Small positive signs in the consumers’ dual-front crisis The road to recovery may be opening, but only slowly

8 minute read

04 June 2020

With some economies reopening and many still enforcing stay-at-home orders, how is overall consumer confidence faring? Explore our global survey findings to find out.

Consumers will likely not come back until they think it is safe to do so, both physically and financially. In our biweekly consumer surveys, we are measuring their anxiety, asking them about the perceived safety-specific activities, and tracking where they intend to spend their money. We are watching for the point where financial concerns start to outweigh health concerns and for when spending intent for more discretionary items starts to increase. One of the more significant observations from our recent survey data is that more consumers are feeling safe going to the store, staying in a hotel, and taking a flight. That is a good thing because that correlates to spending intentions.

Since mid-April, economies around the world are in various stages of reopening. While consumers continue to face the dual-front crisis of personal safety and financial well-being, there are initial positive signs. In a number of countries, initial health and safety concerns show some signs of lessening in the last week, but they still overpower financial well-being concerns and continue to inform consumer behavior.

About the survey

Deloitte is conducting a series of biweekly surveys in multiple countries—we started with 13 in mid-April and have expanded to 15 since—to understand the mindset of the consumer. (See figure 2 for a complete list of countries.) Our third survey, conducted the week of May 11 turned up the findings we share here.

Each biweekly survey is fielded using an online panel methodology where consumers are invited to complete the questionnaire (translated into local languages) via email. These surveys, designed to be nationally representative of the overall population in each market, poll 1,000 consumers in each country.

Check in every two weeks via our dashboard as we continue to explore the consumer mindset and emergent trends in successive surveys.

