US shale: A game of choices has been saved

US shale: A game of choices

03 September 2014

An interactive community of value chains—an ecosystem—can help oil and gas companies effectively manage the rapidly evolving shale market in the United States.

The changing rules of the game

The US shale boom began quietly, but when its time came, it grew quickly. After almost two decades of experimentation in a field in North Texas, the industry underwent a full-blown revolution in just a few years. Record levels of investment flooded into what many had considered one of the world’s most mature energy markets, drawing oil and gas multinationals (supermajors and international exploration and production companies) back to the United States and boosting the country’s oil and gas output by almost 40 percent from 2006 to 2013.1 Seeing the United States’ success, countries such as Argentina, China, and Poland have started exploring their shale potential.2

The boom, surprisingly, changed course when US natural gas (“gas”) prices plummeted to historic lows in 2012. Gas-oriented companies generated weaker-than-expected returns, and a series of multibillion-dollar asset write-downs followed.3 With gas in a slump, all eyes turned to liquids (crude oil, condensates, and natural gas liquids). Although US West Texas Intermediate (WTI) crude prices remained above breakeven levels, intense competition and the problem of excess also gripped the US liquids market. WTI continues to trade at a discount to North Sea Brent, despite reversals of existing pipelines and the opening of new ones in the United States. As a result, select companies have decided to sell their marginal US liquids-rich shale assets to offset corporate capital constraints.4

These ongoing, hard-to-predict changes in the US shale market have not only made decision making complex, but also upended the conventional business strategies of oil and gas companies operating in the region. For example, BP recently decided to form a separate business to manage its onshore oil and gas assets in the United States, which, according to the company, have “unique characteristics.”5

The lack of predictability in the US shale environment has put several questions in front of oil and gas companies and their stakeholders. How will the shale boom unfold over the next few years? How will the evolution in shale progress across the energy value chain and shape the industry’s structure? How can companies refine their approach and play to their segment level and cross-segment strengths? To answer those questions, companies will need to consider the evolution of the US shale game and the resulting impacts.

“With the rapidly evolving (shale) environment, our (BP) business has become less competitive. The new business (the US onshore business unit) will have separate government, processes, and systems designed to improve the competitiveness of its portfolio.” —Source: BP, Investor update 2014, March 4, 2014.

2006–2010: Ante up or sit out

Domestic exploration and production (E&P) companies cracked the code for large-scale shale gas extraction by 2005, offering the promise of growth in the United States. As the shale revolution was unfolding at home, multinationals remained focused on mega projects in the Middle East, Africa, Brazil, US Gulf of Mexico, and Asia—in part because of the uncertainty around the potential and economic viability of US shales.

Thanks to the innovative resource development efforts of domestic E&P companies, US shale began delivering on its promise: Shale gas production more than quadrupled to 3.5 trillion cubic feet (Tcf) from 2005 to 2009.6 Just as the production boom began to catch the attention of multinationals, however, a decline in prices due to economic slowdown and the non-readiness of new demand made them wary. These companies faced a dilemma: Invest in shale or risk being sidelined during a domestic boom. Like a card player approaching the table, they had to decide whether to “ante up” or “sit out” what was becoming the hottest game in the industry.

Domestic E&P companies anted up. They entered early by investing organically, which resulted in a sharp increase in their reserve additions. The US reserve replacement rate (RRR) of select domestic E&P companies averaged between 300 to 500 percent (represented by the light blue dots in the top right quadrant of figure 1) from 2006 to 2010.7 Seeing the growth of these domestic E&P companies, select supermajors and many international E&P companies bought significant shale acreage and reserves in 2009 and 2010, making them attain RRR of above 100 percent in the United States (represented by the dark blue and green dots in the bottom right quadrant of figure 1).

Select oil-heavy supermajors, however, largely chose to sit out and remained focused on deepwater offshore fields. Their purchases in US shales—less than $6 billion each—were not substantial relative to their size and not significant enough to arrest the fall in their US oil and gas reserves. They therefore recorded low RRR in the United States (represented by the dark blue dots in the bottom left quadrant of figure 1). In sum, nearly all domestic E&P companies anted up early, while multinationals entered late and were divided in their US shale strategy from 2006 to 2010.

