The global economy: Set to hit the gas, yet wary of roadblocks has been saved

The global economy: Set to hit the gas, yet wary of roadblocks

29 January 2018

Ten years since the recession, we take a look at how the global economy is faring. Economic activity seems to be strong, driven by trade growth, easy monetary policies, and positive consumer sentiment. However, risks—in the form of high household debt, increasing uncertainties due to geopolitical events, rising protectionist rhetoric, and a move away from a multilateral trading order—could derail the current growth story.

Introduction

The end of this year will mark a decade since the world economy was sucked into a downward spiral that was initially sparked by risky mortgages in the United States. That originating crisis, however, was not the only challenge that emerged in the intervening years. The world experienced Europe’s debt crisis, emerging markets’ vulnerability to volatile capital flows, oil price fluctuations, and geopolitical events such as the Arab Spring and Brexit adding to the uncertainty. The tide, however, seems to be turning of late, especially since last year when the world economy packed quite a punch. According to estimates by the International Monetary Fund (IMF), global real GDP grew 3.6 percent in 2017, the fastest pace in five years.1

With economic activity gathering pace on both sides of the Atlantic and the Asian growth engine ploughing ahead along the Pacific Rim, the global economy seems poised for a strong head start this year. It would, however, be foolhardy to imagine a world without risks. Increasing private sector debt levels, geopolitical risks, and rising protectionist rhetoric may still play spoilsport.

International trade beats the odds

If there is a protagonist in the global growth story of 2017, trade beats the others hands down. According to the IMF, the total volume of global exports is estimated to have grown by 4.1 percent in 2017, up from 2.3 percent in 2016.2 This was the fastest growth in exports since 2011 and the first time in three years that exports growth outpaced global GDP growth. Asia has been a key contributor to trade growth since late 2016, with European economies also joining the trade bandwagon last year (figure 1). Germany, for example, recorded double-digit exports growth in Q3 2017 for the first time in eight years.

Strong growth in international trade also reveals a high degree of resilience despite uncertainty about trade and investment relations, and rising protectionist rhetoric. Asian economies, for example, are increasingly trading with one another, taking advantage of growing demand within the region.3 Similarly, withdrawal of the United States from the Trans-Pacific Partnership (TPP) has not shaken the resolve of the remaining 11 nations to continue with a trade pact, albeit on a smaller scale. And in a shot in the arm for these nations, the United Kingdom has evinced interest to join the TPP as it tries to offset trade losses arising from Brexit.4 This may encourage other non-Pacific nations to follow suit.

Low inflation and easy monetary policy will likely aid growth

Developed economies continue to benefit from accommodative monetary policy. The balance sheets of the central banks of four major economies―the United States, Euro Area, the United Kingdom, and Japan—alone have quadrupled from pre-crisis levels to reach almost $16 trillion, approaching 20 percent of world GDP.5 Despite four policy rate hikes in the United States, the Fed’s interest rate path has been gradual and will likely remain so in 2018.6 In the Eurozone, the European Central Bank (ECB) has been at the forefront of the fight against yields, thereby easing the fiscal pain for debt-ridden economies. Key emerging economies have also eased policy in recent quarters; Turkey and Mexico are notable exceptions.

Higher global liquidity and easy monetary policy have aided credit growth with emerging economies outpacing developed ones (figure 2). A likely reason for the surge in emerging economies is large portfolio inflows from developed economies in search of higher earnings, thereby aiding in the sharp rise in corporate and household credit in the latter.

Accommodative monetary policy could not have been possible without low inflation (figure 3). While subdued energy prices have kept inflation in check in recent years, structural issues, such as muted wage growth in advanced economies and slow productivity growth across the world, have also kept the lid on consumer prices.7 With the inflation outlook expected to remain subdued in the near term, especially in advanced economies, central banks there will likely maintain a relatively accommodative stance despite moves to normalize interest rate paths.

