisation and public expectations rise and central funding from the Resilience and Recovery funds of the European Commission (EC) is targeted towards financially needy nations.7

Due to the diverse pricing and reimbursement models across countries, current access to new medicines and innovative technologies varies substantially across Europe.8 Industry experts believe these disparities make Europe less appealing for healthcare innovations, as evidenced by Europe’s declining share of pharmaceutical R&D investment, clinical trials and manufacturing outputs over the past decade.9 In response, steps like the centralised Health Technology Assessment system, slated for 2025,10 and the 2023 update of the EU pharmaceutical legislation aim to foster a more conducive environment for healthcare advancements to produce a more innovative, and competitive market.11

In 2023, a deteriorating economic outlook further accentuated the scale of the healthcare challenge.12 In addition, climate destabilisation, including extreme heat, increasing air pollution, and the spread of infectious diseases pose multiple threats to the health and well-being of Europe citizens, adding further complexity to already beleaguered healthcare systems.13

In light of these escalating health challenges, a thorough transformation of Europe’s healthcare systems is crucial. Existing reactive and paternalistic healthcare frameworks are falling short in the face of rising demand and high inflationary costs, making it vital to transition towards a more sustainable, resilient and citizen-centric model.

The EC has acknowledged that the healthcare challenge and rising health inequalities, exacerbated by the pandemic, require an urgent, transformative approach to ‘level up’ healthcare capacity and capability. In November 2022, the Commission launched a new EU Global Health Strategy, which recognises that securing the health of European citizens is paramount. The strategy identifies the need for:

- A profound transformation of European healthcare systems, including a relentless focus on digitalisation and building a more sustainable healthcare workforce;

- Incentivising ‘greener’ healthcare systems; and

- Having a stronger focus on primary care and a far greater emphasis on prevention and keeping people healthy while giving them a greater understanding of and more power over their own health.14

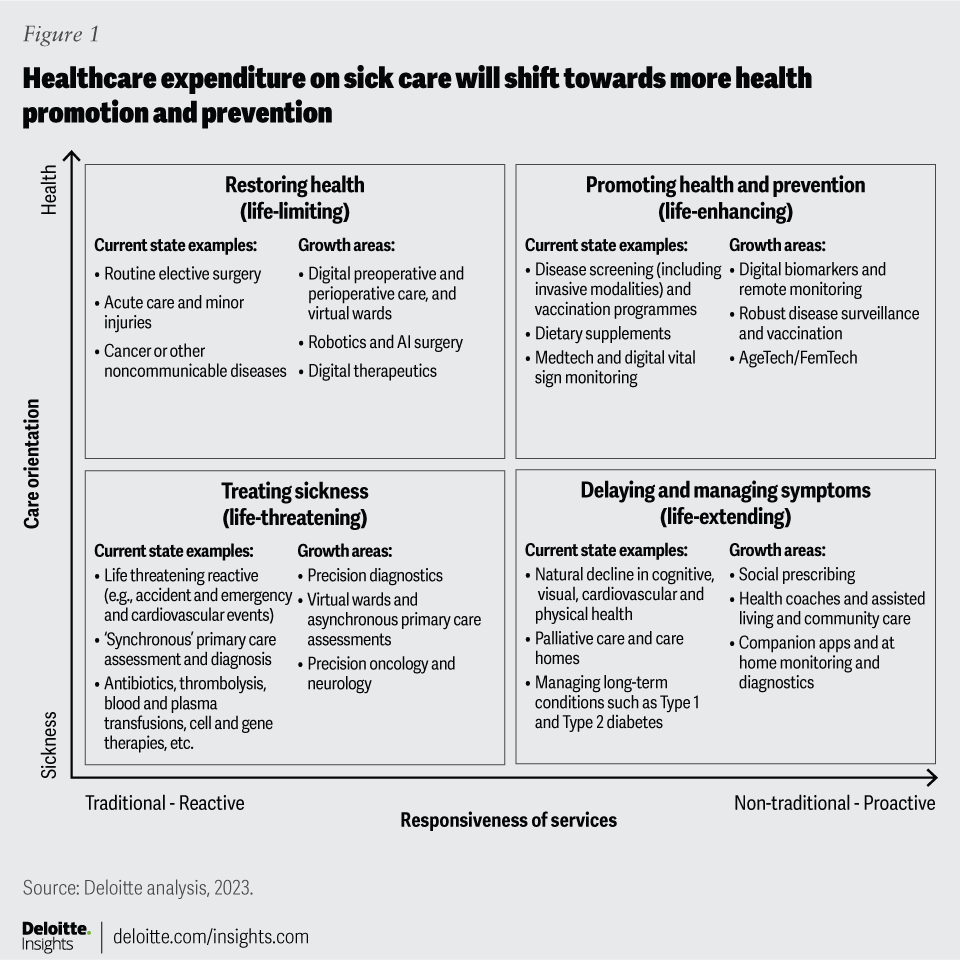

The present moment is pivotal for European countries, individually and as a whole, to reimagine the business and operating models running their healthcare systems, and adopt a more resilient, inclusive and innovative model that accentuates the well-being of its citizens. Such a transition shifts the focus from the current predominantly reactive and treatment-focused system, to one based on proactive health promotion, prevention and delaying and managing symptoms (figure 1). This vision of the future of health could simultaneously meet escalating healthcare demands in a more cost-effective manner and solidify Europe’s position as a torchbearer of sustainable and accessible healthcare globally.

About this report

This report explores six pivotal questions relating to this transition to the future of health in Europe:

- What is the envisioned state of European healthcare by 2040?

- How might the shift to the future of health redistribute healthcare costs?

- What implications might this healthcare transformation hold for incumbent business models?

- What are the principal catalysts for such a shift?

- How will the European healthcare system evolve for all stakeholders?

- Where do European nations stand when it comes to transitioning towards this model, and what should be their primary focus?

1. The envisioned state of European healthcare by 2040

Deloitte's envisioned model for the future of health in Europe is rooted in a holistic understanding of well-being that emphasises prevention over cure. By 2040, healthcare is envisaged to be population-based, efficient and more cost-effective. Treatments will embrace the ‘5P’ approach – predictive, preventative, participatory, personalised and precise – and foster longer and better-quality lives.

Advances in diagnostics and scientific breakthroughs, especially in the ‘omics’ fields (referring to biology disciplines whose names end in the suffix ‘-omics’, such as genomics and proteomics), are anticipated to provide solutions for many hitherto untreatable diseases. Concurrently, the onset of other conditions will be delayed or avoided altogether. When needed, hospital interventions will be minimally invasive, facilitated by innovative technologies in local, digitally enabled, specialised facilities – ensuring shorter stays and continuous patient monitoring (figure 2).

European healthcare systems will reorient to improve public and population health: Public health will become a government priority, focusing on early primary care engagement to promote healthier lifestyles. National public health organisations will fortify infrastructures and collaborate across Europe to build robust infectious disease–combatting strategies. Utilising artificial intelligence (AI) and digital tech, behavioural science, genomics and population data, public health providers will address health inequalities, promote healthy living and execute intelligent national screening and vaccination programmes. These authorities will share health data within a secure, trusted framework. Adopting advanced digital technologies will help overcome barriers like cost and geography, ensuring equitable access to services. These developments will also help meet public expectations of care being seamless, safe and secure, and will be pivotal in Europe’s healthcare transformation – laying the basis for a social compact between citizens and their providers.

