An introduction to Deloitte’s 2024 Digital Media Trends

As streaming, social, and gaming converge, companies should consider comprehensive strategies to define media and entertainment's future—or they could risk living in someone else’s vision.

Jana Arbanas

Kevin Westcott

Jeff Loucks

Chris Arkenberg

Brooke Auxier

Bree Matheson

This year’s Digital Media Trends report points to continued disruption for media and entertainment—not just from streaming, social, and gaming, but also from the ways these media and their technologies are weaving together and enabling new combinations. From so much change and disruption, however, the new landscape is becoming clear—and it may demand that providers move beyond their core businesses. To drive discovery, engagement, and monetization of their intellectual property and services, media, and entertainment (M&E) companies may need holistic strategies that operate across TV and film, social media and user-generated content, and interactive and immersive gaming.

In 2024, our study shows that the map of M&E appears exponentially larger than it did just a decade ago, and the lands are no longer divided by clear borders. Consumer expectations of media and entertainment may now be shaped more by social media, content creators, and video games than by TV and films. How people weigh the value of entertainment options appears to be changing shape as well.

Our survey data shows that US consumers are questioning the value of streaming media while also declaring their unwillingness to ever pay for social media. Just as streaming video providers are rebuilding the ad models that buoyed pay TV, fewer people surveyed are moved by commercial advertising and, instead, seek recommendations from trusted creators and influencers to help them navigate and find value. More are turning to online multiplayer video games for virtual friendship, content discovery, and brand and franchise interactions.

Although technology has enabled much of the change we see, it’s the needs, behaviors, and expectations of younger generations that are demanding the change. Millennials and Gen Zs (and the Alphas that follow them) show both how diverse America has become, and how people increasingly live and socialize beyond physical geography, tugging at an early metaverse. Together, those Americans 41 years and younger represent more than half the population of the United States.1 They’re the collective faces of a growing diversity in ethnicity, race, gender identity, sexual orientation, and neurodiversity. Our study shows how people expect media and entertainment to reflect this reality, and how some key demographics—like women gamers—remain underserved and underutilized by providers.

Despite so much change and disruption, M&E companies can leverage tools and talent to their advantage. Social media creators and influencers can be tour guides and tastemakers, facilitating discovery, hype, and trust. Fans and fan communities can offer stalwart companionship to artists, personalities, stories, and franchises, helping to make it easier for studios and providers to expand their intellectual property and cross into new media. Many people spend idle time in a handful of social media services that have aggregated billions of users. On social media, people discover new and old content, gather recommendations for what to watch and listen to and buy, and get caught in the updrafts of hype and virality. For all M&E providers, social media should be a primary destination to reach and engage audiences. It should be considered instrumental to customer acquisition and retention.

Technologies are there to help, ready to do more heavy lifting than ever. Data, algorithms, and artificial intelligence can help enable providers and creators to develop more compelling content and experiences and match them to the best audiences, fans, and tastemakers. Our study shows that US consumers want the kinds of personalization and customization of content experiences that they have come to expect from social media services. When they discover content and products, whether on streaming, social, or games, they want to be able to easily and immediately make purchases and add to libraries. And more want to follow their favorite stories across TV shows, movies, and video games.

