Navigating toward a new normal: 2023 Deloitte corporate travel study has been saved

The authors would like to thank Stephen Rogers and Sanjay Vadrevu for their contributions to this article.

Cover image by: Sofia Sergi

United States

United States

United States

United States

By many measures,1 leisure travel in the United States and Europe reached pre–COVID-19 levels months ago, after following consistent upward trends since the rollout of vaccines in early 2021. Corporate travel, however, has been slower to return. Decisions about these trips face an entirely different calculus, accounting for a host of factors: traveler safety and willingness to board a flight, client interest in meeting in person, the value of attending a conference, and whether a virtual conferencing platform can replace the trip—just to name a few.

The second half of 2022 was affected by competing forces: On the one hand, the world had spent several months past the peak of pandemic concern, which helped pave the way for the growth of corporate travel. The United States dropped prearrival testing for most foreign visitors in June, several months after Europe. But as the year wore on, concerning economic signals continued. From a background of concern about looming recession, layoffs emerged, affecting the tech sector most acutely.2 In March 2023, financial concerns were compounded by issues in the banking sector, the trajectory of which were uncertain at the time this report was drafted.

As professionals have started to put more trips on their itineraries, many are encountering higher airfares and room rates. These pricing conditions fit awkwardly both with travel buyers’ seemingly cautious financial approach and with many travel suppliers’ widely reported staffing challenges and slow infrastructure updates.

As Deloitte continues to study the future of corporate travel, we are watching the following key trends and developments:

This report draws on a survey of 334 travel managers, executives with various titles and travel-budget oversight, fielded from February 7 to 23, 2023. The survey reached 106 US-based respondents, and 228 European respondents based in the United Kingdom (56), Germany (57), Spain (59), and France (56).

Beginning in 2020, many public companies began sharing various figures related to the strength of corporate travel demand. Deloitte’s estimates and projections rely on the spend figures shared by respondents to our survey.

We would like to note that: 1) there is no reporting standard for corporate travel volume; 2) reported metrics are inconsistent across companies and usually represent a portion of corporate versus the whole (i.e., domestic versus international; passenger revenue versus flown segment, business transient versus group); 3) due to a significant share booked outside of corporate booking engines, suppliers may lack full visibility into corporate volume; 4) developments in travel and work patterns have made accounting for business versus leisure travel more challenging.