Enhanced consumer experience: European citizens will have the autonomy to choose how, when and with whom they would like to engage, but they will expect digital-first and convenient access available through various local institutions such as clinics, community hubs, pharmacies, retail stores or at home. The 5P healthcare approach will promote holistic well-being and reduce long-term chronic conditions. While some individuals may have higher healthcare needs due to genetic or lifestyle factors, advanced technologies and early interventions will provide substantial support, minimising the need for acute treatments. By 2040, or earlier, a significant rise in health and digital literacy is expected, with more people seeing the use of digital health tools like wearables, AI-based chatbots and at-home diagnostics as the norm and healthcare professionals (HCPs) using the data generated to co-create personal health plans. This will foster a deeper understanding of personal health, well-being and increase trust and the options for optimising health outcomes.

Transitioning to a ‘hospital without walls’ model will create cost-effective, sustainable and equitable health systems: By 2040, all but highly specialised hospital care will be delivered through this model, using sensors and devices to connect HCPs with patients and other healthcare facilities. While there will still be a need for digitally advanced physical hospitals for critical care and specialised procedures, these ‘high-tech, high-touch’ hospitals will use AI technologies to optimise care delivery, workforce efficiency and back-office cost-effectiveness to reduce hospital stay durations and costs while improving patient outcomes and experiences.

European HCPs will experience greater job satisfaction and optimise use of their skills: The digital transformation of clinical work, accessible high-quality health records and automation will streamline administrative tasks, enabling agile and flexible work environments. A culture of trust and interdisciplinary collaboration will form with ‘blended teams’ of HCPs transforming care across the healthcare spectrum. Equipped with enhanced AI, digital, genomic, enhanced communication and social skills, HCPs will be backed by proficient teams leveraging advanced coding, AI analysis and data management tools. This setup promotes a collaborative partnership between HCPs and patients in crafting healthcare solutions.

Health equity will anchor patient-centric, collaborative health networks: Optimised health and cross-sector collaborations among private, public and non-profit entities will foster wellness. These collaborations, united in a shared vision and set of values, will empower all citizens to realise their fullest health and wellness potential. Central to this equitable and cost-effective health system will be radically interoperable data and advanced AI technologies. Furthermore, scientific advances, environmental sustainability and health equity will form the foundational principles for European countries’ approach to the future of health.15

2. How the shift to the future of health could redistribute healthcare costs

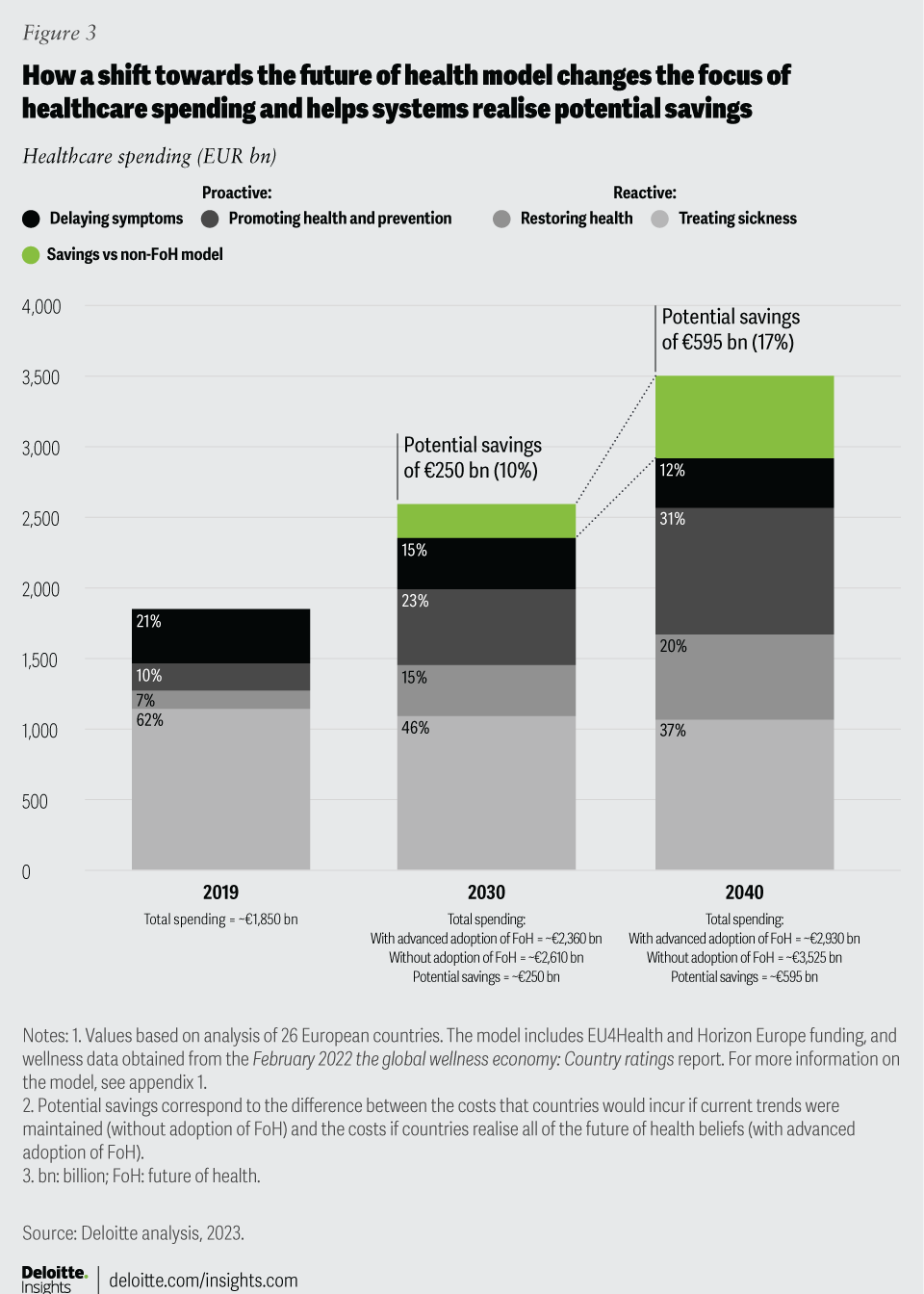

Shifting to this future of health model could significantly reallocate healthcare costs and improve health outcomes across Europe. We adapted a Deloitte-developed US actuarial model16 to gauge the impact of the future of health model on future healthcare funding in Europe. We used comprehensive healthcare spending data across 26 European countries (from 2013 to 2019; see section on methodology).17 Our analysis suggests that switching from focus on treating illness (reactive sick care) to a proactive emphasis on prevention, early detection and supporting wellness (figure 1), could help realise potential savings compared to current trends (which, if continued, could risk rendering healthcare unaffordable) (figure 3).

The modelling forecasts that, by 2040 (and sooner in some countries), a higher proportion of funds (51 per cent compared to 17 per cent in 2019) will target health promotion, illness prevention and health restoration. A much lower proportion (49 per cent compared to 83 per cent in 2019) will target sickness treatment and symptom management. This shift would lessen disease incidence and severity, altering Europe’s expected cost curve and potentially reducing healthcare spending by nearly €250 billion in 2030 and close to €595 billion by 2040. This saved 'well-being dividend' would be higher in countries spending a high percentage of their GDP in healthcare but could be used to accelerate the realisation of the future of health model in countries with steeper health challenges.

How redefining value and returns will drive healthcare transformation

Redefining value and return on investment (ROI) in healthcare, particularly emphasising prevention, is crucial. A 2017 review revealed that every €1 spent on health promotion and disease prevention yielded a €14 return to the economy and that although quantifying returns within a short time scale can be challenging, larger ROIs were seen over ten to 20 years.18 Despite such evidence, European investment in prevention remains inadequate, highlighting the need for a robust focus on ROI analysis that underscores both the health and non-health benefits.19

Healthcare valuation is a complex endeavour, viewed differently by each stakeholder, and is often conducted in silos. Traditionally, government health investments have correlated closely with their GDP, while this provides a consistent cost metric, it overlooks the ‘return’ aspect of such investments. Indeed, governments and other healthcare payers have tended to evaluate value by cost per activity, whereas medical technology and pharma companies have measured value by the willingness of investors to fund innovation and profits generated. Transitioning to the future of health necessitates a crucial departure from mere cost evaluations towards a more holistic outcomes assessment, viewing health and wellness as worthy investments. This is an essential element in the transition and will ensure that healthcare is seen as an asset to every economy – not simply a cost.

