Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue XLIV

9 January 2018

Economy

How to make the best of stimulus?

The consensus is that China's economic growth in 2019, despite sizable challenges such as trade tensions and the unfinished de-leveraging campaign, will achieve a respectable GDP growth rate somewhere in the range of 6.2-6.3% (the World Bank forecasts 6.2%). There are two main reasons for this. First, barring a severe correction in the housing markets of major cities, growth in domestic consumption will remain near the double-digits. And second, even if there is a shortfall in exports, this can be compensated easily with a measured fiscal stimulus, thus allowing investment to make up for the shortfall in the external sector (China might have a moderate current account deficit in 2019). We tend to agree with the consensus but one must not ignore the side effects of underwriting an unrealistic economic growth target, nor underestimate the seductiveness of fiscal stimulus.

China's economic deceleration, which started in Q2 of 2018, has become more apparent in Q4. There are several reasons for this. First, the deleveraging campaign has greatly reduced access to bank lending. With much reduced access to credit, private enterprises have had to resort to other funding avenues such as stock-mortgage loans. But private investors have been slow to come forward as recent government discussions on mixed ownership have only reinforced the idea that SOEs must stay big and strong, thereby fanning fears of quasi-nationalization and further discouraging private investment.

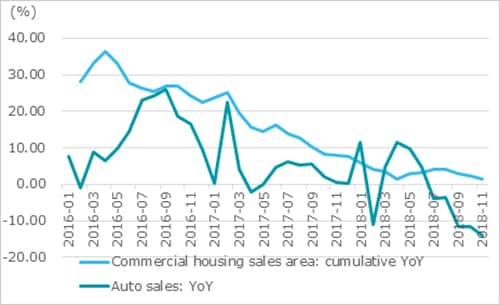

Second, the housing market has seen significantly reduced transactions on the back of a slew of restrictive policies during the year. Third, the automotive sector, a bellwether industry in China, has encountered difficulties (auto sales have seen 5 months of YOY decline) due to base effect (annual sales and car ownership) and the phasing out of tax rebates.

Chart: Slowdown in housing and auto sector

This end-of-the-year slowdown in the housing and auto sector might well prompt policymakers to unleash a fiscal stimulus package simply because such outlays will kick start economic growth. Where the housing market is concerned, an easing of restrictive policies is clearly on the cards despite official reiteration of the "homes are for shelter, not for speculation" line. This is because, between worsening affordability and stagnation in the market, the latter will be a far greater worry for policy-makers. When it comes to the auto industry, should the Government unveil more tax rebates there too in order to spur auto sales? This really depends on the outcome of the next round of US-China trade talks. So far, Washington has deferred its plan to raise the tariff on $200 billion of Chinese imports to March 2, while China is going ahead with its roll back of tariffs on US cars and auto parts. In addition, China has also stepped up the purchase of US soybeans and other agricultural products. Given these encouraging signs, it is conceivable that a truce may be on the cards in Q1 of 2019. Moreover, if the US equity market continues to correct, President Trump might be more eager to strike a deal with China.

Where trade tensions between China and the US are concerned, there are short-term issues (imbalances and market access) and long-term issues (such as the possible spillover effect of China's industrial policies and forced technology transfers) that need to be addressed separately. Short-term issues could be resolved through greater imports of US products and limited deregulation in certain sectors (such as financial services, healthcare and auto sectors). Given that US companies do not have the upper hand in all the pinpointed sectors (the auto sector is a good example), improved market access for US companies actually helps China make up lost ground in the fulfillment of WTO commitments as regards market liberalization, thus killing two rather contentious birds with one stone. However, greater purchases of US imports may also result in trade friction with other trading partners, therefore in the short run, the best policy response for China is to slash import tariffs. In the medium term, it must address the thorny issues of IPR protection and forced technology transfers. But there are no easy answers on how this can be done because progress in IPR protection is hard to quantify. But what is missing in terms of quantifying improvement in IPR protection could be compensated by a faster pace of liberalization, especially by relaxing JV requirements in sectors where profits remain sturdy.

