Analysis

2021 China LSHC Industry Survey Results: ‘State of Industry’

Published: February 2021

LSHC Industry 2021 Outlook Survey Framework

- Survey conducted between January 11th to 28th, 2021

- Engaged China based Pharma & Healthcare sector operators and investors: 150 respondents

(English version)

How did 2020 turn out…

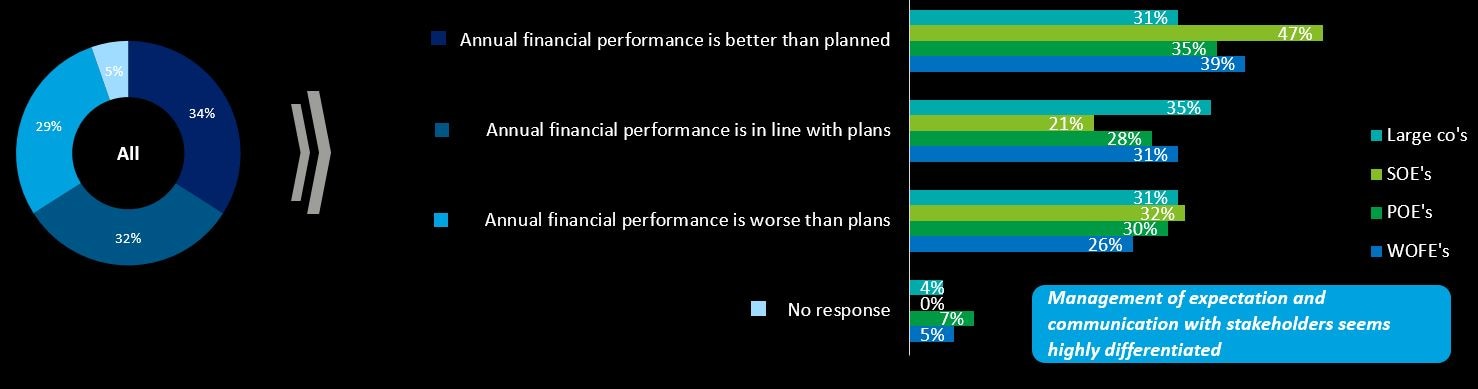

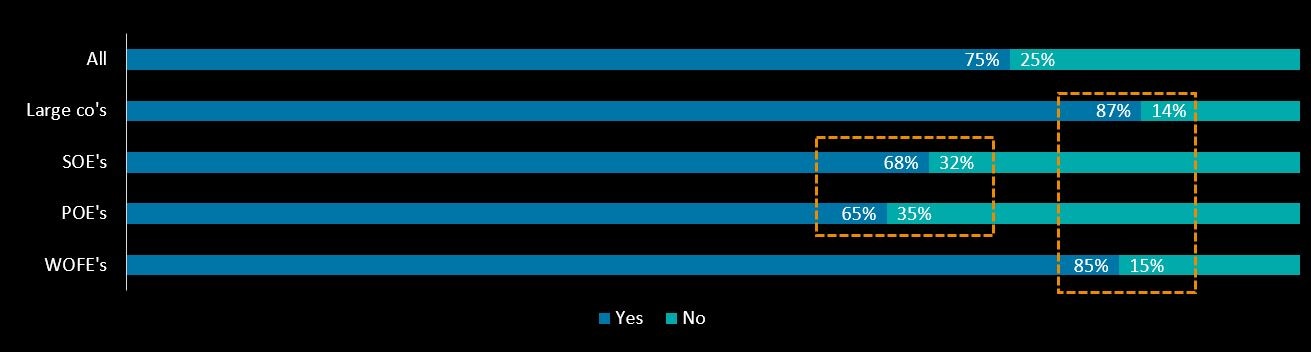

How did your company perform (top line) in 2020?

Insights

- Over 60% of respondents are still able to maintain the annual financial performance to be in line or better than the annual plan

- Only 26% of wholly foreign owned companies state that 2020 was worse than plans

- Nearly a majority of SOE’s (47%) state their annual financial performance was better than planned

