Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue XXXVI

23 April 2018

Economy

Greater market access to mitigate trade friction

Notwithstanding President Trump's seeming obsession with the Sino-US trade deficit, market access (or the lack of it) is in fact the thorniest issue in this longstanding economic relationship. President Xi's long-awaited keynote speech at Boao on April 10 addressed the issue of market access head-on, stressing 1) the implementation of financial liberalization measures and 2) tariff cuts on auto imports as well as the easing of joint venture requirements in the auto industry. Countries like Germany have also demanded for improved market access on grounds of reciprocity, rather than filing a claim for trade imbalance (Germany's trade surplus with China in Q1 of 2018 came in of $7.77bn).

Some ground has already been covered in this regard. On April 11th 2018, PBOC Governor Yi Gang unveiled detailed plans with timetables on further opening-up in the financial sector. For example, foreign equity ownership restrictions of banks and asset management companies will eventually be abolished. In this vein, what has drawn attention, in particular, is PBOC's strong signal of deregulating the deposit rate. According to Dr Yi, base deposit rates set by the PBOC will be converged with money market rates set by market forces. By the time the "last mile" of interest rate deregulation has been traversed, competition among financial institutions will have intensified given the easier entry of foreign financial institutions.

However, the pledge on financial liberalization by China may not completely assuage the Trump Administration for several reasons. First, President Trump seems impatient with gradual changes (e.g., trade deficit). Second, China's promises on financial liberalization could be complicated with relatively strict capital account controls which are unlikely to be eased soon. As the clock ticks on the 60-day grace period before Trump's $150 billion tariff plan goes effect, China may need to take bolder and quicker actions to address the greater concern of “reciprocity” coming from the other side. Meanwhile, despite President Trump's seemingly ever-changing stance on the trade deal, US’s re-joining the TPP, should this be the case, is the next "elephant in the room" as it will not just add a member country to "TPP 11" but make the trade pact a much more compelling one, entailing a series of knock-on effects such as Thailand becoming the next country in the region to follow suit. In which case, would Indonesia, the largest ASEAN economy want to be left out?

Despite a growing positive attitude towards the TPP, China is obviously not ready to adhere due to the stringent requirements on government subsidies to SOEs and labor standards in the treaty. As such, trade friction between China and the U.S. is bound to manifest itself in other ways and spill over to other areas. If the original version of TPP re-emerges, China will have to meet new challenges with regard to improving market access, and face mounting pressure to strike a deal on a rival regional trade arrangement before long. Looking ahead, Premier Li Keqiang's visit to Japan (the 1st high-level visit by a Chinese leader in 8 years) in May and a subsequent trilateral summit with Japanese Prime Minister Shinzo Abe and Korean President Moon Jae-in will shed light on future collaborations among the three largest economies in Asia.

President Xi's assurance of an "unprecedented opening-up" at the Boao meeting has eased trade tensions between the two countries for now, but all eyes will be on policy implementation in the near future. To be precise, the first test concerns the relaxation of requirements for auto joint ventures. Meanwhile, as China's GDP growth holds steady at 6.8% in Q1, economic growth is well on track to reach the government’s goal of "around 6.5%". Surveys conducted at the CEO roundtables of MNC leaders and Chinese entrepreneurs at Boao this year have shown that global and domestic business communities converge on three points: 1) Confidence in China's sustained economic growth. 2) Business environment in China will improve. 3) Investment from private companies needs to be revitalized. The bottom line is that China still has ample policy leeway thanks to its domestic demand and global cyclical upswings.

