Rising tide has been saved

Rising tide Exploring pathways to growth in the mobile semiconductor industry

07 November 2013

- Scott Wilson, PhD

To compete in the mobile 4G era, it will be important for companies to transition from traditional, closed business models to a more open, collaborative approach.

Foreword: Why read this report?

Last year, Deloitte TMT released its Open Mobile 2012 study, which showcased selected findings from a highly targeted survey of senior executives in and around the mobile ecosystem. Our research highlights a broad range of opinions on the opportunities and challenges associated with sustaining top-line growth across and beyond the industry in the immediate three- to five-year time frame. In particular, the study explored the impact that the accelerated development of mobile web technology, changing consumer behavior, and a shifting regulatory policy landscape are having on the issues of competitiveness, growth, and innovation.

With the release of this latest report, also part of our ongoing Open Mobile series, we present a new study—this time focused on the mobile semiconductor industry. With semiconductor companies increasingly having a major impact on all facets of the mobile ecosystem, Deloitte Research explores the leading-edge growth strategies and capabilities that semiconductor firms are using to sustain market leadership and capitalize on new mobile opportunities.

Semiconductor and mobile technology executives will find this report useful in two ways. To begin with, we present a comprehensive overview of the mobile semiconductor ecosystem. Specifically, we highlight, discuss, and synthesize projected growth trends and end-market data to present a new analysis of the mobile semiconductor competitive landscape. Having identified the emerging growth opportunities, we then switch focus to the enterprise level and explore the challenges companies face when executing mobile business model innovation to act on these opportunities. Case studies are presented analyzing several leading semiconductor companies’ approaches to using open innovation and platform leadership strategies in emerging mobile growth markets. Insights and findings from the case studies are then used to inform executive guidance, the core of which is a diagnostic model to assess the development and maturity of mobile platform innovation capabilities.

About the Deloitte Research Open Mobile series

Since 2009, the Deloitte Research Technology, Media, and Telecommunications (TMT) team has explored the advent of the open mobile era and the subsequent shifting competitive landscape in the United States and global mobile markets. The team has produced a number of research reports on a wide range of strategic issues that mobile technology companies face in this increasingly turbulent industry. For more details on our current research and free downloads of all our reports, please visit http://dupress.com/industries/technology-media/.

Executive summary

The growth of wireless data traffic continues at a blistering pace. With it, mobile technology adoption has become widespread across large sections of society, touching on all aspects of daily life. Consumer and enterprise mobile markets are in constant turbulence, and the uptick in demand across the smartphone, tablet, and mobile PC mass markets is expected to continue aggressively in the short to medium term.

At the root of this shift is an ongoing wave of disruption centered on mobile web technology and software innovation. As the consumer mobile web experience progressively mimics the consumer desktop PC experience, competition across the mobile value chain is at an all-time high, with incumbents facing unprecedented pressure from software-driven entrants. Against this backdrop, insights from a recent Deloitte Open Mobile survey highlight a pressing need for incumbent companies to secure viable pathways to growth—or else, risk being marginalized by a growing army of new entrants from nontraditional mobile industries. Together with an exploration of the transformation of the strategy process in mobile technology-oriented companies today, our research highlights the challenges ahead for all firms looking to remain competitive in the face of global hypercompetition.

Within this context, this report highlights an increasingly significant segment of the emerging mobile ecosystem—the semiconductor industry. There are two objectives: Provide an analysis of the most salient growth opportunities within one of the fastest-growing market segments in the mobile industry, and explore the tactics being used by leading semiconductor companies to capture and create value. Drawing on this analysis, we then provide guidance that all companies competing across the mobile industry can use to sustain growth in periods of high market turbulence.

From an industry perspective, our research suggests that a number of key demand drivers across the mobile sector are converging. All represent strong growth opportunities for semiconductor firms that are willing to capitalize on these opportunities by enacting agile platform-growth strategies. A detailed analysis of four primary drivers—wireless traffic growth, mobile device and services growth, connectivity, and mobile software trends—suggests that select firms are well placed to make substantial inroads into the major mobile consumer and enterprise value chains. Additionally, an examination of the leading semiconductor product end markets reveals the effect the 4G era may have on the competitive landscape as companies jostle to gain leadership in emerging mobile markets.

To accompany this industry breakdown, we then switch gears and focus at the enterprise level, taking an in-depth look at the strategic capabilities required to stimulate innovation and enhance the potential for capturing value. Selected case studies highlight semiconductor firms that are developing leading-edge innovation and platform leadership capabilities as pathways to growth in emerging markets.

From this analysis, executive guidance is then offered on maintaining competitiveness amid heightened market competition and technological disruption. Tactics used to transition from traditional, closed business models to a more open, collaborative approach are considered essential for competing in the mobile 4G era. A framework to guide capability development, using the twin strategies of open innovation and platform leadership, is drawn from the lessons learned from the most innovative semiconductor companies in mobile today.

Consumer and enterprise mobile markets are in constant turbulence, and the uptick in demand across the smartphone, tablet, and mobile PC markets is expected to continue aggressively in the short term. But what comes next?

The rising tide that lifts all boats

The once traditionally predictable wireless sector now finds itself constantly disrupted in a period of sustained hypercompetition.1 Deloitte’s Open Mobile series continues to explore this phenomenon in some depth, focusing particularly on incumbent markets under threat from new entrants as well as emerging growth markets harnessing mobile technology at their core. In this report, our attention is broadly on the latter, but within the context of perhaps the driving force of mobile growth today: the semiconductor industry.

Often at the center of mobile technology innovation but rarely grabbing the same headlines enjoyed by the likes of Apple and Google, semiconductor companies continue to play an increasingly important role in defining the rate and direction of mobile device and service innovation sweeping the sector. The impact of this shift is continuing to grow; mobile technology adoption is now widespread and on the rise in industries and sectors that are reconfiguring their business models around mobile platforms. As subsequent consumer and enterprise demand increases for these mobile products and services, semiconductor companies are set to reap economic benefits from their influential positions in emerging mobile ecosystems in industries such as automotive, health care, energy, and commerce.

With mobile’s rising tide continuing to lift companies competing in the sector, this report initially explores the driving factors for semiconductor mobile growth before identifying leading practices for growth and innovation from the industry’s leading players. We highlight companies that are proactively developing new markets in sectors undergoing rapid transition, where incumbents are continually being challenged to respond with innovative new business models.

