Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue XLV

27 February 2019

Economy

RMB: bucking the trend?

Thanks to ongoing trade talks with the US, the renminbi has performed quite well thus far. Markets are looking up, as they seem to think that even a temporary suspension of conflict can only improve the rather subdued sentiment in China and the region, triggering equity rallies and bolstering battered regional currencies. A second possible reason for the stability of the RMB could be that, of late, there has been a sea change in market expectations regarding interest rate hikes by the U.S. Federal Reserve. The most recent decision by the Fed to leave short-term interest rates unchanged has dampened bullish sentiment on the greenback significantly, thereby easing the pressure on the RMB.

Chart: RMB underpinned by a dovish Fed and trade talks

There is, however, a third possibility. The RMB exchange rate is often affected more by politics, than by economics—as evidenced by the decision taken by Beijing to keep the currency stable during the Asian Financial Crisis. This time around, Beijing seems set on keeping the RMB exchange rate steady as a gesture of goodwill as long as trade talks continue. Although comparing Beijing’s current position with the 1985 Plaza Accord between the US and Japan (Japan was then forced to appreciate the Yen sharply in order to defuse trade tension with the US) is probably grossly overstepping the mark, it seems that the market has indeed decided that Beijing will at least keep the RMB stable for the next few months. In our view, the prevailing market perception is probably correct.

However, in reality the policy bias towards a stable exchange rate goes back to the second half of 2018. Despite the various mechanisms that enabled the People’s Bank of China (PBOC) to have a managed floating exchange rate regime, rightly or wrongly, an exchange rate of 7.0 (USD/CNY) has been seen as a key psychological threshold in terms of confidence (even though the PBOC’s reserves were at $3.07 trillion at the end of 2018). The real issue is whether a stronger RMB exchange rate would come at too high a price—that is, lead to sub-par growth or become a drag on corporate profitability, or corner China into a situation that the exchange rate could only rise. Our long-held view is that China does not need a major downward revaluation of the exchange rate in order to restore competitiveness. However, a slightly weaker RMB (an implicit monetary easing) will be in line with the PBOC's accommodative monetary policy. Any monetary tightening (whether from higher interest rates or a strong currency) will increase the pains of deleveraging.

Looking at the Chinese currency through the lens of the US-China trade tension, the best-case scenario would be for China to avoid the 25 percent tariff on $200bn of exports to the US by opening up its domestic market in a meaningful way (services mainly) in addition to greater purchases of US agriculture produce and energy products. However, depending upon a successful outcome from the trade talks also means that China has to keep the RMB exchange rate relatively stable amidst persistent downward pressure. The worst-case scenario is a continued impasse that will weigh heavily on both stock market sentiment and private investment. In addition, such a situation would make it increasingly difficult for Beijing to execute certain much-needed domestic reforms, such as relaxing JV requirements in certain sectors and increasing foreign ownership in the financial sector. In this case, a moderately lower RMB exchange rate would boost exports and improve liquidity. Regardless of the outcome of the trade talks, the PBOC would like to keep monetary conditions loose, at least by cutting reserve requirement rates (probably twice this year).

In theory, China could engineer a modest revaluation of the RMB in such a way that the expectation of further depreciation would be removed. Hong Kong's banking system, which has been circulating the RMB as a legal tender for years, is probably a good litmus test. If RMB deposits in Hong Kong banks remain stable, this would indicate that the market doesn’t anticipate a large RMB revaluation.

Chart: RMB deposits in Hong Kong rose on improving sentiment

In practice, however, it is almost impossible to know where to stop. To maintain a stable exchange rate while allowing interest rate differentials with the United States to widen will bring about distortions in the economy and increase the administrative cost of tighter capital controls. According to Deloitte economists, certain weaknesses of the US economy have become increasingly apparent in both the corporate and consumer sectors because of the higher cost of borrowing. The Federal Reserve's decision not to hike interest rates in the previous FOMC meeting seems to have been validated in its January bank lending survey which showed that lending standards have been tightened significantly since the last recession. If the US interest rate only goes up by 25 bps in 2019, downward pressure on the RMB will ease. But, a dovish Fed will also increase the likelihood of a synchronized global economic slowdown. It will be difficult to argue for strengthening the RMB if protectionist sentiment starts to gather momentum in more countries.

Another important factor affecting the RMB outlook in 2019 is deleveraging. As this will be a multiyear project and can by no means be done in a painless manner, in the end, the debt/GDP ratio has to come down through a combination of economic growth, inflation, and debt workout. Other countries’ experiences of debt reduction suggests that a slightly higher inflation rate will make this process less painful. A slightly higher inflation rate will necessitate a weaker exchange rate.