2011-2013: Betting on profitable liquids or inexpensive gas

By 2011, the US natural gas market had reached a level that surprised almost everyone in the industry. In just two years’ time from 2009 to 2011, production of shale gas had more than doubled, reaching 8 Tcf. The result was a rare dichotomy: Gas prices fell as oil prices rose. The oil-to-gas price ratio increased to 24 in 2011 from 16 in 2009.8

This decoupling of prices dealt oil and gas companies a new hand, and with it, a choice: Switch to premium-priced liquids or invest in inexpensive shale gas for the long term. This second round of choices, coming just five years into the boom, created a conundrum for many oil and gas companies. They either had to change their operating model—especially gas-heavy companies switching to liquids—or “double down” on gas, where prices did not justify expenditures, and forego potential profits from shale oil.

Like players shuffling their cards in the middle of the game, oil and gas companies altered their strategies. Between 2011 and 2013, gas-heavy domestic E&P companies such as EOG Resources and Chesapeake Energy shifted their drilling and production focus toward liquids, which accounted for nearly 100 percent of their reserve additions.9 This shift to liquids changed not only their revenue and margin mix, but also their midstream contracting and their end users’ profile. Select oil-heavy supermajors that had chosen to “sit out” the first round added less liquids reserves (figure 2).

As companies scrambled to adjust their strategies, a flurry of acquisition activity ensued. More than 16 million undeveloped shale acres changed hands—almost 70 percent of it in oil and liquids-rich shale plays. Deal values topped $35 per proved barrel of oil equivalent (BOE) in select shale oil fields, compared with the highest deal value of $22 per BOE in 2008.10

Although the players raised the stakes, their profits remained far behind their growth. Like what happened with domestic gas, the sharp increase in supply started depressing liquids prices relative to prices in international markets. This fall in the domestic gas prices and discounted liquids weighed on companies’ premium purchases and led to multibillion-dollar write-downs in 2013, even forcing some companies to sell their marginal liquids-rich assets to cover for capital constraints.11 For example, BHP Billiton decided to sell roughly half of its less promising liquids acreage in west Texas.12

2014: New cards on the table

The evolution of the shale game can be illustrated by drawing decision lines across the production and price curves for oil and gas (figure 3). The game started in 2005, when oil and gas prices were in equilibrium at a 6:1 ratio (the common starting point in figure 3). In the first round of the game, from 2006 to 2010, the relative strength of oil prices discouraged some from investing in low-priced natural gas (“sit out”), while rising shale gas volumes encouraged others to invest in gas despite price weakness (“ante up”). As the game evolved and prices decoupled, from 2011 to 2013, the lowest gas prices in a decade pushed the early entrants in shale gas to switch to liquids-rich plays, while the companies that sat out in the first phase moved to take advantage of the situation by buying into inexpensive gas. Due to the steep fall in gas prices, average deal value in gas plays fell by nearly 50 percent, from about $2 per proved thousand cubic feet equivalent (Mcfe) in 2008 to $1 per Mcfe in 2012.13

Companies must now plan for the next set of choices, given the flip in prices and production. Because of rising shale oil supplies and weak global demand, oil futures are in backwardation—December 2014 WTI oil futures are about 2.5 percent lower than August futures—and the Brent-WTI price gap remains above $5 a barrel despite the start of new pipelines from Cushing, Oklahoma.14 In contrast, domestic gas prices have bottomed out and the forward curve is in contango, as the growth rate in production has moderated.

In the US onshore liquids value chain, oil upstream will continue to remain the preferred choice. Although the US oil downstream, or oil refining, is currently running at record levels, the probability of seeing large new refineries in the country is low because of stricter environmental regulations, a mature domestic demand base, uncertainty about crude oil exports, and rising competition from new low-cost refineries worldwide.15

On the gas side, a new choice is emerging—one that is not limited to gas producers or the gas upstream segment. Although the recent upward price movement suggests that gas prices bottomed out in 2012, they are still only at one-third of their peak levels and are projected to remain below $5.25 per million British thermal units (MMBtu) until 2025 in real terms (2012 dollars).16 This continued weakness in gas prices has shifted profits from the gas upstream segment to the gas downstream segment: consumers or buyers of (liquified natural gas [LNG] and petrochemicals, from an oil and gas industry perspective).