The auto industry is a case in point. This year’s slowdown of auto sales should have given policymakers a wake-up call, making clear that further subsides will only delay the eventual agony of consolidation necessary to an industry that remains fragmented. What would be the best way to help domestic carmakers make this transition? One way would be to have greater fiscal outlays on social safety nets and job re-training for dislocated workers. More importantly, decisive action on relaxing JV requirements could send a powerful signal that China is committed to making the domestic market a more open. On policy responses, we have been consistently advocating a lower GDP growth target precisely in order to avoid over-capacity and other spillover effects of China's industrial policies. With the benefit of hindsight, one can see that China's massive fiscal stimulus package in 2008 helped the world economy by boosting commodity prices and market sentiment at a time when gloom and doom had besieged the global economy. But China's rapid capture of market share in the manufacturing sector may also have fanned the fires of protectionism in the West. Therefore, if policymakers do feel compelled to rely on an expansionary fiscal policy to cushion external shocks, the emphasis should be more on social development (healthcare, education and low-income housing for example) rather than on infrastructure.

Where monetary policy is concerned, China is likely to face greater constraints in 2019 if the Fed stays on its present course of monetary tightening. We are of the view that because the Fed is more interested in normalizing short-term interest rates and is less concerned about stock market valuations, it will probably stay on its present course. In the medium term, interest rate differentials between China and the US are likely to widen, which will again put more pressure on the RMB. That said, a flattening or even inverted yield curve of the US interest rates--prompted by fears of recession--could take some pressure off the RMB. Slumping crude oil prices have also come as a huge relief to most Asian economies, China in particular. As such, a moderate inflationary outlook in China could provide policymakers more leeway in steering the RMB exchange rate slightly lower as a tool of monetary easing in 2019.

Financial Services

Further opening under a loose credit policy

In 2018, shadow banking activities were brought under regulation, while "de-leveraging and tightened supervision" was reduced to "stabilizing leverage". The People’s Bank of China (PBOC) lowered the reserve requirement ratio (RRR) four times during the year. Financing for small and micro businesses and private enterprises was enhanced as monetary policy moved towards being more neutral and looser. Looking ahead to 2019, liquidity will be stable and a loose credit cycle will begin. In such a situation, foreign capital is likely to come rushing into the market and more stringent regulatory requirements may be placed on financial institutions.

Credit will be eased

Strict regulatory compliance has been imposed on shadow banking activities and the impact on financial deleveraging is clearly reflected in the data: the growth of M2 and total social financing in November registered at 8.0% and 9.9% respectively, the lowest level in history. In 2019, despite this downward economic cycle, "stabilizing leverage" will continue. The PBOC may release liquidity from time to time through reserve requirement ratio reduction, reverse repurchase and other policy tools in order to maintain a loose monetary and credit environment.

Specifically, two categories of enterprise financing stand to benefit: 1.) financing for small and private enterprises will be enhanced through such means as targeted RRR reduction, private enterprise bonds and equity financing tools, and 2.) financing for real estate (RE) companies, which has been dormant for a while, will also accelerate. For example, the government recently announced that high-quality RE companies which have a debt ratio not exceeding 85% and with a triple A rating can issue bonds in order to garner financing. Since the peak period for debt repayments for many RE enterprises falls between 2019 and 2021, this will go some way to ease the financing pressure they have been facing under multiple rounds of regulation.

Further opening-up

Since its announcement at the Boao Forum in April, the specific measures of China's financial opening-up have gradually been implemented: 1/ there are no restrictions on foreign ownership of banks and asset management companies; 2/ though a cap of 51% is currently placed on foreign ownership of joint venture securities companies and personal insurance companies, this restriction will be phased out in three years. As a result, a number of foreign institutions have made preparations to open new branches or to increase their shareholdings in existing ventures, including JP Morgan, UBS, Allianz Insurance, American Express and Bridgewater Associates.

According to PBOC data, the total assets of foreign banks account for about 1.7% of the total assets of China's banking sector while share of inter-bank bonds held by foreign investors is only 1.8%, much lower than the global average of foreign ownership. The entry of more foreign participants will accelerate the integration of China's financial industry into the global financial system. The business model of "foreign capital holding + local operation" will not only increase the market share of foreign capital but also enhance the operation and management capabilities of domestic institutions. In the process of opening up, relevant accounting, auditing, taxation and legal structures will also be improved.

Transformation of banks' WM businesses will accelerate

In 2019, the wealth management (WM) subsidiaries of banks will obtain licenses to open for business. This will have two positive effects. On the one hand, banks’ natural advantages in sales channels and capital will force the mutual fund industry to improve its competitiveness, making the asset management (AM) industry as a whole more market-oriented and competitive. On the other hand, product research, online channels, investment management and creating and nurturing the talent pool will become the key components to competitiveness.

