The Future of Power in Europe

The classic utility is back

European Climate Law sets a legally binding target of climate neutrality by 2050 with an intermediate target of reducing greenhouse gas (GHG) emissions by at least 55% by 2030. This implies a massive transition from the current fossil-based and carbon-intensive energy system to a low-carbon system with strong electrification of many traditionally oil- and gas-fueled processes. This will require huge investment in new renewable generation capacities, well in excess of the current installed base, as well as reinforcement of the European power grid and decommissioning of a multitude of carbon-intensive assets. While many utilities since the 2010s have been pursuing asset-light strategies based on network operations, market services, and retail business, without necessarily dipping into their generation assets, the ambitious climate targets are going to revive the traditional organization of European utilities based on long-term power-asset investment. Such investment needs to recognize the risks and understand the future structure of the energy system and the associated energy markets in which the companies will compete.

Scenario-based analysis of the plausible futures of the European power system

Derived from a scenario-based modeling approach, this study aims to identify the characteristics of the future European low-carbon power system (up to 2050) by clarifying the challenges and risks that utilities face, and suggest best practices for reviving the asset-intensive business model and making it future proof. First, future scenarios for the entire power system are anticipated qualitatively, then these scenarios are enriched by employing Deloitte’s in-house European electricity market model (DEEM) and a common European narrative curated by a team of Deloitte subject-matter experts who form part of the Energy and Resources practice in Europe.

