Hospital revenue trends Outpatient, home, virtual, and other care settings are becoming more common

11 minute read

21 February 2020

Driven by consumer demands, a shift to value-based care, regulations, and advances in technology, the increased utilization of alternative care settings is contributing to the inpatient business model losing its sheen.

Executive summary

Inpatient hospital services are making up less and less of health system revenue and could soon become liabilities to a health system. Gone are the days of a one-week hospital stay after surgery, when health systems were only focusing on making money from “heads in beds.” Many patients now have procedures in ambulatory centers and go home the same day. This shift will likely continue, spurred by:

- Advances in clinical technology

- Growing pressure by payers to adopt value-based payment models that incentivize treating patients in lower-cost settings (where appropriate)

- Consumer desire to avoid hospitals

Learn more

Explore the Health care collection

Learn about Deloitte’s services

Go straight to smart. Get the Deloitte Insights app.

In our future of health vision, we expect most care to be delivered at home, or through virtual, outpatient, and other settings. The focus will increasingly shift to preventing illness—for example, through wellness and prevention strategies, remote monitoring of biological markers, and “fixing” defective genes and cells—rather than allowing a disease to occur and then treating or managing it.1 We expect these to become commonplace by 2040, but our research shows many aspects of this vision, including the shift to outpatient and home settings, are already happening today.

Having studied hospital outpatient revenue trends previously,2 the Deloitte Center for Health Solutions sought to update that analysis and dig deeper to find out what health systems are doing to influence these trends. Research included hospital financial data analysis and interviews with 20 health system executives (see sidebar, “About the research”).

Our findings are a call to action for health systems to invest in care delivery in outpatient, home, virtual, and other alternative settings. Instead of focusing on capturing more hospital inpatients, health systems should start planning for a future where buildings full of beds will likely be a memory. Organizations not yet meaningfully committed to value-based care and still focused on generating more inpatient hospital services may soon find themselves struggling.

Our analysis of hospital revenue trends found that:

