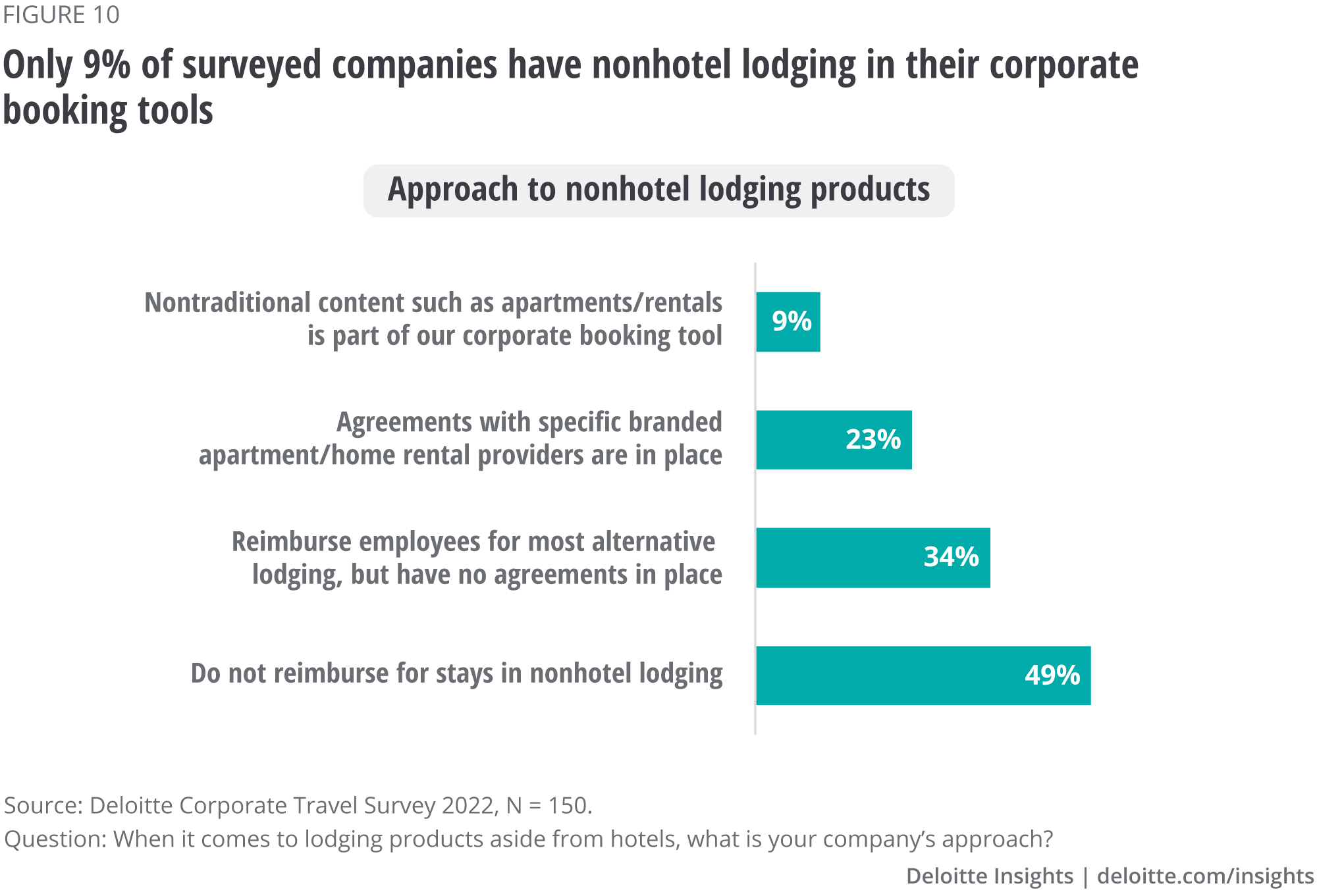

Deloitte’s research shows that the pandemic is creating a large number of new rental travelers, who plan to continue staying in rentals after the pandemic. As homes and apartments are poised to remain in the consideration set for leisure travelers, increased interest among corporate travelers could follow. Some business models are targeting corporate travel with standardized offerings in urban locations and high-end properties that can accommodate retreats for small teams. If these models continue to expand, or if a major rental player creates a targeted business product, rentals could increasingly appear in corporate booking tools.

