Voice of the annuities consumer has been saved

Voice of the annuities consumer Exploring innovative approaches to accelerate annuities market growth

23 May 2015

Despite a generally promising annuities market outlook, insurers may need to address several fundamental systemic challenges to increase market penetration, widen their prospect base, and keep sales on an upward trajectory.

Annuities due for a reinvention

When Charles Dickens wrote, “It was the best of times, it was the worst of times,” he probably did not have the market outlook for annuities growth in mind. Yet the classic assessment that opens A Tale of Two Cities aptly describes the conundrum faced by many annuities writers today.

In many respects, this would indeed appear to be the “best of times” for those looking to sell annuities, given current demographic and economic trends deepening the pool of prime prospects for such longevity-focused solutions.

Fewer and fewer individuals are able to depend on defined benefit pension plans to support them in their retirement years.

For one, the US population has been steadily skewing older: The Pew Research Center estimates that roughly 10,000 Baby Boomers are turning 65 every day, and that phenomenon will continue for at least another 15 years.1 At the same time, fewer and fewer individuals are able to depend on defined benefit pension plans to support them in their retirement years, leaving an increasing percentage of the population on their own to figure out how to save and invest for a financially secure retirement in which they do not outlive their assets.

Annuities, with its core feature of long-term, guaranteed income, should be uniquely positioned to help buyers alleviate this retirement funding concern—an advantage recognized by a slim majority of consumers recently surveyed for this report by the Deloitte Center for Financial Services.2 Yet despite seemingly optimal growth conditions, individual annuity sales have been fluctuating over the past decade. In fact, sales of annuities were 11 percent lower in 2014 than at their peak in 2008 (figure 1), according to the LIMRA Secure Retirement Institute.3

Part of the problem is that persistently low interest rates have made the past few years the worst of times for many annuity providers trying to generate enough of a return on their investments to profitably cover their guaranteed income commitments. As a result, some carriers have been intentionally scaling back their annuity writing while derisking their portfolios. Others are reassessing underwriting and pricing models as well as adjusting their product mix, terms, conditions, and fees to better position themselves for sustainable growth.

View the related infographic

The likelihood of interest rates starting to rise again later in 20154 may prompt a reversal of this retrenchment trend. Indeed, some major carriers that had taken a step back in the past couple of years are now reversing course to expand their annuity business.

However, looking at the bigger picture, our survey identified more fundamental, systemic challenges for insurers to address if they expect to consistently increase market penetration, widen their prospect base, and keep sales on an upward trajectory over the long term.

Which new approaches should annuities writers consider?

What we gathered from our research can be summed up with the phrase, “What got you here won’t get you there”—at least when it comes to connecting more effectively with a wider range of annuities prospects.

For example, our survey found widespread unfamiliarity with the value of annuities and how they work, even among many who have already purchased one. It also revealed that, while intermediaries overwhelmingly remain the lynchpin in reaching out to prospects about annuities and walking them through a sale, some consumer segments are open to hearing directly from carriers—particularly among younger prospects (those between 30 and 44 years old), who at the moment are not typically even being approached about what this product might be able to do for them.

Carriers should therefore consider a number of options to transform their business, both to potentially gain market share within standard target groups as well as to enhance the visibility and attractiveness of their annuities products for nontraditional prospects. Among the tactics to consider is a redesign of the product to address additional needs beyond retirement; to reimagine the industry’s usual marketing approach to broaden familiarity with and trust in annuities; and to expand potential channels to generate new business.

Based on analysis of our survey data, industry practices, regulatory changes, and market developments, this report spotlights four opportunities for annuity writers to attract a broader pool of prospects in traditional and underserved markets (figure 2):

Based on analysis of our survey data, industry practices, regulatory changes, and market developments, this report spotlights four opportunities for annuity writers to attract a broader pool of prospects in traditional and underserved markets (figure 2):

- Increase focus on repeat buyers and capitalize on cross-selling

- Repurpose the product to broaden the utility and attractiveness of annuities

- Appeal directly to consumers with proactive education, marketing, and sales initiatives

- Leverage the workplace channel to significantly increase group sales as well as facilitate more individual purchases within retirement accounts

Some of these opportunities could be seized with a fairly straightforward shift in focus and standard operating procedures, but others may require a more fundamental reinvention in providers’ approach to the marketplace.