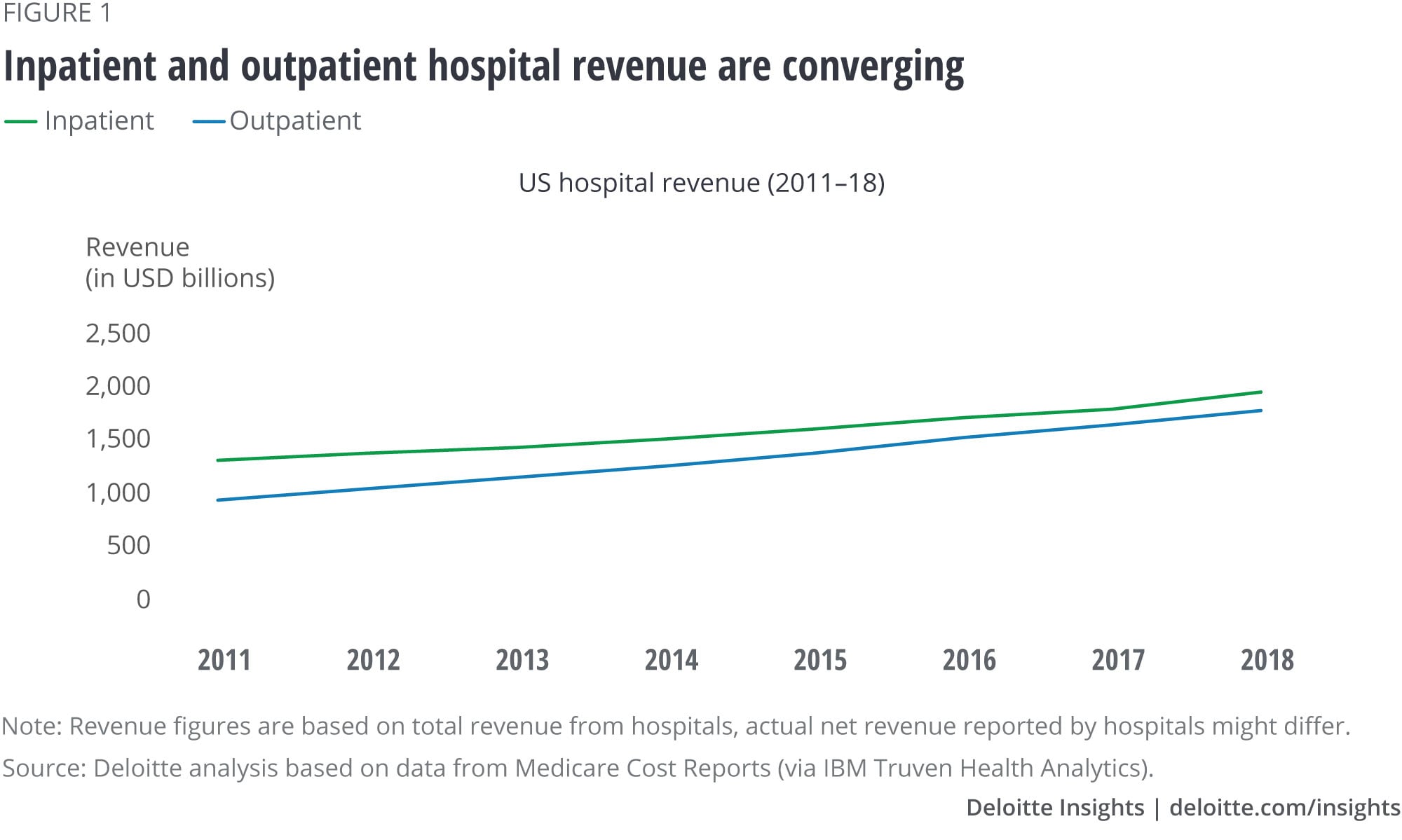

- Between 2011–18, hospital outpatient revenue grew at a higher compounded annual rate (9 percent) compared to inpatient revenue (6 percent).

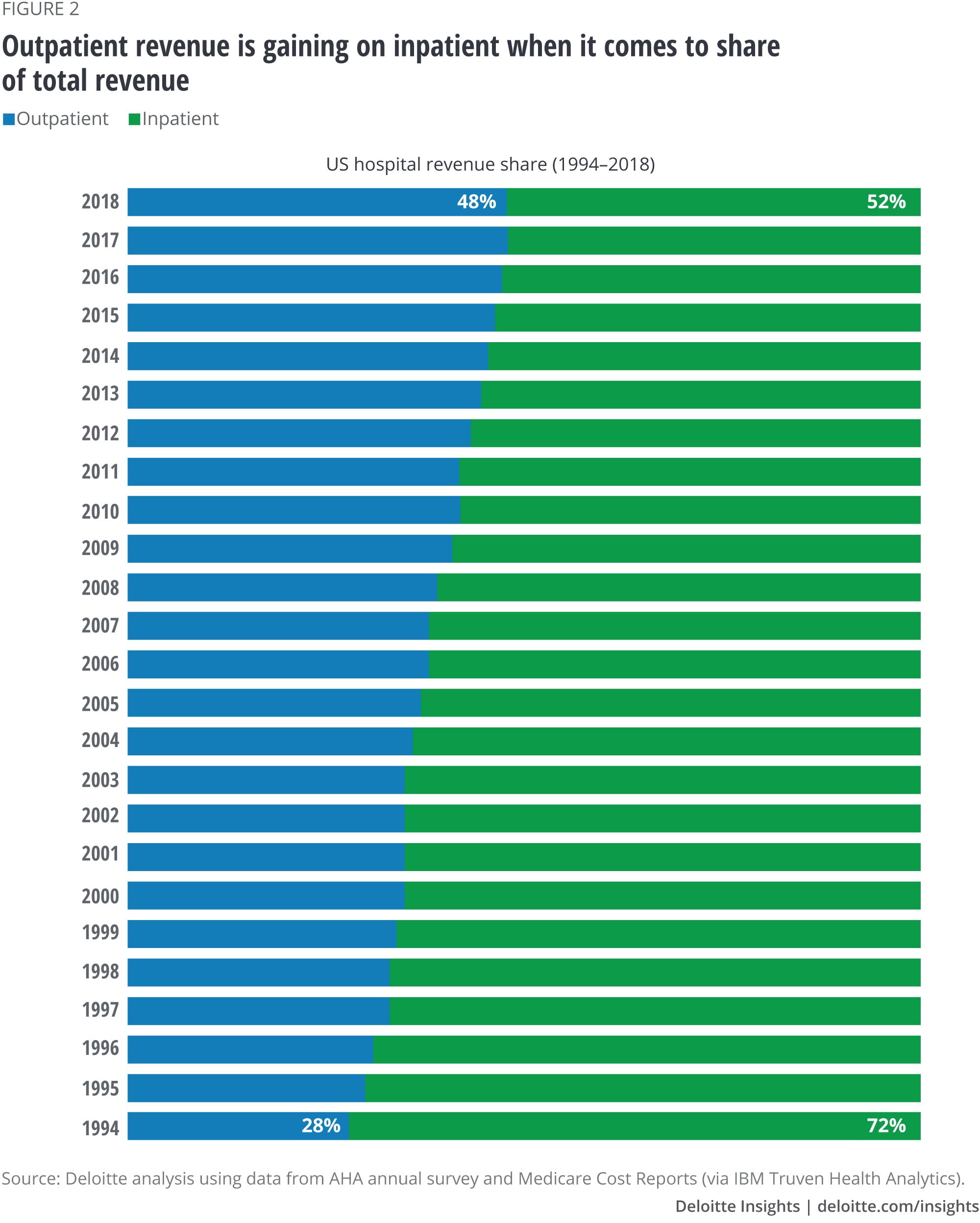

- The aggregate outpatient share of total hospital revenue grew from 28 percent in 1994 to 48 percent in 2018.