Retail

Offline expansion accelerates

Consumers are widely regarded as the center of the retail industry while technology and data are recognized as the main driving forces. During the past decade or so, online retail has experienced explosive growth and has matured as an industry while traditional retail has gone through a period of debilitating downturns. However, by focusing on consumer satisfaction, retailers have made continuous efforts to provide customers with efficient, precise and convenient Omni-channel experiences. However, the latest wave of transformation in the industry has once more brought offline retail to the forefront. The reason for this is a change in management principles and the ubiquity of technologies. Physical stores have come to be recognized as being of "irreplaceable value" as consumer contact points. They also provide enormous scope for exercising the imagination in order to enhance the shopping experience and thus build consumer loyalty. For these reasons, stores have once again become the new focus of China's retail industry.

Acceleration of offline expansion

Starting in 2017, retailers began to aggressively promote their new retail stores. Expansion accelerated in 2018 as more and more market participants announced their own expansion plans.

A pioneer in new retail formats, Hema Fresh, under the wings of Alibaba, operated some 35 stores in late 2017. In 2018, it plans to open 100 stores nationwide, of which up to 40 new stores will be in Beijing and Shanghai. Yonghui Supermarket is also speeding up its expansion into the small format market. In 2017, Yonghui opened 172 Yonghui Life stores (100 of them opened in the fourth quarter of the year), making the total number of Yonghui Life stores well over 200. Moreover, it only took Yonghui one year to open 27 Super-species stores in nine core cities of China. The company plans to open 135 new Bravo stores, 100 Super-species stores and 1,000 Yonghui Life stores by 2020. Suning which adopts large format retail as its main force also swiftly expanded its small format stores in early 2018. On March 31, 133 stores in 43 cities opened for business on the same day. And with its Big Development strategy, Suning plans to open 1,500 small format stores by the end of 2018, and 5,000 within three years.

Figure: Expansion plans

Retailers |

Status by the end of 2017 |

Expansion plan |

Hema Fresh |

Owned 38 stores |

To open more than 100 stores in 2018 |

Yonghui |

Owned more than 200 Yonghui Life stores, 27 super-species stores and opened 133 Bravo |

To open 135 Bravo, 100 super-species and 1,000 Yonghui Life by the end of 2020 |

Suning |

- |

To open 1,500 small format stores in 2018 and 5,000 within three years |

Funtalk |

- |

To open 500 Brookstone stores in 2018 |

Lianhua Supermarket |

Opened 295 stores |

To open 205 stores in 2018 |

SPAR |

- |

To open 97 new stores in 2018 |

Source:Public information

These new offline stores, on the one hand, offer a better Omni-channel shopping experience to the consumers while, on the other hand, they represent an endeavor on the part of the main market players to try new things and innovate to satisfy the needs of the consumers, which ultimately will enhance the overall performance of China's retail industry. Furthermore, these new digital stores could be better integrated into the Omni-channel system.

Takeaways

Rapid expansion is likely to result in rapid revenue growth and continued resource integration. But, in the short term, it may also lead to an excessively heavy financial burden on the mother company and operating pressure on stores. Therefore, during the period of expansion there are several factors that merit close attention:

- Consumer satisfaction is the fundamental starting point. The essence of retail is to satisfy the consumer and hence, retail stores need to know what the needs of consumers in different regions are. The expansion of offline stores needs to be based on a proper understanding of local consumer demand with continuous operation as the ultimate goal. Long-term growth can only be achieved by constantly satisfying the consumer.

- The balance between expansion and good management must be carefully maintained. With rapid expansion, management becomes increasingly complex and difficult. Retailers need to ensure a consistent shopping experience, operating efficiency and overall planning of online and offline resources during the expansion process. Consistency can be ensured by planning and designing in advance.

- Over-investment should be avoided. Last year, capital inflow into the retail industry was tremendous and this created several unfortunate situations of over-investment. Take, for example, unmanned shelves. After a crazy expansion in 2017, the frenzy is fading fast because the costs are much higher than the return right now. For offline expansion, capital investment should be carefully managed since over-investment can lead to huge financial pressures. This could be avoided if, from the outset, close attention is paid to the ratio of cost of investment to returns.