Strengthening labor markets add to positive sentiment

Consumers—a key contributor to economic growth—appear upbeat across economies, buoyed by labor market strength, subdued inflation, and low borrowing costs. For instance, consumer sentiment in the United States (as measured by the Conference Board’s consumer confidence index) is now at its highest level since 2000, and consumption spending has grown faster than income since 2016.8 Sentiment has also improved in Europe, where unemployment in high-debt economies has fallen from their peaks of 2012–2013. This revival is most prominent in Spain, Ireland, and Portugal, while Italy and Greece still have much work to do (figure 4). Even in Japan, which has been struggling to shrug off deflationary pressures for years, consumer confidence has been slowly improving over the past year and is now at its highest level since 2013.9 In emerging economies, continued economic growth, along with cheap access to credit, has aided consumer sentiments and, hence, spending.

Businesses couldn’t have asked for more

Strong economic growth, improving labor markets, low inflation, and positive consumer sentiment have created the perfect scenario for businesses to prosper. Indeed, businesses are more optimistic about the future. According to Deloitte’s Q3 2017 Global CFO Signals, finance leaders responding to the 17 surveys across several regions seemed optimistic across several measures.10 Similarly, business confidence within the Organization for Economic Cooperation and Development (OECD) is on the rise and reached record-high levels in late 2017 (figure 5).11