Methodology for the financial modelling of the future of health and how the cost curve will change

The calculation presented in figure 3 is based on a methodology developed in 2021 by Deloitte’s US Healthcare actuaries in collaboration with industry leaders, proposing that emerging technologies, scientific innovation and consumerisation could lead to better health outcomes and decelerate healthcare spending.

This analysis report Breaking the cost curve presented an in-depth modelling of the financial implications of the future of health vision. They used data from 2011 to 2018 from the National Healthcare Expenditure Accounts to model the impact of six transformative forces shaping the future of health: data sharing, interoperability of data, equitable access, the empowered consumer, behaviour change, and innovative, scientific breakthroughs. The analysis models how the move from a reactive, treatment-based system to a proactive, preventative system would affect the cost of care.

We adapted this model to data from 26 European countries (23 EU nations plus Norway, Switzerland, and the UK), using OECD’s health expenditure data (from 2010 to 2019; excluding 2020 due to COVID-19–related spending spikes) to provide an estimate of how consolidated healthcare funding might change. We projected these healthcare costs up to 2040, distinguishing between Deloitte's current-state and future-state healthcare archetypes. In this projection, for 2019, 90 per cent of total expenditure was mapped to the 12 current-state archetypes, with the remaining allocated to 29 future-state sub-archetypes, considering some changes are already underway.

Additionally, wellness data obtained from the 2022 The Global Wellness Economy: Country Ratings and 2026 projections from ongoing EC initiatives were incorporated to estimate the potential impact of bespoke investment on future European healthcare spending – particularly on digital transformation.

Deloitte’s healthcare leaders across Europe helped evaluate the impact of six transformative forces on their country’s healthcare expenditure trends through three innovation cycles (2020–2026, 2027–2033 and 2034–2040). The higher each impact was rated, the higher was the percentage of money carved out each year from current to future-state sub-categories, showcasing how these six forces could shift healthcare spending, with two-thirds slated for future-state archetypes in 2040.

This transition hinges on all stakeholders, including governments, insurers, HCPs, regulators, academia and industry partners adopting characteristics of one or more of the 29 future-state sub-categories, moving towards more networked business models from the current siloed industry segments.

Finally, funding is either allocated as more traditional reactive healthcare spending or non-traditional proactive expenditures. The difference or ‘well-being dividend’ highlights how embracing the future of health alters spending patterns, potentially curbing the persistent yearly cost escalations to provide more affordable healthcare systems across Europe (figure 3).

3. Implications for incumbents’ business models

Presently, healthcare incumbents focus mainly on disease treatment, and account for 85 per cent of the industry expenditure (see methodology).20 These incumbents include hospitals, other healthcare providers, HCPs, life sciences companies and payers. At the same time, employers are increasingly investing in partnerships that improve the physical and mental health and well-being of their employees.21 The future of health would pivot Europe towards new business models reshaped by technological advancements and regulatory shifts; as well as engaged citizens, empowered with highly personalised data who will increasingly favour organisations prioritising their overall health and well-being.

Such well-being– and prevention-focused business models are already gaining traction across Europe and will disrupt traditional models significantly by capturing a growing share of health revenue – thereby heralding a transformation in dominant healthcare business frameworks.

Deloitte expects the three dominant business models to transform radically:

- End of treatment-focused general hospitals: Today, many European countries are beginning to shift from acute hospital-based treatments to more localised, integrated, cost-effective care settings. Citizen preferences and technological advancements are driving this. For example, an acute myocardial infarction would require hospitalisation; under the future of health model, continuous in-home monitoring could prevent such severe events altogether. Acute or emergency care, when needed, will be provided in specialised settings tailored to a specific need, ensuring precision care instead of a one-size-fits-all approach.

- Slowdown of mass-produced therapies: Advancements in science, technology and availability of massive amounts of health data are enabling pharmaceutical (pharma) companies worldwide to transition from developing mass-produced therapies to more precise, targeted treatments, including using AI technologies to accelerate drug discovery and enhance clinical-trial efficiency. This change is accelerating and disrupting traditional pharma models with a future focused on individualised treatments or treatments for specific groups, which could lead to cost-effective and highly effective products customised to individual genetic and behavioural needs.22 These transformations will revolutionise the pharma value chain from R&D to prescribing – aligning with value-based healthcare (VBHC) models.23

- Transition in healthcare financing and funding models: Despite UHC being a cornerstone of European policy, current funding models in some countries struggle to provide UHC and meet the related Sustainable Development Goal (SDG) to ‘ensure healthy lives and promoting well-being for all at all ages.’24 For others, the cost of funding UHC is becoming unaffordable. The necessity to re-evaluate funding and emphasise outcomes is evident. For example:

- Europe’s current social insurance and taxation models distribute health-related risks across populations to offset the higher costs of less healthy members against the lower costs of healthier members. This favours the traditional volume-based hospital model over citizen-centric primary care and preventive care models. However, advancing health technologies that can capture relevant performance and outcome measures will change the risk dynamics. This shift, powered by data-driven individual risk assessments, paves the way for personalised health products tailored to align with citizens’ risk profiles, lifestyles and behaviours.

- The future of health model anticipates a move towards outcome-based financing targeting healthcare’s quintuple aim: better outcomes, lower costs, enhanced patient outcomes, HCP well-being, and health equity.25 For example, strategies like individual/population capitation and cost-sharing models increase financial certainty. Risk sharing, payment-by-results and outcome-based subscriptions, including data-as-a-service, assure outcome certainty. Funding innovation comprising public-private mechanisms such as social investment financing, green financing and more innovative cross-sectoral investments addressing the social determinants of health can reduce health inequalities. Using tools like social impact bonds and social outcome contracting, banks, national investment banks and private finance institutions can create collaborations to bridge investment gaps and redefine health-promoting systems and services.26

4. Catalysts for a shift to the future of health in Europe

Despite their diversity, all European healthcare systems have the potential to realise the future of health model by 2040 or earlier. Though transformation speeds will vary, European countries will increasingly unite around a shared ‘good health for all’ vision and work more collaboratively to build equitable, resilient affordable healthcare systems.