Much of this past shift is due to technological advances in clinical care delivery. Moreover, technologies like digital consumer apps, predictive analytics, and virtual health are accelerating it further today and are expected to continue to do so in the next few years. Our executive interviews revealed that some health systems are reactive (and still rely heavily on inpatient revenue), while others are intentionally growing their organizations’ capacity in outpatient and home settings. Through investments in nonhospital settings, the latter group is likely better positioned to shift away from inpatient hospital services and be prepared to deliver care in the future of health.

Interviewees recognize the need to shift away from hospital settings and are strategizing in two broad areas:

- Volume strategies: Developing ambulatory and virtual offerings to capture more patients and to better manage emergency department (ED) and inpatient volumes.

- Population health strategies: Creating virtual health services, ambulatory clinic offerings, and support resources around specific populations to better manage cost and quality. If effective, these would reduce the need for inpatient care.

Those with population health strategies are putting in place capabilities and services to help reduce unnecessary inpatient services. This is largely because of incentives in risk-bearing contracts, and their goals to improve consumer engagement and quality and reduce the total cost of care. In our prior study, we found that hospitals with greater revenue from quality and value-based contracts provided more outpatient services than other hospitals.3

Health care is shifting toward value-based care; the days of volume-based care delivery are numbered. Organizations without a meaningful commitment to value-based contracts should start making these changes today and reconsider their current capital strategies. Health systems also should steer their organizations toward outpatient, home, virtual, and other alternative settings. They can do so by considering investments in:

- Technology to support consumer engagement, virtual health, and data-sharing/interoperability

- Brick and mortar clinics and offerings that are not inpatient

- Leadership, culture, and change management with executives and clinicians to gain noninpatient expertise and get out of the hospital mindset

About the research

The Deloitte Center for Health Solutions analyzed hospital financial data of Medicare-certified institutions from the Medicare Cost Report to understand inpatient and outpatient revenue trends for 2011–18. The Medicare Cost Report includes reporting on all patient types, not just Medicare. We also conducted 20 interviews with health system executives who are leading their organizations’ efforts on this front, including population health executives, chief medical officers, chief transformation officers, presidents, strategy executives, ambulatory executives, and others. The executives represented a wide range of health systems, including academic medical centers (AMCs), integrated delivery networks, nonprofits, and for-profits.

Outpatient revenue continues to grow as a share of total hospital revenue

Over the last decade, efforts to provide access to low-cost, high-quality health care have been changing how care is being delivered. Consequently, health system reliance on revenue from inpatient care, which traditionally has been a cash cow for most organizations, is declining and will likely decline even further. Health systems have been witnessing a gradual but significant movement toward outpatient care in the last three decades. This trend is expected to only grow in the coming years. As the industry moves toward fully embracing value-based care, nonhospital settings such as outpatient, home, and virtual care may become the preferred care models for organizations and patients.

Analysis of the latest available hospital financial statement data shows that the gap between inpatient and outpatient revenue is narrowing (figure 1). Between 2011–18, hospital outpatient revenue grew at a higher compounded annual rate (9 percent) than inpatient revenue (6 percent). As a result, the aggregate share of outpatient services in total hospital revenue has grown from 28 percent in 1994 to nearly half (48 percent) in 2018 (figure 2). In recent years, hospital outpatient revenue has nearly equaled inpatient revenue and is likely to surpass it in the coming years.4

Much of this change is driven by an increase in the volume and scope of outpatient services due to technological advances in clinical procedures. According to our interviewed executives, regulations, consumer preference, and early adopters of value-based care have also played a role. Specifically, the following factors have recently contributed heavily:

- Medicare’s two-midnight rule and observation status require that certain patients who previously would have been admitted to the hospital and billed for inpatient services are now admitted to the hospital under observation status with outpatient billing.

- Consumers have an increasing preference for outpatient settings due to their greater convenience and lower out-of-pocket costs.