Learn more

Learn more about connecting for a resilient world

Read our previous report, In the throes of a dual-front crisis

Explore the Deloitte State of the Consumer Tracker

Subscribe to stay on top of changing consumer behavior trends

Learn about Deloitte’s services

Go straight to smart. Get the Deloitte Insights app

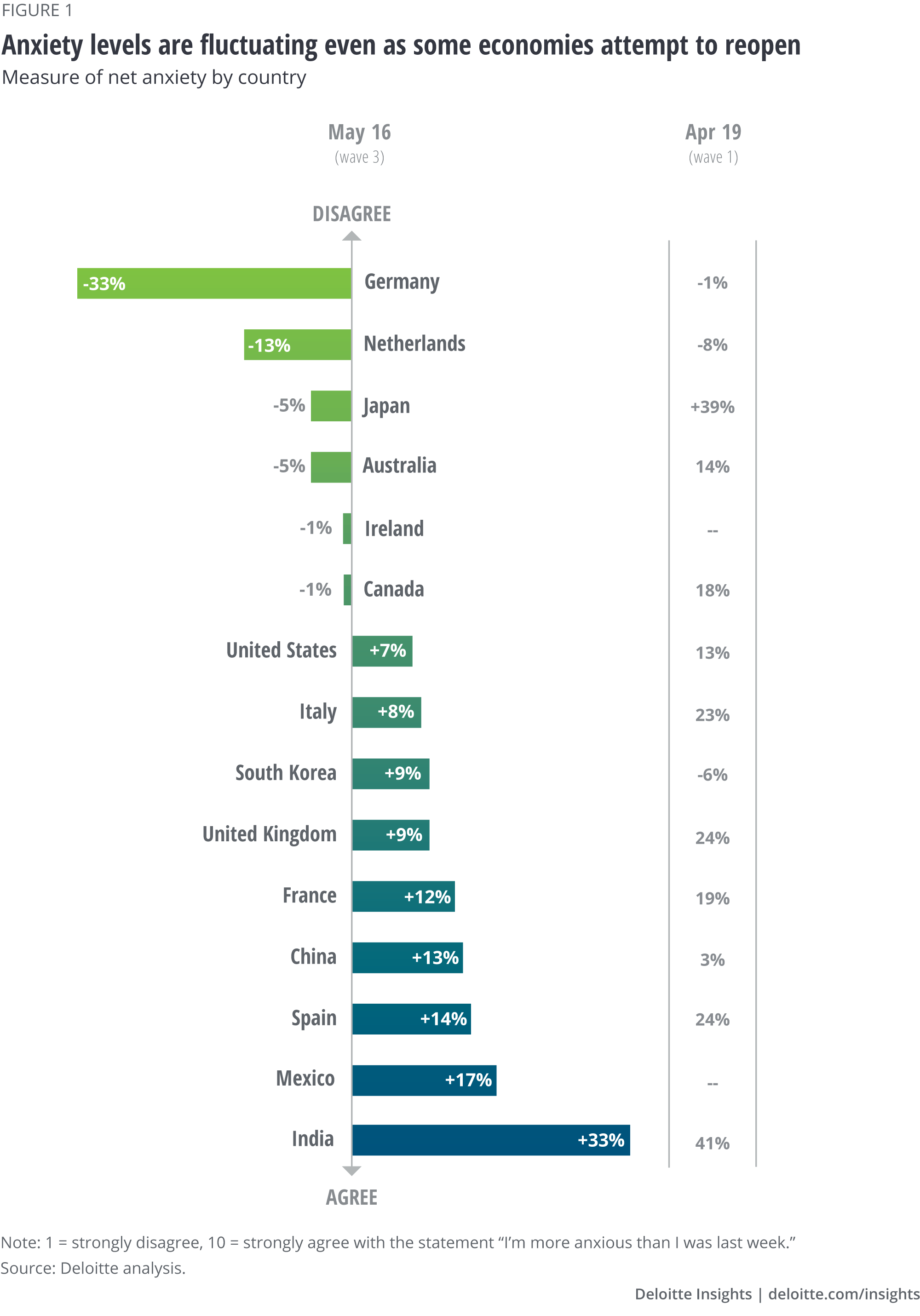

Our collectively anxious moment shows signs of easing

We are living through a collectively anxious moment. Consumers have varying levels of concern for personal safety and financial well-being. That said, the direction of their collective anxiety has slowed somewhat since mid-April (figure 1).

Countries such as India, which saw COVID-19 hit later than others, continue to show higher levels of anxiety while countries that were affected by COVID-19 relatively early on and now have relaxed stay-at-home orders more widely have seen anxiety lessen (figure 1). Within India, the direction of collective net anxiety has also lessened. Japan opened up aspects of its economy on May 14, and in a sign that other countries looking to follow suit will find encouraging, its net anxiety dropped to -5% from +20% in our previous survey. That said, consumers seem attuned to the forward progress and backward steps in this public health crisis—net anxiety in South Korea went up (19% to +9%) following a recent new COVID-19 cluster outbreak in Seoul.

