Press releases

Swiss watchmakers bank on digitalisation to unlock new opportunities

Zurich, 27 September 2017

According to the Deloitte Swiss Watch Industry Study 2017, digital is at the heart of the Swiss watchmakers’ business strategies. Optimism is back; more than half of watch executives surveyed are optimistic about the future of the Swiss watch industry for the next 12 months, compared to only 2% last year. The market remains challenging, but the industry is tackling its transformation with Digital, Swiss made legislation, the introduction of new products and Smartwatches as ingredients of the change.

Swiss watchmakers bank on digitalisation to unlock new opportunities

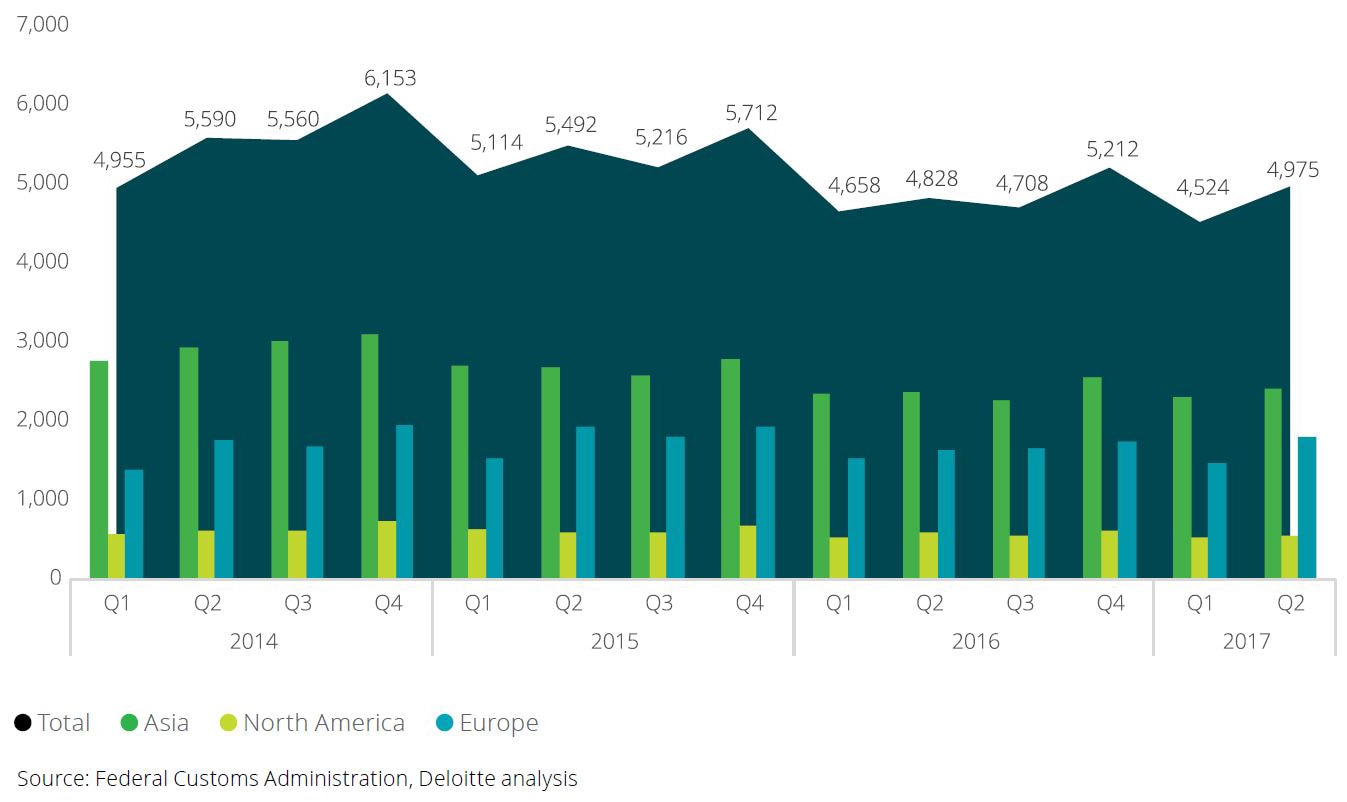

The Swiss watch industry shows first signs of recovery with a rise of watch exports in Q2 2017 to CHF 5.0 billion from CHF 4.8 billion in 2016 after 20 consecutive months of negative growth rates. Yet, this growth is relative and primarily reflects a recovery of mechanical watches while quartz watches continued to decline. Overall, volumes of wristwatches were still down.