About this survey

The Deloitte Center for Financial Services contracted with an independent organization, Research Now, to conduct an online survey in December 2014 of 745 buyers and 757 nonbuyers of annuity products. While these prequalified respondents represent a wide range of age and income groups, approximately two-thirds had household income of between $100,000 and $200,000, and the majority were between the ages of 45 and 74. About 8 out of 10 were married or in a domestic partnership, while the same percentage had at least a four-year college degree. The respondent pool was split in half in terms of gender.

Annuity buyers were asked about their financial objectives, motivating factors, influencers, product knowledge, the role of advisors in their purchase decision, and satisfaction with the product, among other issues related to their customer experience.

Nonbuyers were evenly split among those who had considered purchasing an annuity but had decided against doing so, and those who had never considered buying one. They were queried about their understanding of the product, their shopping experience, any concerns they may have with annuities, and other potential barriers to a sale.

The survey also explored scenarios that might spur a future purchase among current buyers and nonbuyers alike.

Changing the game

Increase focus on repeat buyers and capitalize on cross-selling

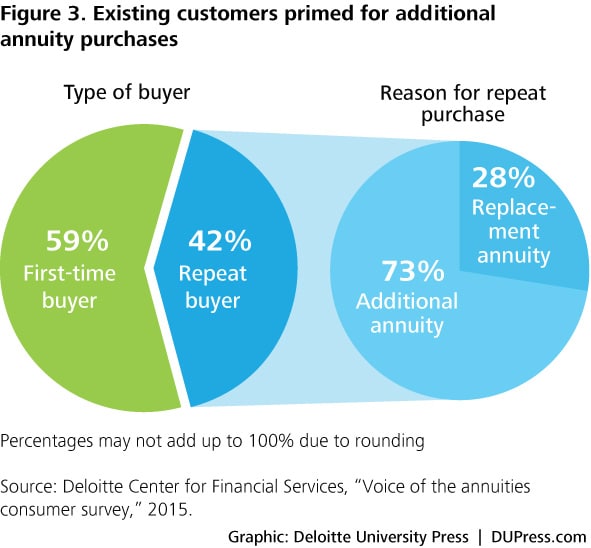

Recurring annuity purchases may offer providers an avenue for growth, given that 42 percent of the buyers we surveyed had already owned at least one other annuity prior to their most recent acquisition. Even more encouraging is that 73 percent of these repeat buyers bought an annuity in addition to, not as a replacement for, their prior purchase (figure 3).

Part of the explanation for the tendency of policyholders to purchase additional annuities could be the high levels of satisfaction among the buyers we surveyed. Indeed, more than half of these respondents were very satisfied with nearly all aspects of their annuity purchase, while only a handful described themselves as somewhat or very dissatisfied.

Part of the explanation for the tendency of policyholders to purchase additional annuities could be the high levels of satisfaction among the buyers we surveyed. Indeed, more than half of these respondents were very satisfied with nearly all aspects of their annuity purchase, while only a handful described themselves as somewhat or very dissatisfied.

A closer look at the context around this finding revealed that 7 out of 10 respondents stuck with what they knew and liked, buying another annuity in the same class as their earlier purchase. For example, those who owned a variable annuity were very likely to purchase another variable product, as opposed to an indexed or fixed annuity.

Meanwhile, of the 28 percent of repeat buyers who had replaced an earlier policy, only 22 percent said it was because they were unhappy with the value of the prior annuity. About 4 in 10 said the prior annuity simply no longer met their financial needs, and about the same percentage said they had replaced an annuity because their advisor recommended the change.