The blistering growth in mobile data traffic

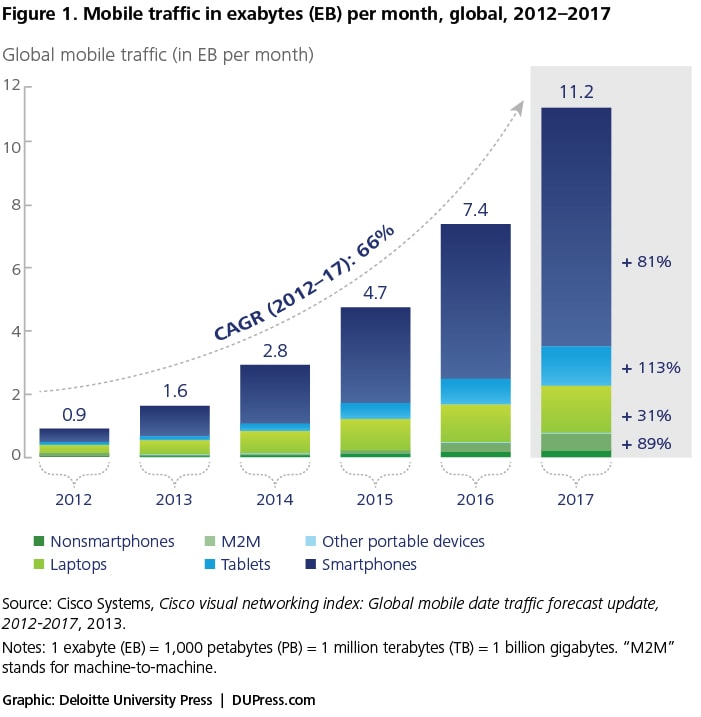

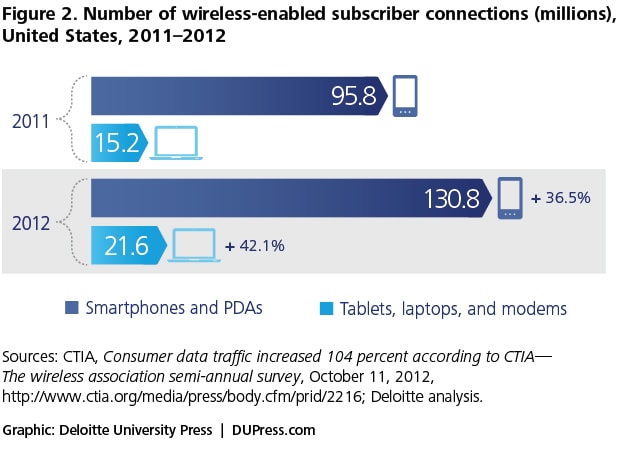

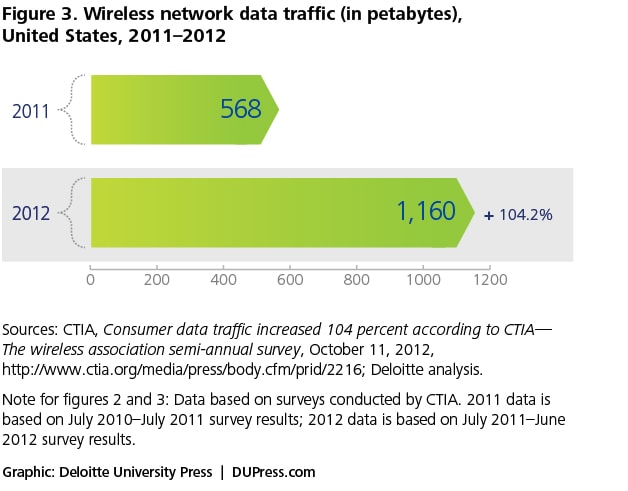

In 2013, Cisco’s annual Visual Networking Index predicted mobile and Internet data traffic to increase 13-fold from 2012 levels over a five-year period (see figure 1). Even more significant, the index forecasts total mobile traffic to increase at a compound annual growth rate (CAGR) of 66 percent across combined consumer and enterprise markets.2 This effect can be observed at the country level. For example, according to industry wireless association CTIA, wireless traffic has doubled in the United States, growing 104 percent year over year between 2011 and 2012 (see figures 2 and 3) with an expansion in the mobile subscriber base. Emerging regional markets are also developing rapidly, with Eastern Europe, the Middle East, Africa, Asia Pacific, and Latin America all believed to eventually outgrow the developed world in terms of mobile traffic growth.

Across the technology, media, and telecom sectors, the magnitude of these forecasts should not be underestimated. The pace of growth in mobile data traffic is staggering, and society has embraced mobile wireless technology in ways that were unthinkable a mere five years ago. As Silicon Valley venture capitalist Mary Meeker points out, innovation in mobile technology and wireless connectivity has rapidly touched upon all facets of life and “reimagined” everything from personal computing, printed media, news, and information to music, video, home entertainment, and art to eating, drinking, health care, banking, and commerce.3 The list is seemingly endless. Mobile technology has undoubtedly changed how we live, work, socialize, and collaborate. And yet, in many ways, we’ve barely scratched the surface. With the advent of ubiquitous wireless access in cities across the developed and developing world set to spur waves of democratized digital populations, the possibility that mobile technology will transcend previous technological shifts in societal impact is very real indeed.

Digging beneath the macro-level data, the most salient questions today surround the sources fueling the growth in data traffic. Specifically, what are the particular events and paradigm shifts behind this surge? From a consumer and enterprise perspective, it seems that a confluence of mobile meta-trends is accelerating the rapid adoption of mobile technology and devices across developed and emerging economies, businesses, and corporations and into the homes of consumers everywhere.

The 4G era takes hold

In economic terms, the emergence of the 4G wireless era has profound consequences for firms competing across the technology, media, and telecommunications sectors. Perhaps more so than previous network standards, 4G network technology in the form of the long-term evolution (LTE) standard will likely boost mobile innovation and adoption and fuel the growth of mobile data traffic to new heights.4

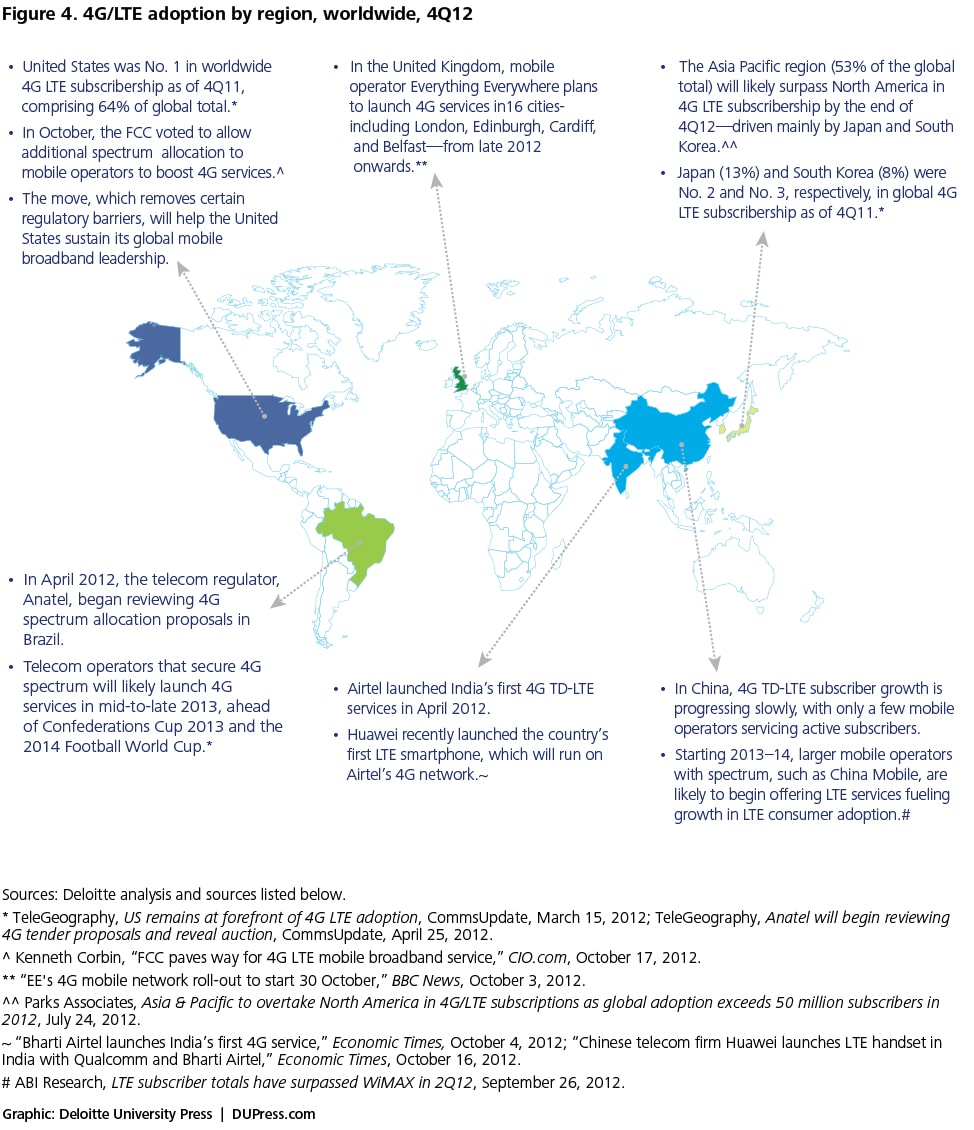

On paper, LTE will provide a jump in network speeds and bandwidth capability, ushering in a new wave of mobile ubiquity. To date, the United States leads the way in 4G adoption, commanding roughly 64 percent of worldwide LTE subscribership (see figure 4). This is not surprising. Many US wireless service providers have announced support for the standard, which is designed to be backward-compatible with GSM and HSPA technologies, giving it a clear cost advantage over competing technologies such as WiMax. LTE will also provide network operators 2–5 times greater spectral efficiency than the most advanced 3G networks, reducing the transmission cost per bit and allowing better economics for carriers and end users. Analyst estimates continue to bear this out, with recent market forecasts suggesting LTE services will generate more than $11 billion in service revenue in the United States by 20155 with global LTE subscribers likely to exceed 1 billion by 2016.6

Recently, wireless service providers in the United States have continued investing substantially to enhance existing mobile network infrastructure. Total capital investments were approximately $25 billion during July 2011–June 2012, including network upgrades from 3G to 4G. Leading the deployment in the United States is Verizon, which successfully launched its LTE network in late 2010 and rapidly expanded to approximately 491 markets by April 2013.7 Meanwhile, not to be outdone, AT&T is currently pushing the expansion of its HSPA+ network while simultaneously expanding the rollout of a new LTE network, which began in summer 2012 with a target of complete coverage in the United States by the end of 2013.8

In global markets, Japan (13 percent) and South Korea (8 percent) are quickly catching up in total LTE subscribership.9 Elsewhere, 4G subscriber rates are set to grow consistently in 2013 and beyond,10 with advanced economies in Europe, Latin America, and Southeast Asia all primed to accelerate LTE rollout in the next 12 months. Not far behind, China will likely ramp up in 2013–14.11 Driven by this uptick, an estimated 1 million new connections are being added each day (see figure 4).