Tech

Homecoming of unicorns

Technological innovation is one of the pillars of Chinese economic productivity and recent years have witnessed the constant emergence of new tech "unicorns". However, despite the fact that they mainly serve the Chinese market, most have opted to list overseas. Take BATJ for example,Baidu (B) and JD.com (J) are listed on NASDAQ while Ali (A) is listed on the NYSE and Tencent (T) is listed on the HKEX.

This is because the current regulatory framework in China is built around the "traditional economy", and in order to be listed, there is a "high profitability" requirement. But tech "unicorns" such as JD.com have yet to be profitable, even though their market valuation is in the billions. JD’s market valuation, for example, has already exceeded USD50 billion.

To address this gap, it is imperative for China's capital market to relax its regulatory barriers in order to support the growth of a new generation of tech enterprises.

Figure: Market Cap vs Profit of tech unicorns (2017)

On March 30, Chinese regulators issued an opinion regarding what needed to be done to bring tech "unicorns" back and outlined the requirements overseas listed "unicorns" would have to fulfil in order to return to the capital markets on the mainland. Targeted sectors included big data, cloud computing, artificial intelligence, software, integrated circuits, high-end manufacturing, bio-medicine and other related emerging industries. The companies in these sectors are also expected to own core technologies and have high market recognition.

The regulators intend to adopt the CDR (Chinese Depository Receipt, similar to American Depository Receipt) model to allow tech giants such as BATJ, Ctrip, and NetEase to list on the A-share market. Also, Foxconn, Xiaomi, Didi, and other unlisted "unicorns" can directly apply for IPOs on the A-share market.

We believe that the return of "unicorns" has six major implications. It will

1. Assist China in industrial upgrade:

The sectors chosen by the regulators represent the future direction of economic transformation. By supporting the development of innovative enterprises, the proportion of "new economy" will increase substantially on the mainland. This will support the formation of a healthy cycle of entrepreneurial innovation and investment.

2. Enhance China's competitiveness:

By protecting core competencies of these tech giants, the proposed approach will enhance China's competitiveness and strengthen its bargaining position in the global marketplace.

3. Boost future growth of unicorns:

Listing on the A-share market will provide a new financing channel for tech "unicorns", which will boost their growth. Because of the leading role they play in the new economy, rapid development of unicorns will also accelerate the growth of their partners within the ecosystem.

4. Improve quality of listed tech sector companies:

For many small to mid-sized market capitalization enterprises on the A-share list, profit has been on a gradual downward trajectory due to intense competition. The return of the tech giants to the A-share market will significantly improve the quality of listed companies, especially those in technology innovation industries.

5. Accelerate A-share internationalization:

To a certain extent, the return of "unicorns" will help make the Chinese capital market converge with overseas capital markets in valuation and correlation. As a result, the domestic A-share market will become more market-oriented and internationalized.

6. Sharing the fruits of China's economic transformation:

Although the main businesses of BATJ and other recognized tech giants is inside China, domestic investors are currently unable to share in the capital dividends generated by the rapid development of these high-tech enterprises. If such a group of high quality tech companies return and choose to be listed on the A-share market, Chinese domestic investors will have the opportunity to reap the benefits of China's economic transformation.

Logistics

A larger delivery network

The rapid development of the instant delivery network

(Note: Instant delivery refers to the delivery method that follows the customer's sudden request for a delivery to be completed as soon as possible. Frequency of requests and quantities vary dramatically and therefore involve a whole other form of logistics organization.)

On April 2, 2018, Alibaba Group partnered with Ant Financial (China's biggest internet financing institution) to acquire full ownership of China's food delivery platform Ele.me for US$9.5 billion, setting a new record for acquisitions in the Chinese internet industry. With its integration into Ali’s ecosystem, the Ele.me platform will offer catering businesses the opportunity to benefit from a much better supply chain, data collection system, and financial services. "It's a major step for Alibaba Group to expand into local lifestyle services via the Ele.me instant delivery platform within its e-commerce ecosystem and to provide a new shopping experience," said Daniel Zhang, CEO of Alibaba Group.