Familiarity with the annuity writer and seller may also create additional purchases in the form of cross-selling opportunities. Nearly half of annuity buyers had already owned at least one other financial product from their annuity company, while about two-thirds said they also had purchased other financial products from the intermediary who sold them their most recent annuity.

More importantly, 77 percent of the annuity buyers surveyed said they would consider making additional investments through the same individual. This means that those with life insurance or other types of coverage, as well as buyers of various investment products, might be more amenable to adding an annuity to their portfolio from the same provider or intermediary.

Call to action

- Don’t overlook potential sales to existing annuity clients or owners of other financial products with the same carrier or intermediary, as our data show that they might be prime prospects for additional annuity purchases.

- Providers should leverage advanced analytics to spotlight potential repeat annuity buyers and cross-selling prospects.

- Augmenting current client portfolios with similar products to build multiple guaranteed income streams over time presents a prime opportunity for increased top-line annuity growth with potentially lower up-front marketing and sales expenses.

Repurpose the product to broaden the appeal of annuities

To capitalize on the high potential for repeat sales, prospects need to first be sold their initial annuity, preferably early in their financial life cycle. Our data therefore underscore the need to build bridges to traditionally overlooked segments—namely, younger prospects and those in lower-income brackets.

Among the nonbuyers surveyed, 55 percent of the youngest age segment (30–44 years old) and 44 percent of the lowest-income group ($25,000–99,000) said they had never considered buying an annuity simply because no one had ever suggested one to them. Moreover, only 8 percent of the youngest segment and no respondents in the lowest-income group were ever even approached by a financial intermediary about buying an annuity.

When asked what they would change in the annuity sales approach to make the product a more likely investment option, a theme voiced by one respondent suggested that carriers “be more open to nontraditional annuity buyers.”

Intermediaries may be shying away from suggesting annuities to younger prospects because they are more likely to have other financial priorities and are too far from retirement to worry about establishing a guaranteed income source later in life.5 Indeed, annuities have traditionally been marketed as instruments designed to address longevity risks and provide long-term financial security for retirement.

That message has certainly gotten through to the annuity buyers queried in the current survey, who indicated their main financial objectives with the purchase were retirement security (53 percent), guaranteed income (44 percent), and an income stream that would last for their lifetime (27 percent). And high satisfaction among our surveyed annuity buyers suggests that, as currently marketed and sold, this product is well suited to serve as an instrument for retirement and longevity security.

However, given the reality of stagnant individual annuity growth rates, it may be pragmatic for insurers to consider augmenting this traditional product line with innovative elements to appeal to a wider—particularly younger—audience. Our survey indicates that there are life events other than retirement that could motivate a younger person to buy an annuity. For example, 35 percent of annuity buyers in the youngest age group said they had purchased one because they “came into a sum of money,” while 23 percent cited the birth of a child as a reason for buying an annuity—perhaps to help finance their education. Cultivating relationships in earlier life stages through more appropriate, targeted policies could lead to multiple purchases before culminating in the product’s traditional focus on retirement planning.

Venture into unconventional product design and features

Insurer success at penetrating untapped market segments will likely require a comprehensive understanding of annuity characteristics that can ultimately discourage a purchase for some: product complexity and investment objectives.

For example, given the considerable diverse components that make up an annuity instrument—such as guarantees, fees, and surrender charges—the product is often perceived as relatively complicated. While half of both buyers and nonbuyers surveyed say they have a basic understanding of annuities, only a small portion (11 percent of nonbuyers and 18 percent of buyers prior to purchase) said they had understood the product and its features very well.

Moreover, among the three-quarters of nonbuyers surveyed who said they were either ambivalent about purchasing an annuity (33 percent) or unlikely to buy one (42 percent) over the next five years, over one in five said they would consider the option if they had a better understanding of the product. This sentiment was particularly prevalent among the youngest age bracket (figure 4).