And with demand rapidly outstripping supply, governments worldwide are seeking to revise regulatory policy to free up more spectrum for 4G licenses. All the while, mobile network traffic continues on an aggressive upward march: It is predicted to grow sevenfold during 2013–2017,12 adding pressure to the call for additional spectrum solutions in markets already facing a crunch.13

It’s a wonderful (connected) life

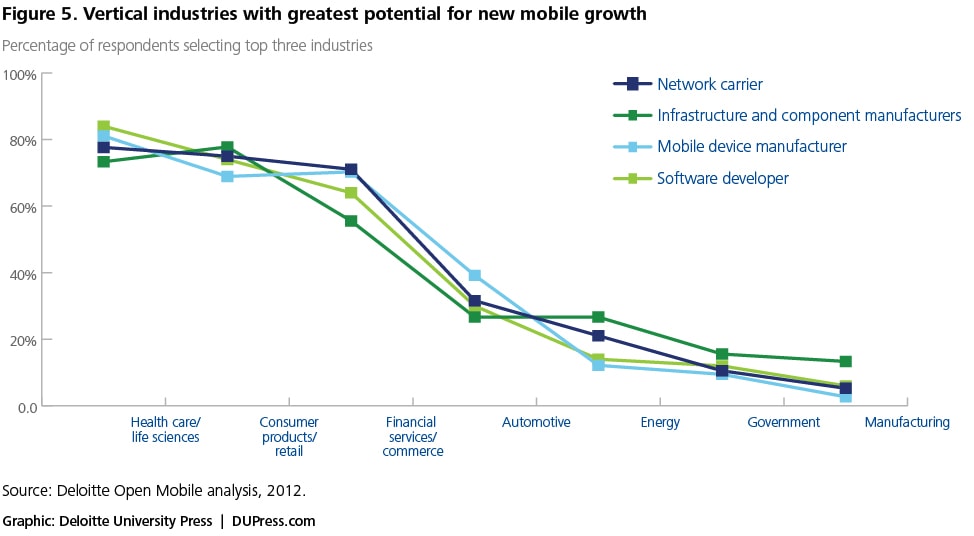

Well beyond the immediate confines of the wireless sector, the impact that 4G will have on non-traditional wireless industries such as commerce, health care, energy, and automotive is expected to be even more pronounced. Here, mobile device and software innovation—focused on enhanced wireless connectivity powered by machine-to-machine (M2M) technologies—is driving business model innovation. The outcome is a flood of new mobile products and services in industries adopting mobile technology at their core. In economic terms, the net effect of this technological shift is significantly positive across multiple facets of the mobile industry’s value chain, from both the supply and demand sides. Executives participating in Deloitte’s recent Open Mobile survey concurred and nominated the top three vertical industries where they thought 4G technology will have the biggest impact on stimulating mobile business model innovation—increasing the potential for value generation outside of traditional mobile and wireless markets in the process.14 Of those polled, 78 percent believe the health care/life sciences sector holds the most potential, with consumer products/retail industry and financial services/commerce also considered prime sectors set to benefit most from the emergence of 4G broadband technology (see figure 5). In terms of value generation drivers across these sectors and beyond, a majority believes mobile services—most prominently in areas such as mobile cloud computing and mobile payments—hold the biggest potential along with increased utilization of M2M technologies, which is also considered a major trend. With new device innovation set to proliferate in these areas, semiconductor companies will be well placed to drive product innovation across a variety of verticals and accelerate the adoption of mobile technology in the process.

The rise of the machines

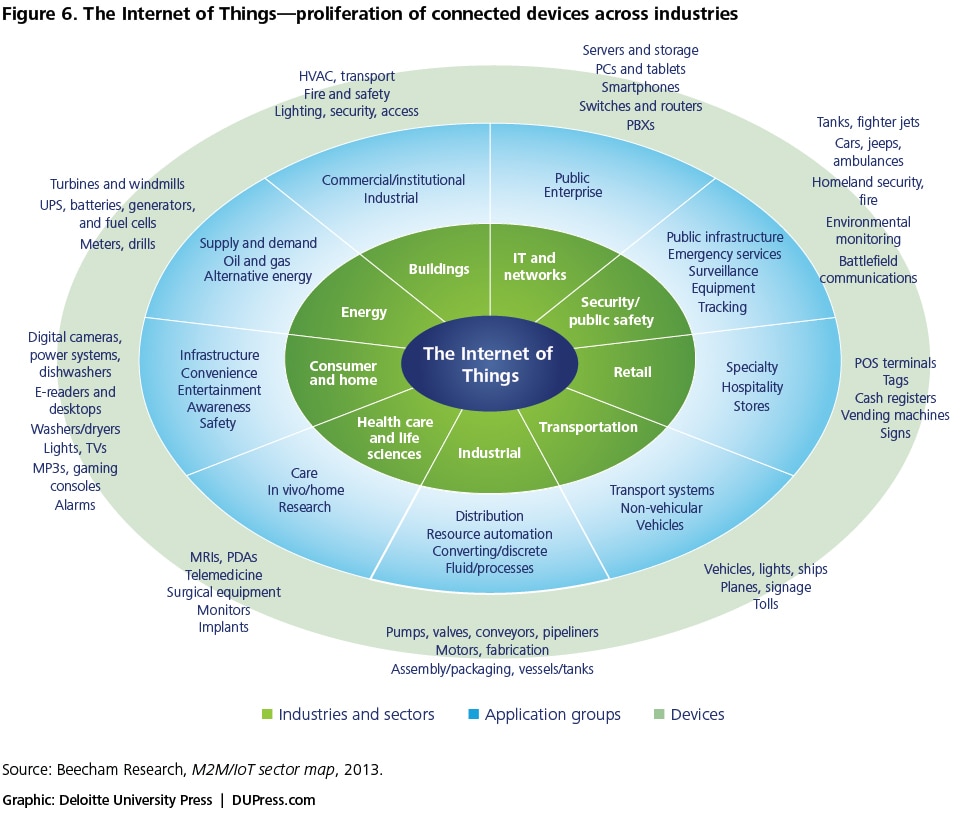

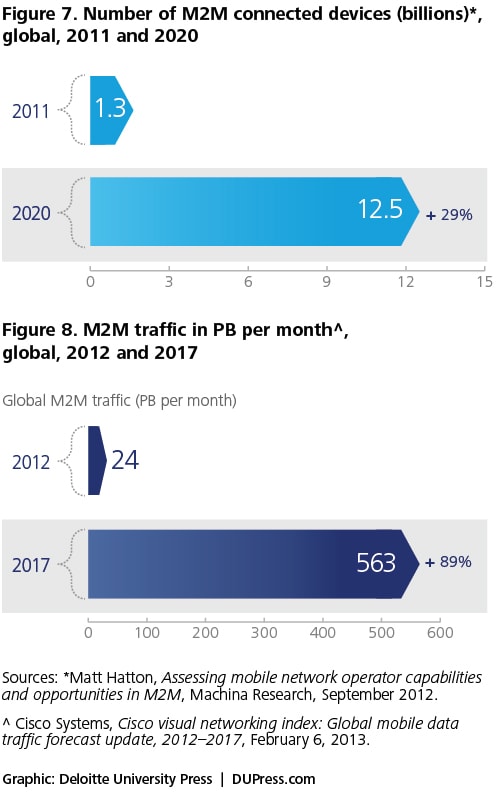

The cornerstone of many of the emerging mobile service opportunities, the rise in wireless connectivity and the subsequent growth in the Internet of Things (IOT) category, is providing significant momentum in connected device categories across consumer and enterprise sectors alike. In industries such as energy, health care, retail, and consumer products, devices integrated by M2M wireless technology are enabling new gateways to connectivity and propelling mobile revenue growth (see figure 6).

As a result, worldwide M2M interconnected devices are on a steady upward march that is expected to surge 10-fold to a global total of 12.5 billion devices by 2020 (see figure 7).15 The resulting forecast in M2M traffic shows a similar trajectory, with traffic predicted to grow 24-fold from 2012–2017, representing a CAGR of 89 percent over the same period (see figure 8).16 Revenue from M2M services spanning a wide range of industry vertical applications, including telematics, health monitoring, smart buildings and security, smart metering, retail point of sale, and retail banking, is set to reach $35 billion by 2016.17

Driving this surge in the M2M market are a number of forces such as the declining cost of mobile device and infrastructure technology, increased deployment of IP, wireless and wireline networks, and a low-cost opportunity for network carriers to eke out new revenue streams by utilizing existing infrastructure in new markets. This opportunity will likely be most prominent across a number of enterprise verticals, with the energy industry—in the form of smart grid and smart metering technologies—expected to experience significant growth in the M2M market. Indeed, the Obama administration’s targeted economic stimulus package of $3.4 billion to modernize the nation’s power grid will further accelerate the development of this particular market.18

The health care sector is also set to gain from the increased adoption of mobile technology, with the US wireless health monitoring device industry forecast to become a $22 billion industry by 2015.19 The majority of the remaining M2M service opportunities are currently clustered around the transportation, automotive, logistics, and fleet management sectors, where applications range from reducing traffic congestion by monitoring traffic flows to facilitating RFID tracking in supply chain management. In all cases, M2M technology assists improvements in productivity, innovation, and compliance-related business functions and is set to play an even greater role in mobile growth strategies as networks and platforms shift to facilitate more open access.