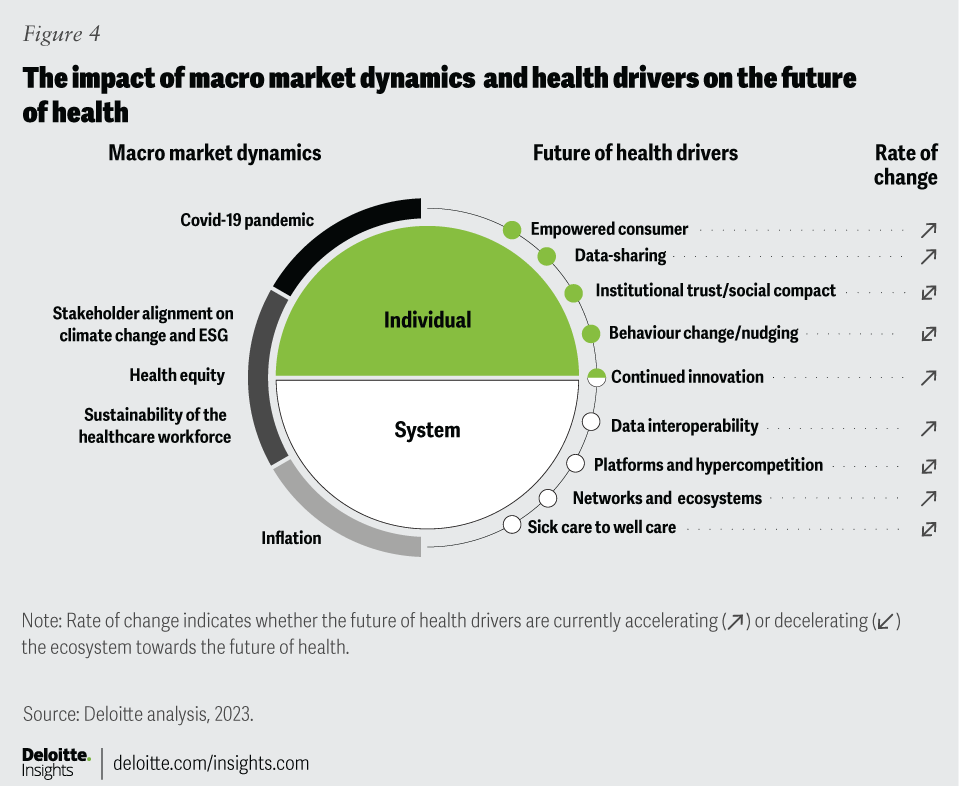

Figure 4 highlights the macro dynamics and health drivers that will affect the pace of change.

ESG (environment, social and corporate governance) climate change and health equity: Unequivocal evidence links physical and mental health with climate change, highlighting the crucial role of all stakeholders in the health ecosystem.27 Evolving regulatory standards and compliance requirements mandate organisations to mitigate ESG risks and demonstrate actionable diversity, equity and inclusion (DEI) policies. This also entails stakeholders taking greater accountability for minimising their adverse environmental and social impacts while enhancing the health and well-being of employees, their families and the communities they operate in. There are also internal pressures from employees and investors, to integrate DEI commitments and climate change mitigation into business strategies and investment decisions and external pressures to promote equitable access and outcomes.28 The swiftness with which health ecosystem stakeholders respond will expedite the journey towards the future of health.

Sustainability of the healthcare workforce: Most European countries face growing shortages of HCPs leading to reduced hands-on care, declining staff morale and lower productivity. Despite the varying scales of the challenge for individual nations, common concerns include the costs and quality implications of maintaining safe staffing levels and recruitment and retention hurdles. In 2020, Europe had an estimated shortfall of 1 million HCPs, a situation worsened by the pandemic and aggravated by a ‘brain drain‘ of medical professionals seeking better working conditions and pay.29 Furthermore, HCP availability varies significantly across countries (a three-fold difference in the number of practising nurses per 1,000 people and a two-fold difference in number of practising doctors per 1,000 people).30 Moreover, 40 per cent of medical doctors are aged over 55 years in 13 of the 44 reporting countries.31 This scenario necessitates bold, innovative long-term strategies in workforce planning, recruitment, skills development and flexible working arrangements.32 Digital transformation and AI adoption will augment HCP skills and improve healthcare delivery productivity.33 Re-envisioning the future of work – identifying automatable tasks, defining roles and determining work locations – will be crucial for advancing towards the future of health.

How individual drivers could affect the pace of transformation

As in figure 4, there are nine drivers that will influence progress toward the future of health. Five of these drivers –consumerisation; interoperable data and data sharing; continued innovation, including AI; and networks and ecosystems – are unstoppable although the pace of transformation may vary from country to country. The other four drivers, however, will need more affirmative action or risk-decelerating progress.

Drivers that accelerate progress towards the future

Consumerisation: Increased awareness among European citizens regarding service quality and access and how this compares to other countries is amplifying the push for more equitable healthcare services. The pandemic also showcased the benefits of data sharing, digitalisation and embracing scientific and technological innovation. This is paving the way for healthcare’s cultural, digital and economic transformation – a trend likely to continue irrespective of policy changes or individual stakeholder actions.

Interoperable data and data sharing: Despite their essential role in the future of health, progress in these actions has been slow due to varying levels of digital literacy, the digital maturity gap among Europe’s health systems and regulations like the General Data Protection Regulation (GDPR).34 However, Deloitte’s 2020 research found that most countries had established digital transformation strategies to address interoperability and health data sharing.35 For example, the EC’s 2030 Digital Compass and the European Health Data Space (EHDS) aim to bridge these gaps by promoting digital transformation and securing health data sharing across Europe. Coupled with national efforts from countries like France, Italy, the Netherlands and the UK. Moreover, interoperability standards like the Fast Healthcare Interoperability Resources (FHIR) are expected to be adopted by 2024, which will speed up the transition towards new care models. The EC also expects every citizen to be able to access their medical records, strengthen their control over their own health data and secure the use of health data for innovation, policymaking and research.36 Eighty per cent of EU citizens aged 16 to 74 are expected to have at least basic digital skills by 2030 and all citizens to have online access to their health records.37

Continued innovation: The speed of scientific and technological innovation, especially during the pandemic, has expedited opportunities to enhance healthcare outcomes, albeit at a high cost. As citizens become more tech-savvy, demand for such innovations will only grow, with consumer health and technology disrupters stepping in to fill unmet needs. The evolution of AI-enabled healthcare technologies holds the potential to transform healthcare delivery across the spectrum – from streamlining back-office operations and medical imaging to expediting drug discovery and clinical trials.38 Advanced AI, particularly, generative AI, aligned with emerging data standards and regulations, is poised to significantly impact all aspects of healthcare by improving operational efficiency and enhancing personalised experiences for patients, resolving data interoperability issues, expediting the realisation of 5P medicine and bolstering digital and data capabilities.39

Existing networks will expand, propelled by collaborative ways of working that intensified during the pandemic , leading to a surge in strong research partnerships and innovation hubs that foster best practice sharing. Multiple types of trusted partnerships between industry, academia and providers, with shared views on value exchange, backed by a creative and reputable financial services sector and government initiatives, will create optimal conditions for the development of new business models, delivering improvements across the health ecosystem.

Potential obstacles to progress

Promoting institutional trust: Institutional trust and a well-understood social compact are pivotal for realising the future of health. Trust significantly shapes healthy behaviours, including encouraging individuals and their families to become vaccinated, have regular check-ups and embrace healthy lifestyles.40 Trust also influences people’s participation in preventive screening and crucial health services. However, trust levels vary markedly, as highlighted by a 2022 European survey, which revealed that trust in their healthcare systems to provide the best available treatments ranged from 91 per cent in Portugal to a mere 10 per cent in Hungary.41 Notably, people who experience discrimination due to factors like age, ethnicity, gender or socioeconomic status tend to have more negative health outcomes and trust their system less. Addressing this requires stakeholders to enhance transparency and adopt responsible policies geared to mitigate social and economic inequities, thereby fostering more trusted relationships with citizens.