While this finding highlights the need for greater efforts to educate younger consumers about annuities (addressed later in this report), it may also advocate for development of simpler products—at least for certain hard-to-penetrate segments. Indeed, in response to open-ended survey questions seeking suggestions on how to improve the product and sales process, the most prevalent comment by far among both buyers and nonbuyers addressed the complexity of annuities and the language used to describe how they work.

Among the comments offered by respondents was a plea for “better-written materials that a layman can understand” along with a call for “easier, plain-English definitions and descriptions of the product.” One respondent said that, next time, he or she would “do more research to understand the financial lingo better.” Others complained that annuities materials should not be written in “legalese,” while urging carriers to provide “a simpler overall product.”

Simplification could have a two-fold impact: reducing hesitance to purchase an annuity stemming from complicated features and charges, while simultaneously preparing first-time buyers who are not yet “retirement focused” for the future purchase of a more sophisticated annuity offering a lifetime income component.

Nearly 40 percent of our nonbuyer respondents (almost all younger than 65) say that they would likely wait until they are closer to retirement to purchase an annuity. Getting this segment interested in annuities earlier may require changing the conversation from pure retirement security issues to other potential uses for the product in earlier life stages. For example, a lower-cost, less complex, and more limited “starter” annuity for younger age brackets could provide annuitized outlays for a child’s eventual college tuition, or even help recent graduates and their parents pay off student loans after graduation. One respondent suggested, “Market to new college graduates paying back loans [and who are] looking to invest a small amount that will increase over time.”

Another possibility is to broaden the purpose and appeal of annuities by introducing more “hybrid” products, such as a policy that offers life insurance protection today with the option to trigger annuitization features when the buyer gets closer to retirement.

Call to action

- Begin to build bridges to younger demographics to foster familiarity with annuities as an asset class.

- Develop simplified products to serve as “starter annuities” to attract a broader and potentially younger consumer base.

- Create new or hybrid products to allow for redirecting the dialogue to serve the needs of less retirement-focused demographics by emphasizing more appropriate life-stage considerations, such as the birth of a child or education financing.

Appeal directly to consumers with more proactive education, marketing, and sales initiatives

While our survey indicates that intermediaries are likely to remain the lynchpin in annuity prospecting and sales, that should not discourage insurers from directly communicating with consumers more often. The goal is not necessarily to disintermediate (although, as we note later in this section, there is some potential for direct-to-consumer sales among younger segments) but to instead better inform prospects about the benefits annuities offer and thereby develop warm leads for the insurer’s sales force.

Lack of awareness and understanding of annuities among the general public has been an ongoing challenge for the insurance industry. That hurdle was validated by our survey results, which found a widespread lack of awareness about how annuities work and the value they offer, even among those who had bought the product. Among nonbuyers, awareness and understanding were even lower.

This problem was also raised repeatedly by respondents when they were asked to suggest ways to improve the annuity sales approach. Respondent comments included, “Provide information in a way that is easy to understand for those of us not well versed in financial products,” and “Annuity companies need to do a better job educating the general public about their products—not just those who might already be interested in annuities.”

This is an important finding, since one in five nonbuyers surveyed said that having a better understanding of the product might prompt them to consider an annuity purchase over the next five years.

Meanwhile, when nonbuyers were asked why they were not likely to purchase an annuity, 30 percent said they understood how the product worked, but felt it was not the right investment for them. A similar number also said that annuities did not offer good “value” for their money. These percentages were somewhat higher—at 40 percent and 44 percent, respectively—among respondents who believed they knew enough about investing to be able to manage on their own without advice from a financial professional.

Carriers therefore need to be more proactive in getting their message out about what annuities can do, how they work, how much they cost, and how they stack up against other investment options. One respondent suggested that it would increase trust and confidence in a provider and their annuity offerings if the consumer had access to “comparison scenarios that clearly show the benefit of an annuity over alternatives.” Ideally, this shift in approach would be implemented not just at an individual company level but also, perhaps, as part of an industry-wide initiative.