- Medicare, Medicaid, and commercial plans are pressuring health systems to take on value-based contracts, which aim to shift care away from inpatient settings.

- Hospitals are acquiring physician practices to support their position in the market, including their ability to deliver on value-based contracts. Physicians are reimbursed at a higher rate if they bill as hospital-based outpatient departments versus freestanding outpatient clinics.

“Shift in care settings” is more important than ever: Value-based care is coming, and hospital buildings need a new use

In Deloitte’s 2019 Health Care CEO Perspectives Study, CEOs from major health systems said the shift in care settings, proactive consumers, and quality-based payment models are the most important drivers affecting the industry in the next 10 years.5 CEOs explained that, enabled by technology, multiple drivers are increasingly pushing care to noninpatient settings. This phenomenon is affecting hospitals’ financial models—compelling them to reconsider their strategies and how they might have to repurpose their hospitals.

“All of my investment now is in outpatient—anything that is not beds. Our ability to create that network outside the hospital is huge.”—CEO of a health system

Going forward, the move from volume to value-based care will reward health systems that shift patients toward outpatient, virtual, and other lower-cost settings. In our prior study, we found that hospitals with greater revenue from quality- and value-based contracts provided more outpatient services than other hospitals.6 While the adoption of value-based care may be slow in some markets, leadership within the US Centers for Medicare and Medicaid Services (CMS) continues to strongly encourage this movement. Seema Verma, administrator for CMS, said: “Value-based payment … is the future. So, make no mistake—if your business model is focused merely on increasing volume rather than improving health outcomes, coordinating care, and cutting waste—you will not succeed under the new paradigm.”7

How is the trend taking shape? Interviewees indicate two main strategies

All the interviewed executives agreed that more care will shift out of hospitals in the future. They discussed how certain orthopedic and cardiac procedures and populations, among others, do not belong in the inpatient setting, and recognized that hospitals should shift these to alternative settings. The reliance on inpatient services, and the shift away from it, varied among the organizations we spoke with. The interviewees reported that their share of revenue from inpatient services versus other sources ranged from 35 to 75 percent. While many said the inpatient revenue share for their organization should (and will) decline, some thought it would be stable if they get paid more for complex patients who will continue to need treatment in inpatient settings.

For those intentionally growing their organizations’ capacity in outpatient and home settings, we found that their strategies fall under two broad categories:

- Volume strategies: Many are bullish on brick-and-mortar clinics and are investing in urgent care centers, ambulatory surgery centers, imaging centers, and primary care clinics. They want to broaden access for their consumers. The goal of these efforts is to capture a broader volume of the population in the marketplace to feed their hospital services. Most of these investments also aim to help better manage hospital capacity and prevent unnecessary ED visits and inpatient admits. Many have been successful thus far at growing volumes and retaining high-paying services in their health system.

- Population health strategies: Health systems bearing significant financial risk or having a Provider Sponsored Plan (PSP) are “seeing the light,” and are attempting to transform their business models to rely less on inpatient revenue. They are investing in remote monitoring and other forms of virtual health, building or buying clinics, and hiring care coordination and other related staff to better coordinate care, treat patients in the lowest cost settings, and improve quality. Their leadership focus has been on the overall bottom line of the entire organization, not just the hospital.

Many have found financial success with value-based care and feel that they are positioned well for broader adoption. For example, some are developing disease management programs that involve a combination of monitoring, access to clinics, and oversight while at home by a care team. Others have proclaimed that they will treat more of their population using fewer beds and have taken a population health approach for managing their noninpatient businesses. They have used a variety of partnerships/joint ventures (JV), collaborations, and greenfield approaches to enter the market with physicians, retail pharmacies, and others in the community.

“The focus of the past 10 years has been on preventing readmissions, and now in the next 10 years, the focus will be on preventing admissions.”—President of a health system

“Our mission is to provide health care to the community. If we can deliver care to the community in a better-quality manner that is less capital intensive, then that is better for our fiduciary commitment to the community.”—Population health executive of a health system

Technology is helping to steer care away from the hospital

Interviewees recognize that technology is moving beyond being a mere enabler to playing a much bigger role in driving care into outpatient settings. The following are some of the ways in which technology can be used to shift care toward outpatient, home, virtual, and other alternative settings, which the interviewees stated as being critical investments for value-based care:

- Clinical technological advances: All interviewees talked about how certain orthopedic, some cardiac, and other procedures are now taking place in outpatient settings due to clinical advances. Monitoring capabilities and regulations are also forcing many to reconsider what treatments can and should be done in the hospital. They expect this trend to continue—many are investing to further advance their clinical capabilities in outpatient settings.