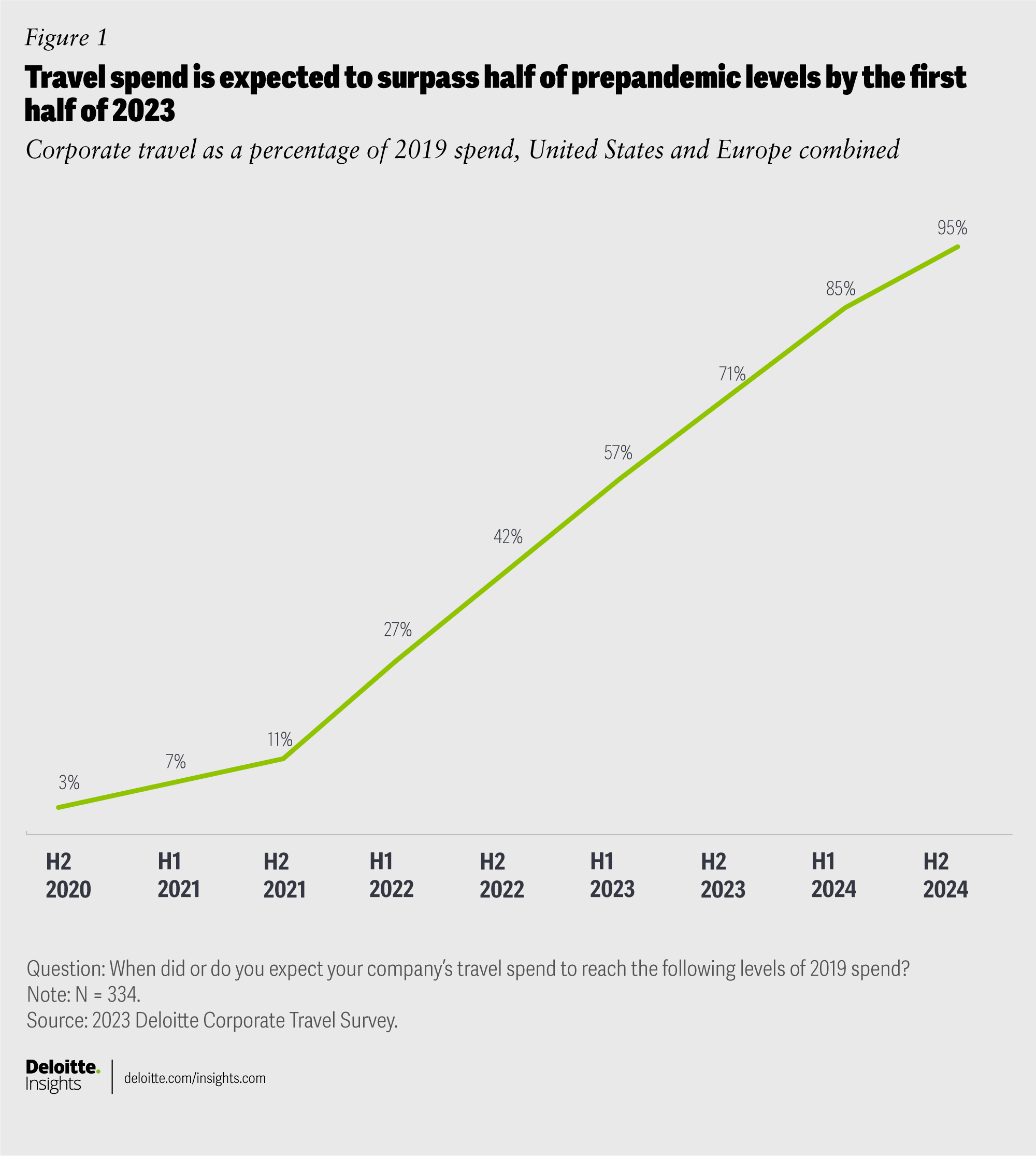

Corporate travel made major strides in 2022. After concerning COVID-19 variants and the outbreak of the Russia-Ukraine conflict set the year off to a rough start, business leaders decided the time was right to reconnect. Accordingly, travel grew roughly twofold from the beginning to the end of the year (figure 1). Spend across the United States and Europe is expected to shoot to 57% of 2019 levels in the first half of 2023, and surge to nearly three-quarters of the prepandemic mark by the end of the year.

While full recovery to 2019 levels appears possible by late 2024, accounting for inflation would leave the corporate travel market between 10% and 20% smaller in real terms than it was prior to the pandemic. Growth in 2023—and likely 2024—will come in an environment of higher airfares and room rates, meaning that the number of trips will likely still lag further behind.

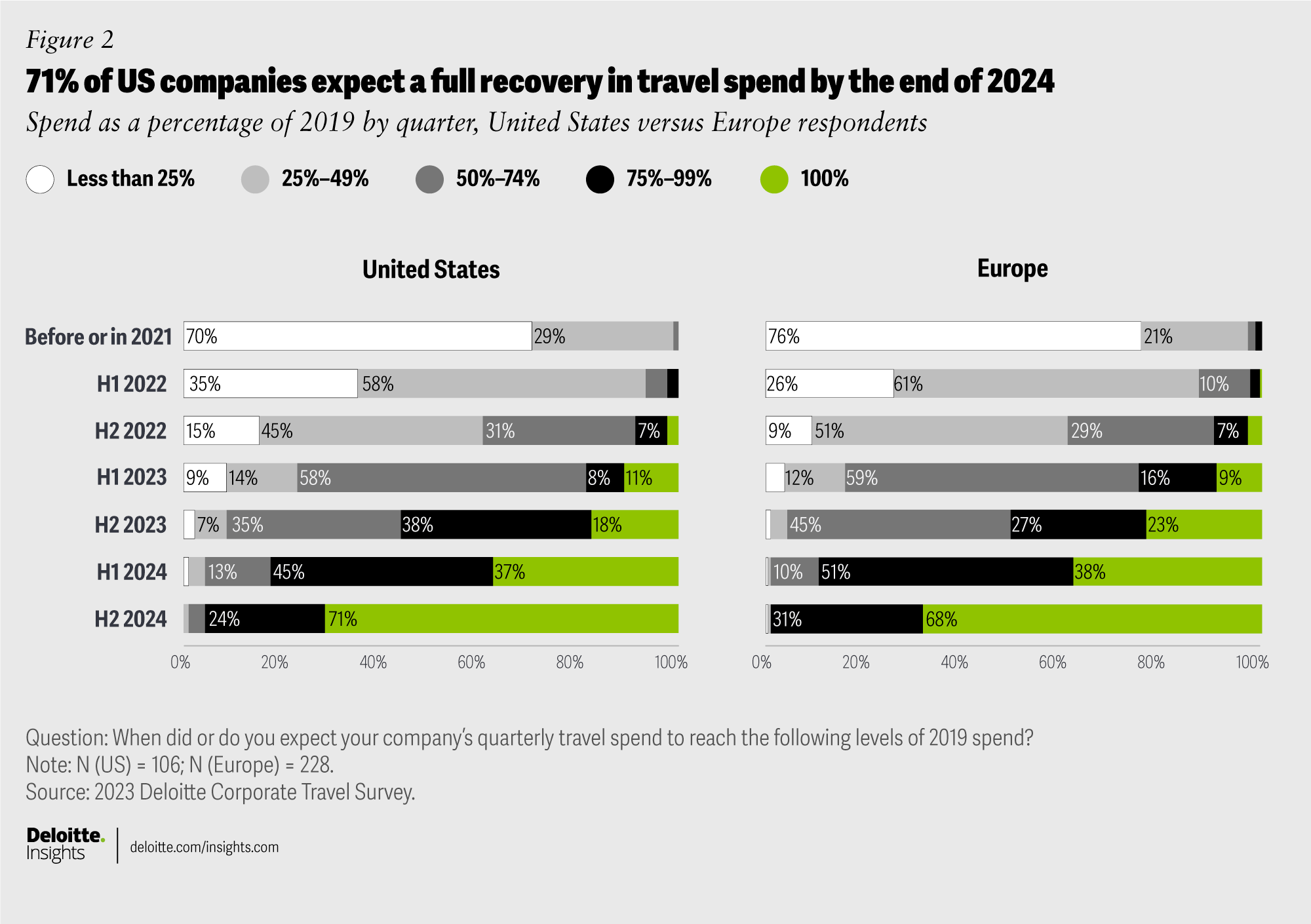

In this third edition of Deloitte’s survey, travel managers’ expectations have once again downshifted compared to the prior survey, though less dramatically. Travel managers in the United States and Europe anticipate very similar trajectories from 2022 through 2024. Altogether, about a quarter (24%) of companies expect their travel spend to exceed three-quarters of 2019 levels in the first half of 2023; that figure more than doubles to 53% by the second half of 2023. The share of US companies expecting to reach full recovery grows fourfold from the end of 2023 to the end of 2024. Among European companies, that figure triples (figure 2).