To sum up, China has many tools to stabilize the RMB in 2019 and even beyond, but the real question is at what cost. On balance, a slightly weaker RMB will bring greater economic benefits than maintaining a stable exchange rate. Of course both the US and China's other trading partners would like to push Beijing to allow the RMB to appreciate. But a strong RMB will tighten monetary conditions, which is inconsistent with the existing policies of revitalizing private investment. If Beijing adjusts the RMB exchange rate by 3-5% (less than 3% will not have any meaningful effect), this might inflame fears of a potential contagion effect in the other economies of the region. However, the contagion effect from RMB revaluation is overstated. Unlike 1997, when emerging Asia was severely hit by drastic outflows of capital, most economies are in a much stronger position in terms of balance of payments and fiscal position. The sharp fall of the Yen that was a result of the 1997-1998 Asian Financial crisis is unthinkable today.

However, the best way to ease such worries is by a greater liberalization of China's vast domestic market so that other economies can also benefit from China's consumption boom. If Beijing can strike a balance between deleveraging and economic growth, a softer RMB exchange rate, so long as it is not a significant revaluation as in 1994, will have little impact on regional economies. All the same, at some point, Beijing will have to embrace a more flexible exchange rate. With hindsight, it appears that it was easier for China’s policymakers to tolerate controlled appreciation when the RMB was facing persistent upward pressures (as since early 2000) than a controlled depreciation. A meaningful liberalization in the financial sector (e.g., securities, credit rating, insurance and asset management etc.,) will create demand for RMB denominated assets from foreign investors who tend to value a higher degree of currency convertibility more than a stable exchange rate per se. And finally, we should revisit our original 2019 forecast of 7.3. Barring a nasty shock from the trade talks, the RMB is likely to undershoot our original forecast, but the direction will remain intact. To put it differently, underlying downward pressure on the RMB is unlikely to disappear in 2019.

Financial Services

Perpetual bonds to improve access to credit

On December 25, 2018, China’s Financial Stability and Development Committee called for the issue of open-ended capital bonds, also called perpetual bonds, as quickly as possible in order to help commercial banks replenish their capital through multiple channels. Within a month, Bank of China was given approvals for the issue of RMB 40 billion worth of perpetual bonds on the interbank bond market to supplement its tier 1 capital. This is the first issue of such bonds by any Chinese commercial bank and is expected to boost Bank of China’s capital adequacy ratio by 0.3 percentage points. Compared to the more traditional method of preferred stock financing, perpetual debt financing is easier to operate and has an immediate impact on capital enhancement, easing liquidity conditions and improving credit lending. However, precisely because it is easy, investment risks cannot be ignored.

Toward TLAC compliance

From the perspective of banking operations, the use of perpetual bonds has three highly beneficial effects: First, it can alleviate capital pressure caused by off-balance sheet assets reverting to the balance sheets. Second, it can facilitate business transformation and development. In fact, this has already begun. The Big Four Banks are preparing to open Wealth Management subsidiaries this year and their registered capital is expected to be RMB10-16 billion. Third, it can encourage growth as, in order to support the real economy, banks need more capital.

As far as external supervision is concerned, in order to meet domestic and international regulatory requirements, the Big Four have already begun to prepare for the adoption of `Total Loss-Absorbing Capacity’ (TLAC) regulatory standards. Last year, systemically important financial institutions in China were asked to meet a set of new stricter standards - the capital adequacy ratio should not be lower than 11.5 percent at the end of 2018. The tier 1 capital adequacy ratio and core tier 1 capital adequacy ratio should be at least 9.5 percent and 8.5 percent respectively. For all other banks, these three indicators were set 1% lower. Internationally, Global Systematically Important Banks (G-SIBs) or "too big to fail" banks, are expected to meet TLAC requirements and hence need to have diversified capital replenishment tools at their disposal, of which perpetual debt is a commonly used one. Starting January 1, 2019, the minimum TLAC requirement for G-SIBs is no less than 16 percent of a group's risk-weighted assets (RWA), with a six-year transition period to no less than 18 percent in 2022, which is stricter than their capital adequacy requirements. HSBC, Barclays and Deutsche Bank have all resorted to such bond issuances to meet the regulatory requirements.