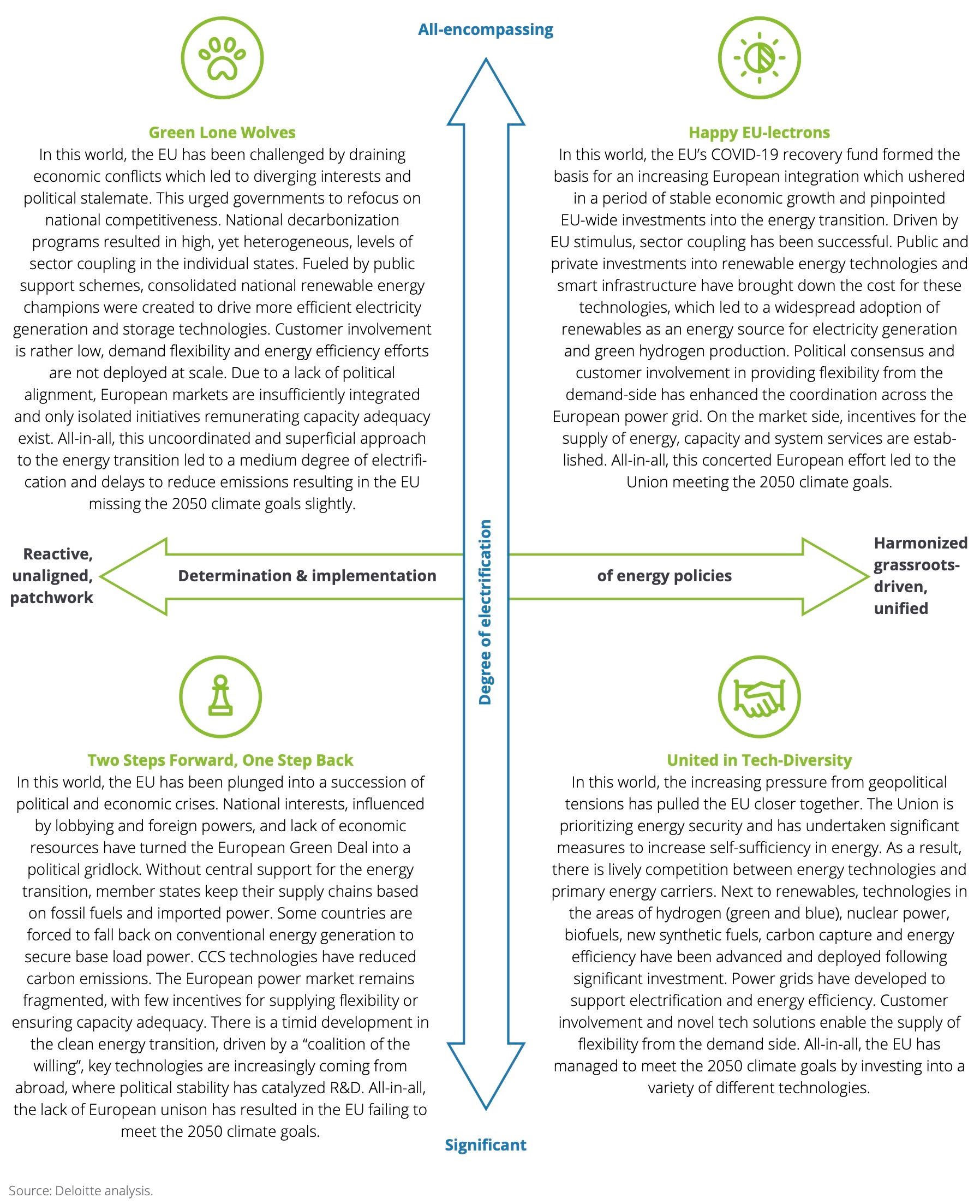

They identify four main future scenarios with varying degrees of electrification and political determination with respect to climate goals. The spectra identified range from “reactive” to “unified” with regards to political determination, and from “significant” to “all encompassing” with regards to electrification level (Figure 1):

Happy EU-lectrons: The first scenario is one in which collaboration and investment at the European level achieves rapid decarbonization. Additional EU stimulus investment facilitates electrification and sector coupling. Thanks to learning by doing, the costs for renewables fall steeply, as well as for green hydrogen production, which increases the rate of adoption overall. Coordination within the cross-border European power grid is optimized due to higher decentralized renewable production, as well as demand-side flexibility adoption. By 2050, the EU will meet its climate goals.

United in Tech Diversity: In this scenario, the EU makes energy security and self-sufficiency its fundamental priorities. Non-electricity energy carriers play a competitive role in the energy mix next to renewables. Investment goes to all low-carbon technologies: clean hydrogen, nuclear power, renewables, biofuels, synthetic fuels, carbon capture, and energy efficiency. The EU achieves its climate goals by 2050, despite lower electrification rates than in the Happy EU-lectrons scenario.

Two Steps Forward, One Step Back: In this scenario, reacting to external and internal pressure in the COVID-19 aftermath, countries increasingly prioritize their own national interests and abandon the EU Green Deal. This slows down the energy transition, with supply chains retaining a large part of their fossil base. CO2 emissions are reduced by developing carbon capture and storage technology. But fragmentation and a lack of unified European initiatives result in a failure to meet climate goals by 2050.

Green Lone Wolves: In this scenario, the EU has been challenged by draining economic conflicts and crises that result in an “every country for itself” dynamic within the EU. Nevertheless, the national decarbonization initiatives still achieve a high level of electrification and successful sector decoupling. Although renewables are developed and deployed in several countries, customer participation is low, and a lack of political alignment hinders their market integration and slows down potential efficiency gains. As a result, the EU misses its 2050 climate goals by a slight margin.