Along with the implementation of new AM regulations, banks’ WM businesses have a long way to go in terms of transformation. Business positioning and risk preference of WM subsidiaries and fund companies of banks as well as publicly-offered mutual fund companies all need to be clearly defined so that investors can understand what services they will be receiving. Investors can purchase WM products online without any restrictions in the future. If the business transformation goes smoothly, the AM businesses of banks will play an important role in the transformation of the asset management (AM) industry in the future.

Financial holding companies face challenges

On the heels of the stringent regulation of shadow banking, AM and internet finance, financial holding (FH) companies will become the next subject of regulatory supervision. The PBOC is currently conducting a simulation supervision of five pilot FH institutions with the object of releasing pertinent regulation guidelines in the first half of 2019.

Financial holding companies refer to non-financial enterprises that invest in financial institutions. These investments are made primarily for two purposes: normal investment returns and obtaining financial licenses to facilitate operation of connected transactions to raise funds for other businesses. In essence, these kinds of operations closely resemble shadow banking activities, and hence they have become the subject of regulatory supervision that targets the shadow banking chain hidden behind FH platforms controlled by FH private enterprises. Regulatory focus will be on market access, capital adequacy ratio, asset-liability ratio, comprehensive risk control and connected transactions. In 2019, FH companies will be made to undergo regulatory compliance for which they will have to conduct self-examination and evaluation, re-examine strategic planning and exercise caution on mergers and acquisitions.

Systemically important financial institutions (SIFIs) face stricter compliance requirements

Five of China's institutions have been placed on the global SIFIs (G-SIFIs) list, namely the `Big Four’ banks (ICBC, ABC, BOC and CCB), and Ping An Insurance. China is in the process of drafting regulatory rules for its own list of SIFIs which will include banks, insurers and securities firms as designated by regulatory agencies. These businesses will be subject to even tougher capital and leverage requirements, and will face higher compliance costs.

A number of banks have already disclosed plans for supplemental capitalization in the tens of billion of Yuan. Banks are expected to take further steps to recapitalize in 2019 for the following reasons: to raise capital (RMB 1 billion to 16 billion) for the new AM subsidiaries, higher capital supplements for credit expansion and higher capital adequacy requirements as required by regulatory compliance. Against such capital needs, all bank’s net profit growth will face severe challenges.

Retail

Transformation vs. divergence

Like in previous years, the retail market has continued to grow – albeit at a slower pace. Till November, total retail sales growth averaged 9.1% year on year. The sequential monthly growth rate, which had been hovering between 8.5% to 9.2% after it registered the second lowest monthly growth rate of 8.5% in May, hit a new low of 8.1% in November. Categories like cosmetics experienced obvious growth decline in the past few months. The slowdown in retail growth is of some concern to the government as boosting domestic consumption is an important part of the Chinese economic agenda. Hence the government has introduced a series of growth oriented policies, such as the new income tax policy and the consumer goods import tariff policy, that support innovative and emerging models of Cross-border E-commerce. Going by the current status of the market, three major trends are likely to emerge in 2019:

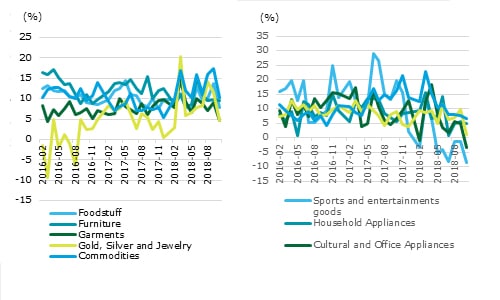

As growth is not uniform across all sectors, it is important to pay close attention to developments in the sub-sectors. The sustained growth of the Chinese economy and a series of government sponsored incentives will continue to be the driving force for consumption. It is worth noting that,according to the monthly sales figures of enterprises above designated size (5 million yuan revenue for retail company), foodstuffs, furniture, garments and other household items enjoyed relatively stable growth over the past 24 months. On the contrary, sports, entertainment, leisure products and office appliances recorded an obvious decline in growth. Sales of cosmetics,in particular, after maintaining a cumulative growth rate of 11.4% in much of 2018, plummeted to 4.4% in November. Thus it seems safe to say that staples will enjoy a relatively stable growth in the upcoming year but the future of other sub-sectors is not so clear.