For more traditional hotels, two years of depressed demand, accompanied by challenges attracting and retaining frontline workers, has led to cutting back on services and amenities. While hotels will no doubt do their best to provide stellar service as corporate travel increases, the challenges remain.

Some corporate travel buyers are turning to their contracts to ensure the best possible onsite experience for their teams, introducing clauses into meeting contracts that specify the availability of amenities during their events. Twelve percent of travel managers involved in meetings contracting say their companies have successfully added such clauses. And more than four in 10 have considered such clauses but have not successfully implemented them yet.

Looking ahead to a new shape and smaller size

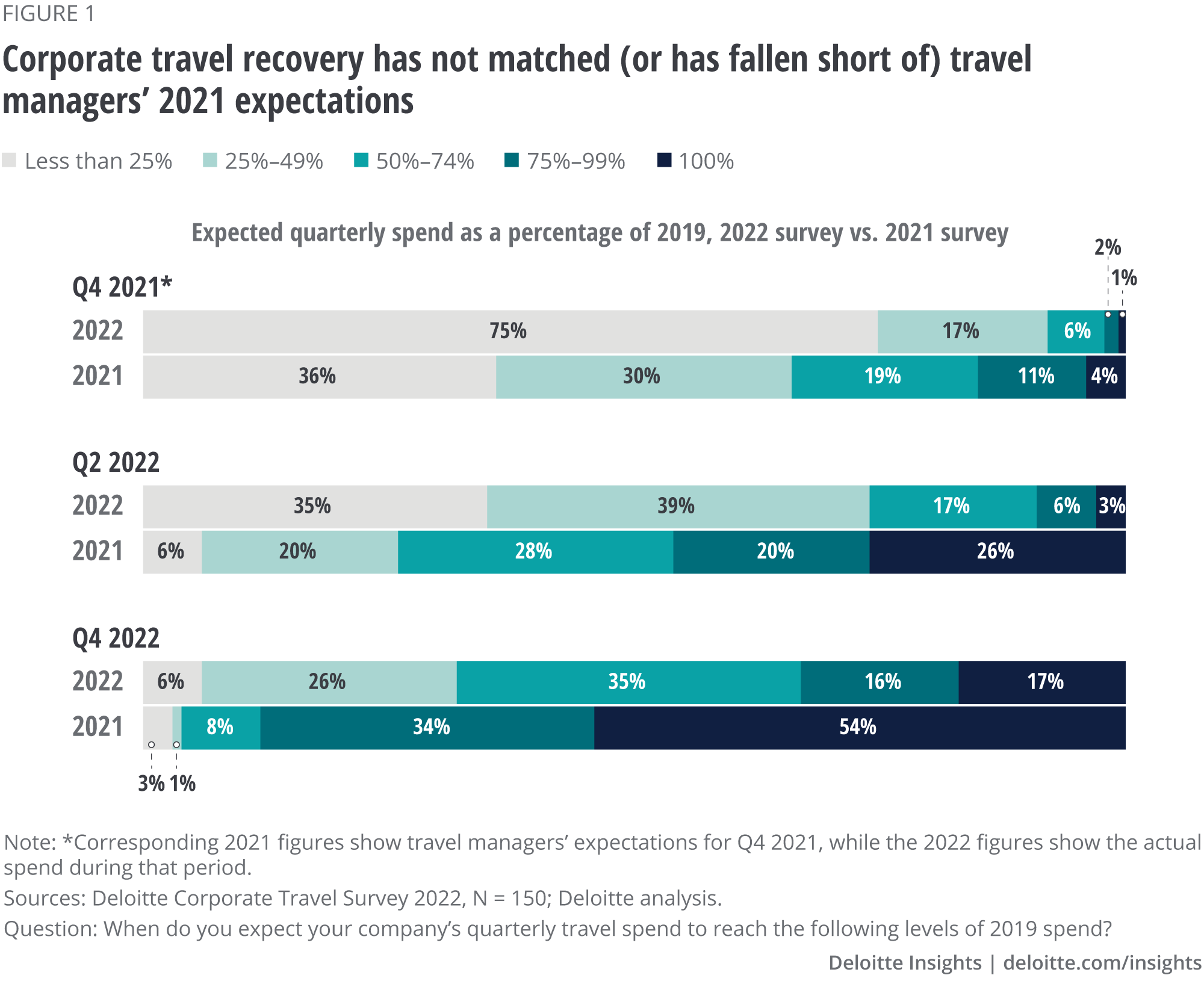

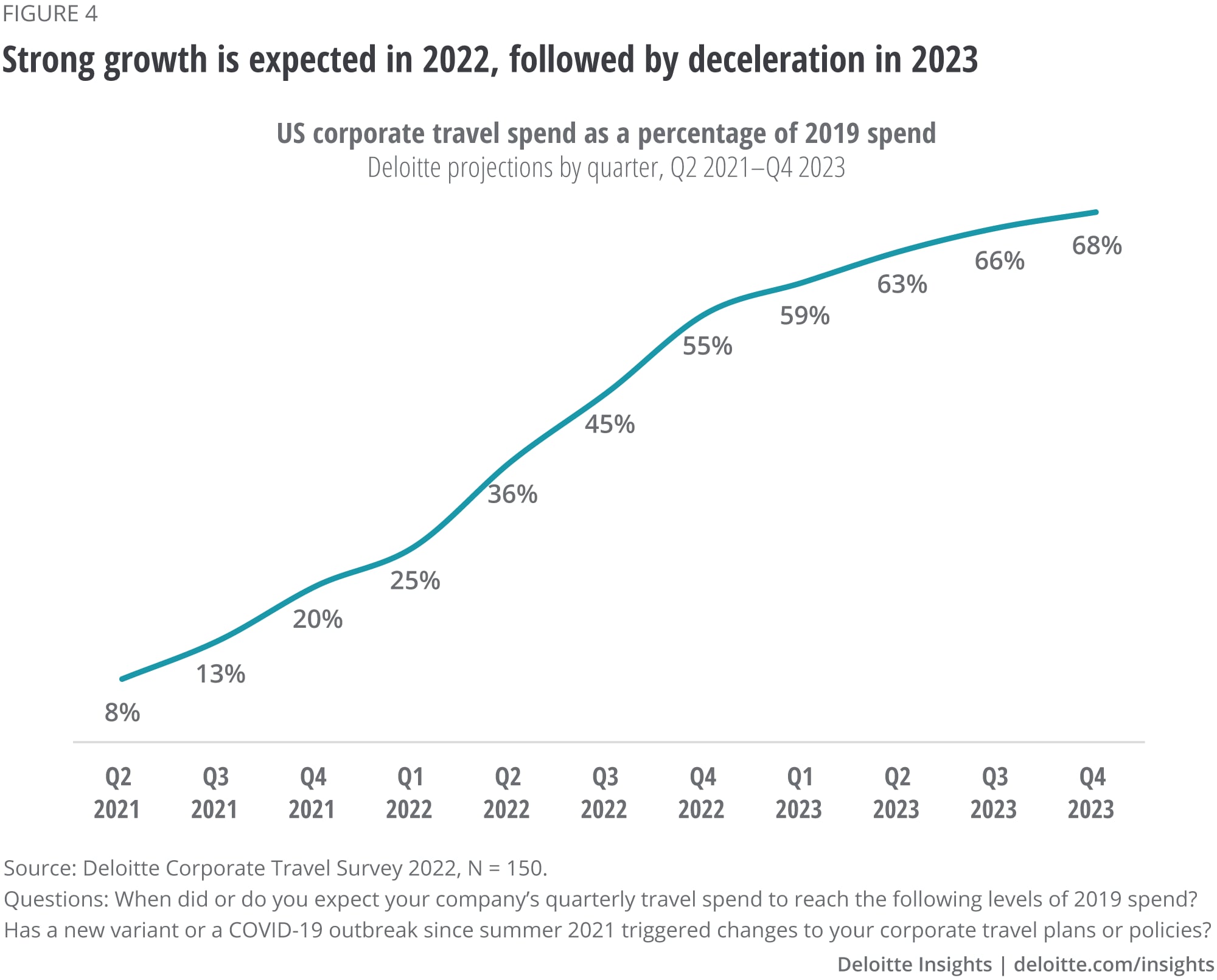

After two years of reduction to less than a quarter of its 2019 size, and months of continued setbacks due to COVID-19 variants, corporate travel is expected to climb back steadily in 2022. This climb will come more slowly than many expected or want, falling far short of prepandemic levels at the end of the year.