A return to optimism

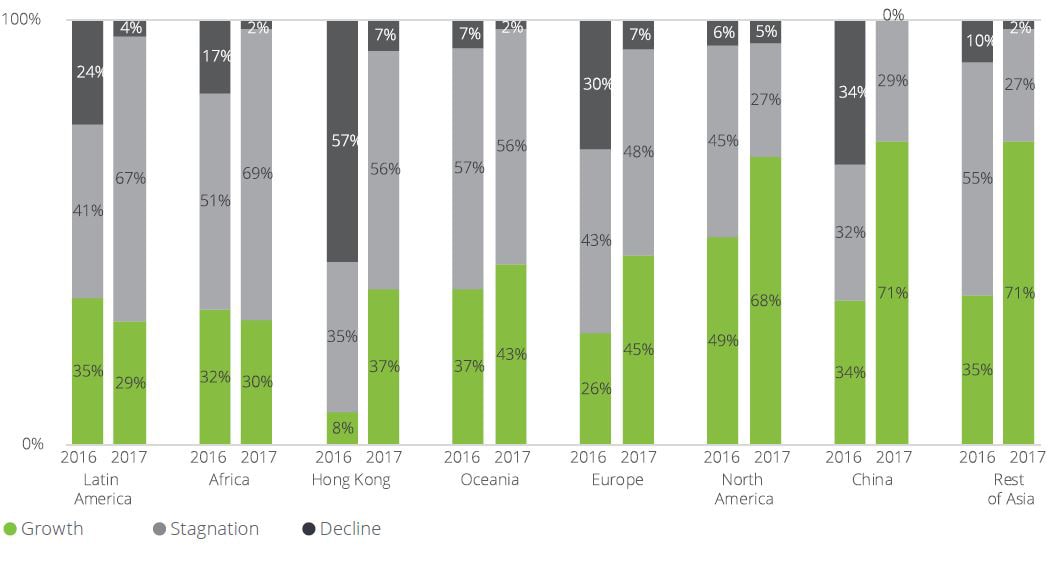

The growing optimism about the outlook for the Swiss watch industry is second highest since the first Deloitte Swiss Watch Industry Study was published in 2012, peaking at 52 % (compared to only 2% in 2016). While 61% of watch executives consider the outlook for the main export markets of the Swiss watch industry, such as China, Hong Kong and the US, to be positive in the next 12 months.

Karine Szegedi, Partner and Head of Fashion & Luxury for Deloitte in Switzerland, says: “2016 was one of the toughest years Swiss watchmakers had to face since the global financial crisis, with lower exports figures than expected, caused by a declining demand in particular in Asia and the United States, the industry’s most important export markets for Swiss watches.”, she adds, “Today, we see promising signs that the industry’s unique positioning in the luxury segment, its innovation capacity and the strong brand image of its key players shall allow them to adapt to the new market conditions.”

With double-digit growth rates in the last quarters, China recorded the strongest recovery in watch exports followed by Europe (9% in Q2 2017 compared to Q2 2016). After a sharp downward trend, Hong Kong finally showed signs of stabilisation with a slight increase in Q2 2017 (+1%). This upbeat is not surprising given the higher expectations for growth in almost all regions, especially in Asia. When asked about their growth expectations 71% watch executives see a positive outlook for China and the rest of Asia. A large majority of respondents (68%) still consider that the US market could grow in the next 12 months, making it the third most promising watch market.

“Reasons that has boosted consumption of luxury goods including high-end watches is the drop in China’s corruption prosecutions and the rise in import taxes and increased controls at Chinese customs. “, comments Karine Szegedi and adds, “Whereas watch executives’ expectations have also improved in relation to sales to foreign tourists in Europe and Switzerland, an important additional export channel for Swiss watch companies that is estimated to make up 5% of total watch exports.”

External risk factors remain strong

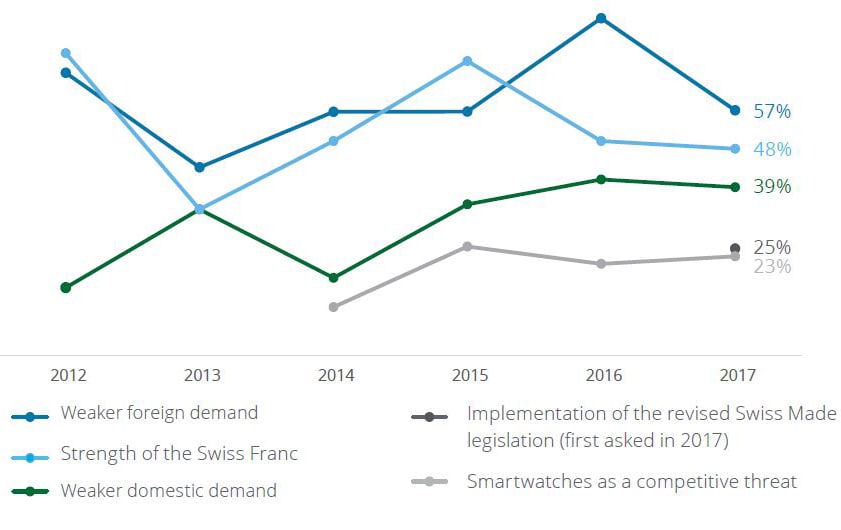

With the implementation of the new Swiss Made rules in early 2017, requiring at least 60% of a watch’s manufacturing costs to be incurred in Switzerland, a new factor has found its way into the top five risks (25%). Only 57% of the watch executives surveyed name weaker foreign demand as a key risk to their business, down from 79% in 2016. The strong Swiss Franc remains also a significant concern, even though it is considered less important than in 2016 (46% in 2017 vs. 50% in 2016). The threat of smartwatches, with less than a quarter (23%) listing that trend as a risk has remained relatively stable compared to 21% in 2016.