Current advertising efforts seem to be a relative nonfactor; only 2 percent of our surveyed buyers said they were prompted to consider buying an annuity by an advertisement. However, that percentage might be bolstered if insurers were to conduct more explicit multimedia campaigns and direct outreach efforts that explain the potential uses for and value of annuities, particularly compared with other options such as mutual funds, which were cited as the top alternative choice among nonbuyers.

Indeed, insurers might consider following the direct advertising approach taken by the pharmaceutical industry, which lays the groundwork for increasing demand by making more people aware of particular drugs, explaining what they do, outlining their potential risks, and ultimately driving consumers to ask health care providers whether a prescription may be right for them. A similar campaign that explains the need for annuities could have the potential to create demand at the source so that more consumers are prompted to inquire about annuities rather than wait for intermediaries to suggest they buy the product.

While intermediaries were by far the primary source for annuity information among our surveyed buyers, insurers can engage in direct marketing as well by creating simpler, perhaps more interactive educational materials, and delivering them online directly to prospects as well as making them available through intermediaries. At the same time, industry groups could help set the stage for more annuity sales by collaborating on an industry-wide educational marketing and advertising campaign to help better articulate the benefits of annuities and broaden the consumer base for the product.

As part of such a joint effort, the annuities industry might benefit from coalescing around a single, high-profile spokesperson to promote and explain annuities to the public—and, perhaps more importantly, to defend the product against criticism raised by media commentators or consumer advocates. Indeed, one respondent said that to increase trust and confidence in annuities, providers should consider “addressing the concerns that are made public by money consultants on TV.”

Carriers could also begin to supplement their ad campaigns with alternative means of establishing direct contact. For example, younger respondents in particular were inclined to rely more on Internet-based sources—including general web searches for news articles, consumer websites, and insurance company websites—for annuity information. This indicates increasing demand for online capabilities and suggests that online efforts, including social media campaigns, could be effective as part of a wider, more holistic digital direct-connect program.

What might prompt prospects to buy directly?

When nonbuyers surveyed were asked what factors might make them more likely to consider buying an annuity over the Internet without involving their own agent or advisor:

- Nearly one in three said they wanted the ability to compare products offered by different companies on one site.

- One in four would expect a discount after eliminating the intermediary.

- One in four would buy online if they could speak with a licensed advisor during the sales process to answer questions.

- About one in five said they would want a single point of contact at the company in case they need more information.

That said, the percentage of respondents going to insurance carrier websites for information on annuities is lower than those using other Internet sources, our survey found. And given that nonindustry online sources are often replete with mixed reviews on annuities, it is important for insurers to find ways to drive more traffic to their own websites, which could help them better control the messaging about their products. One way providers could achieve this might be to add elements of scenario analysis to their sites, fueled by tools that help calculate how much buyers can earn from an annuity while illustrating potential advantages over alternative investment options.

The case for selling annuities directly to consumers over the Internet is more nuanced. On the one hand, our survey revealed that only 17 percent of current annuity owners were either somewhat or very likely to consider buying another annuity directly over the Internet, without a professional financial intermediary shopping for them or advising them. However, this percentage swelled to 45 percent in the case of buyers who were 30–44 years old, which should prompt providers to experiment with direct sales, at least to younger prospects (figure 5).

To avoid potential channel conflict, any direct outreach efforts could conclude with the suggestion, “Ask your financial advisor if an annuity is right for you,” along with a service to connect interested prospects with an affiliated intermediary. However, a carrier could also offer the option to speak with one of its in-house customer service representatives if a prospect prefers that option.

Call to action

- Be far more proactive with external communication efforts, and reexamine traditional methods and channels for promoting and defending annuities with the media and general public.

- Go beyond awareness building, focusing more on articulating the unique benefits of annuities and perhaps countering various criticisms of the product’s value versus the alternatives. This might be easier to accomplish if carriers and their associations join forces and consolidate resources to present a united front, perhaps even around a single spokesperson.

- Explore the potential for interacting directly with consumers online, particularly with younger prospects, to either initiate a sale or cultivate a warm lead for intermediaries.