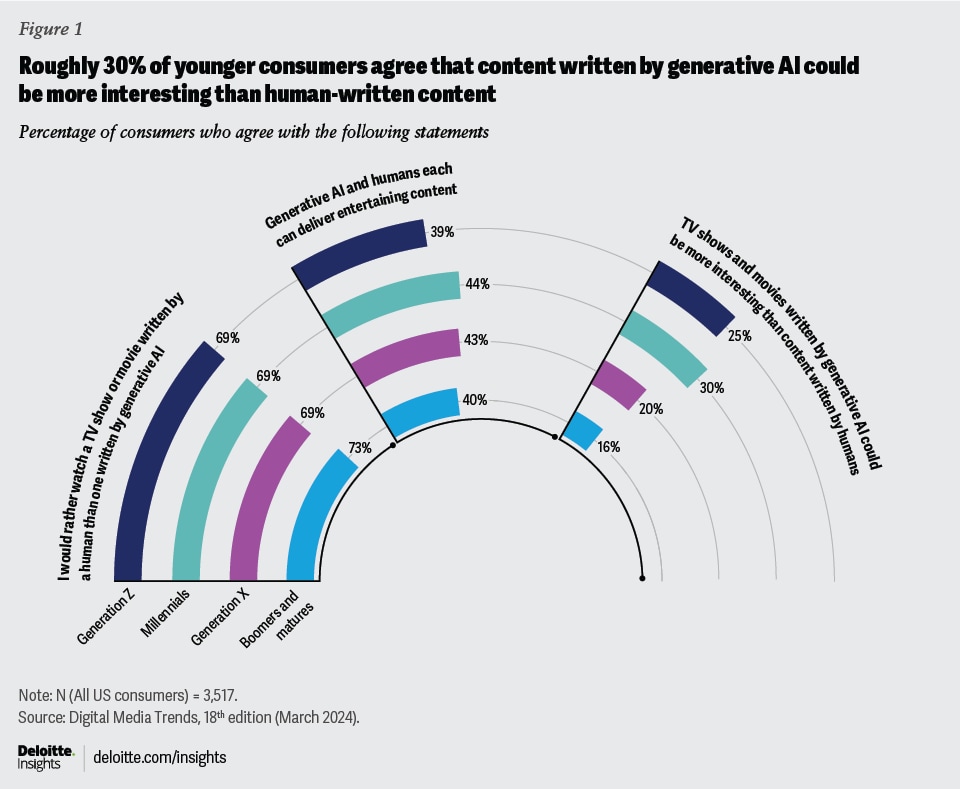

Generative AI could drive additional change on all these fronts, while potentially unlocking entirely new tools and experiences. It’s already empowering content creators and disrupting industry standards.2 Although 70% of our respondents say they would rather watch a TV show or movie written by a human than one written by generative AI, 42% feel that generative AI and humans can each deliver entertaining content. And 22% feel that generative AI could even write TV shows and movies that are more interesting than humans. Gen Zs and millennials are leading the way in experimenting with these tools: Eighteen percent of these generations have used generative AI to create images, and 25% surveyed have used it to create text. Older generations are further behind on these counts.

Although the size of the metaverse is difficult to realize and the technology of blockchain has been difficult to scale, generative AI appears to be expanding quickly. Savvy creators and studios should consider experimenting with how these tools can augment human creativity and enable teams to be more productive. Generative AI could make it easier for companies and creators to improve the quality of content creation but it could also lead to a flood of cheap and novel content that further dissolves the boundaries between “real” and synthetic, commodity and premium. Empowered by generative AI, media and entertainment companies—and society at large—may be about to confront a much larger volume of novelty, content, and creative output.

Amid the disruption that has characterized the first quarter of the 21st century, there appears to be growing demand from audiences, subscribers, and gamers for more focused and intentional change to older business models. It’s unclear if investors agree with catching up or would rather continue “squeezing the lemon” for the last drops of revenue from 20th century business models. Nevertheless, the assumptions and strategic bets based on an evolution of earlier business models are running into the reality of a much broader and deeper revolution in digital media. Companies leveraging traditional business models within their own historic definitions may face insurmountable challenges in the new environment of connected and interdependent digital media. They should be thinking more about the world ahead than the one they’re being forced to leave behind.

In this year’s Digital Media Trends, we dig deeper into the details of how people use and value digital media, offering M&E companies more data and insights to gain a deeper understanding of consumers and how their interests, attitudes, and identities have changed. With this understanding, media and entertainment companies will likely be better positioned to build profitable businesses and operate with confidence in a landscape that keeps shifting.

Study highlights:

- Streaming video services still suffer from high costs, high churn, and competition from many quarters. Streaming providers are now rebuilding the business models that buoyed pay TV: advertising, bundles, and contracts. But can these models work well enough in the modern media landscape that seems to give less attention to advertising and more to creators, influencers, and communities?

- In the United States, around 60% of our respondents identify as gamers, almost equally between men and women. Yet, women gamers continue to face challenges with harassment, bullying, and stereotypes in games and game communities. At a time when more live service games and multiplayer experiences are driving investments (and costs), many women prefer solo mobile games and story-driven adventures. For gaming to continue growing, the gaming industry should consider ways to serve women gamers better.

- Online creators and influencers are media stars, tastemakers, and tour guides, directing their fans to products, brands, experiences, and media content. Traditional media companies may need to develop symbiosis with creators and platforms, while acknowledging the tension inherent in competition for viewers and ad dollars.

- For many people, being a fan is core to their identity. Whether it’s video games, TV and movie franchises, musical acts, or sports teams, fans are willing to spend and follow their favorites across entertainment platforms. Identifying fan-worthy franchises early on, fostering fandom, and providing more ways for customers to engage (and spend) could be essential for M&E companies looking for more revenue and loyalty.

- Generation Z and millennials (and Generation Alpha that follow them) are the most diverse generations in American history—in terms of ethnicity, race, gender identity, sexual orientation, and neurodiversity. They want media and entertainment that reflects the world they see, and the lives they live.

Methodology

These insights are based on an online survey of 3,517 US consumers that was conducted in October 2023. Throughout this report, we reference generations. Our generational definitions are as follows: Generation Z (1997-2009), millennial (1983-1996), Generation X (1966-1982), boomers (1947-1965), and matures (1946 and prior). The survey was fielded by an independent research firm and all data is weighted back to the most recent Census to give a representative view of US consumers.

{kind=link}