Chart: Monthly retail sales growth by enterprises above designated size

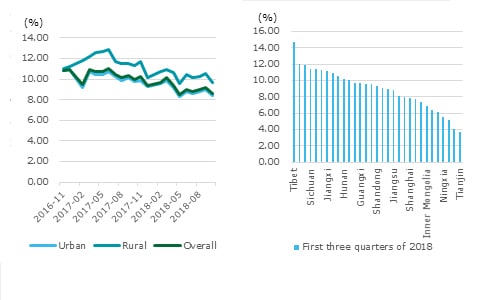

Consumption divergence. According to the National Bureau of Statistics, the inclusion of less developed parts of the country into existing networks of retail and distribution is certain translate into higher growth in the future. This is born out by two pieces of evidence: sales in rural areas is growing at a faster pace than those in urban areas, and second, sales in central and western China are growing much faster than in cities like Beijing and Shanghai. The development of retail technologies and supply systems will further stratify consumers into discrete consumer groups as demands are categorized and met with more precision. So because of the development divergence, in this market as both high-end consumption like cross-border e-commerce and price-sensitive consumption company like Pinduoduo will co-exist, both have future growth potentials.

Chart: Retail sales growth in different areas

Transformation will continue. After an initial phase of very rapid growth, large capital inflows led to the creation of `bubbles’. As a result, some market players have hit a `development bottleneck’ where investments in traditional channels no longer lead to a growth in sales revenue. Hence, they have had to search for other avenues of growth, bringing new technologies and diversification to the retail industry, especially in the sub-sector of new-retail. Investments in new retail are a good barometer of emerging market trends and innovation. In 2016 and 2017, total venture capital investments in this sector exceeded RMB 70 billion, with the average value of investment also increasing rapidly. Projects like conveniences stores and e-commerce garnered the lion’s share of the funding. At the same time, projects like cashier-less retail, supply chain/logistics and other services attracted the lions share of investment even though the average investment amount was much smaller. Investments that support innovation and improve infrastructure will increase the pace of the transformation underway and this is likely to be the case in 2019. In summary, the consumer-centric retail transformation driven by new technologies and data has become the widely accepted norm in the industry and will continue to transform retail. The maturing of technologies, the integration of resources and the transformation promotion by leading companies will be the main forces driving China's retail industry transformation.

Chart: Investments and financing in new retail area

Technology

Silver lining in the dark cloud

The Sino-US trade war will continue to haunt the tech sector

2019 seems destined to be a bumpy year for the tech sectors of China and the US. The tit-for-tat tariffs will probably continue and may even escalate if no agreement can be reached on fundamental structural reform in areas such as intellectual property, technology transfer and cyber-attacks. Chinese telecommunication vendors are particularly vulnerable due to their heavy reliance on US semiconductor chips to produce networking equipment. The consequences could be catastrophic if the US were to impose an export ban on semiconductor chips since there are no viable alternatives on the market. This will also hamper China's ambition to become a global leader in 5G technology.

If the trade war continues into 2019, it will also have a profound impact on the supply chains of MNCs in China. Apple, for example, has long used China as its production base for everything from its signature iPhones to iPads. The company’s supply chain now spans hundreds of companies, culminating in assemblers such as HonHai and Pegatron Corp. But these suppliers are now considering shifting some of its iPhone production away from China should tariffs on U.S. imports rise to 25%. Apple, already grappling with mounting evidence that its latest iPhone line-up has failed to excite consumers, can ill-afford a hike in import taxes. Also, The Chinese Internet sector is beginning to show signs of fatigue as regulatory supervision begins to tighten. Workforce optimisation has spread to online video, gaming and social media companies, cutting jobs across the line in sharp contrast to the rampant hiring spree just a few years ago.

Not all is gloom and doom in the realm of TMT, however. Globally, the technology sector is still expected to experience healthy growth. Opportunities are still abundant as technology reshapes how and what we consume, how we connect with each other and how we perceive the world around us.

Emergence of 5G for the masses

2019 will be the year when fifth-generation (5G) wide-area wireless networks come of age. In 2018, 72 operators tested 5G, and by the end of 2019, we expected 25 operators to have launched 5G service in at least part of their territory. Further, we expect about 20 handset vendors to launch 5G-ready handsets in 2019 (with the first available in Q2), and about 1 million 5G handsets (out of a projected 1.5 billion smartphone handsets sold in 2019) to be shipped by year's end. The most noticeable benefits for users of these initial 5G networks will be faster speeds than current 4G technology: peak speeds of gigabits per second (Gbps), and sustainable speeds estimated at the hundreds of megabits per second (Mbps).