For semiconductor companies looking to exploit these opportunities, the roadblocks are mainly at the sector level where fragmentation exists among the various ecosystems that have grown to support the rollout of M2M across multiple industry subsectors. Several elements of the M2M value chain are at risk within these ecosystems. This includes companies and organizations active in the services (systems integration), software (middleware and application infrastructure vendors), hardware (manufacturers of GPS chips and RFID sensors), and telecom (network access, connectivity, infrastructure vendors) sectors. Each of these areas is subject to technological fragmentation, and a particular lack of standardization is apparent in the many coalitions and standards bodies set up to develop targeted technology solutions. The presence of a general standard would help to achieve seamless national and international coverage, but idiosyncratic solutions for specific devices over specific networks are the main issues currently preventing this from happening. However, if companies can successfully orchestrate a consolidated ecosystem strategy across the most disjointed elements of the current value chain, new pathways to sustainable M2M business models will likely emerge, opening doors for semiconductor companies to exert influence.

However, if companies can successfully orchestrate a consolidated ecosystem strategy across the most disjointed elements of the current value chain, new pathways to sustainable M2M business models will likely emerge, opening doors for semiconductor companies to exert influence.

Smartphones and tablets drive silicon growth platforms

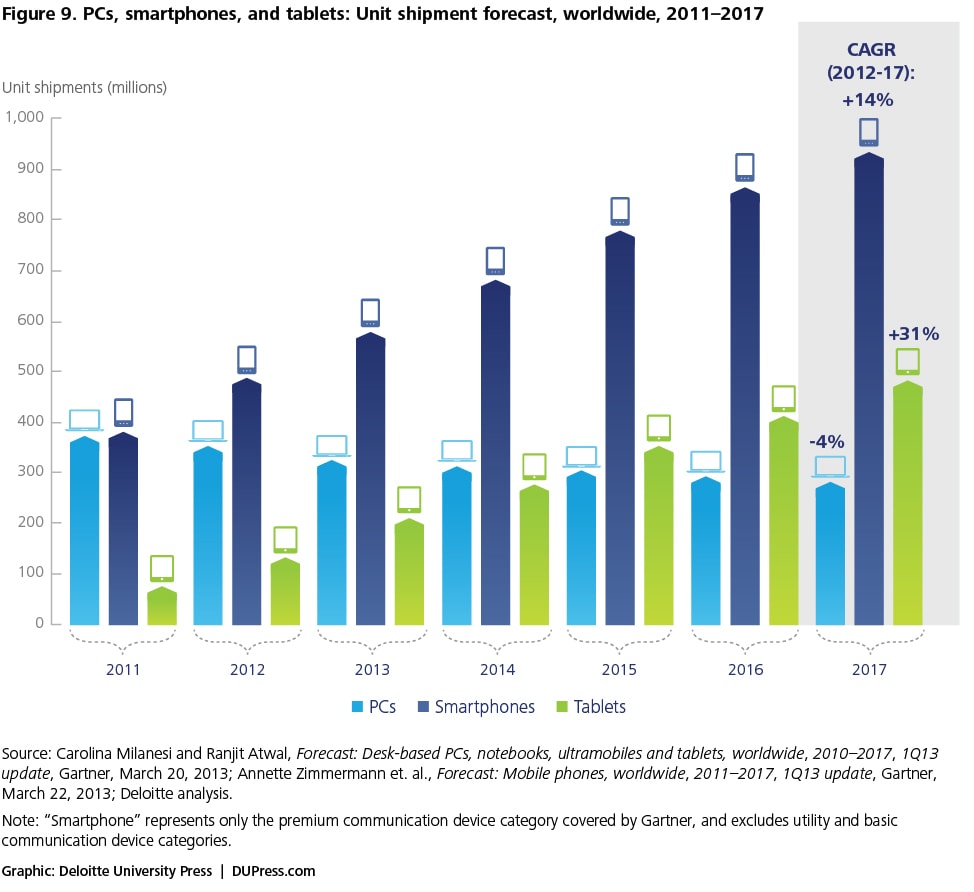

In the mobile device category, the most significant growth driver for the semiconductor sector is the increasing global demand for smartphones and tablets. Again, the numbers are a stark reminder of the rapid rise of connectivity and adoption of mobile technology across all facets of consumer and enterprise markets. A comparison with the traditionally robust PC semiconductor market illustrates just how quickly smartphone and tablet adoption has risen over the last 18 months, with an even greater uptick expected in the next 3–5 years.

A comparison with the traditionally robust PC semiconductor market illustrates just how quickly smartphone and tablet adoption has risen over the last 18 months, with an even greater uptick expected in the next 3–5 years.

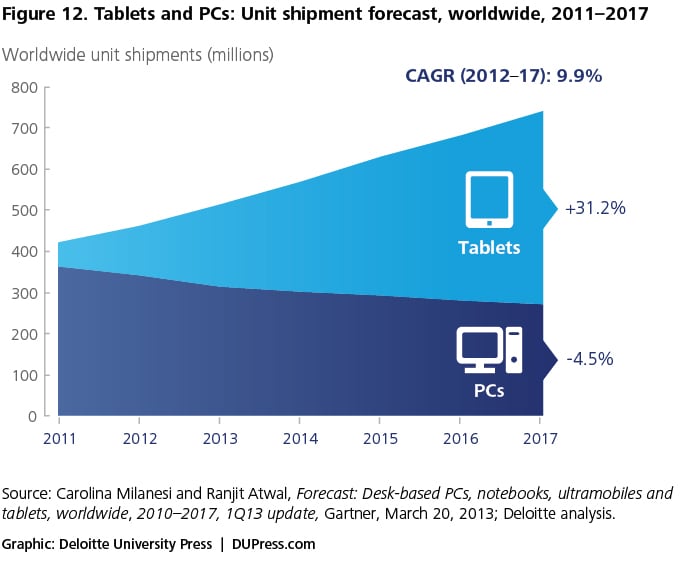

On a global scale, PC shipments are expected to decline at a CAGR of 4.5 percent during 2012–2017, reaching 272 million units shipped in 2017 (see figure 9). PC end revenue is anticipated to decrease at an 8.4 percent CAGR during the same period, reaching $142.2 billion in 2017, reflecting declining consumer demand for this form factor. In contrast, smartphone sales are expected to grow at a CAGR of 14.2 percent during 2012–2017, to 923 million units.20 Subsequently, smartphone revenue is forecast at $346.4 billion in 2017—a CAGR of 12.3 percent over 2012–2017. Premium-category smartphone sales, which exceeded PC shipments for the first time in 2011, will likely continue outperforming PC shipments through 2017 due to growing consumer interest.21 Even more startling is the upward march of tablet device adoption, with worldwide tablet shipments anticipated to grow at a CAGR of 31.2 percent during 2012–2017, reaching 468 million units. Revenue is expected to increase from $40.8 billion in 2012 to $93.2 billion in 2017, a CAGR of 18.0 percent (see figure 9).22

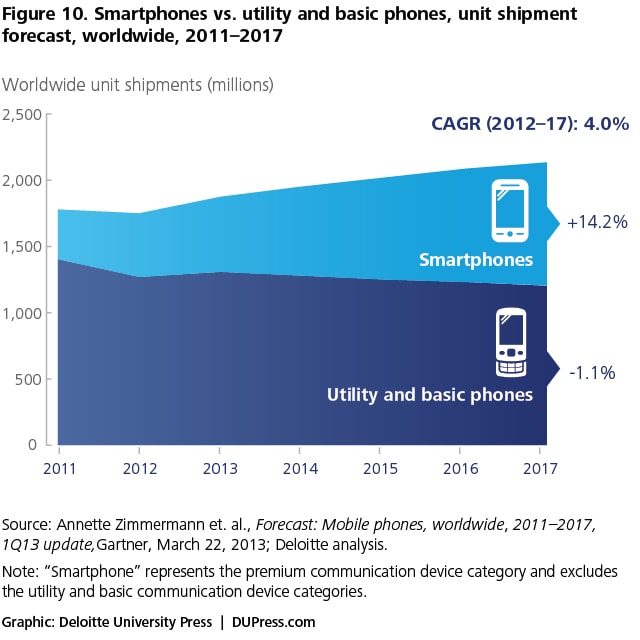

While basic phones taper off, smartphone demand remains somewhat buoyant

At the macro level, worldwide handset sales are expected to be somewhat sluggish during 2013–2017 mainly due to lackluster demand for basic and low-cost phones in both developed and developing economies (see figure 10).23 However, basic and low-cost phones will likely experience stable demand in emerging markets as cost-conscious consumers seek out increasingly affordable devices. Indeed, as mobile technology development accelerates, a trickledown effect is prevalent in many markets, helping spur growth in low-end product categories across emerging economies.24 For example, in regional markets such as China, technology reuse has never been higher and is set to spike further, with a reference design approach in semiconductor chipset utilization becoming common among vendors. This will likely help stimulate demand and lay the groundwork for waves of lower-end product introductions across the smartphone segment.25