Domestic E&P companies are generally best suited for these conditions because of their smaller capital structure, which supports lower profits per barrel and enables them to move swiftly across emerging drilling prospects. Select E&P companies, for example, also have a proprietary database for all hydraulic fracturing specifications for more than 5,000 wells, which they will continue to “slice and dice” to find the new bottom of the cost curve.This margin migration is evident in the rise in total shareholder returns of the gas downstream segment. The Standard & Poor’s (S&P) Composite Chemicals index outperformed the S&P Composite E&P index by almost 25 percent, and the stock price of the largest stand-alone US LNG exporter rose by 400 percent from 2012 to 2013.17 As of July 31, 2014, more than 35 LNG export applications were on file with the US Department of Energy for approval, and almost 150 chemical projects have been announced in the United States—highlighting the extent of the growth opportunities and margin migration toward the gas downstream.18

In sum, the kink in price and production curves suggest the coming of a third set of choices for oil and gas companies operating in the US onshore market—shale oil upstream or the gas downstream. Given the competition for capital in the oil and gas industry and the need to prioritize each dollar, the investment decisions companies make in 2014 will likely be key to the industry’s long-term profitability and business model.

Dealing new cards

Shale oil is the fastest-growing resource in the United States because of the advantaged oil-to-gas price ratio. However, this fast growth will likely make the shale oil market more fragmented and less differentiated—much like the current domestic shale gas market. Consider the effect of more than 500 independents drilling for the same oil in the same market.19 The competition in this market will intensify over the next few years as the growth rate slows down and turns negative because of the depletion of “sweet spots”. Deloitte MarketPoint LLC estimates that US unconventional oil production will peak by 2020 at about 4.5 million barrels a day (MMbbl/d).20

On the other hand, US shale gas production is projected to revive after 2016 and double to 20 Tcf by 2040.21 This strength in shale gas and associated natural gas liquids (NGLs) production will depend on large-scale investments in “the” US gas downstream. According to the EIA, 33 percent of the increase in US shale gas and 85 percent of the growth in US NGLs will be driven by the growth in LNG and petrochemicals, respectively, from 2011 to 2025 (figure 4). The price differential between global oil (or oil-linked global gas) and US gas is projected to remain far above the equilibrium price level of 6:1, ranging between 18:1 to 26:1 until 2040. According to Sasol’s CEO, the company’s proposed new ethane cracker in Louisiana can afford for the ratio to go as low as 16:1.22 This will continue to provide the US petrochemical and LNG export industries a profound and sustainable competitive advantage for the foreseeable future.

The cost to produce ethylene (the base petrochemical product) in the United States is now the second-lowest in the world because of low prices for feedstock, power, and fuel, which constitute 65 percent to 85 percent of the production cost.23 The fact that more than $100 billion in investment is finding its way into the US petrochemicals segment is a testament to the value and affordability of America’s shale gas and ethane supplies.24

The other half of the US gas downstream segment, the LNG business, shares a positive outlook similar to that of petrochemicals. The LNG business benefits from not just the advantaged gas price but also the lower capital costs associated with the conversion of existing regasification terminals. In contrast to costly greenfield international LNG projects, US brownfield conversion projects are 1.5 to 2.5 times cheaper. The conversion also provides timing, construction, and operating cost advantages over new projects, which are plagued by cost inflation.25

In sum, the gas downstream segment is poised to be the US oil and gas industry’s biggest long-term advancement since the development of shale gas. However, unlike the shale oil market, where pure-play E&P companies would continue to lead development, the gas downstream segment will likely have a diverse set of industry participants. For example, supermajors, domestic pure plays (like Dow Chemical and LyondellBasell), and international chemical companies (like Sasol and Formosa Plastics) will likely compete for the sizeable growth opportunities in the US petrochemical industry. On the other hand, the US LNG export market will have a new set of competitors for upstream players—midstream companies, domestic utilities, and foreign diversified entities, which together represent more than 85 percent of the proposed US LNG export capacity. Knowing that each participant will aim for a competitive lead, it will be interesting to see how they seize these opportunities, deal with each other, and shape the US oil and gas industry.

Petrochemicals: A competitive United States

Oil-based naphtha is projected to remain the prime feedstock for the global petrochemical industry, and hence will continue to be the ethylene price-setter. These oil-linked product (ethylene and its derivatives) prices and the cost of gas-linked feedstock (NGLs) will keep the competitiveness of the US petrochemical industry intact for the foreseeable future.

