News

Global luxury goods sector remains resilient, Swiss players lead the way

Richemont, Swatch Group and Rolex in the Global Top 10 of new Deloitte report

ZURICH, 15 May 2014 - The world’s 75 largest luxury goods companies generated sales of $171.8 billion through the end of last fiscal year1, despite a slowdown in the global economy. The average size of the Top 75 companies was $2.3 billion in luxury goods sales. With three Swiss companies in the Top 10 – Richemont, Swatch Group and Rolex – and a total of six in the ranking, Switzerland emphasises its leading role in the luxury goods industry. This is according to the first Global Powers of Luxury Goods report issued by Deloitte.

Luxury goods conglomerates and mono-brand companies are primarily among the Top 10 worldwide and impress with strong performances:

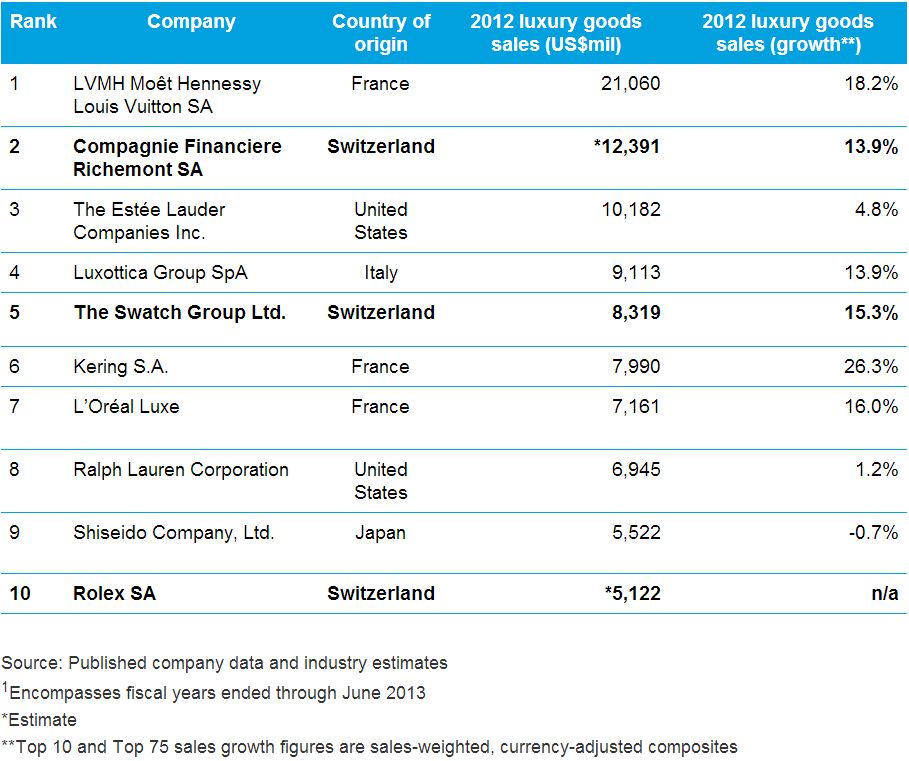

Top 10 luxury goods companies worldwide

Six Swiss companies in the Top 75

Switzerland outperformed the Top 75 on both the top and bottom line. Of the six Swiss companies, three had luxury goods sales in excess of $5 billion and are represented among the Top 10: Richemont (2), the Swatch Group (5) and Rolex (10). Richemont and Swatch accounted for a combined 74.9 percent of Switzerland’s Top 75 luxury goods sales. Other Swiss companies in the worldwide ranking are Patek Philippe (35), Audemars Piguet & Cie (47) and Breitling (58). The six companies held a significant 16.1 percent share of the total Top 75 luxury good sales in 2012 and were also the largest, with an average size of $4,608 million. This is more than double of the Top 75 average size ($2,290 million).

Karine Szegedi, Partner Consumer Business for Deloitte in Switzerland, commented on the strong results of Swiss companies in the global ranking: “The watch industry is the leading luxury market in Switzerland for good reason: Customers from all over the world highly rely on the top quality, service and heritage of those companies.”