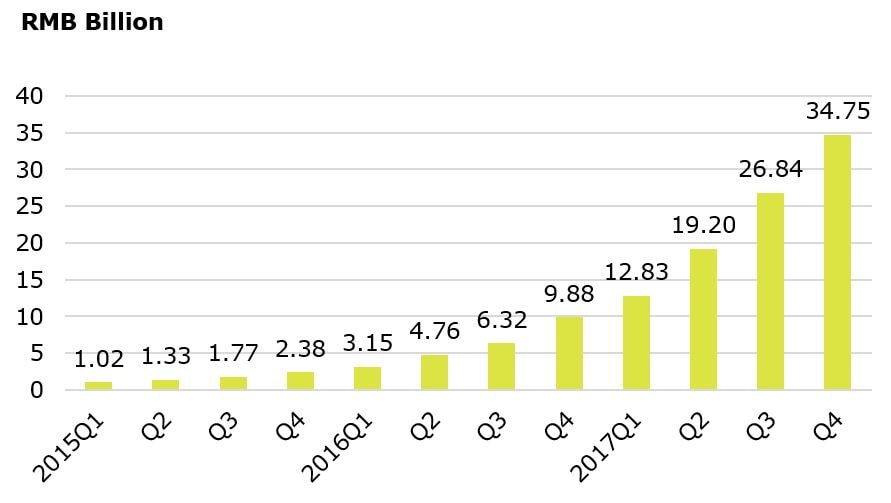

Since 2015, the instant delivery industry has grown exponentially, benefiting from the rapid expansion of upstream food delivery platforms such as Ele.me and Meituan.com. The number of transactions in the instant delivery market increased 35-fold from 2015 to 2017, and as a result, more and more possibilities have emerged in the instant delivery industry. From food delivery to grocery delivery, a number of couriers and new retail players are rushing into this sector.

Figure 1: The increase of the instant delivery market from 2015 to 2017

Instant delivery enterprises and courier enterprises move into each other’s turf

The "territory grab" frenzy in the delivery industry has ebbed, and competition is now no longer about being the "fastest". Instead, "accurate" distribution and "full" service have now become the mantra. Instant delivery, therefore, is no longer confined to food delivery. Flowers, cakes, medicine, business documents, chain stores and convenience stores are all covered. For instance, for the last two years, Dada (an instant delivery company) provided parcel delivery services to JD Logistics (a courier company) during peak holiday shopping time. And, Baidu's food delivery platform had a short-term cooperation with SF Express for parcel delivery service in Beijing and other cities.

Traditional express courier companies have also begun to move into the instant delivery business. In August 2016, SF Express launched their own "Instant Delivery" service, focusing on the urgent dispatch business in the city within a radius of 3-5 kilometers, and on servicing the one-hour local life radius. In March 2018, Yunda Express's instant delivery platform "Cloud Delivery" came online.

Figure 2: The integration trend of courier enterprises and instant delivery enterprises

A larger and more efficient delivery network is being developed

A high frequency of transactions, large volumes and a strong relationship with users of the food delivery business has greatly aided the development of the instant delivery industry. Food deliveries account for nearly 70% of the instant delivery volume but other sectors are catching up as customers begin to enjoy the luxury of instant delivery. Meanwhile, because customers are getting used to receiving orders fast, they will probably demand more from traditional courier enterprises, which will force the latter to work harder on improving the efficiency of their "last mile" delivery services.

It is becoming increasingly clear that life service applications will soon take the lead in the era of new retail. Data from all aspects of a consumer’s life not only feed into sub-industries within the ecosystem of the internet Giants (such as Alibaba and JD.com), but also affect many other industries such as finance, entertainment and travel. However, a larger and more efficient delivery network is needed to support these collaborations. In the future, the integration of traffic, capacity, and scheduling systems will become the key to the entire delivery network.