5G wireless technology will have three major applications. First, 5G will be used for wireless connections, mainly by devices such as smartphones. Second, 5G will be used to connect "less mobile" devices, mainly 5G modems or hotspots: dedicated wireless access devices small enough to be mobile that will connect to the 5G networks which in turn enable them to connect to other devices via WI-FI technology. Finally, there will be 5G fixed-wireless access (FWA) devices, with antennas permanently mounted on buildings or in windows, providing homes or businesses with wireless broadband in place of a wired connection.

The few are bringing AI to the many

In 2019, companies will accelerate their adoption of cloud-based artificial intelligence (Al) software and services. Among companies that adopt AI technology, 70 percent will obtain AI capabilities through cloud-based enterprise software while 65 percent will create AI applications using cloud-based development services.

More importantly, we will see the democratization of Al capabilities and benefits that were previously the preserve of early adopters will become available to everybody. The problem with Al is that to date, many companies have lacked the expertise and resources to take full advantage of it. Machine learning and deep learning typically require teams of AI experts, access to large data sets, and specialized infrastructure and processing power. Companies that can bring these assets together then need to find the right uses for them. Applying AI to create customized solutions, and scale them throughout the company requires imagination and a level of investment and sophistication that takes time to develop. This is why AI has been and continues to be out of reach for many companies who in theory stand to benefit enormously from AI technologies. For this reason, the initial benefits of AI have accrued mainly to the global "tech giants.” China's BAT (Baidu, Alibaba, and Tencent) is investing heavily in AI while expanding into areas previously dominated by US companies such as chip design, virtual assistants, and autonomous vehicles.

To develop their AI services, these tech giants are following a familiar playbook: (1) finding a solution to an internal challenge or opportunity; (2) perfecting the solution at scale within the company; and (3) launching a service that quickly attracts a mass following. Hence, Amazon, Google, Microsoft and China's BAT are launching AI development platforms and standalone applications to the wider market based on their own AI experience. Through the cloud, smaller players can also access services that address shortfalls such as having to make big upfront investments. In short, the cloud is democratizing access to Al by giving companies the ability to use AI without having to invest too much in hardware or software.

China's world-leading connectivity nurtures new digital business models

By the start of 2019, 600 million people in China will be using their phones to make payments, about 550 million people will regularly use their smartphones to shop online, and about 200 million people will use mobile enabled bike-sharing services. In 2019, China will have the world's largest fiber-to-the-premise (FTTP) deployment, exceeding the runner-up by a significant margin. It will also most likely have over 330 million full-fiber connections, representing about 70 percent of the world's total. China's strengths in connectivity will probably be a key factor enabling it to diversify from manufacturing the technology to developing and executing new digital business models. Its communications infrastructure will provide a foundation for the development of at least three significant new industries, each of which could generate tens of billions of dollars in revenue annually by 2023.

Looking ahead, China's communications network is likely to be the foundation of several key new bandwidth-hungry applications including machine vision, social credit, and new retail concepts.

- Machine vision is likely to play an increasingly crucial role in authentication. A person's facial features may be the identifier used to authorize payment for everyday goods, or to verify access to public transport systems. Over time, the quality of the verification image is likely to become better and better as the software behind it gets refined.

- Social credit can be an alternative to traditional credit rating systems that rely on credit card history, mortgage payments, or time employed. In China and many other emerging countries where such records may not exist for a large proportion of the population, social credit systems can fill the gap.

- Finally, Alibaba and Tencent (both of which were formerly online-only businesses) are buying into the traditional physical-store retail model and looking to use their digital knowledge to create better shopping experiences. Tech companies are looking to AI to improve supply chain efficiency and to optimize inventory and product recommendations. They are also experimenting with deploying cameras and developing autonomous stores.

Chinese semiconductors will power artificial intelligence

While China leads the world in the consumption of semiconductor products (it consumes more than 50 percent of all semiconductors produced annually), Chinese manufacturers only meet around 30 percent of domestic demand. Amidst shifting macroeconomics and the growing value of Al, the Chinese government and leading digital businesses have signalled that greater self-reliance in semiconductors is a vital component of the future. They are investing and hiring aggressively to create onshore manufacturing capabilities on par with the top global foundries. Many Chinese companies are designing specialized semiconductors for Al and have already designed chip architectures that are at the cutting edge of the mobile smartphone industry.