Optimizing the capital structure of banks

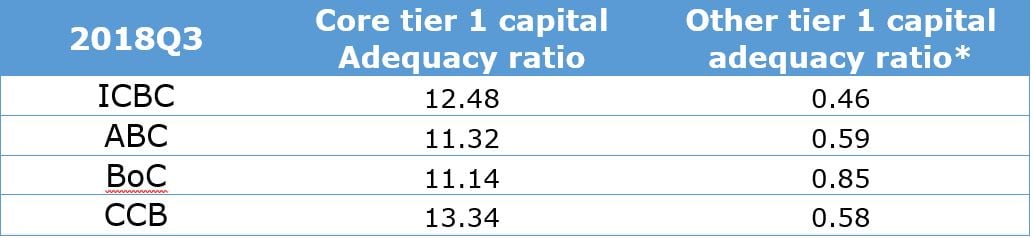

The use of perpetual bonds broadens the refinancing channels for banks, allowing them to increase the ratio of other tier-1 capital, optimize the capital structure and reduce costs. Compared with foreign banks, Chinese banks have very limited refinancing channels. At present, the tier-1 capital of 29 listed banks is almost same as their core tier-1 capital - namely, common stock with good capital quality but high cost. Other kinds of tier-1 capital only takes a very small proportion, around 0.68% at the end of the third quarter of 2018. Listed banks have previously relied heavily on the issue of preferred stock for capital replenishment. Compared with preferred stock financing, perpetual debt financing is much more flexible: First, all banks, listed or otherwise, can issue perpetual bonds; Second, the approval process is simple and the bonds are mostly issued in the inter-bank bond market; Third, banks may defer the payment of dividends according to their financial situation; and Fourth, losses can be written down or converted, as this kind of bond has both debt and equity characteristics.

Table: other tier 1 capital adequacy ratio of the Big Four is not high

Investment risks

Unlike the mature financial markets of Europe and the United States, bank issued perpetual bonds have just begun in China. As a new hybrid instrument of stock and debt, transaction and investment risks need to be closely monitored and evaluated.

The Chinese Central Bank is keen to improve liquidity through the use of perpetual bonds. For example, a new Central Bank Bills Swap has been set up and qualified perpetual bonds are included as collateral. Insurance and other financial institutions are also allowed to invest in perpetual bonds. However, investors should be mindful of the proliferation of liquidity and the risk of associated transactions within the financial system. It also remains to be seen whether markets will accept bank issued perpetual bonds with no fixed terms, multiple deferred interest payments and no interest rate jump mechanism.

In others word, more banks are now going to be able to use perpetual bonds as an instrument of debt financing to supplement tier 1 capital (Harbin Bank and China Minsheng have announced their bond issue plans), which can reduce the refinancing pressure in the secondary market and the pressure on the stock market. It is expected that the size of the bank issued perpetual bond market will grow at a rapid pace and may result in a flood of liquidity. Investors should focus on banks with good ratings and high capital adequacy.

Automotive

An unsettling year for auto dealers

Sometime in 2019, China’s auto dealers, devastated by massive stockpiles and worsening liquidity, are expected to endure a long and relentless reshuffle nationwide. The demise of dealerships will manifest itself in a growing number of store closures and frequent mergers and acquisitions. This reshuffle takes on greater urgency as a new sales model is set to shake up the industry.

Over the last few years, auto dealers have been experiencing shrinking profitability. The cooling economy as well as the unresolved trade tensions have largely dented Chinese consumers’ confidence who turned more cautious on purchase of big-ticket items in 2018. Unsold vehicle inventories greatly eroded dealer’s cash flows. Throughout the year, the vehicle inventory alert level was over 50% — the benchmark reading which indicates high inventory pressure.

Not only did dealers lose money on each car they sold, they were also hurt by high employee turnovers, resulting in huge financial losses for the dealers as good salesmen are essential to the business. It is estimated that more than two thirds of all dealers incurred losses in 2018. Among the remaining dealers, only 10% of them saw an increase in profits with respect to the previous year. We expect that underperforming domestic carmakers and joint ventures will be hit hardest.

Chart: Revenue and profit breakdown of dealer groups

In addition to worsening profitability, auto dealers have also to face internal and external risks. In fact, a lot of foreign OEMs are getting so wary of China’s growth prospects that a number of them have started lowering sales targets and downsizing sales networks in the hope of reducing costs and achieving higher operation efficiency. Last year, two prominent OEMs announced that they would combine their passenger and commercial vehicle sales networks by granting stores that used to sell only sedans and SUVs the right to sell vans and trucks. We expect that such mergers will continue to occur in 2019, but the biggest surprise could come in the form of a merger of regional sales networks (foreign carmakers normally collaborate with two local partners and establish separate networks to maintain a balanced development in the Chinese market).