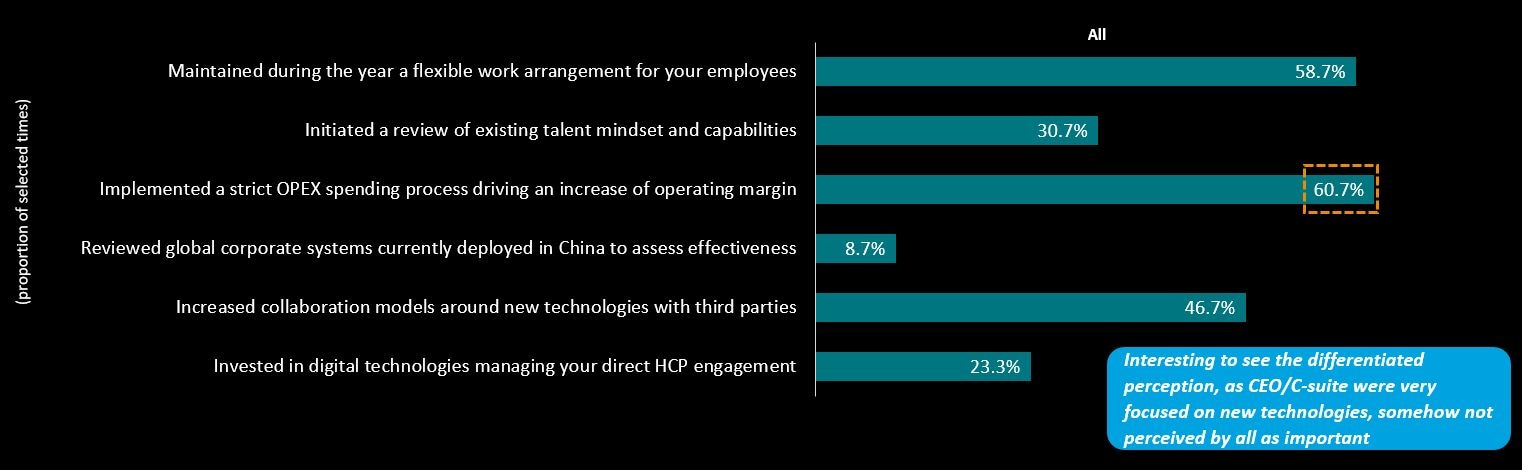

During the recovery, which were the key actions to manage the impacts of the Covid crisis?

Insights

- The top two key actions included a strict OPEX spending process maintaining flexible work arrangements

- As expected flexible work arrangements were implemented by all throughout the year (in line with snapshot survey in 2/2020)

- Larger Companies focused on OPEX spending controls to protect their bottom line profits

- Collaboration initiatives around new technologies were top in mind, and more so for CEO/C-suite from WOFE who ranked this 2nd with 67%

- Global system deployment efficacy was not top in mind during Covid-times

- Investment in commercial & marketing digital technologies varied significantly across the respondents

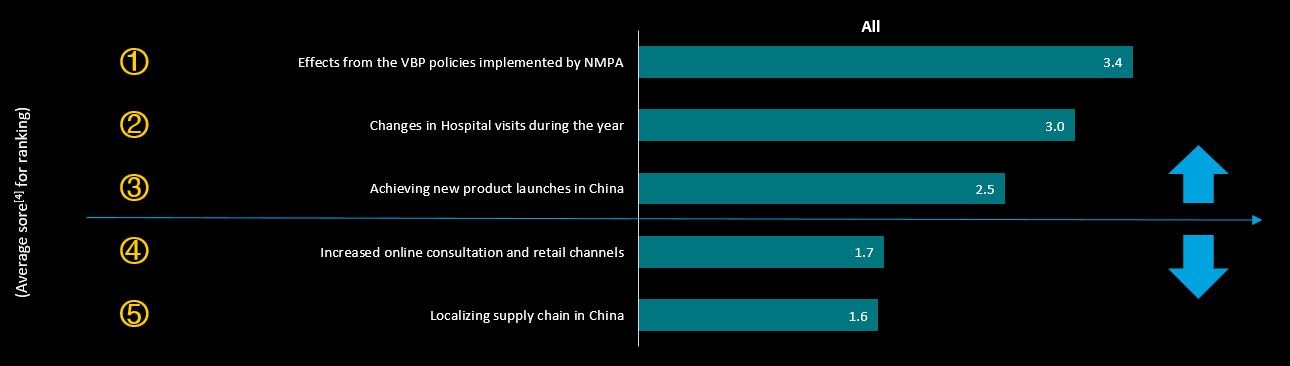

Your 2020 business performance was mainly impacted by? (ranking of importance)

Insights

- The VBP policies & implementation is the top impacting factor to all respondents

- Regulatory related (VBP), hospital visits (main promotion channel) and keeping new product launches on track were top three factors on commercial impact

- Online channels and reviewing supply chain structures were considered as a much lesser importance