Encouraging behavioural change: Altering individuals’ behaviours towards healthier lifestyles is challenging. Despite abundant evidence that investment in prevention is fundamental to a resilient and sustainable health system, spending on prevention through the various country-level financing schemes (whether government schemes, SHI or PHI) remains remarkably low, averaging less than three per cent of total spending by all healthcare players.42 Consequently, a growing socio-economic divide in health behaviours exists across most European countries; individuals in higher socio-economic groups tend to have better health literacy and invest more of their own money in improving their health, while those in lower brackets often have less health literacy, engage in unhealthier lifestyles and have fewer resources for improving their well-being. Addressing this disparity extends beyond isolated measures like sugar taxes and public smoking fines; it requires comprehensive cross-government actions, incentives, taxes and regulations to ‘nudge’ people to make better choices. Moreover, peer groups, local communities, employers and charities are integral to improving public health within local communities.43

Advancing platforms and hyper-competition: Platform-based, technology-enabled interactions between citizens and health stakeholders will accelerate the future of health. Currently, industry stakeholders compete for siloed sections of the care pathway, but disrupters and technology are prompting payers and citizens’ demands for price transparency and wellness-focused end-to-end clinical pathways. Many health technology innovators are developing platform-based business models to meet these expectations, which will eventually draw all stakeholders together to provide a seamless end-to-end care pathway. Such models can enhance and broaden service offerings by leveraging the wider digital network to co-create goods and services, improving choice. As healthcare products diversify, no single organisation can dominate the full spectrum of care, making the platform business model attractive for producing comparable outcomes with lower capital costs.44 These models facilitate information sharing and goods and services exchange among ecosystem players, competing based on consumer experience. The adoption rate of these platforms will significantly influence the pace at which the future of health is realised.

Transforming from sick care to holistic well-being: Europe’s prevailing reactive sick care model has historically overshadowed holistic well-being approaches. Despite numerous policies aimed at improving service integration, transitioning care outside of hospitals and emphasising prevention and primary care, the shift from acute hospital-centred treatments has been slow. Transitioning the model necessitates challenging entrenched attitudes, although research shows it benefits population health and cost-effectiveness. Achieving this transition requires committed leaders to overcome resistance from stakeholders comfortable with the status quo and foster a collaborative environment focused on quality improvement, safety and effective communication strategies and to design services around the needs of individuals. New funding models are imperative to support these changes. History indicates that such transitions are challenging, time-consuming and require a change management approach. Crucial investments in primary care, public health-led integrated systems, a healthcare workforce proficient in AI, digital and genomics skills, and the advancement of digitally mature, interoperable data systems are essential for success.

5. How the future of health could evolve for individual stakeholders

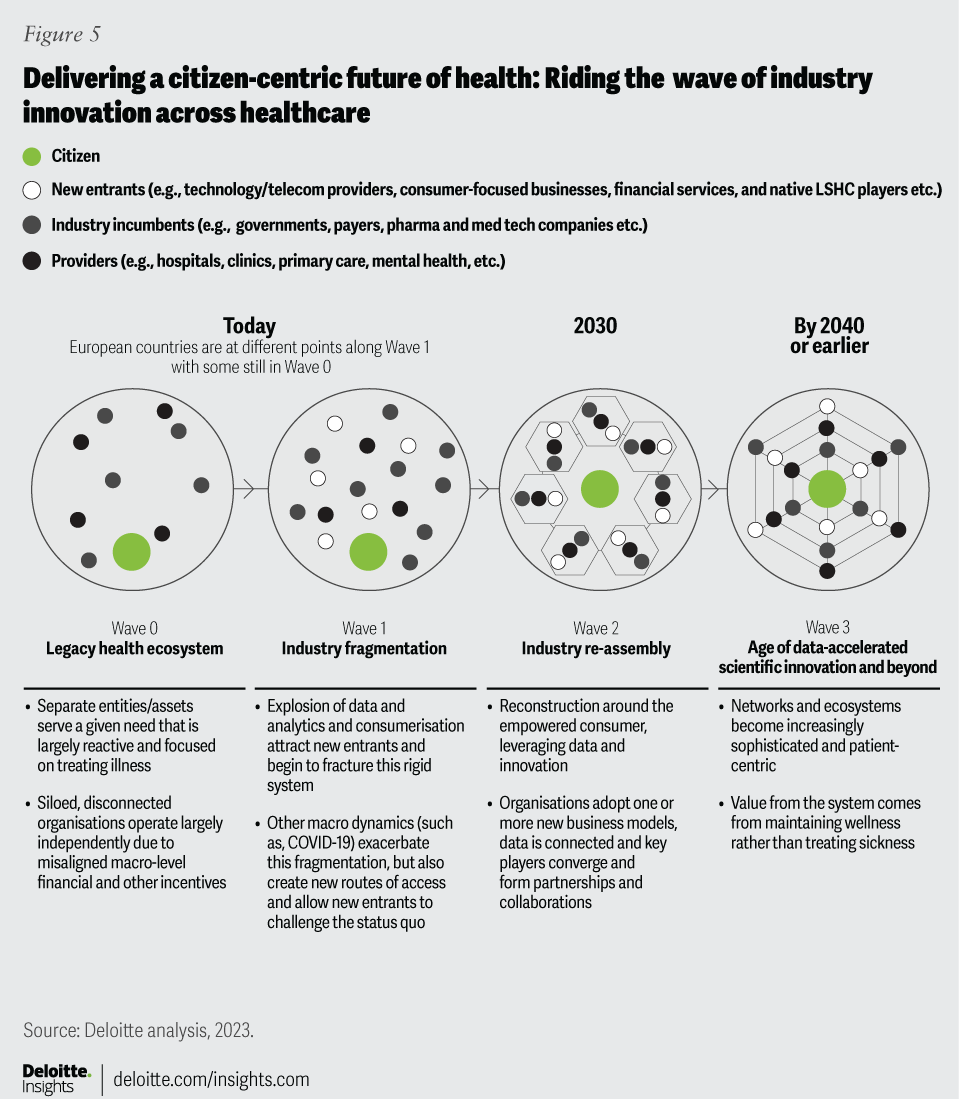

European healthcare is on the brink of a significant transformation, with organisations moving from the current siloed system to an interconnected network of partner organisations (figure 5). Legacy stakeholders face a choice: evolve or defensively protect their existing market share. Those who reinvent themselves can contribute to realising the future of health, while others might succumb to external competition.

This transformation, driven by enhanced customer engagement and data connectivity and interoperability, will redefine traditional roles within scientific and healthcare domains.45 In the future of health landscape, stakeholders like MedTech, pharma and technology companies and big data organisations will assume new roles (see methodology) aligning with outcome-based care delivery. These roles will harmonise existing capabilities, core missions and shared values towards a unified goal, presenting a distinct outlook for every stakeholder involved.

Governments, private and public insurance organisations and other payers will implement UHC for core services using new outcome-based funding models: Providing equal levels of universal access and financial protection for citizens will be embraced across Europe by 2040. Many countries will adopt UHC earlier, propelled by strengthened commitments to the SDGs. Clear strategies and targets will define covered services and the responsibilities of individuals and providers. Regulatory and legislative measures will remove financial barriers, harmonising services through multi-sectorial agreements and new public-private partnerships. Payers will transition from ‘treatment plans’ to emphasise prevention and well-being, employing novel business, funding and regulatory models. New revenue streams with customised offerings will incentives healthy behaviours among citizens. With the advent of advanced personalised treatments, governments and other payers will seek evidence on ROI, reduced health inequalities and improved environmental and social sustainability.

Empowered citizen: Individuals will have effortless digital access to their secure health records and will define who uses their data and for what purposes. With digital proficiency, they will proactively manage their health risks, leveraging AgeTech, FemTech, geriatric science, and precision and regenerative medicine for insights into healthy ageing. Hyper-personalised insights from validated apps, connected devices and wearables will foster a commitment to physical and mental health through tailored exercise and nutrition. Although individual responsibility for health will be well-understood, some will benefit from ‘nudges’ via virtual health coaches and digital twins to modify their behaviours. The shift to prevention will include genetic testing, new vaccines and continuous health monitoring through ingestible and embeddable technologies, alongside personalised supplements and prophylactic treatments to boost their microbiomes and prevent disease. Facial recognition technology will detect mental health changes and behaviours, with mood and sleep monitored. As sensors and genetic testing costs drop, individuals will be willing to invest in personalised therapies.