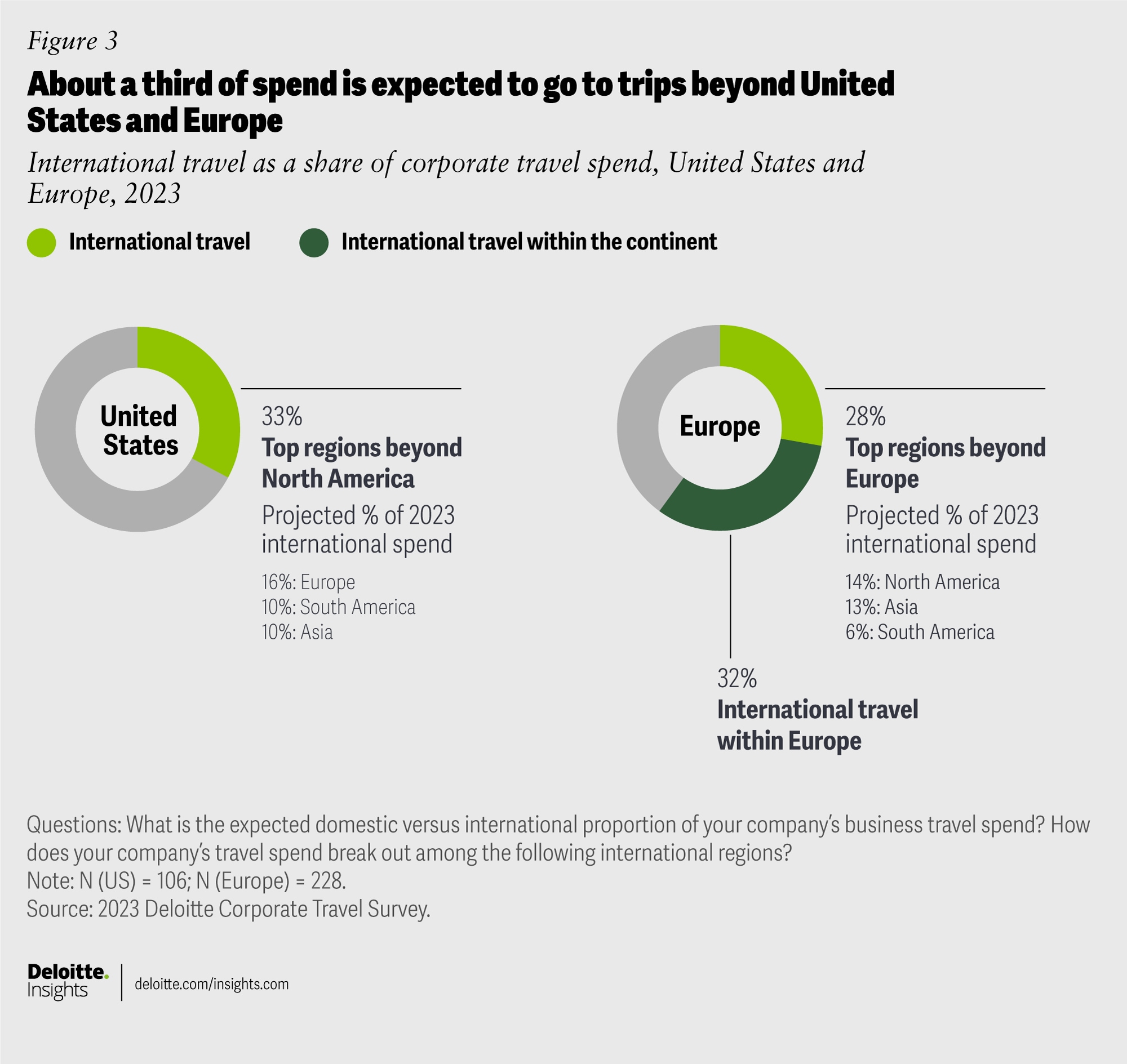

The biggest drivers of the expected continued increase in travel, according to the survey, are the growth of live events and easing of restrictions. As of early 2023, international borders were finally truly open for the world’s biggest economies, with China being the last to clear the way for inbound and outbound trips. US respondents expect international trips to account for 33% of 2023 spend, up from 21% in Deloitte’s 2022 survey, and similar to 2019. Long-haul corporate trips from Europe are still catching up: Respondents expect 28% of spend to go to trips beyond the continent, down from 34% in 2019 (figure 3). Even after restrictions are officially dropped, it can take some time for travel to resume at scale, especially for long-haul trips or destinations requiring visas, which might take longer to attain due to processing bottlenecks.3

The top reasons for these international trips primarily involve connecting with clients and prospects, but there is some variability across the United States and Europe. For European respondents, client project work is the biggest reason for trips beyond the continent, followed by sales meetings. American companies reported that the biggest reason for international travel is to connect with global industry colleagues at conferences and to build client relationships.