Needed investments and capacity expansion

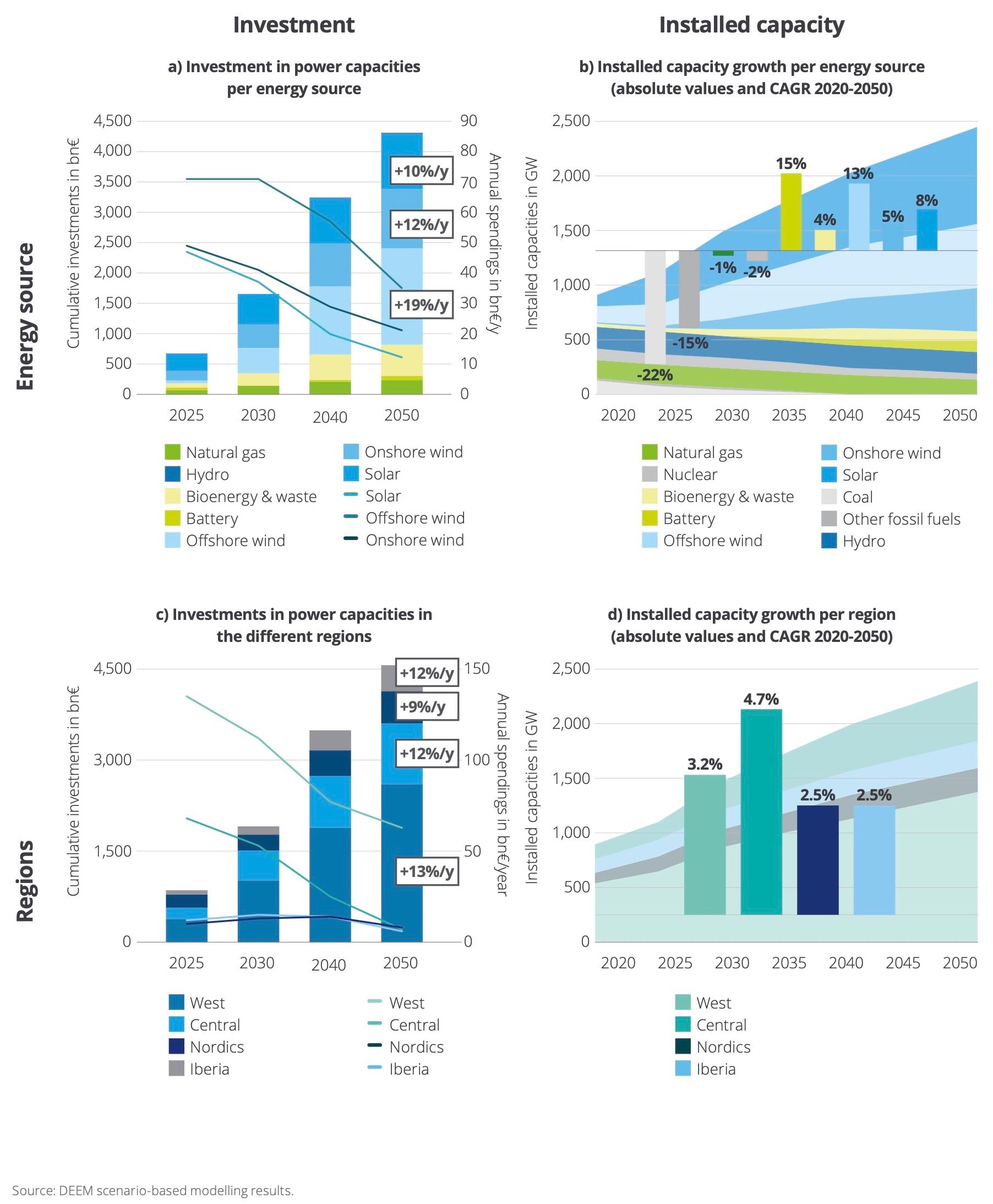

Happy EU-lectrons is the scenario for ideal policy development, international cooperation, and a highly electrified and unified European power market. Such a scenario results in strong development of renewables, storage options, and cross-border interconnections (Figure 2). Offshore and onshore wind attract the highest investments (over €70 billion/year and €45 billion/year by the late 2020s), with annual average growth of 19% and 12% between 2020 and 2050, respectively. Wind-power technologies are followed by solar power (€40 billion/year by the late 2020s) with annual growth of 10% over the same period. The capacity increase however is led by solar power (from 280 GW in 2025 to 860 GW of installed capacity by 2050), followed by onshore and offshore wind (from 200 GW and 20 GW in 2025 to 580 GW and 350 GW of installed capacity by 2050, respectively).

As to the geographical decomposition of the investments, growth in renewable energy investments is led by Western Europe with an annual growth rate of 12.5% in the period from 2020 to 2050, followed by Central Europe (11.6%). However, the installed capacity of renewables grows fastest in Central European countries (4.7%/year) between 2020 and 2050, followed by Western Europe (3.2%).