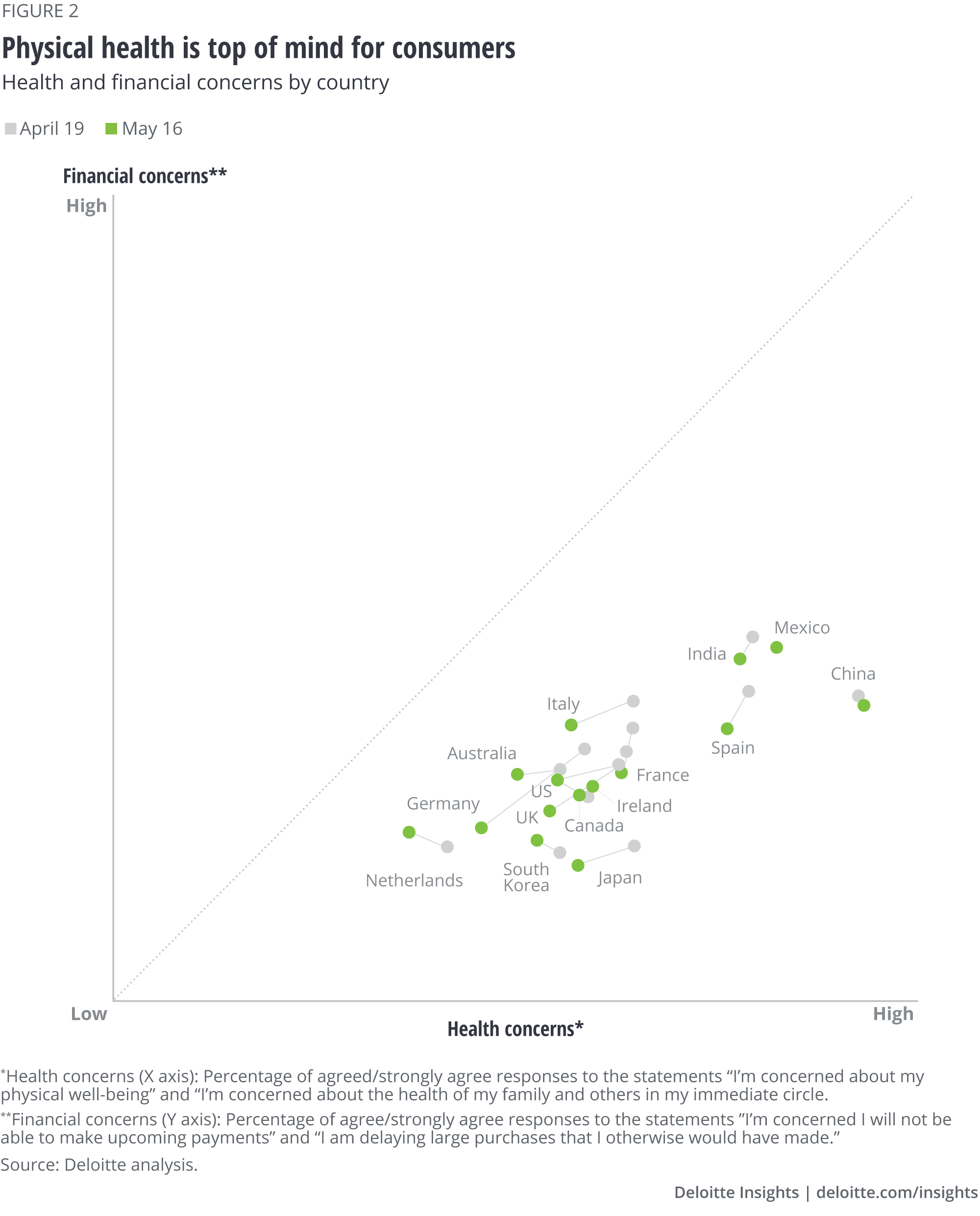

Health concerns still overshadow financial concerns

In the matter of weeks, the ordinary act of going to the store or taking a flight became more fraught with concern. As economies attempt to reopen, it’s likely not until the public feels safe that consumers will return to behaviors that we only recently took for granted. In fact, we do not expect to see a return to normal, or even a new normal, until total concern descends from its elevated level and financial concerns overtake those of immediate health and safety. We are watching for country results to migrate toward the origin and across the dividing line (figure 2).