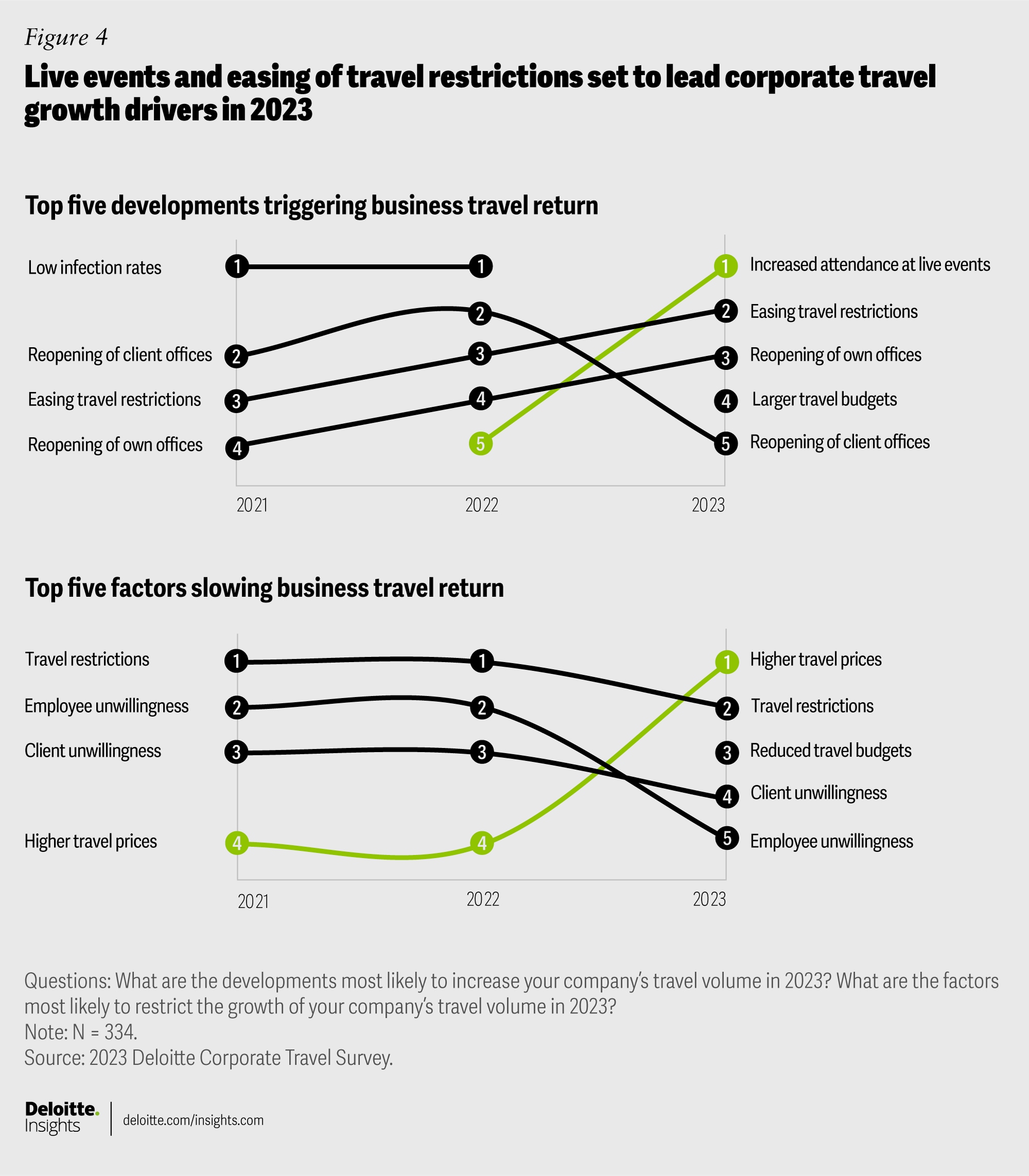

Live events appear poised to be a major contributor to business travel demand in the coming year. They leapfrogged from American companies’ fifth biggest reason for international travel in 2022 to their first in 2023 (figure 4). This trend extends to domestic trips and to European companies, as anticipated in Deloitte’s 2023 Travel Industry Outlook. Increased event attendance is the No. 1 driver of growing spend, cited by more than half of respondents in both Europe and the United States. For American companies, it is also the biggest impetus for international trips.

Pent-up demand likely plays a role, as many industry conferences were canceled or held online for two years or more. But this strong interest also could signal events’ growing importance as remote and hybrid work remain fixtures of the corporate world. When it is harder to call on prospects and clients in their offices, conferences can offer appealing opportunities to connect.

As attendees return to industry events, many companies also are adjusting their internal events. Half report that they have split their larger gatherings into smaller, regional, virtually connected ones. Nearly as many (44%) say they have adopted a hybrid approach. Companies also are increasingly looking to use their own gatherings to foster external connections: Fifty-four percent of European respondents, and 42% of Americans, say they are integrating more clients into internal events. And some are adjusting when these events take place: Thirty-three percent of American respondents and 22% of Europeans say they are moving internal events to warmer months, and more Europeans say they are integrating more clients.

With COVID-19 being less of an acute health concern for many, and border restrictions increasingly similar to the prepandemic period, why would corporate travel not immediately snap back to its prior growth trajectory? Bottom-line concerns and sustainability are two of the biggest reasons. And these are supported by the ability to leverage technology to decrease the number of trips needed.

Companies continue to see some degree of tech replaceability for all types of travel use cases. But there are clear standouts. Internal trainings and internal team meetings are rated as most replaceable, with more than 44% of respondents rating each at the extreme low end on the need for in-person interaction. On the other end of the spectrum, only 7% and 11% of respondents gave similar ratings, respectively, to client acquisition and client rapport–building.