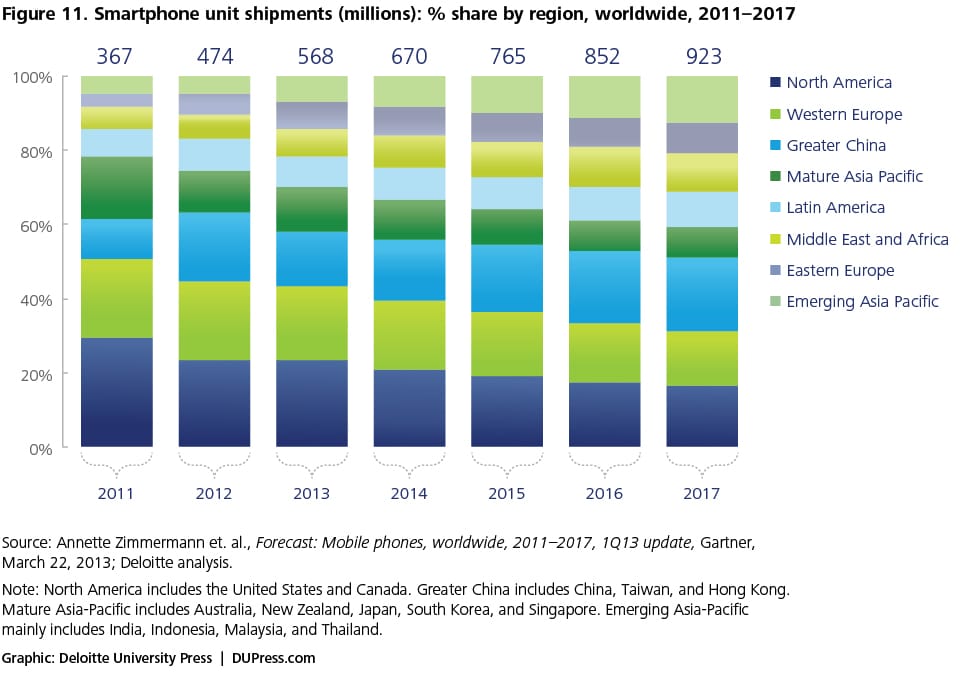

On the flip side, however, with global carriers’ network transitions to the 4G era increasing, the consumer transition from basic to smartphone adoption is growing, and demand for smartphones will likely remain strong through 2017 as technology development accelerates and prices decline across the category. Emerging markets are projected to again lead the way in smartphone growth projections. The emerging and mature Asia-Pacific region in particular is set to become the leading smartphone market by 2017, with forecast adoption in excess of 21 percent. Greater China, North America, and Western Europe are forecast to be the second-, third-, and fourth-biggest end markets for smartphones, respectively, as of 2017 (see figure 11).26

Emerging regional markets, such as the Middle East and Africa (26.1 percent CAGR during 2012–2017), Eastern Europe (24.4 percent), and Greater China (15.8 percent), are also projected to experience significant growth during 2013–2015. China, in particular, will likely emerge as the second-largest regional market for smartphones by 2017, accounting for 20 percent of global shipments (see figure 11).27 Other forecasts are even more bullish; some analysts expect China’s connected device market, which encompasses a broad range of consumer electronic devices in addition to mobile devices, to experience sixfold growth by 2020, representing some $700 billion in potential revenue—twice the current semiconductor market.28 The key catalysts for this expected adoption surge are an abundance of carrier-subsidized smartphones, customized handsets from domestic vendors, and the move to 3G and 4G networks, all spurring smartphone demand in China, emerging Asia Pacific countries, and Latin America during 2012–2017.

The tablet takeover

One of the biggest shifts in mobile device ownership over the last 12 months has been driven by a voracious consumer demand for tablets, which have undoubtedly become the mobile device du jour across an increasingly wide demographic. Such is the extent of the demand that some analysts predict up to 44 percent of consumers worldwide will own tablets by mid-late 2013, with 25 percent being first-time owners.29In the United States this trend is particularly pronounced, with tablet ownership thought to be in the region of 25 percent in 2012, compared to just 3 percent in 2010.30 Indeed, a recent study by Deloitte predicted that almost 50 percent of US consumers will likely own tablets by 2013, with 22 percent likely to be first- time buyers.31

Au revoir, PCs?

In the short term, a victim of this shift toward ultra-mobile computing platforms could be the market for desktop PCs. With the mobile web experience increasingly matching, and in some cases exceeding, the desktop PC web experience, a significant amount of IP and Internet traffic is originating from non-PC devices. As tablets such as Apple’s iPad® become “content creation devices,” consumer demand for PCs is expected to taper off and remain sluggish through 2017 (see figure 12). New design form factors and innovative mobile software development will likely spur consumer adoption and help address email, social networking, web browsing, and mobility requirements at lower price points compared to PCs.

As tablets such as Apple’s iPad® become “content creation devices,” consumer demand for PCs is expected to taper off and remain sluggish through 2017.

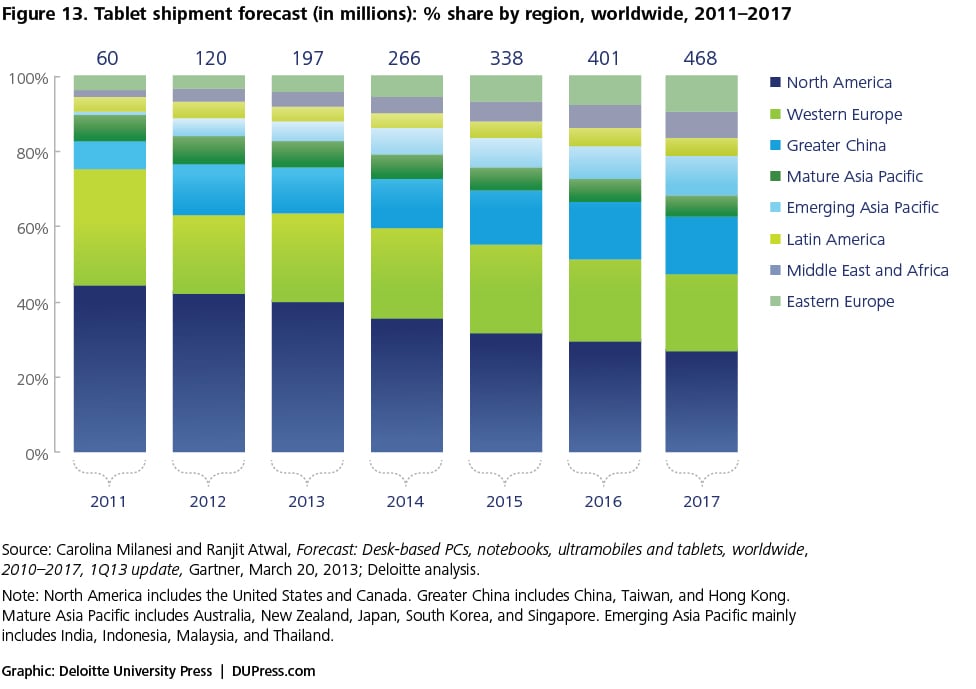

From a regional perspective, North America and Western Europe continued to propel tablet demand in 2011–2012. However, emerging market regions (Greater China, in particular) are predicted to slowly develop into the major end markets, driving tablet demand through 2017. In terms of total shipment, 256.9 million tablets are expected to be shipped worldwide in 2015, representing a 31.5 percent CAGR throughout 2012–2015. Subsequent tablet revenue is expected to increase from $41.6 billion in 2012 to $64.3 billion in 2015—a CAGR of 15.6 percent. Among all regions, North America—primarily the United States—will continue to fuel tablet shipments through 2016 (see figure 13).32 Deloitte’s survey reveals 36 percent of US consumers already own a tablet device, with Millenials and Xers being the leading users. Moreover, the survey shows that Millennials and Xers are the most likely to use a tablet as a viable replacement for a laptop.33

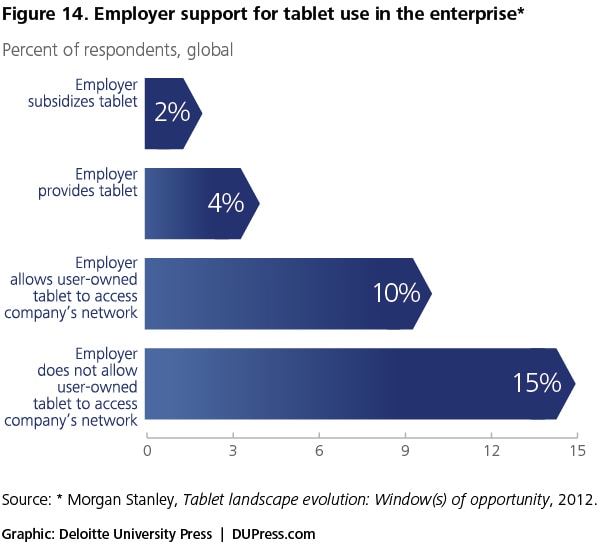

Beyond the consumer market, tablet adoption is progressing at a steady, albeit more restrained, pace within the enterprise. A recent sample of CIOs surveyed in Europe and the United States revealed that firms that plan to purchase (or have purchased) tablets for corporate use are slowly increasing.34 While this research reflects a somewhat slow uptake by enterprises, support is steadily rising; approximately 30 percent of those surveyed expect to support or adopt tablets in the workplace by the end of 2013 (see figure 14).35 Key barriers to adoption are currently cost-related and mainly associated with device hardware investment and software support. Additionally, network access and security concerns, combined with a general lack of enterprise tablet software applications, are also thought to be inhibitors to a more widespread adoption. These concerns should be addressed in 2014 for tablet adoption to make a greater corporate impact even as corporate smartphone adoption reaches new heights.