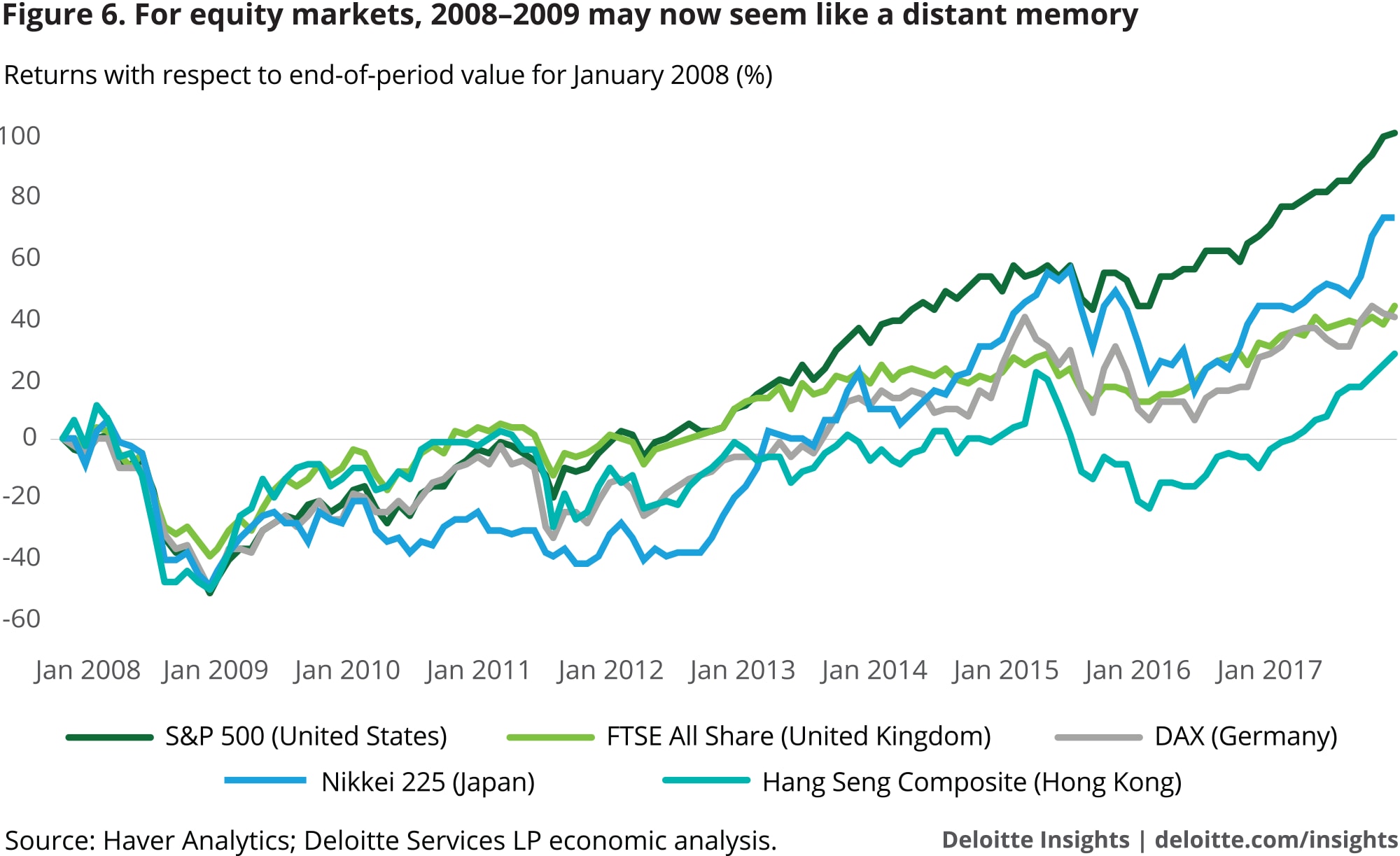

Greater optimism is also evident in financial markets (figure 6). Key equity markets have either started the new year with a new peak (United States, Germany) or are finding their way there (Japan, Hong Kong). Upbeat businesses sentiment is good news for investments, which continues to be a drag on some economies. In Brazil, for example, investments grew for the first time in three years in Q3 2017. In the Eurozone, spending on machinery and equipment has been improving after suffering much in 2012–2013, thereby aiding economic activity. In addition to greater optimism, businesses may feel encouraged to invest more due to widespread expectation that corporate profitability will improve and the labor market will strengthen further.

Foolhardy would be the policymaker who ignores risks

It would be a dampener to talk about risks when key indicators are hinting at a continued uptick in economic activity. But, of all things history offers insights to, risks would be foolhardy to ignore. An elongated period of loose monetary policy and strong growth in consumer spending in emerging economies have led to a rise in leverage. The surge in non-guaranteed private sector credit particularly stands out. Over 2000–2016, private sector non-guaranteed long-term outstanding debt grew at an average annual rate of 11.0 percent, much higher than the corresponding 6.5 percent rise in the debt of private creditors with public guarantee.12

In the Asia-Pacific region, the credit binge since 2008 is most evident for households. For many economies in the region, household debt as a share of disposable income is now higher than what it was in the United States prior to the outbreak of the Great Recession (figure 7).13 Worse, high household debt has links to real estate cycles, something that Canada, Australia, and several economies in Asia (including China) have witnessed in recent times.14

High household debt is not the only risk weighing on policymakers this year. Normalization of monetary policy by the Fed and ECB may reverse capital flows into emerging economies, thereby denting their exchange rates and external borrowing costs. According to the IMF, raising the policy rate and shrinking the balance sheet in the United States alone will likely reduce portfolio inflows by about $70 billion over the next two years.15 Any slowdown in China poses another risk—with debt levels rising in the country even as it turns more to domestic drivers for growth, any dip in economic activity might have implications for global commodity prices, demand for key Asian exporters, and global financial stability.16

Adding to the list of concerns is rising protectionist rhetoric and a move away from a multilateral trading order. While there is a question mark hanging over the North American Free Trade Agreement as we know it, negotiations for a smooth Brexit have suffered in recent days.17 Businesses are therefore in uneasy terrain. Should manufacturers move factories? Will financial services in Europe relocate away from London? Who should retailers bank on: the tried-and-tested US consumer or the happy spender in Asia? For businesses, adding to the discomfort will be technology-related disruptions and rising geopolitical risk in the Korean peninsula and the Middle East.

The embers of such fires, if they were to burn, will be felt much beyond the regions themselves, spurring a vicious circle of economic and financial woes. A big casualty, as history again teaches us, would be the current global economic revival. Economists, as always, will be hoping that cool heads and warm hearts prevail.