The second threat to automakers comes from the emerging EV start-ups and the novel business model they take pride in which cuts out franchise dealerships. Most of the new carmakers have built up self-operating sales networks which take the form of a mobile app in combination with offline urban boutique stores that promise an omni-channel retail experience.

Direct sales are the ideal way for fledgling EV makers who are still at an early stage of development to sell their vehicles. This is because dealing directly with customers enables companies to provide a consistent brand experience to their customers. The direct sales model traces back to Tesla which pioneered this novel way of selling in the United States. With changing consumer needs and intensified competition, traditional OEMs are widely expected to re-examine the franchise dealership model and to create direct-to-consumer outlets (either online or through brick-and-mortar stores) in addition to their franchises in the next few years. Another source of competition is the emerging car-leasing platforms. Featuring leasing packages that lower upfront costs and downsized showrooms, these platforms have been attracting many new customers — from non-franchised retailers in rural areas where auto dealer groups rarely have any presence and instead wholesale vehicles to local retailers.

To make matters worse, online car sales platform Autohome has announced to increase the service charge for sales leads generation for auto dealers. Despite an industry-wide resistance, dealers with lower bargaining power and hardly any digital marketing campaigns will have to bear the burden of additional sales costs. A few OEMs have started equipping dealers with digital sales tactics to counter the rising cost of sales against the backdrop of an industry-wide reshuffle.

Energy

The creation of a behemoth

The establishment of a national natural gas pipeline company will set the tone for further gas price liberalization and accelerate the coal-to-gas transition. But one condition must be met - open and transparent access for everyone.

Pipeline giant on the cards

The long-awaited establishment of a national pipeline company is finally about to happen. The official plan is expected to be announced in the first half of 2019.

China's gas demand is forecast to rise 11.4% y-o-y to 308 billion cubic meters (Bcm) in 2019 according to a recent report from CNPC. A connected pipeline network will ease the infrastructure bottleneck and benefit the nation's coal-to-gas transition effort. Although no official plan has been announced yet, several alternatives are doing the rounds. The most popular approach to form the pipeline company contains three steps:

- Step 1: CNPC, Sinopec and CNOOC (the Big Three) divest their pipeline assets and transfer them to a new pipeline company. Ownership stakes of this company will be determined based on an evaluation of each party’s asset value.

- Step 2: State-owned and private investment capital should be allowed to invest in the construction of the new pipelines, lowering the combined stake of the Big Three to around 50%;

- Step 3: The pipeline company shall seek an IPO.

Open access

Creating a national gas pipeline company would be a major overhaul of China’s gas market as it would open the gas network to suppliers other than the current owners of the pipelines. The so-called third-party access could help smaller gas producers purchase available capacity on the pipeline network. Currently, China's gas pipelines are mainly operated by oil majors, who have been content to reap higher revenues from shortage-fueled price hikes to help offset losses from expensive imports of LNG and by limiting third-party access to their pipelines. Independent producers find it hard to get a foothold as the network is operated by their giant State-owned competitors.

Another issue is the mechanism for unifying gas quality and billing mechanisms. To address this issue, the National Development and Reform Commission issued draft regulations in August 2018 for the "Fair and Open Supervision of Oil and Gas Pipeline Network Facilities" that proposed an open access billing methodology using heat value rather than cubic meter based volumetric readings. But the final rules have yet to be issued due to reluctance to open access to third parties on the part of the three majors.

Getting ready

Unlike their western peers, most of China's oil majors have not signed a Take or Pay sales contract with the downstream gas purchaser to secure stable gas sales hence the entry of third-party gas sources will certainly make it more difficult to sell their own gas.

CNPC owns about 75% of China's pipeline assets. The spin-off will have a huge impact on its business. CNPC has been working on consolidating its natural gas sales companies to best utilize its current resources.

Sinopec's pipeline spinoff clears the very last hurdle for the IPO of its retail unit, which has been delayed as Sinopec first needs to put its crude and refined product pipelines at the disposal of the national pipeline company. But on January 16, China's State Council finally gave the go-ahead to Sinopec for an IPO of its retail business in Hong Kong.

Third-party participants will be able to rent long-distance pipelines and storage facilities in the years to come. This means they would be able to buy spot LNG cargoes from overseas markets when prices drop, deliver the cargoes to storage facilities and sell them when demand peaks in winter.

