COVID-19. Coronavirus. SARS-CoV-2. Pandemic. Sanitary or humanitarian crisis. Regardless of the wording used, regardless of our language, culture, region or social status, we are currently going through a historical period whose consequences will undoubtedly survive the virus. Driven by a pandemic context, changes in habits, perceptions and priorities will redefine the status quo. Just look at the past. Justinian's plague (6th to 8th century) contributed to the end of antiquity, while the Black Death (14th century) brought about the end of serfdom in Europe, the mainstay of the feudal system. Closer to home, major changes redefined agriculture and medicine in New France in response to scurvy epidemics. To break that pandemic, it was necessary to drastically change the settlers’ habits and integrate the knowledge of the First Nations.

While our daily life and social order are profoundly reshaping, Deloitte’s economic practice presents a series on the socio-economic transition that is currently taking place in Quebec. This series, which will be presented in four parts, the first issue of which (Diagnose) presents the current socio-economic situation in Quebec and will serve as a foundation for the idea that an economic crisis is divided into three phases (Respond-Recover-Thrive).

Diagnostic of the socio-economic transition in quebec

Summarized in Deloitte’s Dashboard, the economic data surrounding this self-inflicted recession takes us into uncharted territory. With Quebec losing $100 billion[1] in wealth, including rising public debt and declining GDP, and a provincial unemployment rate of 17%—compared to 13% for Canada as a whole[2] — Quebecers are wondering whether we will see a rapid recovery or whether we will instead see an economic downturn that is struggling to recover or a recovery that is stalled, for example, by a second wave of the pandemic. Figure 1 below shows the extent of job loss in Quebec compared to the rest of Canada. Quebec has experienced more job losses than the rest of Canada and, in particular, in the goods-producing sector where Quebec has lost 26% of jobs compared to only 15% nationally.

Figure 1: COVID-19 job losses by industry and province (%) understanding prior to reopening

In the short term, the reopening:

The government will need to weigh the sector’s economic contribution, which includes its contribution to GDP, the number of jobs and the maintenance of essential services, against the risks posed by its recovery (Figure 2). In order to better understand the dynamics of reopening, all sectors should be categorized under three broad groups.

- Presently open: In order for society to function, even in times of pandemic as is currently the case, certain sectors considered essential must be open. These sectors include healthcare, public transit, information and communication, agriculture and food trade, as well as public administration and national defence.

- Imminent reopening: These sectors are those for which public authorities consider the risk of transmission to be lower than their economic contribution. For Quebec specifically, these are the sectors included in the April 28 reopening announcement: manufacturing, retail, and construction (residential and commercial).

- Unknown reopening: These sectors are those for which the public authorities consider the transmission risk to be greater than their economic contribution. For these industries, such as tourism, culture and the arts, aviation, or any other industries that require greater proximity, governments, regulators and businesses themselves will need to put rules in place before giving the signal to reopen.

Figure 2: Transmission risk vs economic contribution by sector

In the medium and long term, targeted intervention:

According to a McKinsey study[1], the survival of many businesses will link the capacity to adapt to the need to adapt. This is consistent with the Canadian outlook for the future that Deloitte has prepared for various sectors.

This analysis is anchored around the social distancing raised by COVID-19. Adaptive capacity refers to the ease with which industries are able to continue to operate without fundamental transformation while respecting social distancing. For example, adaptive capacity is stronger for companies that can operate remotely than those that require greater proximity. The need to adapt refers to the need to transform business practices because of proximity. Thus, as business proximity increases, so does the risk to health and the need to transform activities.

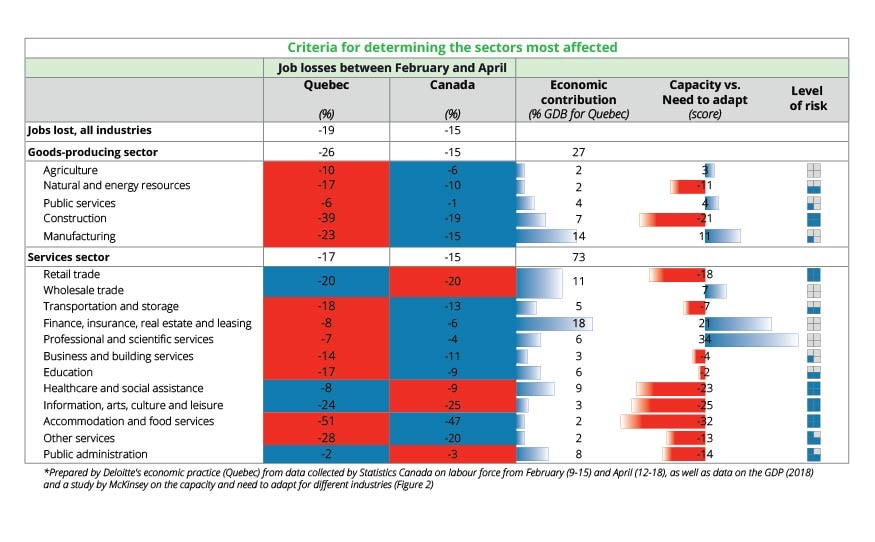

In short, it is the proximity industries (retail, tourism, aviation, food services, hotels, entertainment, etc.) that have been the most affected to date and that, given their difficulty in adapting to distance standards, show indications of prolonged disruption. Certain parts of these industries are considered to be essential. To bring this analysis back to the Quebec market, we look at the economic weight (contribution to the gross domestic product) in each of these sectors. Considering job losses between February and April (in %), the economic contribution and difference between the capacity and the need to adapting, we have three criteria that, when combined, show the most at-risk industries in Quebec’s economy. Figure 3 below measures these three criteria for each industry and presents the three sectors that will require government intervention.

Figure 3 – Criteria for identifying the sectors most affected

it should also be remembered that this analysis in silos, or in other words by industry, has certain limitations in terms of systemic and regional impacts as well as in terms of the relationships between the industries themselves. First is the collapse of certain industries (i.e., aerospace), which could have multiple repercussions for many other sectors, some even presenting potential opportunities, namely the mobility of the workforce between the affected industries. Next, the economic contribution of these industries is at the provincial level, while for certain regions, the level could be high or low. For example, the mining industry is far away from the metropolitan area, but is very significant in Northern Quebec. These industries will require greater collaboration with the various levels of government and it will be necessary to mitigate the impacts in the short, medium and long term. In the next part of this series, we will be analyzing government involvement.

Contact us

Nathalie Sinclair-Desgagné

Senior Manager, Economic Advisory

nsinclairdesgagne@deloitte.ca

514-369-9520

[1] CIRANO. 2020. La valeur d’une vie : COVID-19 contre la SAAQ. Excerpt from: https://cirano.qc.ca/files/publications/2020PE-13.pdf

[2] Statistics Canada. April 2020. Labour Force Survey. Excerpt from: https://www150.statcan.gc.ca/n1/daily-quotidien/200508/dq200508a-eng.htm

[3] Tera Allas, Pal Erik Sjatil, Sebastian Stern & Eckart Windhagen. April 29, 2020. How European businesses can position themselves for recovery. Excerpt from: https://www.mckinsey.com/industries/public-sector/our-insights/how-european-businesses-can-position-themselves-for-recovery