In 2019, to meet growing domestic demand for chip sets, revenues from semiconductors manufactured in China will grow by 25 percent to approximately US$1100 billion from an estimated US$85 billion in 2018. This increase in revenues will be driven in part by the growing commercialization of artificial intelligence (AI). In 2019, a Chinese chip foundry will begin producing semiconductors that specialize in supporting AI and machine learning (ML) tasks.

While China may have fallen short in the development of its semiconductor industry in the past, with strong coordination between the government and domestic manufacturers, this time round it could quite well succeed as it is putting a great deal of capital and its massive market behind the advancement of its semiconductor agenda. Its success will depend on the increasing co-operation between computation, data collection and emerging technologies.

Automotive

Navigating a cyclical stagnation

China’s car market may enter an extended period of zero growth but bright spots remain.

In early December, CAAM forecast that auto sales growth will stall in 2019, citing expiration of tax incentives, a cooling economy and sagging consumer confidence as the primary reasons. The organization also warned it would take at least three years for the market to regain its strength. Car sales are likely to hover between 28 and 29 million prior to 2021. Despite the slowdown, we still believe that there will be an internal consumption upgrade in the car market that will drive car sales in the next few years. This trend is already evident in sales of premium vehicles which stood out as the only performing segment this year. The consumption upgrade not only reflects the desire of certain segments of consumers to shop for higher-quality vehicles at higher prices but also addresses their preferences for passenger vehicles that are more spacious with all the latest technological ‘bells and whistles’ and which are environmentally friendly. We expect that demand for premium cars will account for about 12% of the market in 2019.

NEV segment will continue to outshine the rest. Both foreign brands and start-ups have committed to accelerating NEV production and offering new models of NEVs by either making new investments or securing existing capacities via partnership with domestic carmakers. These moves have successfully rejuvenated the NEV market with much better and more competitive car models since last year. Additionally, we’ve seen an increasing readiness in many Chinese cities for a mass adoption of electric vehicles. In early December, NDRC along with other regulatory bodies released an action plan to step up the construction of charging stations and to realize a 1:1 charger-to-EV ratio by the end of 2020.

Nevertheless, the NEV industry is expected to face headwinds in the near future. First, fiscal subsidies will shrink by up to 40% (equivalent to 9,000 yuan). Since EV demand is highly price sensitive, the higher cost (If OEMs fail to step in and fill the subsidy gap, electric cars are expected to see an approximately 10% to 15% increase in prices) will to some degree dampen a client’s willingness to purchase. China has replaced subsidies with a dual-credit scheme that aims to keep NEV makers that have accumulated an excess of credits financially afloat. However, NEV credit trading hasn’t proven to be very lucrative for carmakers as there is a lack of clarity on the value of each credit. Second, foreign carmakers remain on the sidelines in terms of establishing a footprint in China’s NEV market. Instead of coming to the market with competitive models, they, for now, would rather meet the government-mandated NEV quota requirement by selling the credit-generating models of their Chinese partners. Taking into account all the afore-mentioned factors, we estimate NEV sales will grow by about 20% to 1.5 million units in 2019.

Further opening-up and industry reshuffle. We expect a handful of foreign OEMs will either increase their investment to become the controlling shareholder of their China JVs or seek to establish wholly-owned NEV operations, leaving their Chinese partners in a technology vacuum. In addition, China has recently given the green light to “car assembly”, encouraging NEV start-ups to leverage their assembler’s manufacturing license before applying for their own and to reduce excessive capacities at the same time. This move, however, may inadvertently allow carmakers with low value addition to stay in business for a much longer period of time.

Energy

Super cycle coming to an end

Shale production fluctuation causes faster price gyrations

Both Brent and WTI crude oil prices have gone down more than 30 percent since reaching a peak in October as investors worried about economic slowdown and over supply. OPEC and non-OPEC producers are expected to soothe growing market concerns by cutting back on production by 1.2 million barrels a day starting in January. Nevertheless, there is a growing consensus that the traditional boom-bust cycle is being replaced by faster price gyrations based on production fluctuation. This new trend makes price movement less extreme but also more difficult to predict. The ever-changing number of barrels of crude available from shale operations is one of the main causes.