A sustainable healthcare professional workforce: Advances in AI robotics, cognitive automation, data sharing and digitalisation will bolster productivity and work/life balance for HCPs. Empowered multi-professional teams will manage workflows and schedules effectively, enjoying enriched career paths. Task shifting and reorganisation will be commonplace based on adaptive, agile work methods, and will foster a diverse, blended workforce. HCPs will engage in multi-professional training enabled by scientific and technological innovations to understand data management, and the ethical, privacy and security considerations linked to digital technology. Diagnosis and treatment decisions will evolve to align with 5P medicine, driven by breakthroughs in AI, enhanced connectivity, nanotechnology and quantum computing. AI-supported clinical decision tools will aid HCPs in delivering hyper-personalised diagnostics and evidence-based interventions. Using virtual reality/augmented reality (VR/AR), customer relationship management systems (CRM) and data analytics, HCPs will comprehensively understand individuals and promote personalised, omnichannel engagement.

Healthcare providers will adopt a patient-centric, digital-first approach with end-to-end visibility of outcomes: European citizens needing support will be automatically directed to the most appropriate care setting. Primary care networks will address population health needs through a person-centric model, using AI for remote monitoring and point-of-care diagnostics while harnessing real-world data (RWD) on vital signs. The fusion of data science, cloud technologies and consensus on interoperability standards will enhance the accessibility and security of health records, enabling seamless data and insight retrieval through blockchain-like, open-source technology. Virtual command centres will oversee relationships using AI-amplifying services like connected ambulances, e-pharmacies and AI-enabled pathology and radiology. Community health hubs and ‘hospitals without walls’ will offer top-tier health and wellness services. Collaborating with big tech, product developers and telecommunication companies, well-being providers will leverage the low latency of 6G/edge computing in critical care for on-demand and remote robotic surgery. Hospitals will restructure their business models, concentrating on high-acuity, complex cases and using advanced technologies for a seamless, data-driven patient journey.

MedTech companies will drive VBHC: AI-enabled products and services technologies will enable a better understanding of the clinical context in which they are used, providing cost-effective solutions. MedTech will use sophisticated data analytics and work closely with end users to develop new cognitive technologies for better health outcomes. Partnering with consumer and tech companies will enrich their advanced analytics, brand development and customer engagement. Companies previously focused on hardware (diagnostic and surgical equipment, joint replacements, pacemakers, etc.) will broaden their focus to include data collection, analysis and software that align with evolving care models. Many will transition to ‘software-as-a-service’ providers, emphasising preventative care for specific patient groups. Companion diagnostics will play a crucial tool in personalising therapies. These strategies will differentiate products, shield against price erosion, create long-term customer trust and increase market share and revenue. Innovative payment models like risk sharing and flexible per-person per-use arrangements will support new engagement models. To stay relevant, Medtech will adopt FAIR principles (findable, accessible, interoperable and reusable data) and robust governance frameworks, employing ‘security by design’ through data encryption and authentication mechanisms. They will collaborate with healthcare providers to manage AI ethics, data privacy and cybersecurity challenges.

Pharma companies will use AI across the value chain to increase productivity and facilitate the delivery of 5P medicine: Optimising R&D and manufacturing processes will be crucial for pharma to realise effective ROI on innovation. Enhancing supply chain security and access to innovative drugs will spur the development of hyper-tailored therapies that cure disease rather than treat symptoms. Through AI-enabled digital platforms, adherence to FAIR data principles and research partnerships with academia and tech entities, pharma companies will radically change their operating models, improving success rates and reducing drug development costs and time. Innovative decentralised clinical trials will identify new patient-centric digital endpoints and indications. Companies will employ data-rich visualisation tools for virtual clinical trials, ensuring faster recruitment, enrolment and monitoring of diverse patient groups. Generative AI technologies will accelerate drug discovery with more precise pathologies. Using apps and wearables, e-consent platforms, and telehealth will curtail clinical trial time and financial costs. De novo design, in silico computer simulations and synthetic control arms will accelerate decision-making at critical milestones. Advanced analytics, control towers and digital twins will aid in simulating and monitoring clinical trials, manufacturing and supply chain operations. Patient groups, offering a unique 360-degree perspective on patients’ lives, will be crucial participants in designing and managing clinical trials and post-market surveillance.

Collaborative VBHC partnerships among all stakeholders will advance the future of health in most countries: Given Europe’s size, economic outlook, robust science base, and innovation-friendly regulations. These factors create a conducive environment for sustainable, mission-driven healthcare collaborations. Trust within and among innovation clusters will enable strong research partnerships among academia, product developers and patient groups. These partnerships will inform R&D and generate evidence on outcomes and product/service effectiveness to share with HCPs and citizens. National and local governments have created favourable economic environments to stimulate investment in life sciences R&D. Systematic funding through public-private partnerships and venture funding fosters scalable innovation. RWD and aligned objectives help compliance with regulatory legislation and to coordinate timely responses. Data forms the foundation of VBHC partnerships, with patients readily sharing health data in a value exchange. Emerging standards for data analysis, sharing and transparency enhance trust, drive efficiencies, broaden patient access and lower costs.

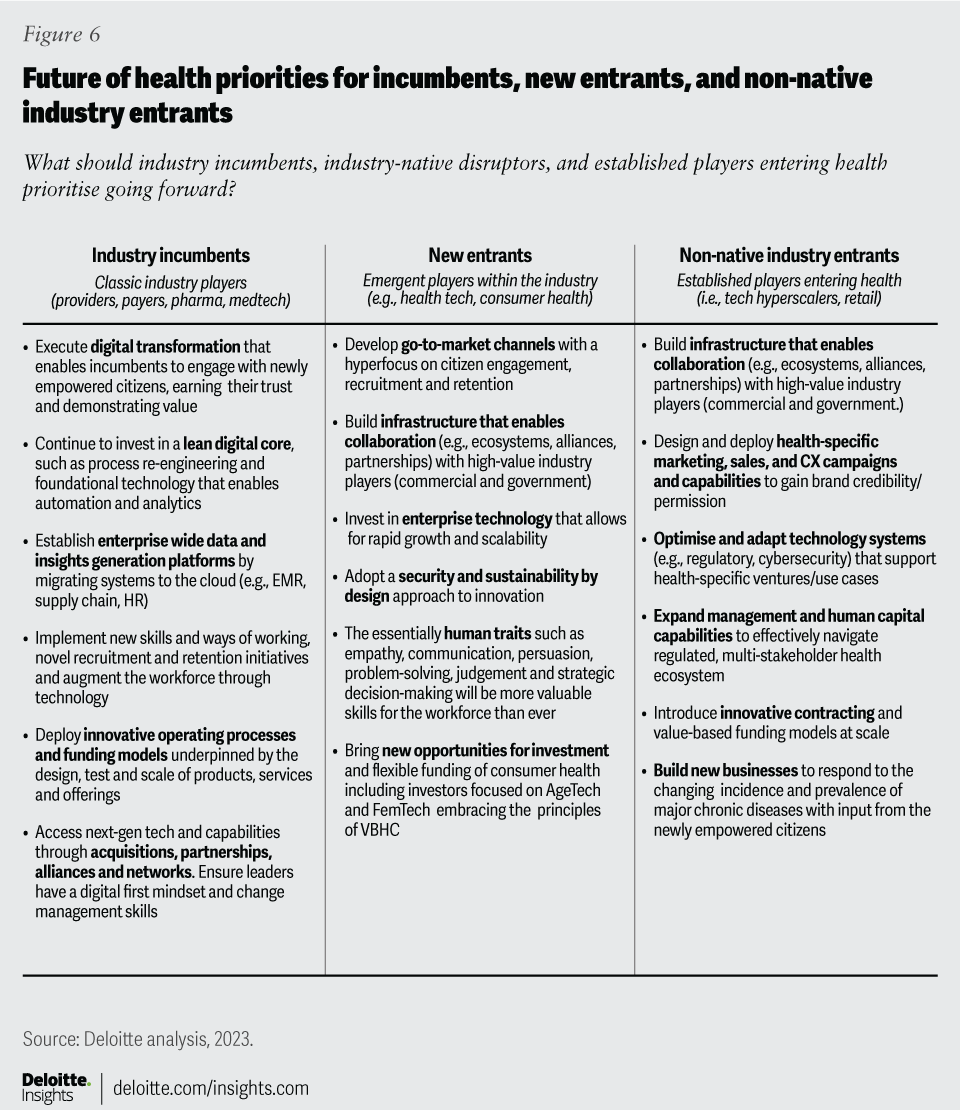

Figure 6 details the actions that stakeholders – incumbents, new entrants and non-native entrants – should consider when preparing themselves to be an effective part of the future of health in Europe.