Leverage the workplace channel

Deloitte’s survey focused primarily on opportunities to increase individual annuity sales through financial advisors and agents, rather than on making group sales through the work site channel. However, recent market developments and regulatory changes are facilitating and even encouraging an expansion of the annuities market—both group and individual—via employer-based platforms.

Among those surveyed, a number of respondents spontaneously cited the work site channel as a potential motivator in spurring a future annuity purchase. Along these lines, respondents suggested that annuity writers “work with employers as part of benefit packages” and “encourage employers to recommend them.” Others said, “My employer should help me understand this option.”

Over the past few years, a number of carriers have bolstered their annuity sales on a large scale by executing pension risk transfer deals, in which insurers take over the longevity exposure of an employer’s defined benefit plan via a group annuity arrangement. The number of such buyouts rose 28 percent to 277 last year, while the value of the transfers more than doubled to $8.5 billion, according to LIMRA’s Secure Retirement Institute.6

Over the longer term, the accelerating transition from defined benefit to defined contribution plans, along with changes in investment regulations for consumer-driven retirement accounts, makes the 401(k) market a natural conduit for annuities writers to connect with more individuals looking for longevity solutions. Indeed, the work site offers an opportunity to reach prospects who are prime candidates to roll over at least part of their retirement savings to secure guaranteed lifetime income protection via an annuity.

Until recently, opportunities to buy annuities as part of employer-sponsored retirement plans were quite limited. As a result, interest among annuities prospects for workplace sales is underdeveloped. Among the nonbuyers we surveyed, just 14 percent of those aged 30–44 and 17 percent of those aged 45–54 said that they might purchase an annuity in the next five years if their employer offered them the opportunity to buy one through their benefit plan.

However, recent federal regulatory actions may help generate more interest in the annuity option through the workplace channel. For example, in July 2014, the Internal Revenue Service (IRS) issued new rules allowing individuals to buy longevity annuities—a type of deferred income annuity that begins payments at an advanced age—in both their 401(k) and individual retirement accounts (IRAs).7

The IRS also put out a notice in 2014 allowing employers to include deferred-income annuities in target date funds used as a default investment option in 401(k) plans. The Department of Labor (DOL) followed up with a letter of its own confirming that possibility.8 The DOL letter lays out how plan sponsors can meet fiduciary standards when appointing an investment manager to select specific annuity products and providers to meet the lifetime income guarantee.

“As Boomers approach retirement, and life expectancies increase, income annuities can be an important planning tool for a secure retirement,” says J. Mark Iwry, deputy assistant Treasury secretary for retirement and health policy. “By encouraging the use of income annuities, [Treasury’s] guidance can help retirees protect themselves from outliving their savings.”9

Target date funds, which automatically reallocate investments from equities to less volatile fixed-income securities as plan participants approach their intended retirement year, are often included as a default investment for those who do not make the effort to elect a choice on their own. The new IRS/DOL policy allows target date funds to include annuities as part of a fund’s fixed-income investments—on a voluntary or default basis—set up to make payments to beneficiaries either immediately upon retirement or some number of years afterwards. In this way, a portion of an employee’s retirement savings can be put toward an annuity offering guaranteed income for life, while the rest can be put toward other investments.

The appeal of a partial annuitization scenario in defined benefit plan distributions was highlighted in a study published in the Journal of Economic Research in August 2014.10 The survey found that, in a hypothetical purchasing situation, allowing individuals to annuitize a fraction of their defined benefit plan would increase the potential for annuitization, as opposed to an “all-or-nothing” situation in which a beneficiary has to choose between a complete annuitization versus a lump sum distribution. When offered a choice of partial annuitization, the percentage of those hypothetically choosing to annuitize increased from 50 percent to 80 percent.

Even if plan sponsors decide to include annuities as an investment option rather than an automated default choice, the potential increase in annuities’ availability through workplace plans could still put annuity carriers in a prime position to better educate employees about the need for reliable retirement income streams, as well as increase the potential for annuity products to meet that demand.