Chart: Crude Oil Price (USD per barrel)

|

2016 |

2017 |

2018 |

2019 |

WTI Crude |

43.33 |

50.79 |

65.18 |

54.19 |

Brent Crude |

43.74 |

54.15 |

71.40 |

61.00 |

Source: EIA

Natural gas demand outgrows oil

China's demand for oil is projected to grow 2.7% in 2019, driven by growth in the petrochemical industry and car ownership. Natural gas consumption will grow 9%, much faster than oil consumption as the government is working hard to tackle air pollution in the major cities and to steer China’s energy mix towards cleaner fuel sources. China's steadfast pivot to natural gas portends a continued structural decline in crude oil production as investors focus their attention on natural gas and renewables-related projects at the expense of coal and oil.

Natural gas imports set to boost

China's natural gas imports will grow strongly in 2019, keeping pace with the robust nationwide gasification efforts. In September, Beijing announced guidelines to expand import options in terms of countries (regions) of origin, modes of transport, import channels and contract types ("Opinions on Promoting Coordination and Development of Natural Gas"). LNG imports will outstrip pipeline gas imports over the next two years even though slowing economic growth and demographic trends, as well as rising contract prices, represent potential headwinds to stronger growth.

China's capex geared towards upstream

Global spending on oil and gas will increase from USD 507 billion in 2018 to USD 540 billion in 2019, according to an EIU survey, signifying the return of a sector-wise development momentum after one of the most aggressive down-cycles in recent history. As global spending is shifting from oil to gas and downstream sectors, China's investment, in contrast, will be geared towards the upstream as NOCs prioritize domestic oil and gas projects to support growth in domestic demand.

Logistics

Striving to further upgrade

The arrival of the digital economy has brought about significant changes to the logistics industry. First, globalization has gradually broken down geographical boundaries, making the global deployment of resources not only possible but also easier, ushering in an era of `global logistics’. Second, data and artificial intelligence applications have become the key elements for the large-scale deployment of big data technology and intelligent hardware which propels the logistics industry towards the goal of interconnectedness and intelligence. Third, digital development drives the better realization of green logistics. There is no doubt that the digital economy will have a profound impact on the structure and development of the logistics industry in the future.

Logistics globalization resources need to be integrated

As a traditionally large-scale industry, the logistics industry, with the help of internet technologies, is gradually transforming itself into a global industry in the context of the current economic globalization and the fast-paced growth of multinational corporations. In the future, if logistics companies want to ensure delivery within 72 hours or an even shorter timeframe on a global scale, there is no way to accomplish such a goal relying on any one logistics company alone. To achieve the globalization goal of the logistics industry, it is imperative to integrate the logistics elements of the world, connecting logistics partners across the globe and forming a global logistics network. Only once this kind of a network is established, can one even talk of implementing an optimal configuration of digitalization and intelligence. In other words, in the logistics industry, first one has to have the network, then one can invest in the hardware (and software).

However, in the process of internationalization, China's logistics industry still has to tackle numerous issues. For example, strategic international transportation channels have yet to be fully established. Chinese companies still lag behind foreign logistics giants in terms of imported resource integration capability and logistics service competitiveness. Chinese companies could try to close the gap by improving their rankings on the Global Logistics Performance Index.

At the same time, international customer demand has changed too, going from standardization to customization. Hence, international logistics suppliers should also transform their service offerings accordingly, from pursuing quantity to pursuing quality; from providing a single uniform product service to providing personalized and customized services; and from providing port-to-port services to providing door-to-door services.

In the new era, the road map for the development of China's logistics industry is clear. The next step for China's logistics industry is to further open up, participate and compete internationally, and integrate more global logistics resources into their network.

B2B logistics needs a more `intelligent’ upgrade

China's logistics industry has entered the stage of cost reduction and efficiency enhancement. Intelligent cost reduction will become the focus during this stage.

In recent years, the B2C logistics business represented by express delivery and e-commerce has been an important vehicle for growth. However, the truth is that mainstream demand for logistics still is production logistics. As the world's largest manufacturing country, B2B logistics resulting from the manufacturing sector account for more than 90% of the logistics market. In the first three quarters of 2018, the total volume of industrial logistics transactions reached RMB 184.5 trillion, accounting for 90.4% of total social logistics. But, in spite of the huge market, B2B logistics still faces many challenges, such as the lack of sharing of logistics resources, information asymmetry and a subsequent serious waste of resources.