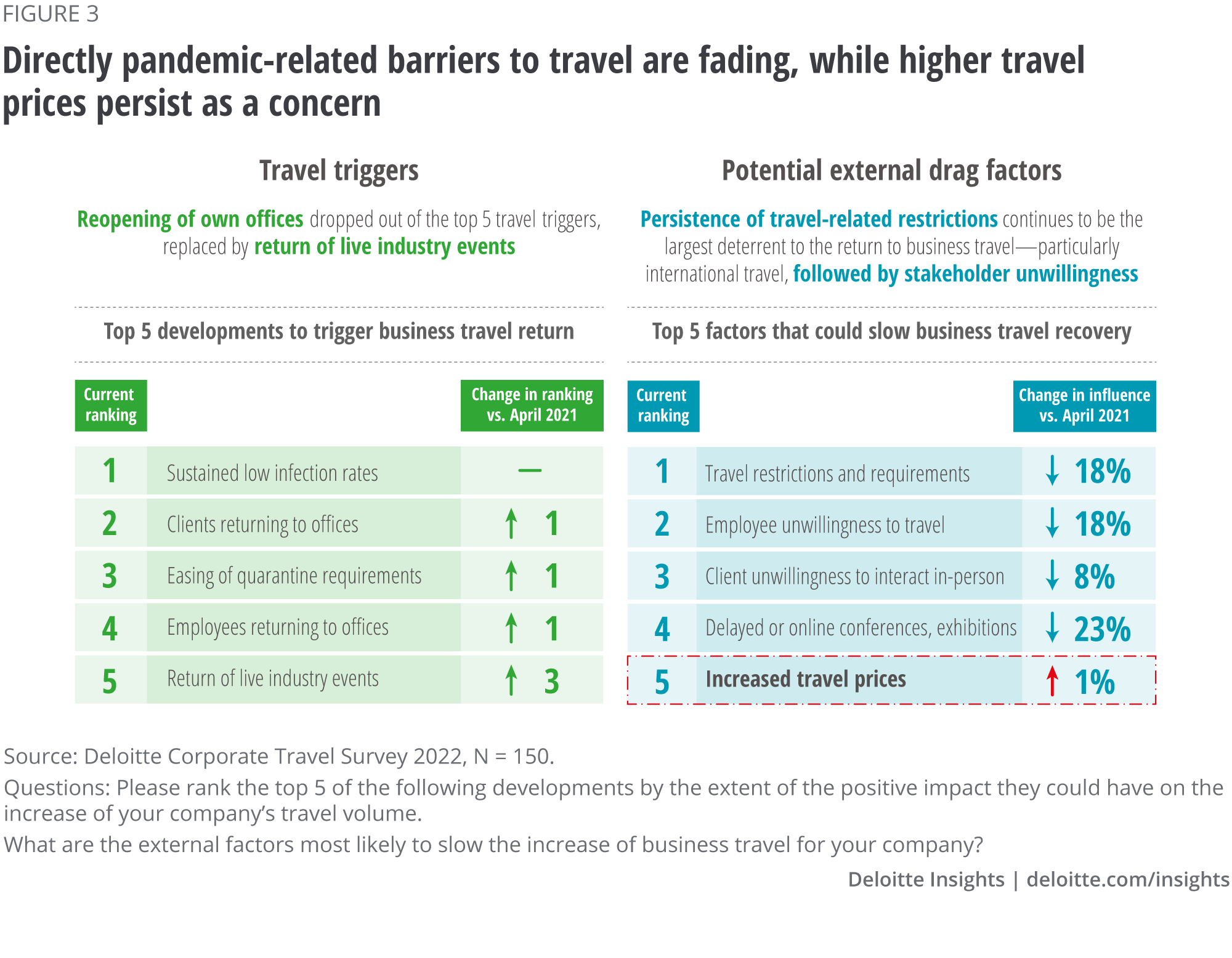

In addition to adapting to a new reality of fewer overall trips, travel providers should be aware of long-term shifts and short-term trends. Workplace flexibility is here to stay, and so are its effects on corporate travel. A new commitment to sustainability joins a much older commitment to cost containment, and together they will likely increase scrutiny of return on investment. While leaders recognize the value of live events, they may send fewer delegates and have greater interest in exceptional experiences.

Most of the changes underway present challenges to corporate travel providers. But for savvy and forward-thinking leaders with a partnership mindset, these changes can open up new opportunities to evolve and grow.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}