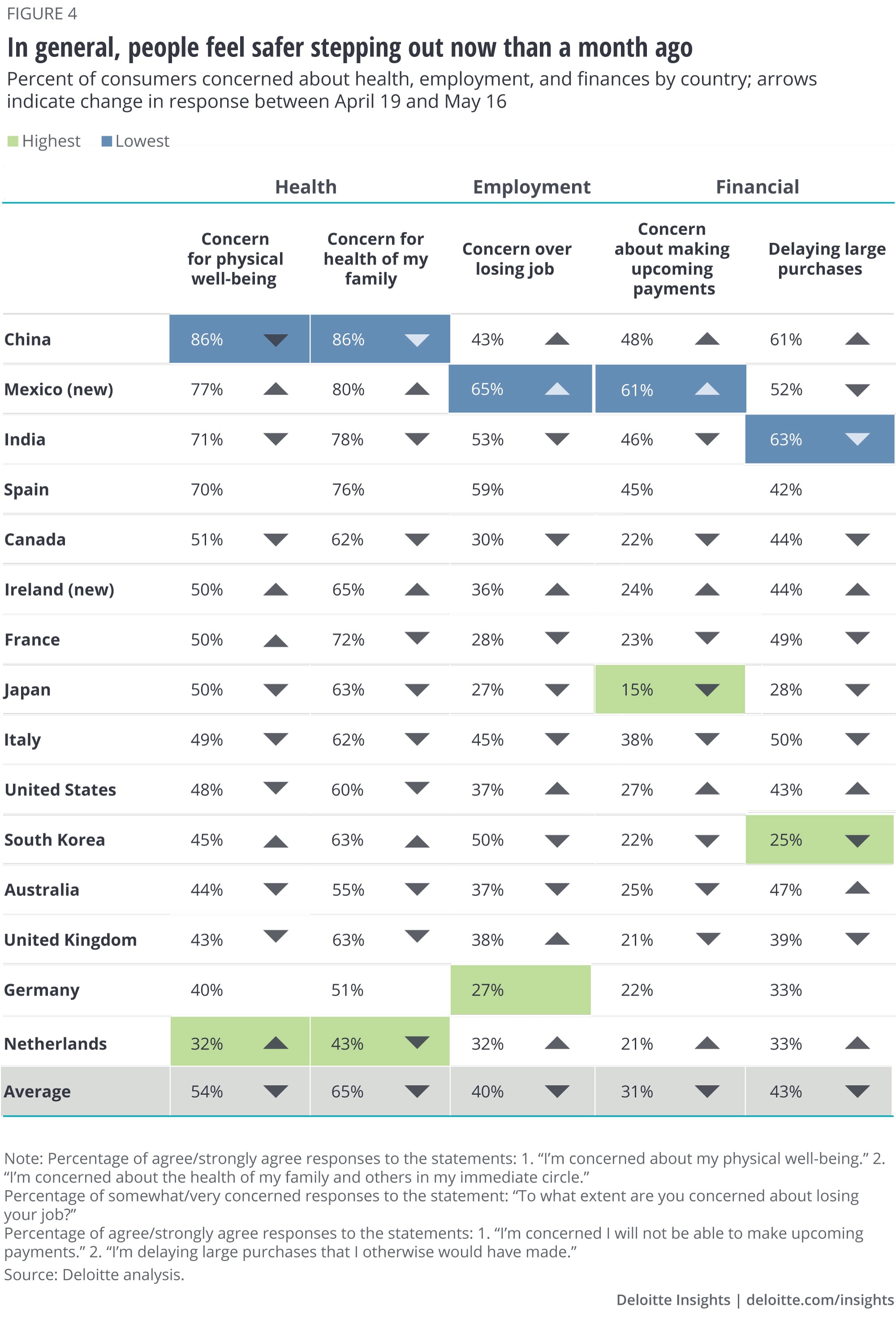

For now, concern for one’s physical health remains high relative to concern for financial health. However, there are some signs of easing in health concerns amongst most countries. Personal health concerns have dropped in seven out of the 13 original countries in our survey, while concerns around the health of others have dropped in 11. In China, Mexico, India, and Spain, health concerns remain the highest. In China, Mexico, and India financial concerns are more or less on par with health concerns. Western Europe, the rest of North America, Australia, South Korea, and Japan appear to share similar levels of health concerns with some differing levels of financial concerns; Italy reports higher and South Korea and Japan lower financial concerns than the other countries in this group.

The knock-on effect of COVID-19 is the impact on the global economy and rising unemployment across the globe. On average, across all the countries we surveyed, 40% of respondents who still had a job were concerned about losing their jobs (figure 3). That is only slightly lower than mid-April (42%), led by respondents in Mexico (65%), Spain (59%), India (53%), and South Korea (50%). As the unemployment rate in China rises,1 concern over losing a job has risen from 36% in mid-April to 43% in mid-May as have concerns over making upcoming payments, 38% to 48%. Respondents in Mexico and India are also the most concerned about making upcoming payments. And respondents in India (63%) and China (61%) are the most likely to be delaying large purchases. Meanwhile, respondents in Germany and France feel the most secure in their employment status. Financial concerns have also lessened somewhat in Germany and the United Kingdom. The mixed responses underscore the national nature of the dual-front crisis.