Smart logistics is characterized by “digital drive” (using data to create benefits) and “collaborative sharing” (creating a collaborative environment for enterprises to share information and resources). But B2B logistics involves multiple business entities across different industries and these manufacturers and logistics service providers may not have a sufficient level of willingness to establish digital connectivity networks. On the other hand, many ocean shipping companies, port operators and e-commerce companies, in addition to logistics service providers, have been transforming themselves into integrated logistics service providers, building logistics ecosystem platforms which revolve around their core businesses. This makes it more difficult to accomplish collaborative sharing.

However, B2C's high-experience and high-standard logistics services in the retail consumer segment have provided valuable lessons to the logistics industry as a whole and are also forcing B2B logistics services to upgrade. In the future, cost reductions will have to come from an increase in efficiency and the creation and expansion of digital supply chains.

Green logistics goes `upstream’ in the industrial chain

For China's express delivery companies, "being fast" can only guarantee that they will not lose but "being green" will result in total victory. At present, many express delivery companies are working towards the goal of being environmental friendly by adopting a variety of measures such as recyclable packaging cartons, electronic sheets, green-energy logistics vehicles.

But to be truly effective, green logistics should be further extended `upstream’ in the industrial chain. In order to promote green logistics, e-commerce enterprises, logistics enterprises and brand owners should come onboard and work together towards a common goal. Only by connecting ‘upstream’ and ‘downstream’ can we achieve better and more environmentally friendly logistics. In addition, the implementation of a multi-dimensional capacity buildup such as green storage facilities, green technical equipment and green enterprise management standards will also contribute to the rapid development of China's green logistics.

Life Science & Healthcare

From scale to innovation

Total sales of China's Pharmaceuticals, Medical Devices and Medical Supplies is expected to reach RMB1.1 trillion in 2018, accounting for a year-on-year increase of around 15%. The high growth came primarily as a result of stringent supervision and policy support for clinical innovation in the past several years. Looking forward to 2019, sales growth is forecast to slow down due to a new round of cost-cutting policy measures and an increase in the cost of Active Pharmaceutical Ingredients (API).

Policies put more pressure on drug prices

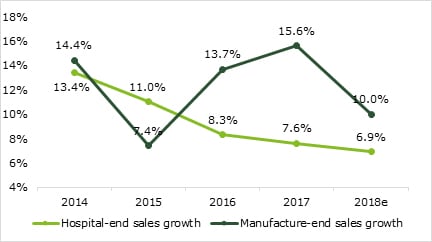

Implementation of the previous round of cost control policy measures such as the "Two Invoice System" and "Price Negotiations with Medical Insurance" has resulted in a great many changes to the structure of China's pharmaceuticals industry. The drug distribution market has become more concentrated as a result and drug sales growth at hospitals has continued to slow down. It is fair to say that these approaches have effectively reduced drug prices and unnecessary healthcare expenditure.

Chart: Hospital-end growth VS Manufacture-End growth

The fourth quarter of 2018 ushered in a new round of cost control policies, the most important one being "drug procurement with target quantity". This new centralized drug procurement program requires drug companies to lower their drug prices in exchange for a guaranteed purchase quantity, usually 70% of total market demand. Under this program, prices for the 31 off-patent generic drugs will be reduced by as much as 96%. If the coverage of this program keeps growing, it will have significant ramifications for both pharmaceutical MNCs and domestic drug makers.

Increasing cost on APIs will push down the margins

The cost pressure on China's pharmaceutical companies is also growing as prices of Active Pharmaceutical Ingredients (API) have been increasing since 2017. Higher environmental compliance requirements have forced numerous small- and mid-sized API suppliers to close operations, which has resulted in a reduction in capacity, so much so that currently supply can hardly match demand.

As a result, drug makers are now under pressure from two fronts: 1/The margin from OTC and generic drugs will become lower and lower in the future, reducing profits and 2/ pursuing new drug development has become crucial for China's pharmaceutical companies, pushing up costs.

Clinical commercialization is accelerating in China

Efficiency for new drug development of China's drug companies continued to improve in 2018, especially in the areas of biotech and immunotherapy. The first domestic PD-1 Inhibitor (an immunotherapy drug) was approved by the CFDA in December 2018 and 3-5 domestic companies are expected to have their products approved soon. These achievements indicate that China's innovative pharmaceutical companies have already been able to compete with global leaders on developing "first -in-class" and "best-in-class" products. We believe that they will attract more and more attention and investment worldwide in the future.