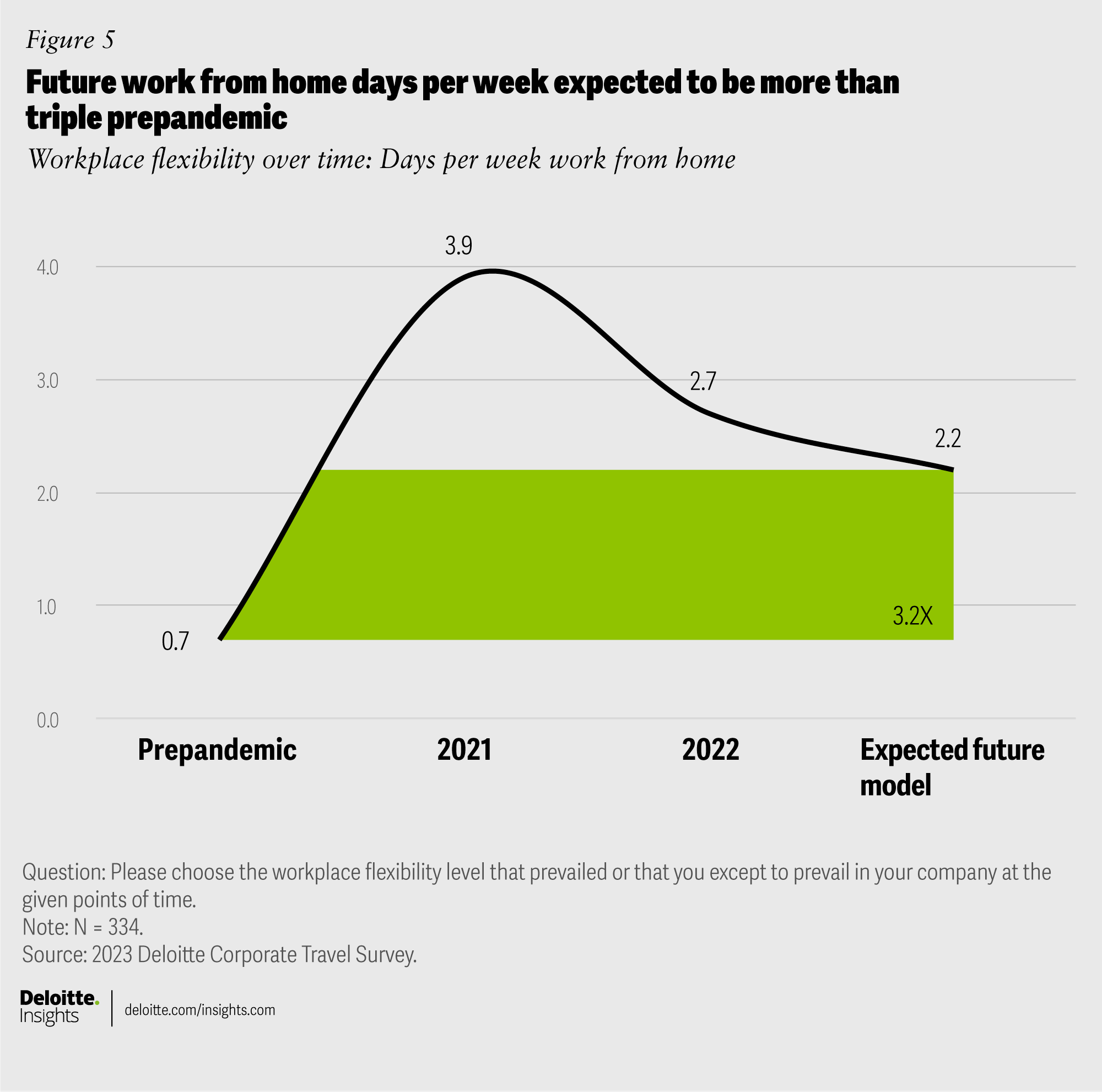

The same technology that is replacing some travel is used by some companies on a daily basis to enable working from home (WFH), which seems likely to stick going forward. Travel managers expect the future workplace flexibility model to have 3.2 times the WFH days compared to the prepandemic frequency (figure 5).

Employees seem to prefer the hybrid work model as well. According to the Deloitte Global State of the Consumer Tracker,4 on average, people who can work remotely already are doing so for 2.6 days per week, but would like to do so for 3.5 days.

This rise in WFH preference and incidence over the past two years has solidified some changes in the type of business trips taken. According to the survey, employees are traveling to more cities within driving distance from their location. There is also a reported increase in trips to the company headquarters by relocated employees, most of which (70%) are either completely or partially paid for by the company.

The biggest impacts that flexible work arrangements are having on travel volume are less direct: Companies have learned that virtual conferencing can support, to some degree, every business need that travel serves. And distributed workforces make it more complicated to arrange in-person meetings with clients, prospects, and internal teams that are spending fewer days in the office.

Compared to Deloitte’s 2022 survey, there has been big movement in the incorporation of nonhotel accommodation into company travel policies. Among US companies:

European companies trail slightly behind American ones in formal arrangements (incorporation into booking tools or agreements with specific providers), but one in four reimburse employees for nonhotel stays without such formal structures in place.