Europe – the centre of luxury

The report shows the high concentration of luxury goods companies headquartered in France, Italy, Spain, Switzerland, the United Kingdom and the United States. These six countries represented nearly 87 percent of the Top 75 luxury goods companies and accounted for more than 90 percent of global luxury goods sales in 2012.

“France, Italy and Switzerland achieved strong composite luxury sales growth in 2012, with France and Switzerland outpacing the 12.6 percent composite growth for the Top 75 at 19.4 percent and 14.8 percent”, said Karine Szegedi. “The Eurozone includes four of the Top 10 luxury markets in the world: Italy (3), France (4), Germany (7) and Spain (9)”, stated Szegedi, underlining the role of Europe as the centre of the luxury goods industry.

Growth to pick up speed

“Despite operating in a troubled economic environment, luxury goods companies fared better than consumer product companies and global economies generally. For the remainder of this year, we expect growth in developed economies to pick up speed while significant risks in emerging markets remain,” said Karine Szegedi. “The overall performance of the luxury sector will depend not only on economic growth, but on factors such as volume of travel, protection of intellectual property, consumer propensity to save, and changing income distribution. We are therefore set to see a growing number of luxury goods conglomerates seek to boost growth and market share through consolidation in the second half of 2014.”

Key drivers of M&A activity in the luxury goods sector

Compared with the rest of the consumer products industry, luxury goods have been relatively insulated from recent economic distress. Accordingly, the luxury sector has outperformed the consumer goods M&A market as a whole. Three main trends are driving deal making in the luxury and premium goods sector:

Globalisation

Growth of wealthy and upper middle class consumers in emerging markets has been the biggest driver of M&A activity in recent years. Asia Pacific, Latin America, the Middle East and Africa accounted for a combined 19 percent of the luxury market in 2013. “The appetite for European and American brands remains strong in emerging markets, so these companies are bolstering their presence in those regions”, said Howard da Silva, Consumer Business Industry Leader for Deloitte in Switzerland.

Value chain integration

Luxury goods companies also keep tight control over all aspects of business from product design and sourcing of raw materials to manufacturing, marketing and distribution. Ownership of all aspects of the value chain helps ensure that quality and service can be maintained, thus protecting brand heritage. As a result, vertical integration has become another important driver of M&A activity in the luxury goods sector.

Consolidation as a growth strategy

Industry consolidation is another factor driving M&A activity. The large luxury conglomerates operate in diverse subsectors, the common denominator being a broad expertise in luxury including an intimate understanding of the luxury consumer. Seasoned investment firms are also contributing to the greater consolidation of luxury brands into a smaller number of holding companies. All of these consolidators are seeking scalable brands, including distressed or underperforming businesses that simply do not have the experience, knowledge, or resources to manage ever-expanding operations.

About the Global Powers of Luxury Goods report

The report identifies the largest luxury goods companies around the world. It also provides an outlook for the leading luxury goods economies, insights for mergers and acquisitions (M&A) activity in the sector, and discusses the major trends affecting the industry including the retail and ecommerce operations of the largest 75 luxury goods companies. The 1st annual Global Powers of Luxury Goods report is focused on four broad categories of luxury goods: designer apparel (ready-to-wear), handbags and accessories, fine jewellery and watches as well as cosmetics and fragrances. The report excludes the luxury categories of autos, travel and leisure services, boating and yachts, fine art and collectables, and fine wines and spirits.

To download a copy of the full report, please click here.

About Deloitte in Switzerland

Deloitte is a leading accounting and consulting company in Switzerland and provides industry-specific services in the areas of audit, tax, consulting and corporate finance. With approximately 1,100 employees at six locations in Basel, Berne, Geneva, Lausanne, Lugano and Zurich (headquarters), Deloitte serves companies and institutions of all legal forms and sizes in all industry sectors. Deloitte AG is a subsidiary of Deloitte LLP, the UK member firm of Deloitte Touche Tohmatsu Limited (DTTL). DTTL member firms comprise of approximately 200,000 employees in more than 150 countries around the world.