Price makers are high on the cost curve: Global ethylene prices are largely set by oil-based crackers in Asia and Europe, which represent more than 65 percent of global ethylene capacity. The proportion of US ethane-based crackers would remain less than 27.5 percent, even if all of the proposed 12.5 MMTPA of low-cost ethylene capacity is added in the United States and no capacity expansion is considered worldwide.

A significant price cushion is available to US ethane-based crackers: The ethylene cash costs of US ethane-based crackers are nearly one-fourth of those of global naphtha-based crackers. For the cash costs of both to be equal, ceteris paribus, US ethane prices would need to increase by 4 to 5 times over July 2014 price levels.

LNG: Advantage to the United States

The landed cost (including a 15 percent before-tax internal rate of return) of US natural gas in Japan is estimated to be $10 to $11 per thousand cubic feet (Mcf), $1 to $2.50 lower than Australian and Canadian exports despite higher shipping costs via the Panama Canal.

Lowest downstream capital cost: Brownfield LNG projects in the United States provide a significant downstream cost advantage over their brethren in Australia and Canada. US LNG projects cost around $800 per million metric tons per annum (MTPA) of LNG capacity, compared with $1,500 to $1,700 per MTPA in Australia and $1,000 to 1,500 per MTPA in Canada.

Reducing upstream supply cost: Among the three regions, Australia has the lowest upstream supply cost because of large offshore fields that reduce the number of wells required. However, the large-scale development and adoption of new technologies in the United States has increased the economic ultimate recovery (EUR) of shale plays such as Marcellus to more than 10 billion cubic feet (Bcf) and reduced the cost to drill and complete a well to less than $7 million.

Building a winning hand

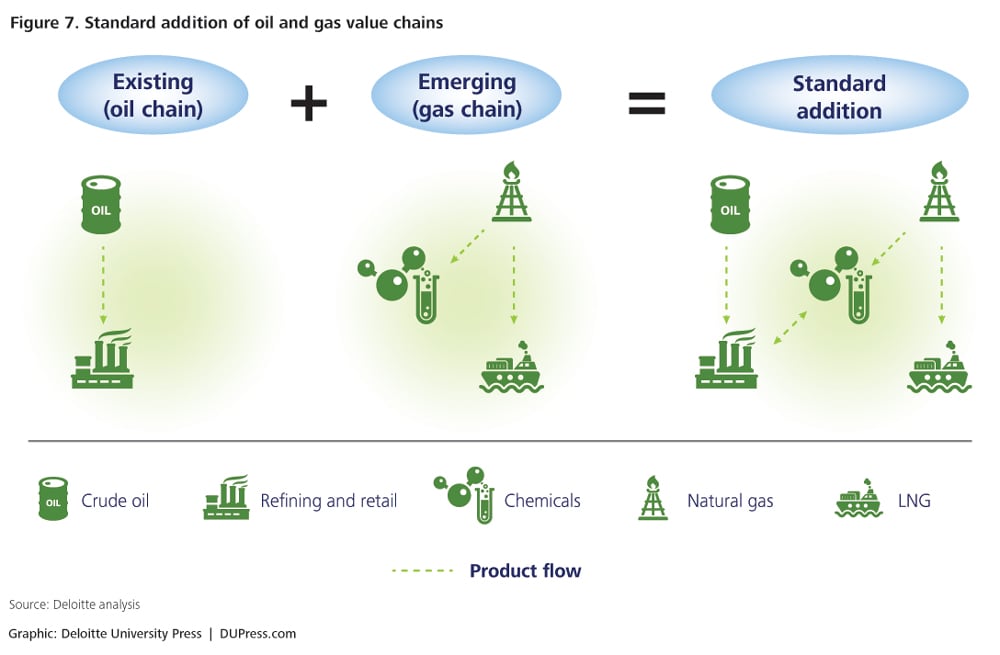

With the coming of the gas downstream segment, or the emergence of the full gas value chain, the United States could be one of the few countries holding a “royal flush,” with advantages ranging from a worldwide competitive position in oil and gas upstream to refining, LNG, and petrochemicals. However, a simple addition of all the segments would only bring “standard” benefits.