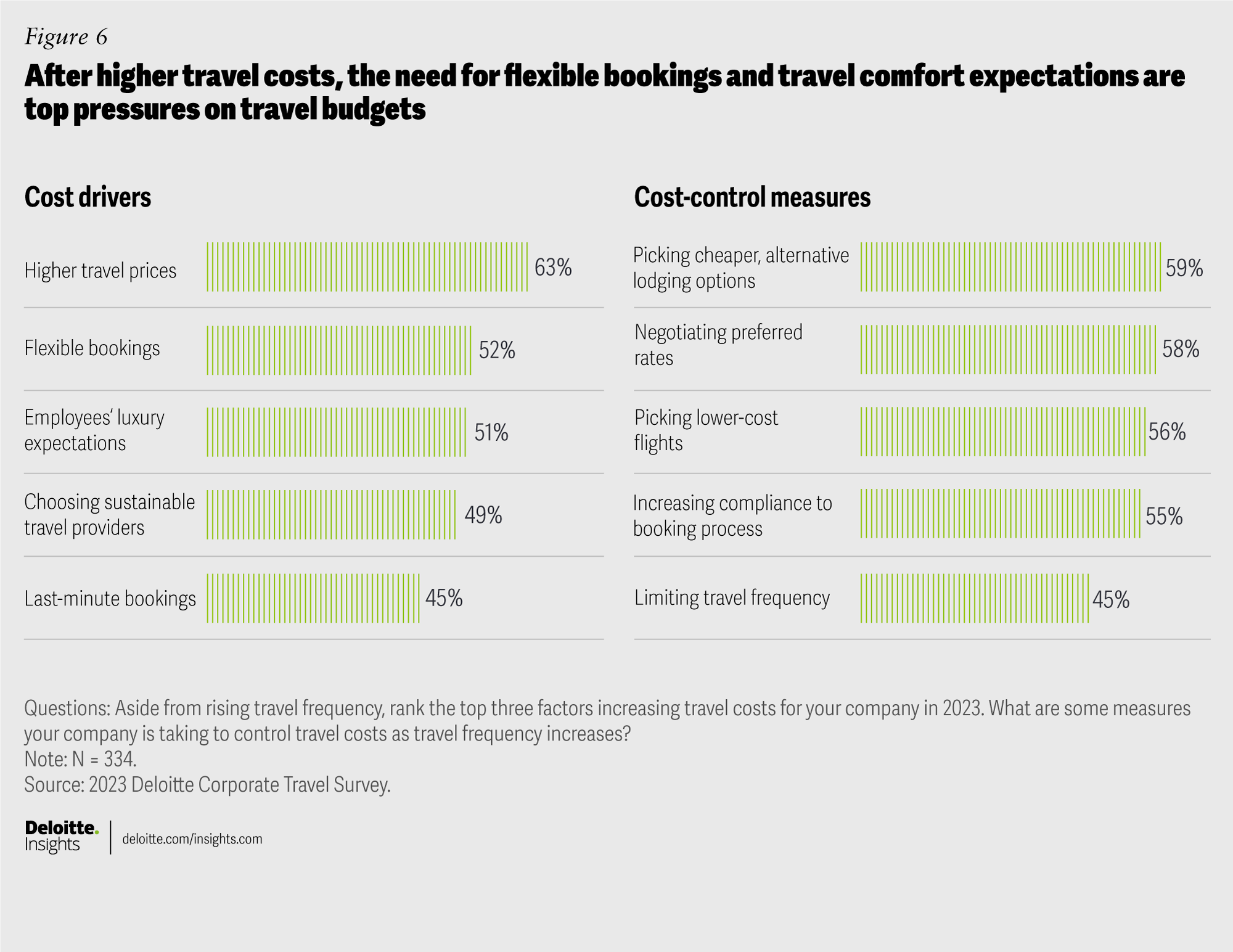

As corporate travel continues its expansion after three lean years, companies face a challenging cost environment. Higher airfares and room rates are the largest contributor to growing costs, and they have also become the No. 1 factor deterring the number of trips taken, up from No. 5 in 2022 (figure 4).

While consumer industries have been affected by inflation broadly, and published airfares and room rates have also risen for leisure trips,5 corporate travel faces distinct pressures. After years of reduced travel, many companies are working to accommodate shifting expectations from their workforce. About half of respondents report that employees’ expectations of luxury services (such as first or business class airfares and upscale hotels) and the need for flexible or last-minute bookings are pushing costs up in 2023 (figure 6). A similar share say that the pursuit of sustainable providers also adds to costs.

At the same time, some companies have also been renegotiating contracts after two or more years in a holding pattern due to the pandemic. Three in 10 respondents say that suppliers froze their negotiated rates in 2020 and 2021 based on (higher) 2019 volume. This was true for more American respondents (35%) than European ones (28%).