Eventually, carriers and consumers alike could benefit from having a requirement in place that 401(k) and other defined contribution plans at least offer an annuity-driven lifetime income option, although this would require additional regulatory changes. At some point, perhaps 401(k) and IRA statements could go beyond reporting how many total dollars are in a retirement account to explain and model how beneficiaries might generate a regular income over their lifetime with an annuity product, similar to the lifetime income statements included in Social Security benefit reports.

Call to action

- Carriers with sufficient capital and risk appetite could absorb large numbers of longevity risks in one fell swoop via pension risk transfers. This trend will likely accelerate over the next few years as a growing number of employers with defined benefit plans seek to remove longevity risks from their balance sheets.

- Consider partial annuitization offerings for defined benefit plan distributions. The efficacy of a partial annuitization proposition, rather than an “all-or-nothing” scenario in which beneficiaries must choose between a lump sum or full annuitization, has been shown to increase the appeal of annuities to a broader client base.

- Over the long term, a major opportunity to expand individual sales could come through workplace marketing, with annuities assuming a much higher profile as an option for both 401(k) portfolios and IRA rollovers thanks to changes in federal regulations facilitating such choices.

Where do annuities writers go from here?

The annuities market remains in a state of flux. A number of competitors have left the market or cut back their presence considerably during the current prolonged low-interest-rate period. Those still fully engaged are focused on optimizing their product mix and carving out a bigger share of the traditional annuities market pie.

Yet on a fundamental level, the more the annuities market has changed, the more it has remained the same in many ways. Our research tells us that most annuities writers persist in chasing the same kinds of prospects—mostly older and closer to retirement—while bypassing younger prospects who are just starting to build their nest eggs. Insurers also continue to rely very heavily on intermediaries to get the message out about the purpose and value of their products. Meanwhile, annuities are still a mystery to most buyers, let alone nonbuyers, which could discourage referrals and make it difficult to cultivate new prospects.

This status quo is unlikely to remain viable over the long haul for insurers seeking opportunities for bigger, more consistent annuities growth. Companies should try to change this dynamic by developing a new mind-set to break free of the constraints—both internal and external—that are inhibiting a robust expansion in prospective buyers and, ultimately, sales. Annuities writers should therefore consider taking a multipronged approach to transforming their standard operating procedures by:

- More effectively leveraging current client relationships with advanced analytics, targeting both existing annuities buyers and those with related financial products

- Seeding the field for their distribution force with more direct communication and education efforts that increase awareness of how annuities function and the value they offer, particularly compared with other investment options

- Creating more flexible products, some of which are simplified or offer solutions beyond retirement financing

- Upgrading work site marketing and sales efforts to expand both the group and individual annuities markets

- Building bridges to younger generations through targeted marketing and new channels, both to broaden the pool of prospects and to set the stage for repeat sales later in the financial life cycle

Over the long term, instead of competing in a zero-sum market share battle over the same narrow target segments, carriers should be rethinking their business models to appeal to a wider array of consumers, create a more receptive audience for their messaging, and ultimately make a more compelling case for buying an annuity. That way, they stand a stronger chance of expanding the available market while differentiating their brand in the process.

About the Center for Financial Services

The Deloitte Center for Financial Services (DCFS), part of the firm’s US financial services practice, is a source of up-to-the-minute insights on the most important issues facing senior-level decision makers within banks, capital markets firms, mutual fund companies, investment management firms, insurance carriers, and real estate organizations.

We offer an integrated view of financial services issues, delivered through a mix of research, industry events, and roundtables, and provocative thought leadership—all tailored to specific organizational roles and functions.

Deloitte Consulting LLP’s financial services industry practice brings together multidisciplinary capabilities and teams of client service professionals with diverse experience and knowledge in order to provide customized solutions for banks, securities firms, insurance companies, investment management firms, and real estate services companies in the United States and around the world. Our life and annuity practice brings depth and breadth of experience in business strategy, product management, asset management, operations, human capital, and technology services.