A profile of the mobile semiconductor industry

From a market perspective, the semiconductor mobile ecosystem is a complex and evolving entity. Growth opportunities in component end markets are, on the surface, somewhat fragmented, but consolidation across a number of key technology trends is evident. This consolidation will have important ramifications for opportunities (and challenges) across the semiconductor end markets, which combined, make up the broader mobile semiconductor ecosystem. Before breaking down the end markets, a general overview of the industry and the leading players is useful to understand the current competitive landscape.

From a market perspective, the semiconductor mobile ecosystem is a complex and evolving entity. Growth opportunities in component end markets are, on the surface, somewhat fragmented, but consolidation across a number of key technology trends is evident.

Overview and revenue league tables

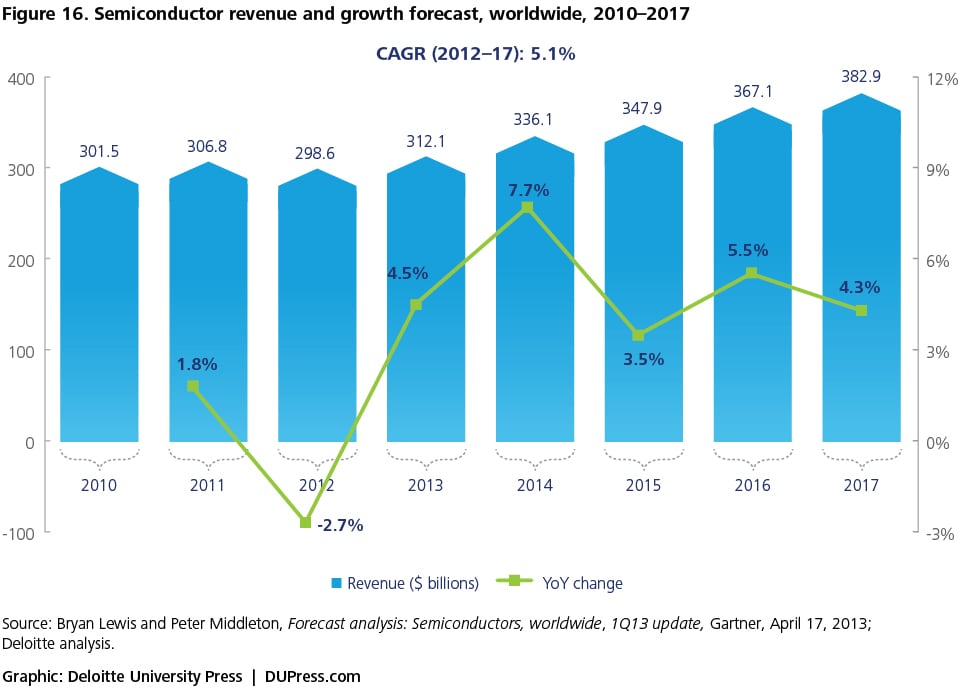

The past two years have seen a number of challenges confront the semiconductor industry as it deals with a stuttering recovery from the global economic slowdown, sovereign debt concerns, and the impact natural disasters, such as the Japanese tsunami, had on consumer demand and supply chain capability (see figure 16). Consequently, overall revenue growth has been hampered, with PC OEMs in particular facing demand challenges that directly negated investment in capital expenditure through early 2012.

However, despite the continued macroeconomic slowdown and lackluster PC demand, the emergence of increasingly popular, sophisticated mobile devices, specifically smartphones, tablets, and ultrabooks, bodes well for mobile semiconductor demand through 2015. With the likes of Apple and Samsung continually sustaining hardware and software innovation across the smartphone and tablet categories, the introduction of more sophisticated semiconductor platforms will likely drive industry revenue and investment in multiple end markets. To that end, major semiconductor manufacturers—including Intel, Samsung, and TSMC—have all announced aggressive spending plans, given an expected positive demand outlook for mobile devices in particular.

A fragmented competitive landscape

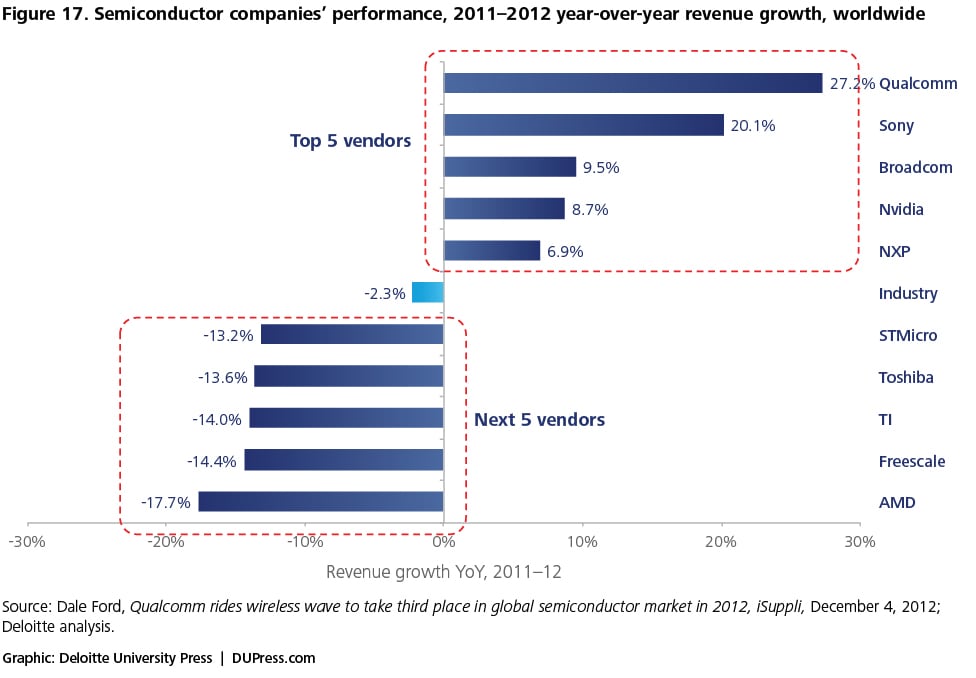

At the enterprise level, the industry remains broadly fragmented, with a number of companies competing across distinct product end markets and serving a wide number of industries. Intel remains the world’s biggest semiconductor firm, sustaining a leading market share of approximately 16 percent built on solid microprocessor and memory sales and bolstered with the company’s recent Infineon (baseband unit) acquisition (see table 1). Samsung’s semiconductor group continues to hold the No. 2 position, increasing its market share to 10.1 percent in 2012 and steadily narrowing the gap with Intel (see figure 17). Qualcomm’s revenue growth of 27 percent was the highest among the top 10 companies, a result of its leading position in the fast-growing mobile devices market, which enabled it to leapfrog three positions on the revenue league table to No. 3 in 2012 (see table 1). Although dominant in the PC and server markets, major competitors to Intel such as Samsung, Qualcomm, and Broadcom will continue to bolster market share in the mobile smartphone and tablet markets—traditionally an area on which Intel has had little focus.36

Table 1. Top 10 semiconductor vendors by revenue, worldwide, 2012

| Revenue ($ billions) | Market share | 2011–2012 Revenue change | |

| Intel | 47.5 | 15.7% | -2.4% |

| Samsung* | 30.5 | 10.1% | 6.7% |

| Qualcomm | 13.0 | 4.3% | 27.2% |

| TI | 12.0 | 4.0% | -14.0% |

| Toshiba | 11.0 | 3.6% | -13.6% |

| Renesas | 9.4 | 3.1% | -11.4% |

| SK Hynix | 8.5 | 2.8% | -8.9% |

| STMicro | 8.5 | 2.8% | -13.2% |

| Broadcom | 7.8 | 2.6% | 9.5% |

| Micron | 7.0 | 2.3% | -5.6% |

Source: Dale Ford, Qualcomm rides wireless wave to take third place in global semiconductor market in 2012, iSuppli, December 4, 2012.

* Samsung semiconductor revenue only.

Table 2. Semiconductor revenue, % contribution by end-use application, 2012–2017, worldwide

| End-use application | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| Data processing | 39.3 | 39.5 | 39.9 | 39.4 | 39.7 | 39.5 |

| Communications | 28.7 | 29.1 | 29.0 | 29.5 | 29.4 | 29.5 |

| Consumer | 14.3 | 13.8 | 13.2 | 12.8 | 12.0 | 11.4 |

| Industrial | 8.3 | 8.3 | 8.6 | 8.7 | 9.1 | 9.3 |

| Automotive | 8.2 | 8.2 | 8.2 | 8.5 | 8.8 | 9.2 |

| Military and civil aerospace | 1.2 | 1.2 | 1.1 | 1.1 | 1.1 | 1.1 |

| Total | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 |

Source: Bryan Lewis and Peter Middleton, Forecast analysis: Semiconductors, worldwide, 1Q13 update, Gartner, April 17, 2013. Note: Numbers rounded off for purposes of this analysis.