- Data-sharing and platforms, interoperability, and analytics: The interviewed executives viewed data and access to it as critical areas of focus to support better decisions (business and clinical). They recognized the need for data to flow across all their new noninpatient entities, help with virtual connections, and ensure care coordination and quality. Some viewed these as important capabilities to better manage populations while others want them to help prevent ED visits and inpatient admits.

- Virtual health: All executives agreed that virtual health is another key area of investment to shift patients away from inpatient settings. They see the value of virtual services in terms of better access, meeting consumer demand, managing populations better, and preventing ED visits and inpatient admits. Nearly all interviewed executives are investing in some form of virtual health offerings. Most are focused on physician-to-physician consults, virtual specialty access in certain markets, and, to a lesser extent, direct-to-consumer virtual visits.

- Consumer engagement and digital platforms: All the interviewed executives agreed that creating a better consumer experience through digital technologies could help them better engage consumers and build better relationships. The types of technologies they are investing in include online scheduling, technology that helps with wayfinding, direct communication with physicians, appointment reminders, and more. These offerings can be accessed online, through EHRs, by phone, in kiosks at clinics, and elsewhere. All aim to better engage consumers and prevent unnecessary inpatient care.

“We are trying to take care of more people using less money. To the extent technology can allow us to deliver care in less expensive physical spaces, it gives us scale without having to make traditional capital investments.”—Chief transformation and experience officer at a health system

What will it take? Advice from executives at leading organizations

While acknowledging that steering their organizations away from the traditional hospital-revenue-generation mindset is challenging, interviewees agreed that health systems should focus (strategically and financially) away from inpatient hospital services and instead begin investing in outpatient, home, virtual, and alternative settings. They advise their colleagues, who are trying to accelerate the shift to develop the following capabilities and attributes, to better support those investments:

- Leadership that is thoughtful, courageous, and brave: Leaders should be willing to cannibalize hospital revenue and focus on the organization’s overall bottom line instead of individual service line profit and loss (P&Ls). Steering a large ship that has been on its course for decades takes a lot of work.

- Expertise on how to run noninpatient businesses: Many recognize that running a hospital does not always translate to other health care businesses. Some organizations hired executives with ambulatory and population health expertise.

- Investment in technology, particularly data-sharing, interoperability, and analytics: Data from all care settings and the ability to analyze it, could support better decision-making and can enable health systems to steer patients toward the most appropriate (and lower-cost) care setting.

- Partnership and collaboration: Organizations recognized that they cannot do it alone because they lack the needed offerings outside the hospital. Many discussed close relationships and collaboration with a broad spectrum of industry stakeholders—retail pharmacies, payers/employers, technology companies, community service providers, and more.

- Being both consumer- and physician-centric: Nearly all interviewees discussed physician collaboration and involvement and having the consumer at the center of their efforts. Physicians are critical stakeholders who should be engaged in decisions. All decisions should consider the consumer experience.

“We need to give ourselves license to take the bolder steps to increase affordability and convenience.”—Senior vice president and chief strategy officer at a health system

Health systems need to act

The shift toward outpatient is happening and will likely have a tremendous impact on operations, business models, staffing, and capital. Health systems should prepare for the future today and start thinking not only about how to manage their traditional business model but also how to invest in and create new competing business models at the same time. Organizations that do not prepare for a future, driven by value-based contracts, are likely to struggle. With multiple drivers shifting care toward outpatient and other alternative care settings, decision-makers could do better to turn their focus away from inpatient settings.

Deloitte Health Care

Innovation starts with insight and seeing challenges in a new way. Amid unprecedented uncertainty and change across the health care industry, stakeholders are looking for new ways to transform the journey of care. Our US Health Care practice helps clients transform uncertainty into possibility and rapid change into lasting progress. Comprehensive audit, advisory, consulting, and tax capabilities can deliver value at every step, from insight to strategy to action. Our people know how to anticipate, collaborate, innovate, and create opportunity from even the unforeseen obstacle.

Learn more

Get in touch

- Steve Burrill

- Vice chairman, US Health Care leader

- Deloitte & Touche LLP

- +1 713 982 2821

- sburrill@deloitte.com

Related content

Learn more about technology in health care

-

Health care Collection

Health care Collection -

Digital health technology Article4 years ago

Digital health technology Article4 years ago -

Virtual health care Video

Virtual health care Video -

Predictive analytics in health care Article4 years ago

Predictive analytics in health care Article4 years ago -

Showing cybersecurity's value to health care leadership Article5 years ago

Showing cybersecurity's value to health care leadership Article5 years ago -

Creating a treasure trove of data for health plans Article5 years ago

Creating a treasure trove of data for health plans Article5 years ago