A standard addition links multiple segments primarily through product transfers (figure 7). These transfers were once considered essential for the industry. Paul Frankel, often referred to as the father of petroleum economics, argued in his 1946 book Essentials of Petroleum that these transfers maximize profits, reduce risk, and create stability in an intrinsically unstable and non-self-adjusting industry.26

The development of a free and actively traded spot market has undermined the benefits of product transfers—especially for primary, easily transported oil products such as crude oil, gasoline, and distillates. These changes meant that an upstream oil producer or a refining unit could easily dispose of and buy supplies in the open market. A refiner now typically pays the same price whether it buys from its own upstream unit or from outside the company. As a result, a standard addition only offers marginal benefits—primarily savings from the common use of selling, general, and administrative costs, which is only 1 to 3 percent of many companies’ sales.27 This and the perceived benefit of focus and market preference for pure plays explain why a number of integrated companies are segregating and becoming pure-play specialists.

The US gas market is still in “adjustment” mode because of transportation bottlenecks, demand-supply imbalance, and price variance between shale plays. Although in the current situation, there could be a case for owning the full gas chain and capturing the total margin or price arbitrage, the market, similar to oil, will likely self-adjust in the medium to long term. An interconnected network across shale plays, increased tradability of gas products, and a number of highly competitive pure plays across each segment would marginalize the benefits of gas integration, at least for investors.

These pure plays are what investors often want in order to take advantage of the volatility and market disruption that occurs between segments. However, multiple shale factors in play are likely to drive unforeseen margin migration between segments, raising the risk of overinvesting in one while negating the growth prospects of the other. In 2006, for example, large shale-heavy oil and gas producers in the United States reported operating margins of about 45 percent; by 2012, typical margins had dropped to about 20 percent. On the other hand, the margins of typical US petrochemical producers nearly doubled, shifting investments from upstream to downstream. But in the first six months of 2014, a rally in gas prices of about 30 percent over the 2013 average, primarily due to extreme winters, reversed some of the gains of the gas downstream. Such imbalanced growth and volatile prices create disequilibrium in the industry, leading to an unstable industry scenario.

This instability may further increase because there are now multiple sources, multiple grades, multiple processes, multiple end uses, and multiple fuel prices in the United States. The US shale boom is now spread over 20 active shale basins producing multiple grades of crude and variable ethane/propane mix, unlike the standard grades of the past. Small-sized plants such as crude oil topping units, propane dehydrogenation plants, and condensate splitters are gaining traction and offering new downstream opportunities. Fuels (gas and coal in power, NGLs and naphtha in chemicals, gas and fuel oil in refining, diesel and natural gas in transportation) are becoming substitutable and prices are fast decoupling, making fuel switching rampant among end users.

Considering these changes, integrated companies that simply add value chains, or pure plays that pursue stand-alone strategies, may end up creating a parallel and underutilized infrastructure, skewing investments to only one segment, stretching balance sheets, and sinking returns during rough price cycles. In other words, such behavior may repeat the problems of surplus witnessed in the first two rounds of the game.

Considering these changes, integrated companies that simply add value chains, or pure plays that pursue stand-alone strategies, may end up creating a parallel and underutilized infrastructure, skewing investments to only one segment, stretching balance sheets, and sinking returns during rough price cycles. In other words, such behavior may repeat the problems of surplus witnessed in the first two rounds of the game.

To overcome these challenges, oil and gas companies need to come together to build an interactive community of value chains—an ecosystem—that maximizes the benefits of a rapidly evolving shale market by synchronizing the growth of all interdependent segments of the industry. A strategic ecosystem can retain the flexibility of being an investor’s favored pure-play structure and simultaneously harness cross-segment operational synergies—focusing more on reaping benefits through collaboration and less on owning the value chain, allowing each company to do what it does best (figure 8).

How can companies build this kind of stronger oil and gas ecosystem? How can industry participants exploit the opportunities in shale together?

The three Fs: The building blocks of an ecosystem

A standard value chain is characterized by product transfers, incremental value addition, and limited intersegment synergies. But a strategic ecosystem can be defined as a network of segments that maximizes (financial) value for segments; connects processes, creates new products, and provides supply (feedstock) flexibility; and unifies the disjointed asset base (facilities) of the industry—the “three Fs.”

Playing all hands together

The transition from standard value chain addition to a strategic ecosystem requires establishing beneficial dependencies between segments. These dependencies are not just about developing product flows, but creating a web of optimized processes, technologies, transportation and storage, supply chain, talent, real estate, and capital project delivery solutions across all segments.