At a regional level, opportunities in emerging markets are propelling growth across the main vertical industries and end markets. PC consumption in the near term remains somewhat buoyant; emerging markets accounted for roughly two thirds of total PC shipments in 2012. This trend is expected to continue, with forecasts for 2016 anticipating China, Brazil, Russia, and India to lead PC consumption, ahead of the United States. This is a significant shift from 2010–2011, when only two of the top five PC consumers were from emerging markets.37

Breaking down the mobile end markets

A deeper analysis of the mobile semiconductor ecosystem reveals a number of key component end markets across which technology trends and drivers are making a sustained impact on top-line growth opportunities.

Application processor end market snapshot

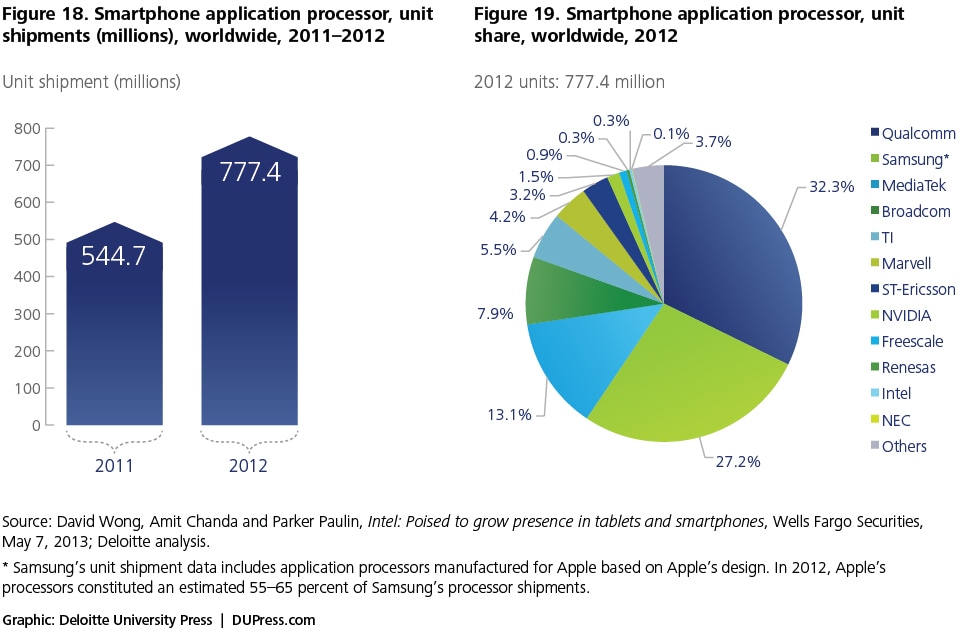

In the mobile application processor (AP) market, it’s a tale of two segments, with smartphones and the booming tablet market driving revenue. Increasing sales of high-end smartphones from tier 1 manufacturers boosted discrete AP sales during 2011–2012 (see figures 18 and 19). The continued strong demand for high-end phones using discrete processors (for example, the Samsung Galaxy series and Apple’s iPhone® series) helped sustain sales. This allowed semiconductor companies to enhance flexibility by replicating processor design across multiple device categories, thereby maximizing device performance.

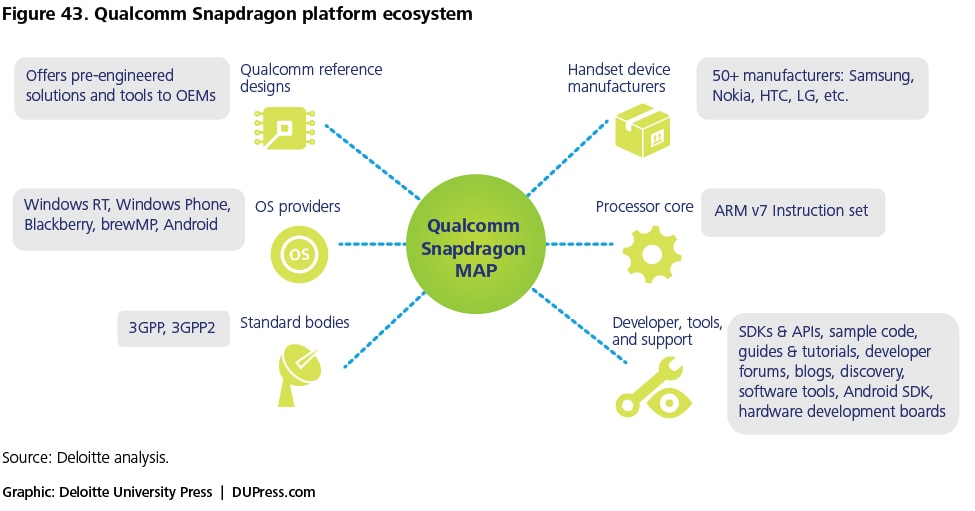

At the other end of the segment, growing demand for low-end and mid-range smartphones in emerging markets fueled growth for integrated application processors in 2011 and 2012, as integrated platforms (primarily an application processor plus baseband modem) helped reduce system costs and offered significant power-saving benefits to OEMs. Leading the way is Qualcomm (see figure 19), which benefited from solid adoption of its Snapdragon platform in multiple devices, building on established relationships with a number of smartphone vendors that included Samsung, LG, Nokia, RIM, and Motorola. The firm’s Snapdragon S4 platform is also being used by Microsoft as part of its initial rollout of Windows RT-based tablets based on the ARM architecture. Texas Instruments (TI) also held a competitive market position in 2011–2012, due to the steady adoption of its OMAP integrated platform across a range of tablets and handhelds38 (including the hugely popular Amazon Kindle). Likewise, Samsung was successful in leveraging its Exynos platform across similar device categories. NVIDIA also improved its market share to 3.6 percent in 2012, primarily due the increased adoption of its dual-core Tegra platform across multiple Android smartphones and tablet devices as well as adoption of the processor in Microsoft’s Windows RT-based products.39 ST-Ericsson and Broadcom also improved their traction with the high-volume, low-cost smartphone devices powered by Android.40 Meanwhile, Intel is looking to quickly catch up, via its Atom processor for use on the Windows 8 platform, which aims to compete with both the Tegra and Snapdragon platforms in the process.

Nonetheless, from a broader architecture perspective, ARM continues to dominate in the mobile application processor market for smartphones and tablets. As of 2012, an estimated 95 percent of smartphones were powered by ARM CPU cores.41 Major manufacturers such as Qualcomm, Samsung, Apple (Ax series), Broadcom, NVIDIA, and TI have all licensed and continue to license ARM’s processor technology to manufacture chips for mobile devices. Leveraging a powerful, ecosystem-based partnership has allowed the company to compete with Intel’s x86 architecture platform and carve out a dominating position in the smartphones sector. Partnerships with semiconductor design vendors, chip manufacturers and foundries, mobile device vendors, and mobile OS providers have cemented ARM’s position as the cornerstone of the mobile ecosystem. The firm captures value by licensing its chip design IP and architecture rather than by manufacturing its own chipsets, and as of 2012, its ecosystem numbered close to 1,000 partners. By providing the process architecture IP license and the necessary design tools, ARM allows its partners to design custom chips based on ARM CPU cores. Major mobile OS platforms designed for mobile chips based on ARM’s processor architecture include Apple’s iOS, Google’s Android, and the Windows platform—another indication that Intel has been relatively late to capitalize on the mobile market opportunity.42

To remedy this, Intel is aggressively attempting to penetrate the smartphone market with its new range of Atom x86-based processors, going head to head with ARM in developing power-efficient chips to serve the immediate market. In parallel, the company, which currently manufactures mobile chips using 32-nanometer (nm) line widths, is also ramping up a new 22-nm 3D manufacturing process that is scheduled to come online in 2013; processors are expected to be commercially available by 2014. In response, ARM signed an agreement with GlobalFoundries in August 2012 to collaborate on manufacturing chips using 3D transistor technology.43

Looking further out, Intel’s development of a more power-efficient PC processor, using the next-gen Haswell architecture—the successor to Ivy Bridge—will optimize power consumption due to an integrated CPU and platform controller hub. This will theoretically reduce consumption by approximately 30–50 percent compared to Ivy Bridge. Expectations are that Haswell will eventually trickle down into the tablet market over the next 2–3 years. But despite these moves, the current mobile applications processor market is still considered to be of somewhat limited growth potential for the company.44

Cellular baseband end market snapshot

As global wireless network providers maintain a steady upgrade of network technology, semiconductor companies are well placed to profit from the increasing adoption of High-Speed Packet Access+ (HSPA+) technology in smartphones, coupled with solid GSM/GPRS/EDGE baseband processor unit growth. 4G LTE network rollout began ramping up in 2H11 in the developed markets, and is expected to become a significant growth driver for baseband processors 2013 onward.

Other growth drivers for baseband modem chipsets (adjacent to the mobile phone segment) include laptops, tablets, ultrabooks/hybrids, and e-readers. M2M technologies, including smart meters, are also being equipped with wireless connectivity solutions. Verticals such as the energy and the automotive industry, which are investing heavily in M2M technology, will likely provide a robust and steady growth channel for semiconductor companies 3–5 years out.