The separation of the telecom network from operators and the ensuing fee reform played a key role in the boom of China's internet sector. By the same token, the establishment of a national pipeline company signals that China's natural gas market liberalization is gradually coming of age.

Life Science & Healthcare

Battle of the checkpoint inhibitors

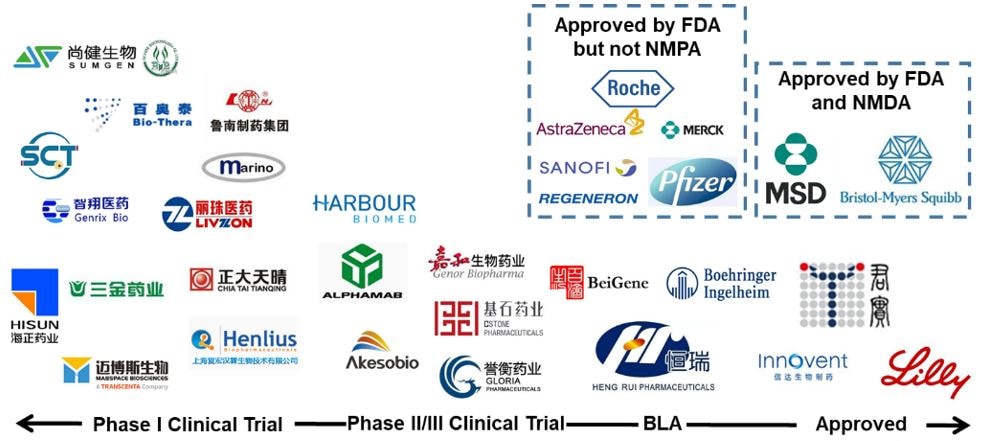

Anti-PD-1/PD-L1 drugs have become the most popular checkpoint inhibitors in the pharmaceutical sector. In the second half of 2018, the China National Medical Product Administration (NMPA) approved two Anti-PD-1/PD-L1 drugs made by multinational companies, namely Opdivo by Bristol-Myers Squibb and Keytruda by MSD. At the same time, towards the end of 2018, the PD-1/PD-L1 products of two domestic drug makers, Junshi Pharma and Innovent Bio also received approval. In addition, Baigene and Hengrui Pharma are also on the docket for approval. All of this indicates that the battle between multinational drug makers and domestic players in this area is heating up.

Figure: China Anti-PD1/PD-L1 drug landscape (By Jan 2019)

Indication coverage is the key to competition

As the Anti-PD-1/PD-L1 drug acts to block the cancer pathway, it does not specifically target any particular type of cancer and can hence be used for many different types of cancers. By the end of 2018, the FDA approved 17 indications for Opdivo and 15 indications for Keytruda. However, both drugs have only one approved indication in China, as do Junshi Pharma and Innovent Bio's products. This goes to show that product approval is only the first step in the game. To maintain their competitiveness in the field, players should focus more on indication coverage in the future, especially on those cancers with a big potential market such as lung cancer and digestive cancers. In addition, discovering how PD-1/PD-L1 can be used in combination with other therapies is also important.

Production capacity will be the key challenge

The complexity of biological drug manufacturing, the high cost of building bio drug production facilities and the lack of talent in bio drug manufacturing are key challenges for drug producers worldwide, and they are even more difficult for young Chinese innovative pharmaceutical companies who have few established facilities.

To better prepare for the challenges ahead, Chinese companies should seek solutions before the problems manifest themselves. For example, Beigene signed a commercial supply agreement with Boehringer Ingelheim in early 2018 to manufacture its anti-PD-1 product at the latter’s facility in Shanghai. Innovent Bio has also built a relationship of cooperation with Eli Lilly for the same purpose. In addition, Beigene and Innovent Bio are also expanding their own production plants for long-term purpose. Predictably, the implementation of manufacturing capacities will be the deciding factor of future competition for market share.

Price wars if market becomes crowded

Based on the currently disclosed prices, domestic products have a significant price advantage. Annual program fees of Opdivo and Keytruda range from RMB 150~200k while the annual fee of Junshi's product is priced at less than RMB 100k. Although there will be no direct competition due to the different coverage on indications in the short term, a price war seems inevitable in the long term as more products come to share the same indications and more new players enter the field. In order to cushion the potential impact of a price war on profits, multinational drug makers should start planning their medical insurance entry strategy as early as possible.