Oil and gas companies can create this web of interlocked assets by following a capex-light, flexible investment strategy that encourages collaboration. Rather than each company owning and creating a parallel infrastructure, oil and gas companies can form marketing alliances, share technology and infrastructure, enter into offtake and service agreements, connect inputs and yields of facilities, and safeguard supplies and margins through strategic partnerships and joint ventures.

This type of collaboration would yield results if it is primary to a company’s decision making and adopted industry-wide, rather than being ancillary or limited to a few companies as it is currently. Fortunately, the addition of the gas downstream segment has presented many avenues for collaboration and incented more participants to establish new linkages across all industry segments (figures 9 and 10).

A chemical unit, for example, could collaborate with a light crude processing unit or a mini-refinery to absorb the latter’s naphtha output and enhance the associated production of chemical feeds such as propylene. Similarly, NGLs processors could increasingly enter into dynamic ethane/propane supply agreements with chemical companies, allowing the latter to switch between ethane and propane in real time depending on the market and price conditions of its derivative products.

Midstream companies could take a larger role in interlocking upstream and downstream assets, due to their larger size and reach across shale plays. Apart from shouldering the capex burden, they could offer contracting and feedstock flexibility to upstream and downstream companies. Further, midstream companies could configure their offering—creating “pseudo crudes”—by blending new crudes in real time with the help of an upstream company and providing “grade on demand” flexibility to refiners. Similarly, the NGLs extraction from natural gas and LNG liquefaction share multi-staged cooling and feed-splitting processes, offering an opportunity to midstream and gas downstream segments to collaborate.

Upstream participants and supermajors can progressively enter into a lease or subscription contract for midstream and utility companies’ US LNG capacity. Shell and Kinder Morgan’s agreement to modify the existing Elba Express Pipeline and Elba Island LNG Terminal is an example of such cross-segment collaboration. Under this agreement, the Kinder Morgan group will own 51 percent of the entity and operate the facility. Shell will own the remaining 49 percent and fully subscribe the liquefaction capacity. The project will use Shell’s innovative small-scale liquefaction unit, which will be integrated with the existing Elba Island facility and enable rapid construction, allowing Kinder Morgan to derive new value from its existing asset base.28

Supermajors and international E&P companies could widely market their global re-gasification terminals, swap interest in global LNG projects, and offer their global supply and trading experience to US midstream companies. By doing this, they can benefit from the growing trade of LNG in the spot market. In 2012, the spot and short-term LNG market reached 31 percent of total volumes, up from less than 5 percent in 2000.29 This shift toward the spot market is likely to increase as US companies begin exporting LNG, more buyers seek destination flexibility clauses, trading desks are established, and re-export of LNG increases worldwide.

In sum, the potential benefits of this new style of collaboration are limitless. It may not only drive growth across all oil and gas segments, but also help to make America’s energy industry stronger.

Coming up aces

The US shale boom has opened the doors for growth across the two primary segments of the oil and gas industry. This growth started in oil and gas upstream business through the development of shale gas and shale oil, and it is now moving to downstream petrochemicals and LNG businesses. This new gas-heavy face of the downstream segment will feed on advantaged domestic gas and its co-products, less-pricey conversion and expansion of existing facilities, and price arbitrage between the United States and international markets.

With growth comes increased competition—especially given that the United States has many pure-play specialists operating domestically and integrated companies with global operations—and a need to prioritize scarce capital. Foreseeing this challenge, US oil and gas businesses could work toward establishing a capex-light ecosystem that retains the flexibility of the pure-play structure favored by investors while simultaneously harnessing cross-segment operational synergies of an integrated structure. In other words, they could work toward creating a resource-centric oil and gas ecosystem in which assets, operations, talent, and support functions interlock across businesses.

Such an ecosystem can help the US oil and gas industry to sustain its competitiveness even if the current hydrocarbon price or feedstock cost advantage starts narrowing or ceases to exist. Together, ecosystem participants can also withstand the unforeseen margin migration between segments, which will likely become common as players in the United States free themselves of the “one source, one grade, one process, one end use, and one price” mindset. Luckily, the promise of the gas downstream segment and its addition to the existing oil value chain has presented new opportunities for collaboration to shape this ecosystem in the United States.