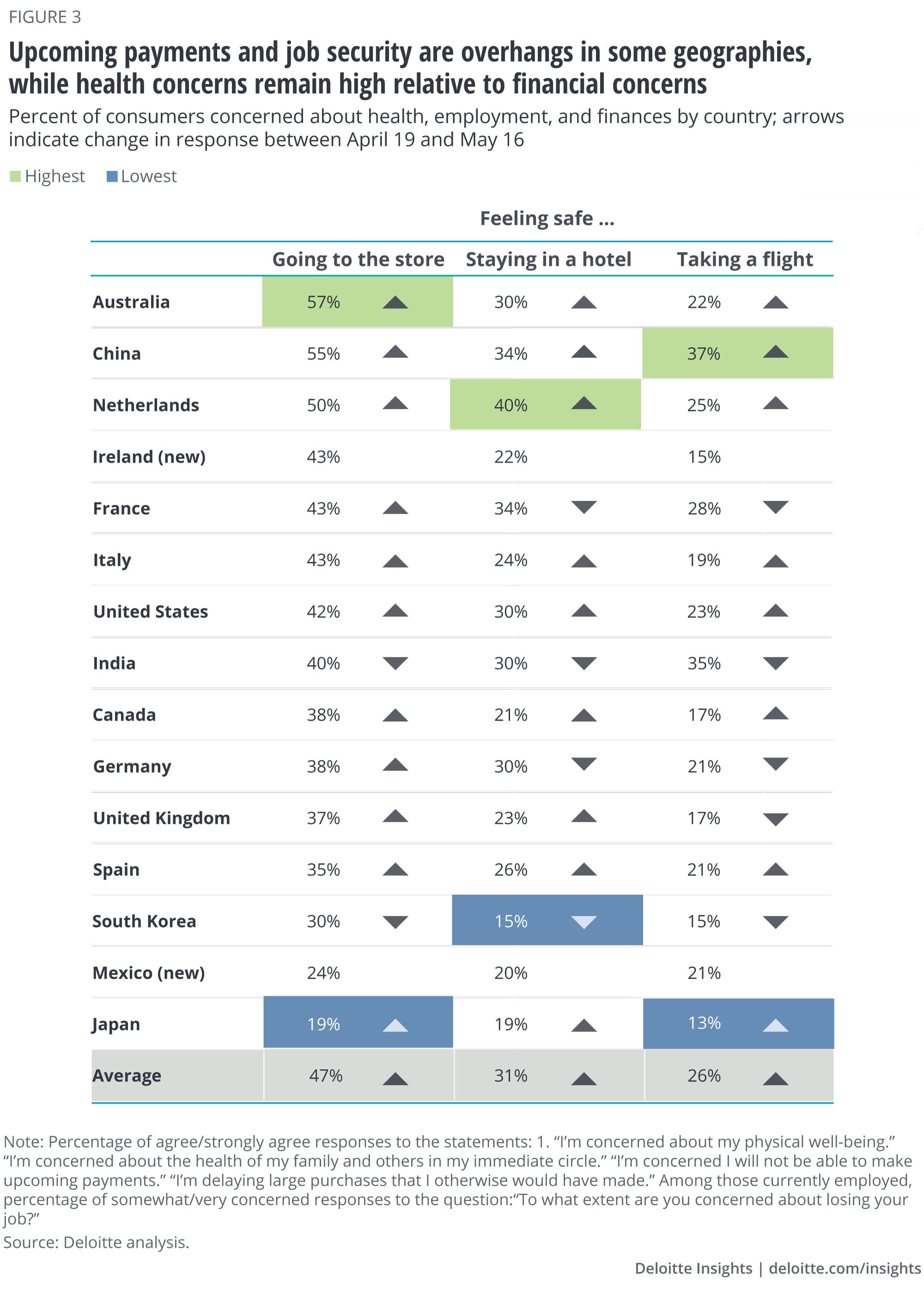

Do consumers feel safe doing ordinary things?