Digital is key

For the first time since the Swiss Watch Industry Study was launched in 2012, “Developing e-commerce and digital channels” was a new answer option for the business strategies. 55% of watch executives see it as a major priority, making it the second priority after introduction of new products (64%, slightly down from 69% in 2016). The growing importance of having a digital strategy is not surprising given the overall luxury market transformation. Online retail sales are growing much faster than overall revenues. Until recently many Swiss watch brands had tended to be reluctant to adopt online sales channels; however this no longer seems to be the case.

Jules Boudrand, Director Watch Industry at Deloitte in Switzerland, says, “Watch brands like Tag Heuer or Panerai launched their first watches to be sold exclusively online this year. Some luxury watch-brands also partnered with blogs for limited editions. These moves come in addition to the growing development of monobrand e-boutiques by many Swiss watch brands.”

However, these days digital includes much more than just online sales. Increasing customer connectivity expands the digital influence to offline shopping. Deloitte’s online consumer survey conducted among 4,500 people in six countries shows that a substantial majority of people surveyed are still likely to buy a watch in-store, although in Germany already half of the respondents would consider buying a watch online. The use of digital has also become key to Swiss watch companies’ marketing strategies. In 2017 social media remains the most important marketing channel, followed by having a dedicated team for social community management which has overtaken bloggers.

Smartwatches not perceived as a threat

Even though Apple continues to grow its offering and other players announce partnerships with large sport brands to gain market share, Swiss watch executives do not see smartwatches as a threat to their business. A large majority (72%) do not expect them to have an impact on their sales and 14% see smartwatches as an opportunity.

“This growing market led by Apple continues to be driven by health and fitness aspects. It, however, remains difficult even for tech companies as illustrated by recent exits of this category. As the latest smartwatches launched by Tag Heuer, Montblanc and Louis Vuitton are all equipped with Android Wear and have similar specifications, it is the appeal of the brand, price positioning and differentiating factors which will be key to a potential success.”, comments Jules Boudrand.”

Millennials encourage confidence

Millennials are already an influential and growing part of the premium consumer market but will shortly be the dominant segment according to a recent research from Deloitte on millennials1. It appeared that with a budget of CHF 5,000, most of them would chose to buy a luxury watch, rather than a new smartwatch every year, for the next 10 years. A positive sign that the Swiss luxury watch industry has a bright future ahead, even among younger generations.

Read more

For more insight on the Swiss watch industry, please revert to our «Deloitte Swiss Watch Industry Study» and/or get in touch to talk to one of our industry experts.

Contacts

About the «Deloitte Swiss Watch Industry Study»

The 2017 version of the Deloitte Swiss Watch Industry Study is the sixth of its kind and unique to the Swiss market. Based on an online survey with more than 60 watch executives conducted between May and July 2017 and personal discussions throughout the year as well as a consumer survey among 4,500 people in China, Germany, Italy, Japan, Switzerland and the US (by the data collection provider Research Now), it is an indicator of the current sentiment in the Swiss watch market.

You can find our 2017 Deloitte Swiss Watch Industry Study on our website.

Deloitte Switzerland

Deloitte is a leading accounting and consulting company in Switzerland and provides industry-specific services in the areas of Audit & Assurance, Consulting, Financial Advisory, Risk Advisory and Tax & Legal. With more than 1,800 employees at six locations in Basel, Berne, Geneva, Lausanne, Lugano and Zurich (headquarters), Deloitte serves companies and organisations of all legal forms and sizes in all industry sectors.

Deloitte Switzerland is an affiliate of Deloitte Northwest Europe, a member firm of the global network of Deloitte Touche Tohmatsu Limited (DTTL) comprising of around 245,000 employees in more than 150 countries.

Note to editors

In this press release, Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity.

Deloitte AG is an affiliate of Deloitte NWE LLP, a member firm of DTTL. Deloitte NWE LLP and DTTL do not provide services to clients. Deloitte AG is an audit firm recognised and supervised by the Federal Audit Oversight Authority (FAOA) and the Swiss Financial Market Supervisory Authority (FINMA).

Please see www.deloitte.com/ch/about to learn more about our global network.

© 2017 Deloitte AG. All rights reserved.

1Survey conducted in China, Germany, Italy, Japan, Switzerland and the United States by Research Now in May and July 2017.

2Deloitte «Bling it on – What makes a millennial spend more?», July 2017.