- Product launch was viewed by the larger co’s and foreign pharma’s as key to their business performance in 2020

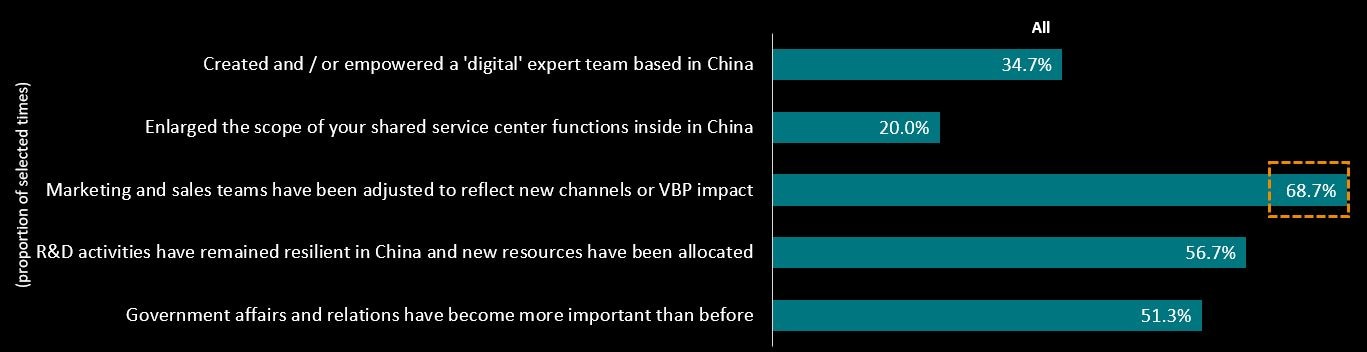

Within your organizational & business model which are the key changes implemented in 2020?

Insights

- As expected and anticipated, marketing & sales teams remained a focus as VBP changed the engagement needs

- R&D capabilities and GA’s teams have been even more important than before

- While the industry is embracing its ‘digital revolution’, only 35% of respondents have cited this a focus in 2020

Considering China's very specific data and security environment, have you done any of below implementations?

Insights

- Around half of all, except POE’s, have allocated more than expected resources in IT & data compliance framework

- A majority of large co’s and WOFE’s will allocate more resources in 2021 in the IT & data security and compliance development in response to the rapid growth in digital healthcare in China

- For POE’s and SOE’s, resource allocation in IT security development seem of a lesser business priority (2020 and 2021)

Online/internet business channel plays critical role during the crisis period, does your company consider to increase investment on these new channels?

Insights

- 75% of respondents are investing or willing to increase the investment in the online channel development

- Willingness in increasing the investment into online/internet channels among POE’s and SOE’s is significantly lower

- All types of respondents that are more willing to invest through both self-development and collaboration, especially large co’s

- In comparison, domestic players have a stronger intention in build the online channel with their own capability, while WOFE’s are more into the co-development mode

How might 2021 turn out…

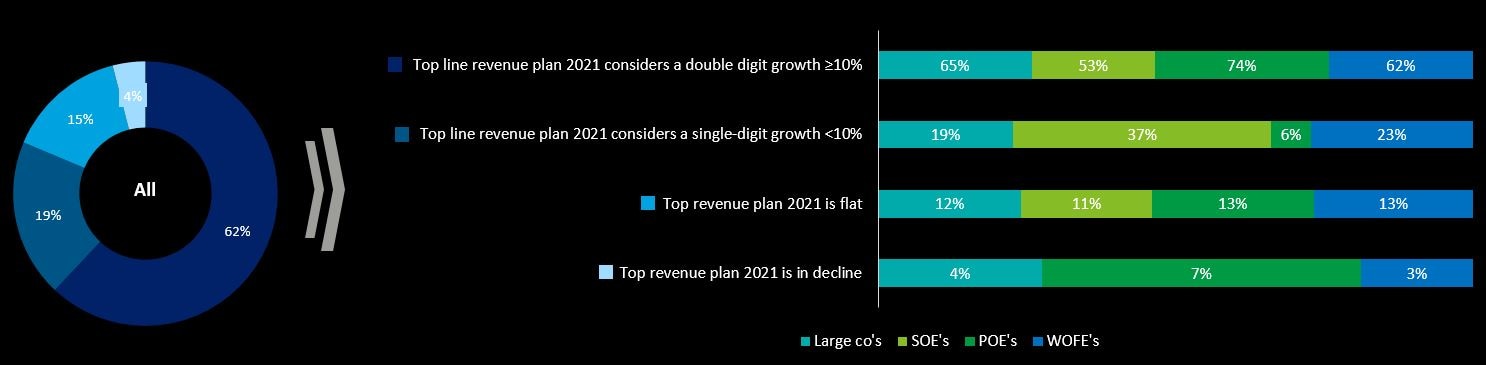

How do you foresee the Covid pandemic on your China business outlook?