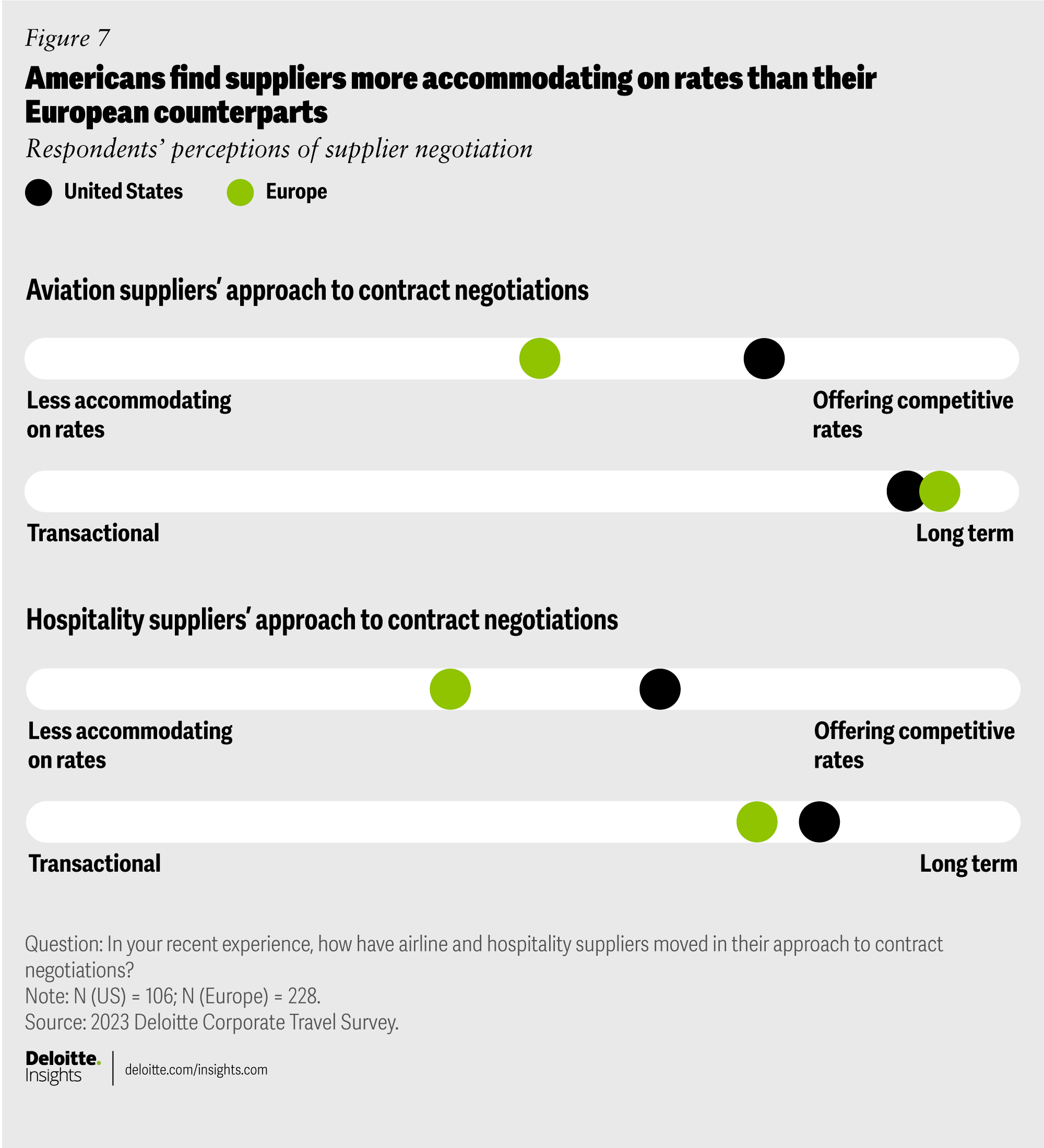

The possibility of prolonged lower business travel may be affecting negotiations. As suppliers and travel buyers have worked to update their contract terms in 2022 and 2023, some have encountered significant rate increases. In Q4 earnings calls, the CEOs of Marriott,6 IHG,7 and other leading hotel companies attributed recent strong performance partly to higher corporate rates. Overall though, most buyers seem satisfied with the deals they are striking. About one in five (19%) say that hotels are less accommodating on rates because they expect lower volume; just 11% report the same for airlines.

European suppliers appear to be less forthcoming with competitive rates than Americans: Fifty-four percent of European respondents report favorable airline pricing on positive volume expectations versus 63% in the United States. That regional gap is similar on the hospitality side (figure 7). In both regions, travel buyers generally believe that suppliers are taking a long-term view of their relationships versus pressing their advantage in the moment.

Higher rates likely have a dampening effect on the number of trips taken, but less so than last year. Just under half (45%) of companies say they limit frequency to control costs, down from 72% in 2022. Instead, the focus has shifted to mitigating the cost per trip with cheaper lodging (59%) and lower-cost flights (56%).

The experience of 2020 and much of 2021 demonstrated that businesses could still function with travel at a near standstill, saving companies millions. But even the most bottom line–driven leaders likely know that travel is more than just an expense line.

COVID-19 lockdowns brought travel-related decisions into the boardroom for many companies overnight. And for many, the calculus of when and how to return to the road may have also helped to reinforce a more strategic positioning. When asked about five different approaches companies could take toward considering the value side of the travel equation, 63% of respondents said their company has adopted at least three to some extent (figure 8). Most prominently, seven in 10 say their company strategically evaluates and prioritizes travel's potential outcomes (such as revenue generation) and side effects (such as cost, emissions, and health risks).

While these numbers demonstrate that a majority of companies treat travel with some strategic importance, they also indicate potential room for improvement. The travel management function has historically focused on controlling costs, and many companies are likely in early stages of better tracking how the benefits warrant those costs. Corporate travel suppliers and partners may have opportunities to help companies navigate toward better optimization, both by playing a bigger role in supporting positive trip outcomes, and by helping to measure trips’ impact.

As some companies seek to reduce their carbon footprint to meet either regulatory requirements or their own goals, travel attracts attention as a significant contributor to emissions. Although just one in seven surveyed companies in the United States and one in five in Europe expect sustainability curbs to reduce their travel in 2023, just over 40% of each say they are working to optimize their corporate travel policy to decrease their environmental impact.

With sustainability being a clear corporate priority for many, travel suppliers have invested significantly in initiatives to reduce their carbon footprint and demonstrate their green commitment—from designing brand-wide initiatives and striving to maintain multiple sustainability certifications, to funding research and incubating startups. In addition to reducing emissions, these efforts by airlines and hotels are also aimed at attracting and retaining corporate clients.

Although just one in seven surveyed companies in the United States and one in five in Europe expect sustainability curbs to reduce their travel in 2023, just over 40% of each say they are working to optimize their corporate travel policy to decrease their environmental impact.