Deloitte offers audit and enterprise risk, tax, consulting, and financial advisory services to companies across the oil and gas industry. Specialty services include resource evaluation and advisory services, capital projects services, merger and acquisition services, and services from dedicated groups including Deloitte Energy Advisors, Deloitte MarketPoint, the Petroleum Services Group, and Vigilant by Deloitte. Reach out to the contacts listed in this report for more information or read more about our oil and gas industry practice on www.deloitte.com/us/oilandgas.

Glossary of terms

| Associated natural gas production | Associated gas refers to the dry natural gas extracted as an additional product while drilling for oil or NGLs. |

| Condensates | Condensates refer to light liquid hydrocarbons recovered from lease separators or field facilities at associated and non-associated natural gas wells, mostly pentanes and heavier hydrocarbons, which normally enter the crude oil stream after production. |

| Cracker | Cracking is the process whereby complex organic molecules are broken down into simpler molecules. |

| Downstream | Downstream companies include facility-based businesses engaged in the conversion of raw hydrocarbons into finished products (here, refining, chemicals, and LNG). |

| Estimated ultimate recovery (EUR) | Estimated ultimate recovery (EUR) is an approximation of the quantity of oil or gas that is potentially recoverable or has already been recovered from a reserve or well. |

| Ethane | Ethane is a straight-chain saturated (paraffinic) hydrocarbon extracted predominantly from the natural gas stream, which is gaseous at standard temperature and pressure. It is a colorless gas that boils at a temperature of -127 degrees Fahrenheit. |

| Feedstock | Feedstock refers to any unprocessed material used to supply a manufacturing process. |

| Hydraulic fracturing | Hydraulic fracturing, commonly known as fracking, is the technique of creating fractures in rocks and rock formations by injecting fracking fluids into the cracks to extract petroleum, natural gas, or other substances. The method is widely used in shale gas production in the United States. |

| Independents | Independents are companies in the upstream part of the energy value chain engaged in exploration and production of oil and natural gas. |

| Liquefaction | To move natural gas across oceans, it is converted into liquefied natural gas (LNG), a process called liquefaction. LNG is natural gas that has been cooled to –260° F (–162° C), changing it from a gas into a liquid that is 1/600th of its original volume. |

| Liquids-rich shale plays | Liquids-rich shale plays are shale formations that contain natural gas with high NGLs content. The NGLs content of liquids-rich shale plays ranges from 2.5 to 5.3 gallons per Mcf. |

| Midstream | Midstream refers to companies involved in the gathering, processing, transporting via pipelines, and storage of natural gas and liquids. |

| NGLs | NGLs are higher hydrocarbons such as ethane, propane, butane, and natural gasoline (pentanes plus). NGLs typically have higher energy content and are denser than dry gas. |

| Regasification | At regasification terminals, liquefied natural gas delivered by LNG tankers is returned to the gaseous state. |

| Reserve replacement rate (RRR) | The reserve-replacement ratio measures the amount of proved reserves added to a company’s reserve base during the year relative to the amount of oil and gas produced. A rate of above 100 percent suggests a net addition of reserves, while a ratio of below 100 percent means a net depletion of reserves. |

| Shale gas | Shale gas is natural gas trapped within shale formations (a fine-grained, sedimentary rock). Shale gas has become an increasingly important source of natural gas in the United States over the past decade. |

| Shale oil/tight oil | Tight oil refers to the light crude oil trapped in shale, limestone, and sandstone formations characterized by very low porosity and permeability. It may also be called light tight oil (LTO), tight shale oil, or even shale oil. |

| Shale play | A set of known or postulated oil and gas accumulations sharing similar geologic, geographic, and temporal properties, such as source rock, migration pathway, timing, trapping mechanism, and hydrocarbon type. |

| Specialists | Specialists refer to companies operating in one segment. |

| Supermajors | Supermajors is a name used to describe the world’s five largest publicly owned, integrated oil and gas companies with operations worldwide. |

| Sweet spots | Sweet spots refer to the highest-producing shale plays/fields. |

| Unconventionals | An umbrella term for oil and natural gas that is produced by means that do not meet the criteria for conventional production. This primarily includes oil sands, shale oil, and shale gas. |

| Upstream | Upstream companies are those engaged in the exploration and production of crude oil, natural gas, and natural gas liquids. |