Insights

- A large majority (62%) see a rather bright outlook and forecast a ≥ 10% growth in 2021 (only 19% see no growth or decline in 2021)

- POE’s have the most ambitious outlook, while a total of 85% of WOFE’s expect growth

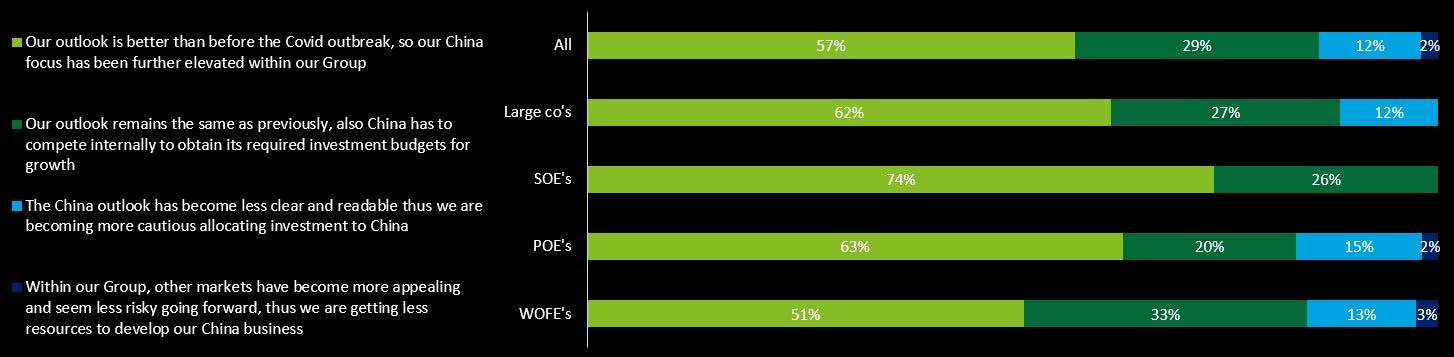

Has your overall business and portfolio strategy changed for China in the next 3-5 years?

Insights

- A majority (57%) has a better outlook in China market and may further elevate the China focus

- SOE’s are having the most optimistic attitude and aggressive in elevate the China focus and followed by POE’s, expecting further local preferential policies to be published in 2021 and onwards

- Only a very small group (2% = 3 respondents) considers the China market to be less attractive going forward

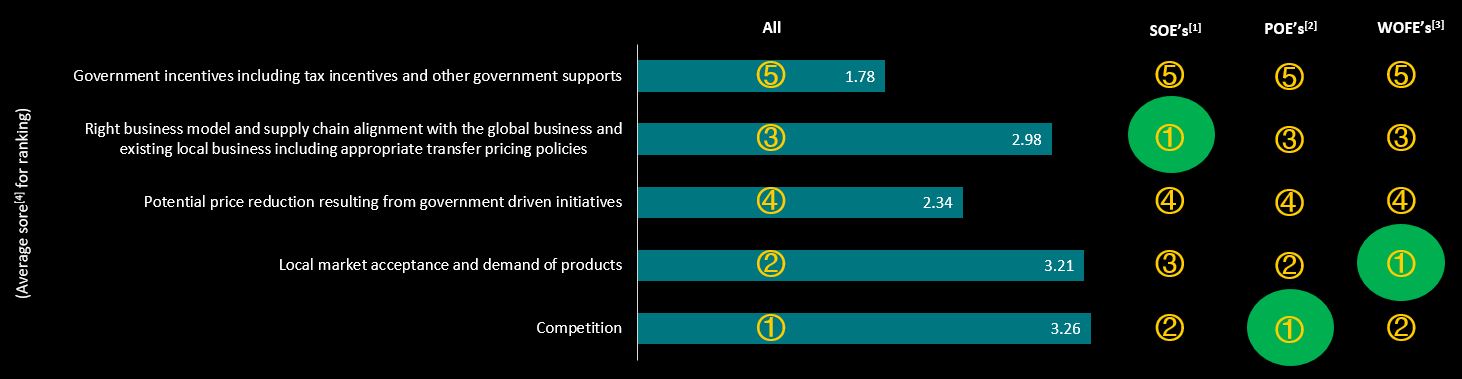

What do you think are the most relevant considerations from your perspectives when introducing new products into China?