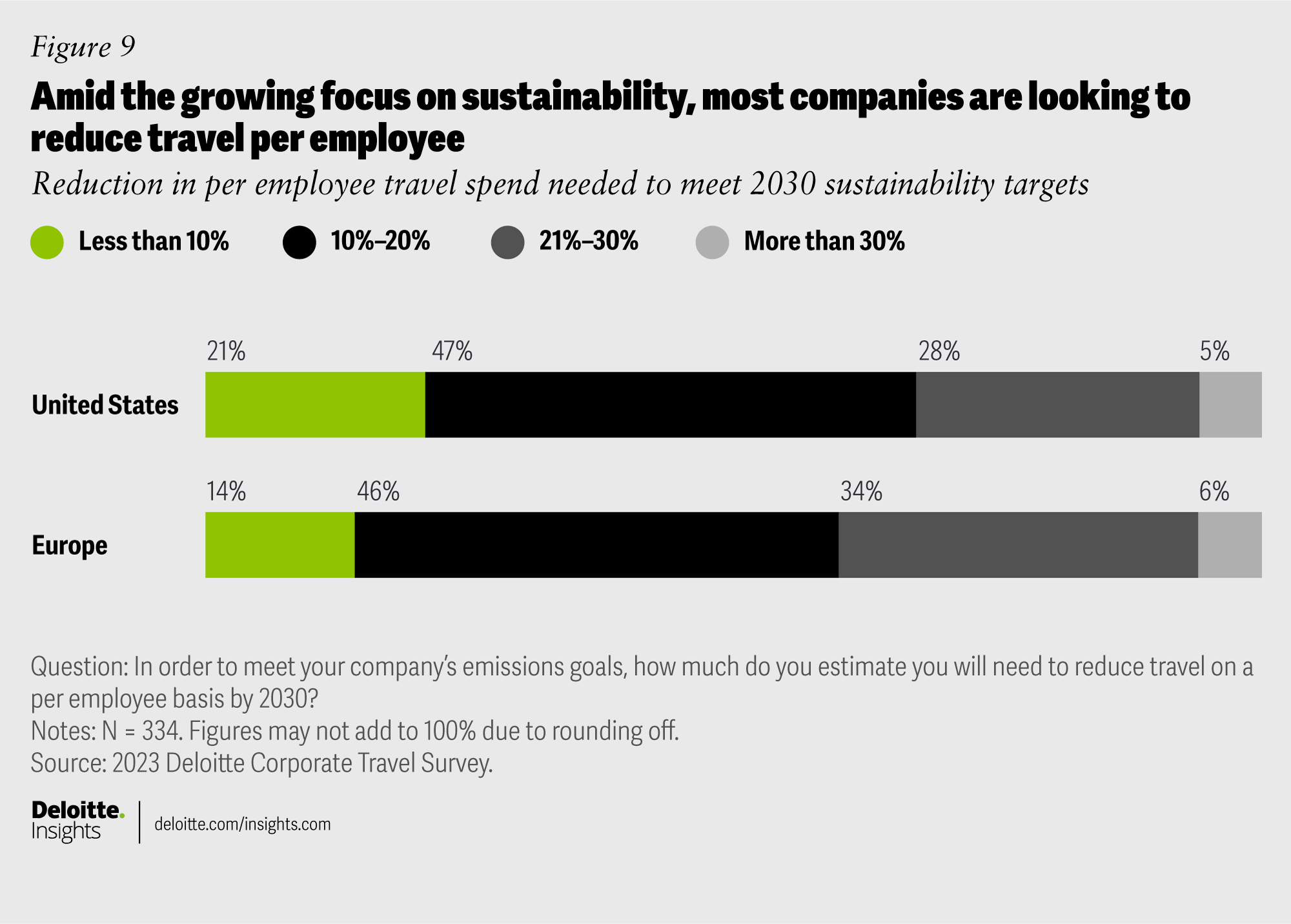

The stakes for these investments are real. As it stands, four in 10 European companies surveyed and a third in the United States say they need to reduce travel per employee more than 20% by 2030 to meet sustainability targets (figure 9). And many are building this into their policies: Forty-three percent of respondents (42% in the United States and 45% in Europe) say they are in the process of implementing a structure to assign carbon-emission budgets to teams alongside financial budgets. Complications abound for consistent emissions tracking and for mandating such budgets.

To better understand which supplier efforts are most likely to support continued engagement with travel buyers, Deloitte looked at seven different sustainability metrics or attributes for hotels, airlines, and car rental providers. About two-thirds of companies say they are taking each into consideration, but the degree and type of consideration varies (figure 10).

Overall mandated use by survey respondents is relatively low and is most widely adopted around the following: electric rental cars (possibly requiring employees to book them when available), airline seat upgrades, and carbon emissions per flight itinerary. These attributes are also most likely to be flagged in corporate booking engines, perhaps due to relative clarity compared to hotel-related attributes. On the hotel side, there appears to be a lot of data collection and tracking, but less activity that clearly signals sustainability efforts can help attract more bookings.

Travel suppliers and intermediaries should stay in conversation with corporate buyers on their progress in tracking travel emissions, and arming travelers with information to choose the most sustainable alternative. It may not be easy to create verifiable standards to measure the climate impact of each travel purchase, but demand for such standards is apparent.

Love it, hate it, or indifferent, the phrase “new normal” seems applicable to corporate travel in 2023 and 2024. Any talk of an upward trajectory for travel may carry caveats for at least several years, given the recent past—caveats about variants, new health emergencies, and economic and geopolitical instability. But barring major crises, corporate travel looks poised to bound upward for a year or so, before a likely return to the single-digit gains that were common prior to the pandemic.

The most significant new aspects of the new normal are coming into sharper focus. Changes in how work gets done look likely to limit corporate travel’s upside and alter the stakes of trips taken. Sustainability commitments and requirements also are expected to limit corporate travel growth, but opportunity is apparent in the willingness among travel buyers to work side by side with suppliers as they seek ways to make travel greener. And all of this appears to be happening in the context of a delicate and shifting balance around cost, value, and the strategic positioning of travel. For the travel suppliers and intermediaries that serve corporate clients, these emerging realities could create openings for smarter partnerships and collaborations that have the potential to unlock travel’s competitive advantages while minimizing its downsides.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}