The world over, we are observing that the concern about one’s personal health typically informs the feeling of safety in doing what was, up until very recently, life’s ordinary activities. Across the countries we surveyed, nearly half (47%) of respondents said that they feel safe going to the store—up from 35% a month earlier. It suggests that retailers’ safety precautions have helped and that nearly half of consumers are adjusting to the new normal. However, in some countries such as Mexico, South Korea, and Japan, there is still considerable apprehension about going to the store. In early May, Mexico saw increases in COVID-19 cases2 and in South Korea, fears were reinflamed when headlines showed a possible second wave in late this year.3 Perceptions of safety remain low in Japan despite daily decreases in new virus cases.4

After weeks of stay-at-home orders, the vast majority of consumers are not ready to hit the road or take a flight for leisure travel though the sentiment toward travel has improved slightly. Three in 10 (31%) feel safe staying in a hotel. While not a huge jump, it’s still an improvement from 25% a month earlier. More people feel safe to fly as well—26% in mid-May compared to 22% in mid-April.

Consumers’ concerns about their well-being have obvious implications for retailers, restaurants, hoteliers, airlines, and a host of other consumer-oriented businesses. As economies reopen, people will likely need to feel safe if society seeks to return semblance of normalcy. While most countries are experiencing upward trends, India’s and South Korea’s see-saw trajectory is evidence that the public can be overwhelmed by the realities on the ground and concern over a resurgent virus.