Insights

- Overall, the competition in China market is the top consideration to all respondents, along with local demand & market acceptance

- SOE’s highlight a particular need for supply chain arrangements and eventual global dependency

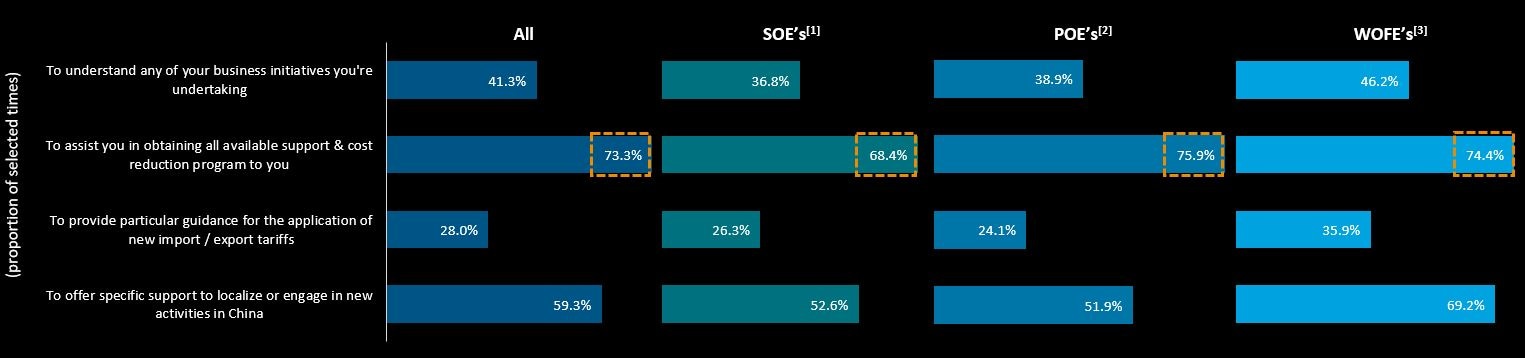

Have government administrations increased their engagement to…

Insights

- Very consistent views on government administration support across all respondents

- WOFE’s perceive a specific push to further review localization and engage in ‘new activities’

- The import & export tariffs application guidance from the government seem to take relatively less attention from all

With China's dual circulation strategy, do you expect that…

Insights

- With the government’s purpose in bring up more innovation and first-in-class products in China, the new drug registration and market access timeline are expected to be further shorten and accelerated under the dual circulation strategy

- The dual circulation strategy is also expected to bring a more frequent and boarder coverage of VBP implication and NRDL updates which will further eliminate products that are unable to offer a lower price

- All industry respondents are sharing the similar expectations, POE’s are slightly more expecting in the preferential treatment

- WOFE’s are also having a higher expectation in further regulatory & government measures to impact the industry

Key Insights and Outlook

From 2020 to 2021…

Government involvement will continue to increase speeding up domestic innovation and competition, to the benefit of Chinese patients

- Potentially a more frequent and boarder practice of VBP and NRDL coverage, the market will become highly centralized, also pricing strategies and cost controlling will become even more important in the future.

- Outward looking scenarios planning with high agility will be a key for success for all players.

New business models and digital technologies will make Chinese patients to become highly engaged well-being focused consumers

- With the covid-19 outbreak, business models are changing and the adoption of digital channels has accelerated, thus blurring the lines between ‘consumers’ and ‘patients’.

- Collaborations between LSHC companies and third parties, such as technology companies, are popping up, thus requiring adjusting skills & mind sets of existing teams.

- IT innovation and data security will become a higher priority ever than before.

China’s market will continue to grow faster than most mature markets and will be impossible to be ignored

- The government is aiming to promote local first-in-class products over me-too/me-better, and we are seeing more relevant policies and initiatives in supporting the domestic players.

- Many domestic players are enhancing their R&D and product portfolio through partnering, and seeking for more preferential policies to be announced in 2021.

- Looking towards a long term sizable market too large to be ignored, foreign players have started to further develop a China-centric market access and pricing strategy, meanwhile proactively in looking for local support from the government affairs and relation enrichment.

Note: [1] Large co’s companies with revenue above 5BRMB; [2] SOE: State-owned Enterprise; [3] POE: Private-owned Enterprise; [4] WOFE: Wholly foreign-owned enterprise