6. Where European countries stand in transitioning towards the future of health

Europe’s nations differ in their progression towards the future of health due to:

- Healthcare market size and funding

- Digital infrastructure maturity and data-sharing capabilities

- Digital and health literacy levels and health behaviour cultures

- Citizen engagement, empowerment and trust

- Service choice and equitable access

- Research, innovation partnerships and collaborations

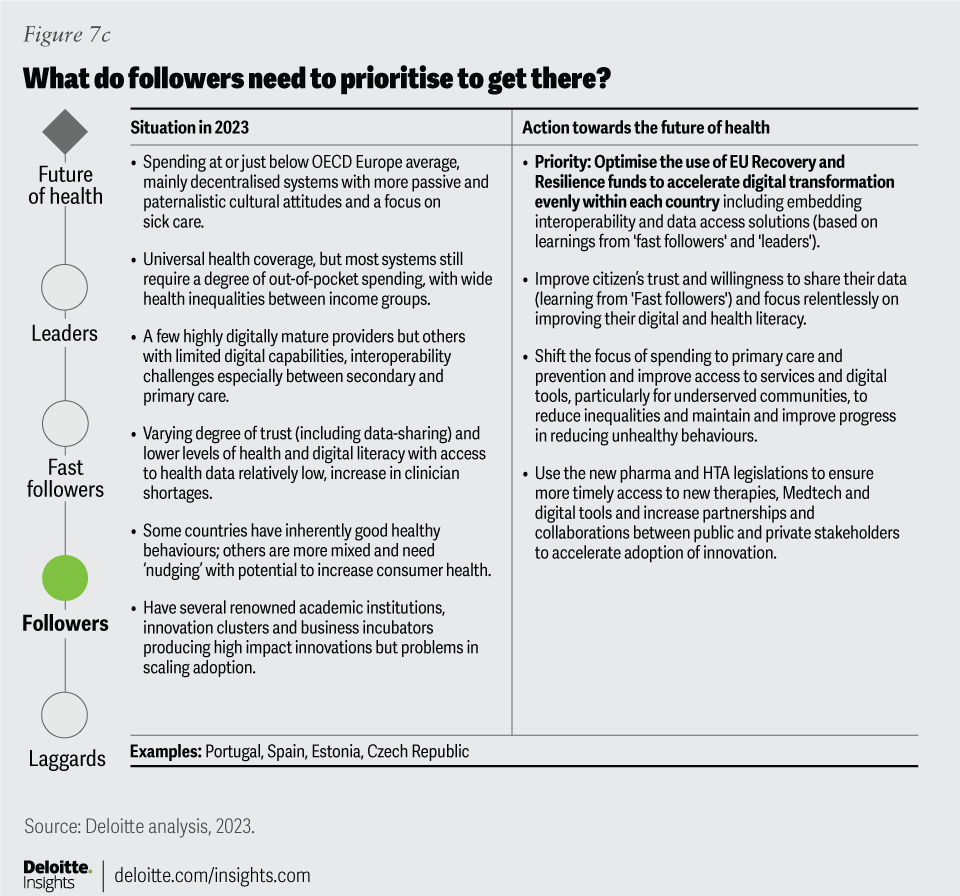

After long periods of static approaches, many European countries are re-evaluating their healthcare systems. Countries like Finland, France and the UK have initiated significant reforms. Conversely, nations like Italy, Spain and some Eastern European countries, bolstered by the EC’s ‘Recovery and Resilience Facility,’ are better-positioned to overcome historical barriers and implement substantial reform programmes. Nevertheless, each country’s journey towards the future of health depends on top-down and bottom-up leadership, coupled with a commitment to change.