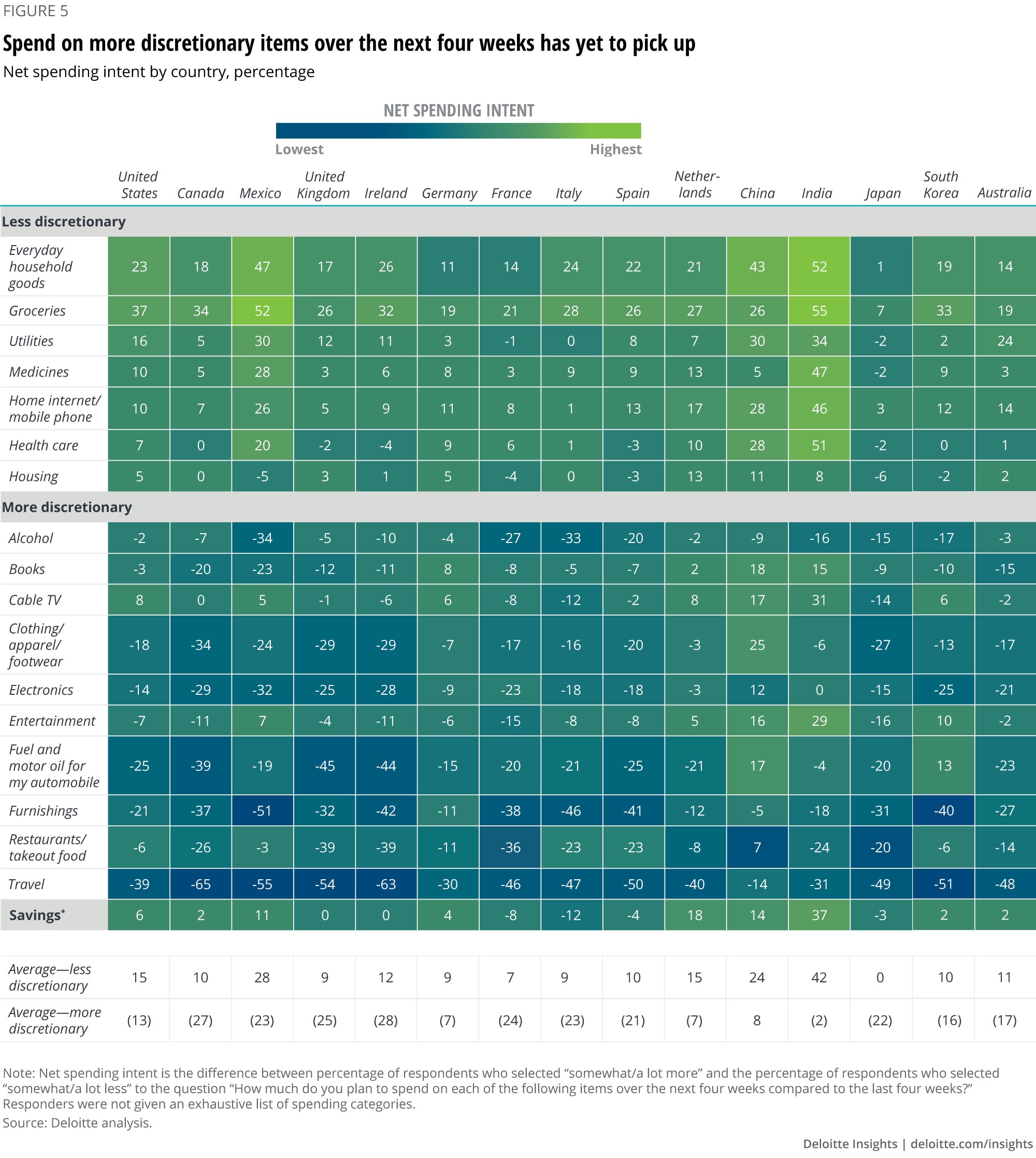

Where are consumers spending their money?

As economic uncertainty continues, consumers remain cautious and curb net spending intent on more discretionary items over the next four weeks (figure 5). Relative to mid-April, consumers have also slowed their net spending intent on less discretionary items in the last several weeks. Presumably, they have stockpiled the necessities and are maintaining their levels. (We chose to ask about a four-week period because it represents a typical household budgetary timeframe. Our survey tracks a rolling four weeks.)

China appears to be an exception on more discretionary spend—there are early signs of more discretionary spend intentions returning to China. The Netherlands and Germany are beginning to show pockets of more discretionary spend intent.

As stay-at-home orders lift, certain categories, such as travel, have a hill to climb. However, China’s net spending intent on travel has improved to -14% now from 31% a month ago. While still not in positive territory, the rate of change appears to be slowing and moving in the right direction. Combined with China’s relatively higher sentiment about flying and staying in hotels, its domestic travel market may be one to watch as a first mover on the road to recovery.