The Happy EU-lectrons scenario is not the only possible future

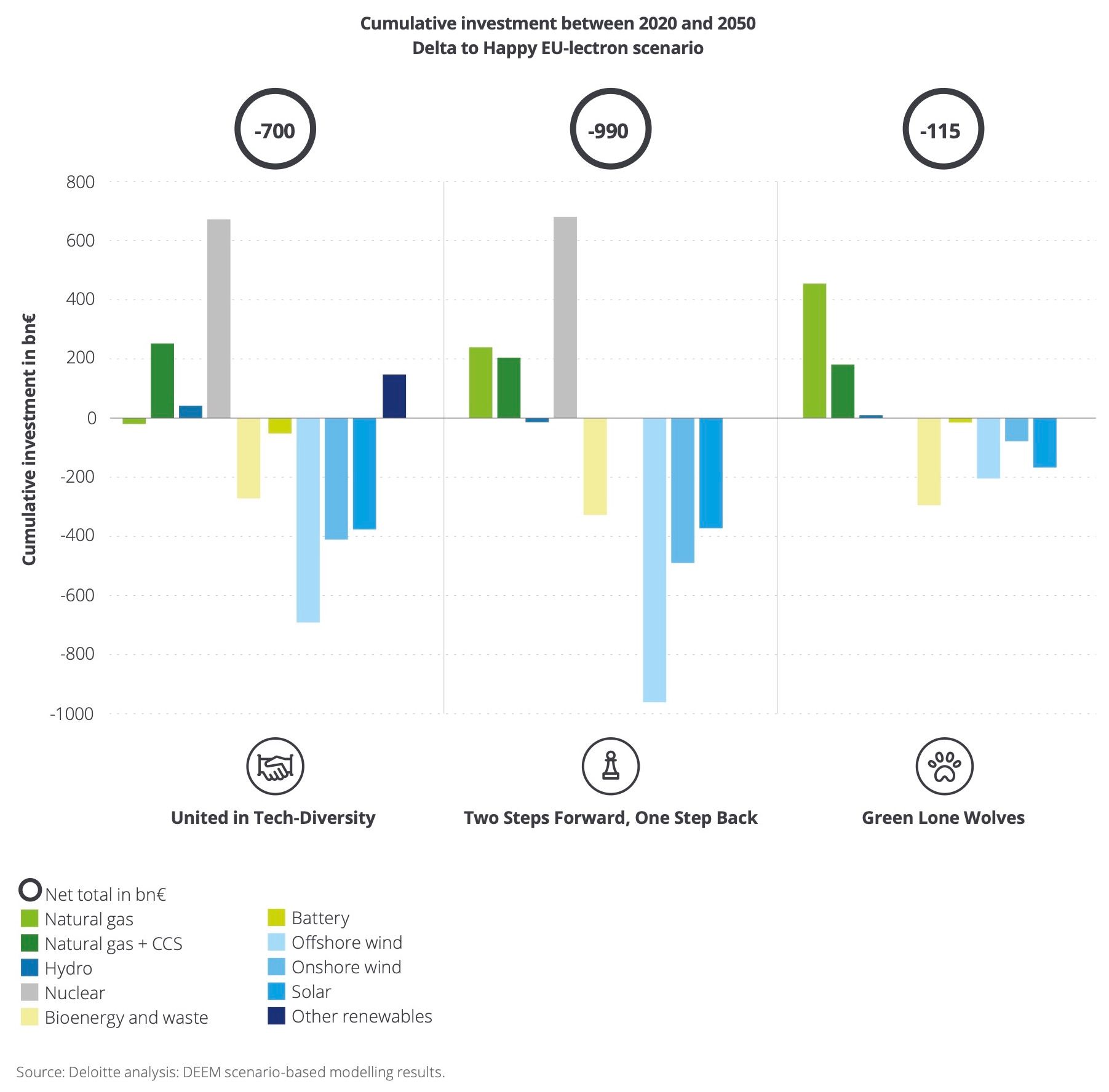

The Happy EU-lectrons scenario is associated with a massive increase in interconnection capacities, rapid electric-vehicle roll out, significant green hydrogen production, and ambitious CO2 pricing. This scenario is a fascinating vision for many. But it may not be the most likely, nor the most desirable. Investment in renewables in the Happy EU-lectrons and Green Lone Wolves scenarios is on par, yet the Two Steps Forward, One Step Back scenario shows a €1 trillion lower investment. None of the two latter scenarios achieve the emission-reduction levels required to stay in line with the European climate goals. Another scenario consistent with climate goals is the United in Tech Diversity scenario, which is underpinned by lower renewable development and electrification, but the same levels of emission reductions. This scenario requires lower investment in the power system as well (Figure 3).