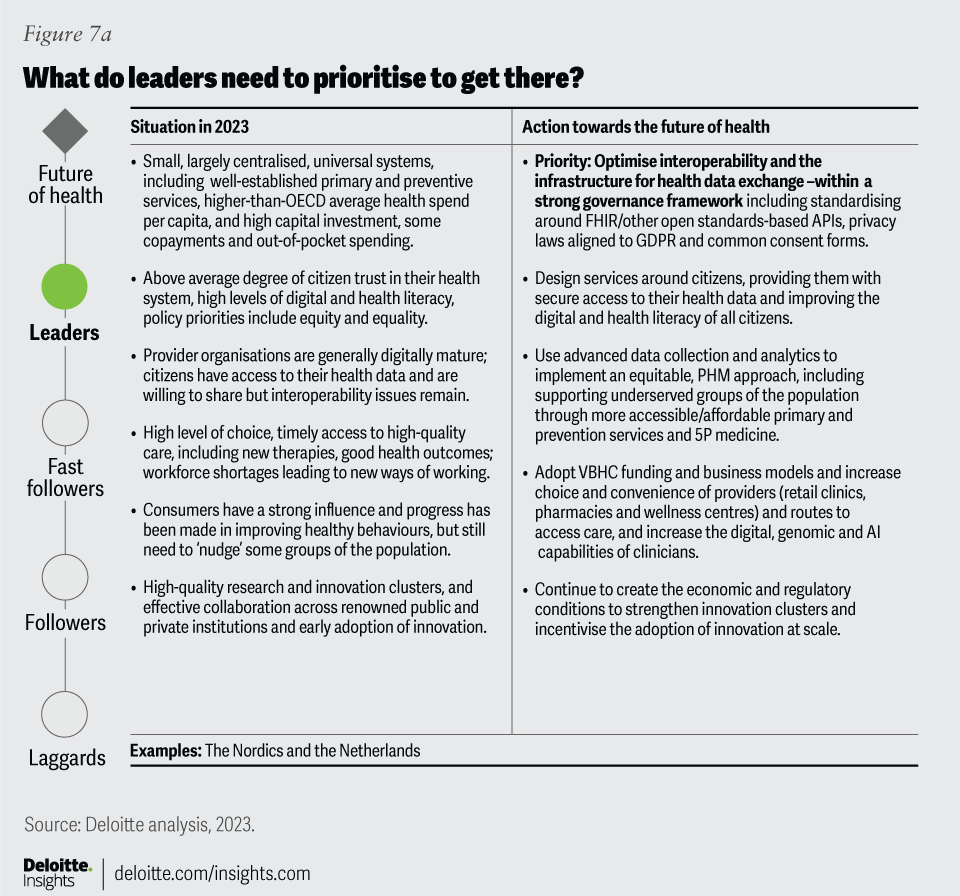

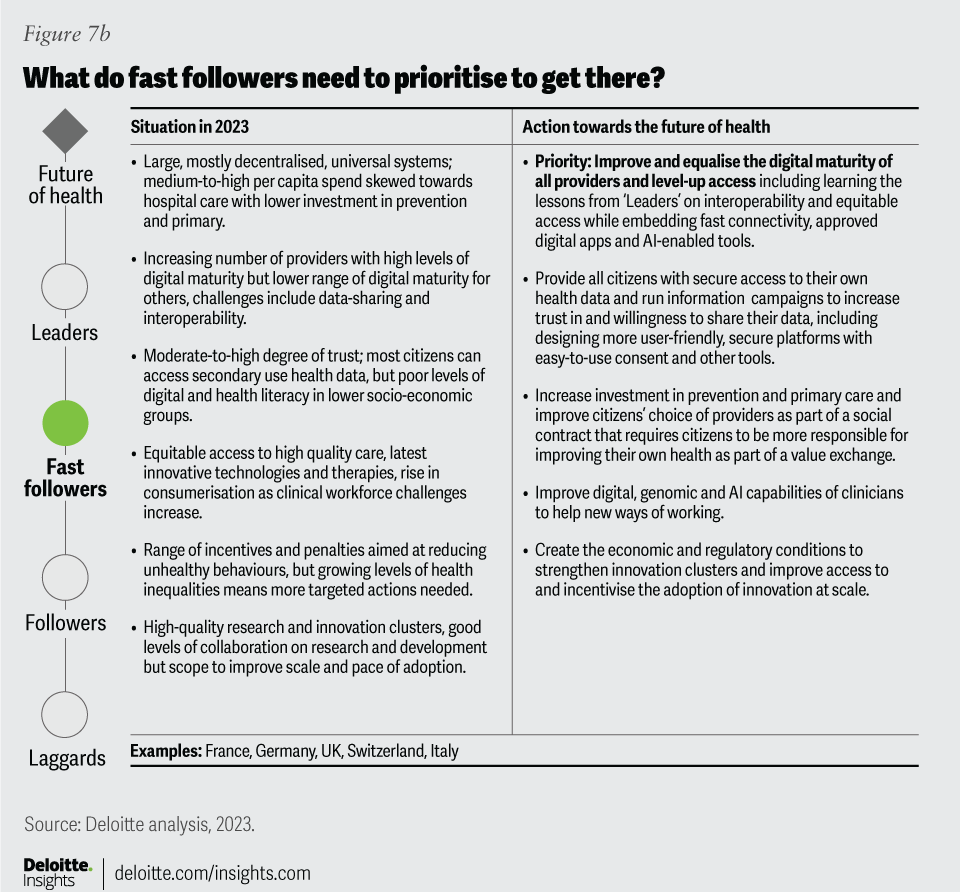

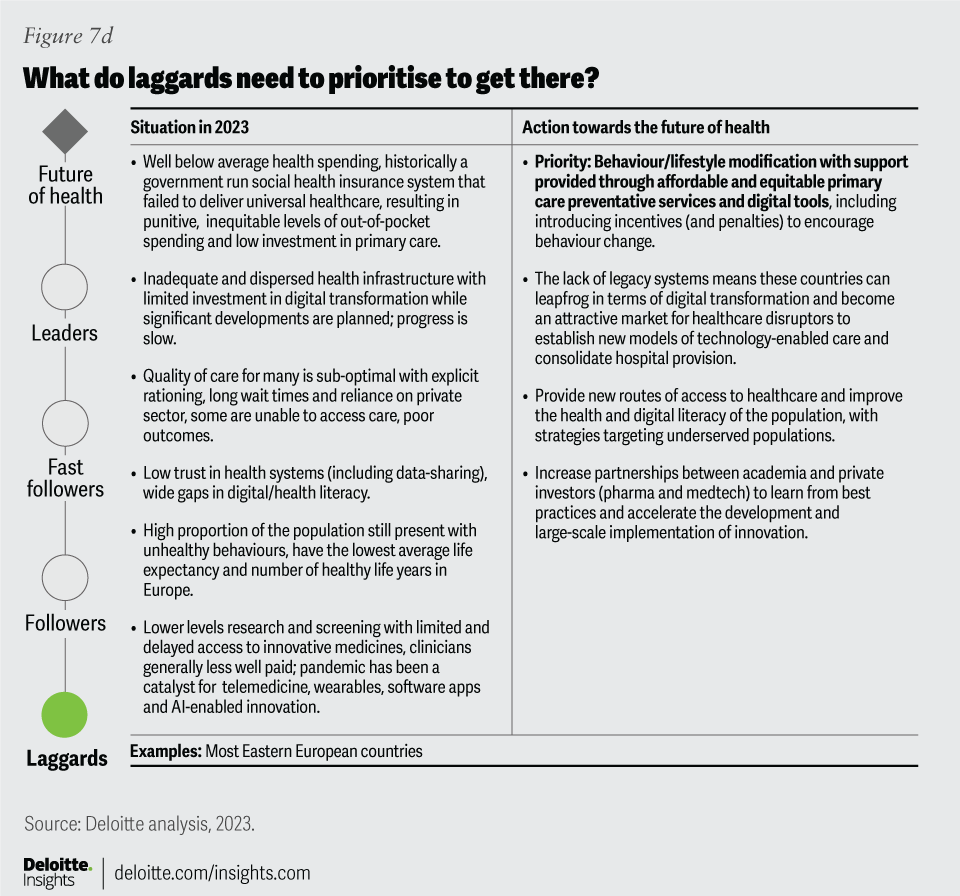

Using insights from Deloitte’s healthcare experts in our European member firms and data from the OECD, WHO and other European performance reports (see methodology), we have categorised countries into four healthcare system groups: leaders, fast followers, followers and laggards (figure 7). These categories aid in assessing each country's priorities to achieve the future of health.

European countries are at different stages in their journey towards the future of health: What do they need to prioritise to get there?

The categorisation of countries into different healthcare groups is not strictly precise due to varying research focus, data quality, and indicators used. Countries will likely shift between categories in line with the effectiveness of their transformation actions. There is no one single ‘best practice model’ in healthcare; countries excel in different aspects due to healthcare’s inherent complexity.46

Nevertheless, smaller, digitally mature healthcare systems like those in the Netherlands and the Nordics, with narrower health inequalities and better access to preventative and early diagnostic care and evidence-based public health interventions, are poised to realise the future of health vision sooner than larger, decentralised systems like those in Germany, Italy, Spain, Switzerland and the UK. Most Eastern European countries, hindered by lower funding and less-developed infrastructure, face a longer journey without significant transformation. However, this challenge presents substantial opportunity for disruptive entities to instigate radical change in these markets.

For every country, the emphasis should now be “less on inputs and more on outcomes and how countries achieve them.”47 Every country needs courageous, responsible and collaborative leadership that adopts a holistic view of the challenges ahead, engages with various health ecosystem stakeholders and fosters new alliances towards shared goals. Increased inter-system collaboration and innovation sharing can help lagging systems learn, adopt and adapt. Through this analysis, we aim to stimulate discussions that contribute to enhancing the equality, sustainability and resilience of healthcare systems across Europe.

Conclusion

The European health industry is on the cusp of a transformative shift impacting all stakeholders. Incumbents can either lead this change as innovative market leaders or resist it and lose their market share. Those that thrive will partner with disruptors and work towards a shared goal in the future of health. While disease won’t be eliminated, innovations in data, science and technology will enable earlier risk identification, proactive intervention and insightful understanding of disease progression to support individual well-being actively and effectively. The focus will switch from wellness to holistic well-being, with entities like pharmacy hubs and digital health providers assuming new roles to drive value in a revamped health ecosystem. This vision, if realised, will lead to healthier populations and more affordable and sustainable healthcare. By 2040, if our projections hold, the healthcare industry will be radically different, significantly extending the population's lives by years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}