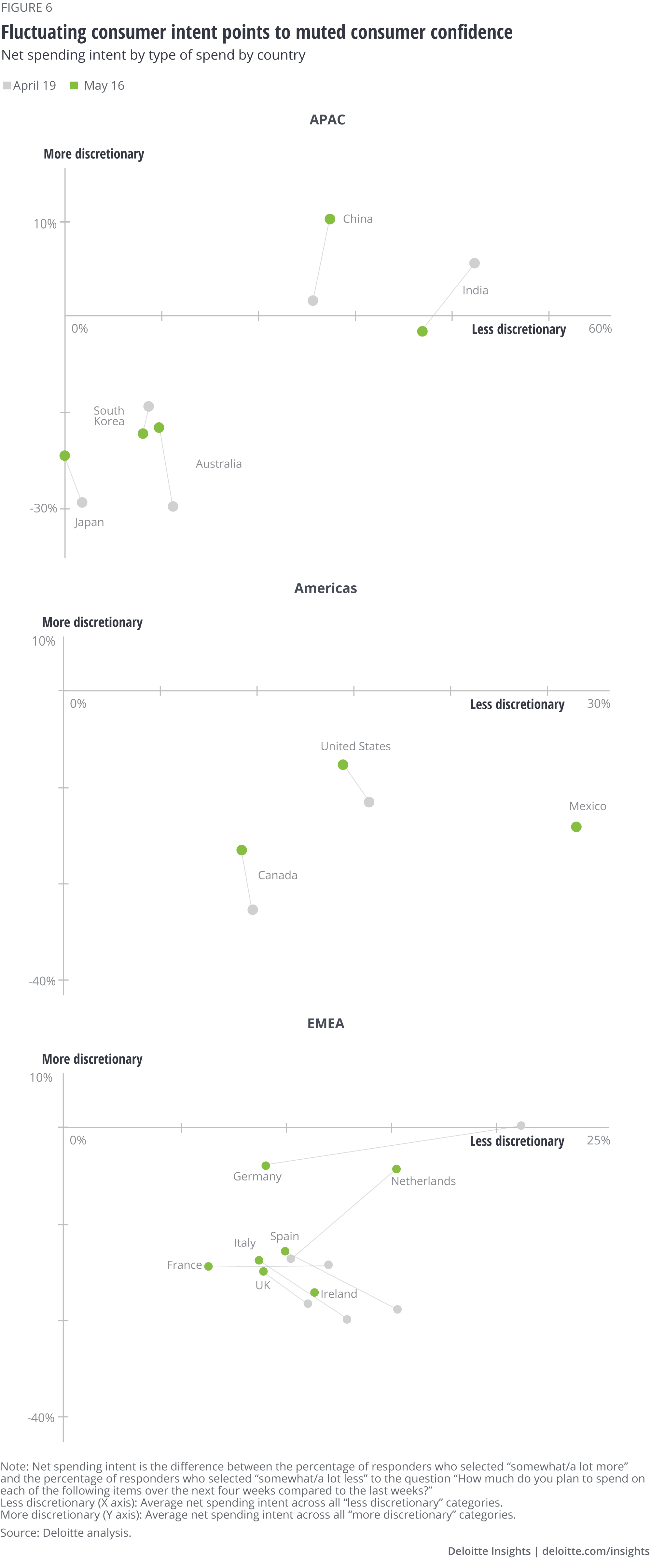

What does the average net spending intent by country tell us?

When we take a more macro view of net spending intent, China and India show the most volatility on average net spending intent for more discretionary and less discretionary items, but for different reasons (figure 6).5 As mentioned above, China may be seeing early signs of emergence from the impact of COVID-19. Meanwhile, India is moving through the initial stages of stockpiling as the country experiences a relatively delayed impact of COVID-19.

Movement up and to the right is a sign of consumer intent returning. As the Netherlands accelerates its economic reopening,6 it is the only country in our survey that has consistently moved in that direction. The majority of countries have improved upward on more discretionary spend intent, but leftward on less discretionary spend intent. Japan, for example, has no intention to increase less discretionary spend over the next four weeks compared to the previous four weeks. Japanese headlines speak to recessionary storm clouds.7 And, despite Germany’s relatively solid position overall, it continues to contract on net spending intent on less discretionary categories and, to a lesser extent, on more discretionary categories.

As economies continue to open up, the extent to which net spending intent fluctuates for more discretionary items may be a good indicator of pent-up demand in each market.

Many economists are predicting a W-shaped recovery with a potential resurgence of COVID-19 later this year.8 There are news stories, such as those in South Korea and Germany, of localized outbreaks influencing consumer behavior.9 It will be telling to see how countries rise to the occasion to protect their citizens and their economies.

Deloitte Consumer Industry Center

Technology is changing rapidly, and so are consumers, radically altering how companies do business. The Deloitte Consumer Industry Center delivers insights that help leaders in the automotive, consumer products, retail, transportation, hospitality, and services sectors better understand their business environment and where it’s heading.

Learn more

Get in touch

- Leon Pieters

- Global Consumer Industry leader

- Partner | Deloitte NL

- leonpieters@deloitte.nl

- +31 6 52 67 25 24

© 2021. See Terms of Use for more information.

More on consumer behavior

-

Retail distribution Collection

Retail distribution Collection -

Advancing the fresh campaign Article5 years ago

Advancing the fresh campaign Article5 years ago -

In an uncertain economy, does fresh produce spoil revenue growth? Article5 years ago

In an uncertain economy, does fresh produce spoil revenue growth? Article5 years ago -

Augmented shopping: The quiet revolution Article5 years ago

Augmented shopping: The quiet revolution Article5 years ago -

The consumer is changing, but perhaps not how you think Article5 years ago

The consumer is changing, but perhaps not how you think Article5 years ago