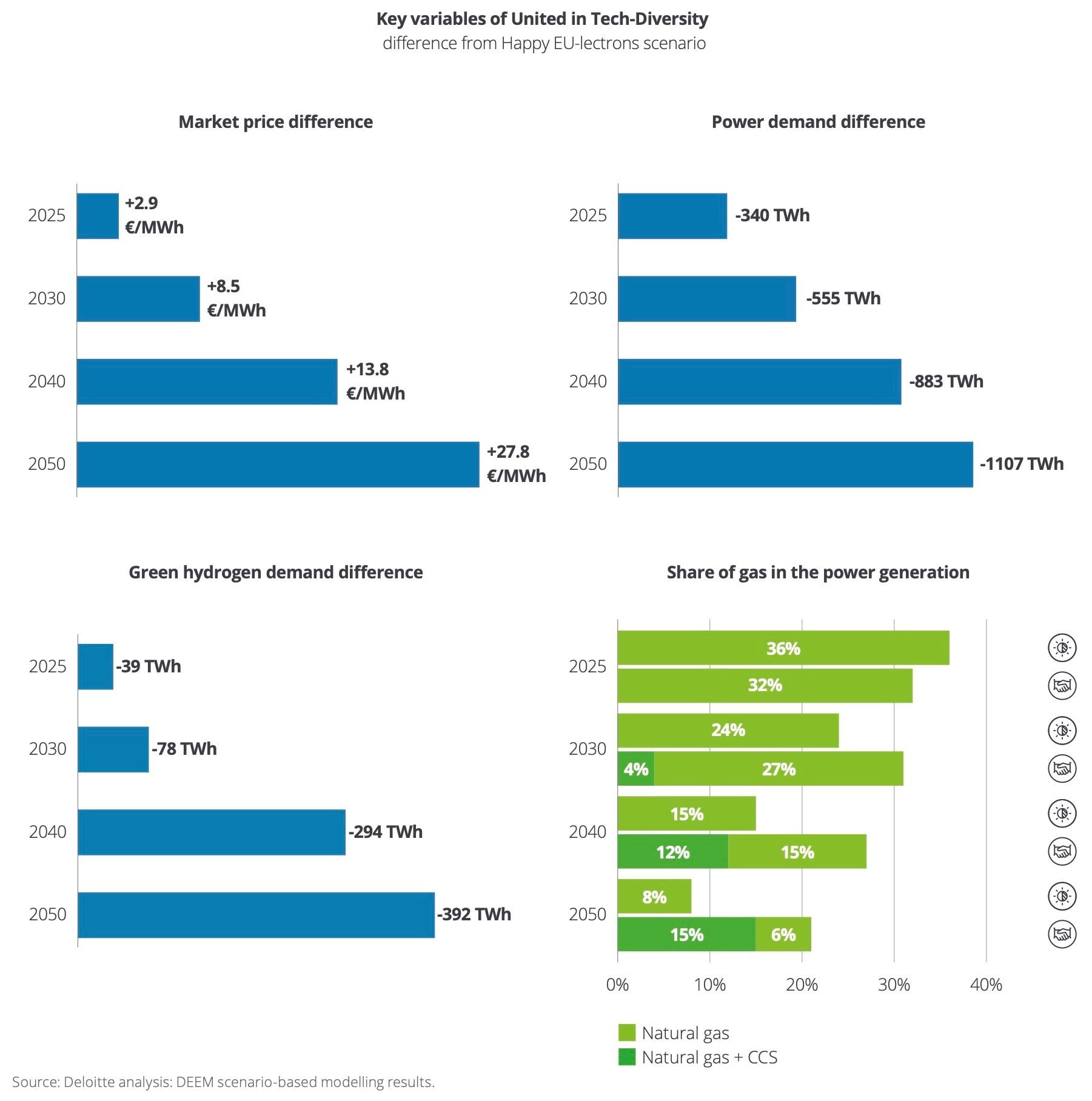

The lower power-system investment in the United in Tech Diversity scenario vis-à-vis the Happy EU-lectrons scenario does not necessarily mean that unit electricity cost and the electricity price of this scenario are lower, since electricity demand is also lower. In fact, such a future will lead to higher electricity market prices compared to Happy EU-lectrons (on average nearly €28/MWh higher in 2050), since power generators must procure costly natural gas to run the combined cycle gas turbines (CCGT) with or without CCS (Figure 4). This effect persists despite lower power demand due to less electrified end uses and lower demand for green hydrogen from industry.

To sum up, there are some obvious losers, winners, and question marks when it comes to investment in energy generation. The winners are clearly variable renewables: solar PV and onshore and offshore wind. The clear loser is coal, while the big question mark hangs over the future role of nuclear, bioenergies, and natural gas with or without CCS. In particular for natural gas combined with CCS, we see the highest relative variance of all major technologies.

Back to the future

It is certain that the European power system is set to grow. Whatever the scenario, huge investment is needed in the future European power system (notably in renewables) to stay in line with the bloc’s climate goals. Uncertain is the magnitude of this growth, which creates a multitude of uncertainties for the industry.

The power industry needs to organize for asset-intensive growth. This largely depends on retaining operating licenses, especially through credible environmental, social, and governance (ESG) tracing criteria and continued access to low-cost capital, as well as disposing of the best sites for renewable energy generation. Hourly electricity prices vary significantly in a highly renewable power system. This price volatility provides strategic market opportunities for new actors such as demand-side flexibility providers (load-shedding and load-shifting), thus improving the viability of their future business models. Utilities must prepare by investing in such technology. The most important challenge is probably the change required to assure supply-demand equilibrium and transport power in the future European system. This will require significant investment in digitalization of processes and in smart network operations. In summary, utility executives should embrace scenario thinking when developing their strategies and planning their investments so as to prioritize critical skills and capabilities. Decision makers should make sure that this strategy is flexible enough to adapt to changes that require constant monitoring of key scenario parameters.

Contact

Bernhard Lorentz

Managing Partner Deloitte Sustainability & Climate GmbH

Global Consulting Sustainability & Climate Strategy Leader