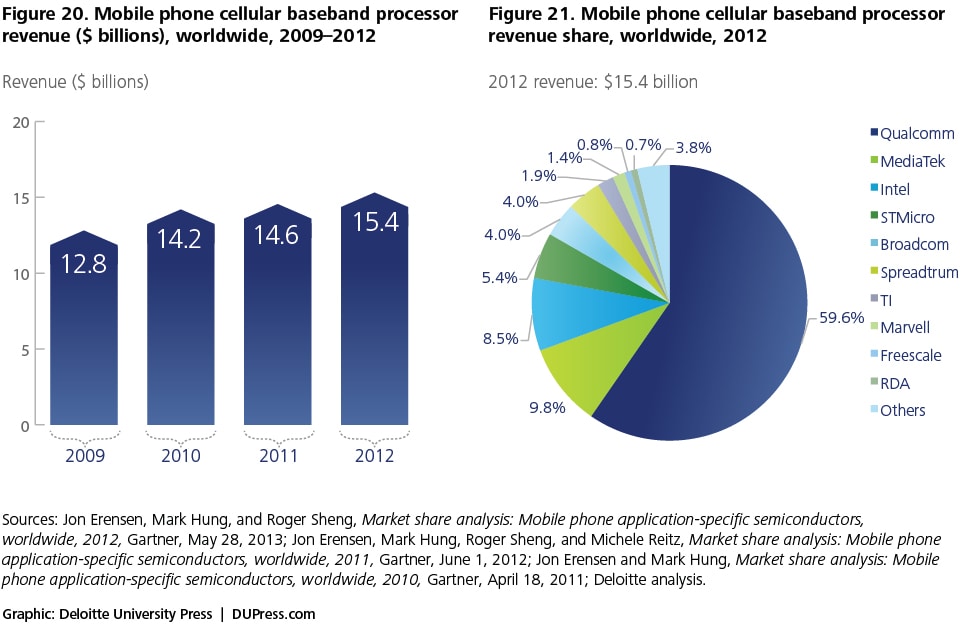

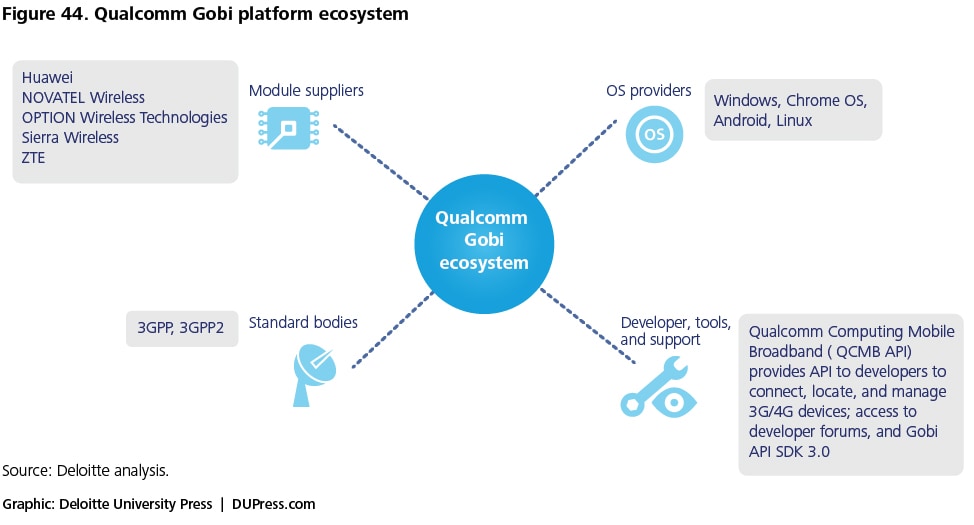

In terms of the competitive landscape, the sustainable growth of 3G and 4G network technologies contributed to the strong revenue positions of baseband vendors Qualcomm and Broadcom. In particular, integrated application processors helped propel revenues. Qualcomm also holds a dominant position in the market for USB dongles and embedded solutions with its Gobi platform. Companies such as MediaTek, on the other hand, attribute their past revenue growth to older 2G and 2.5G solutions, and are now focused on increasing market share in 3G and 4G solutions (see figure 21).

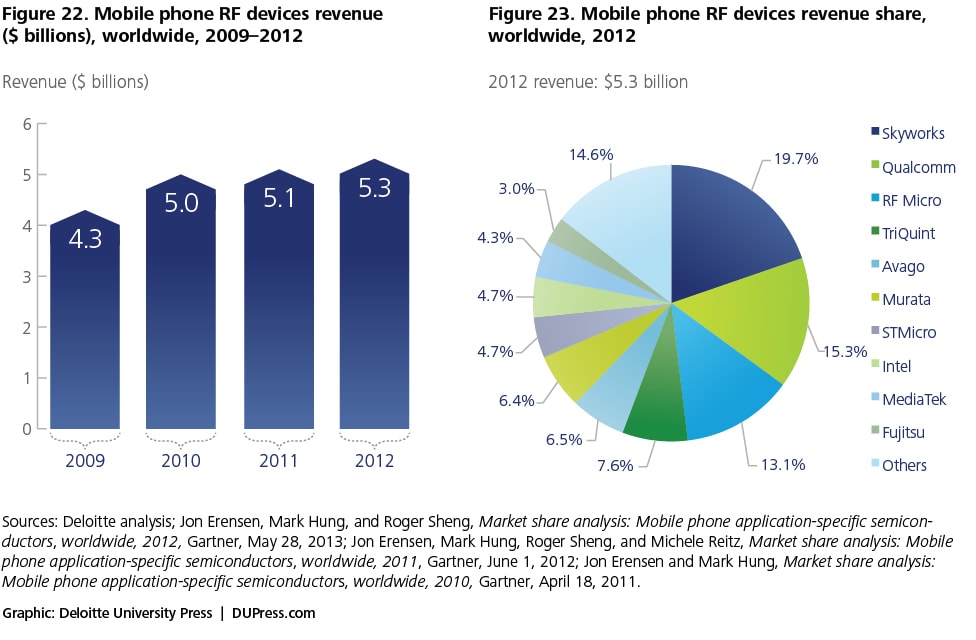

RF semiconductor end market snapshot

Radio frequency (RF) device revenue increased 4.3 percent year over year to $5.3 billion in 2012. RF transceiver revenue grew 6.6 percent year over year, while power amplifier revenue was up 2.8 percent (see figure 22). Transceivers continue to be increasingly integrated with baseband processors, mainly in low-end and mid-range phones. The market for power amplifiers benefited from rising demand for mobile phones with 3G and 4G technologies, which require extra power amplifiers to support additional bands. This led to firms such as Skyworks and Avago benefiting from key design wins with large smartphone vendors, including Apple and Samsung. In the transceivers segment, leading baseband vendors such as Qualcomm, STMicro, Intel, and MediaTek held strong market positions, given their alliances with tier 1 smartphone vendors (see figure 23).45

Wireless connectivity end market snapshot

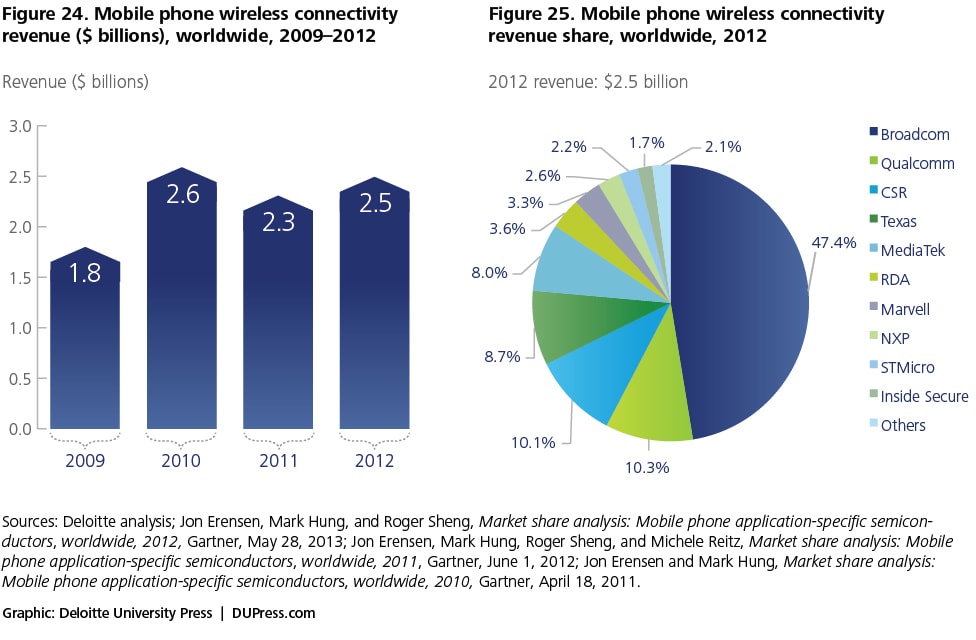

The market for wireless connectivity has transitioned from single-function chipsets for Bluetooth, Wi-Fi, and GPS toward wireless combo chips, which combine some or all of those functions within a single chip solution. While solutions that combined Wi-Fi, Bluetooth, and FM remained dominant in 2011 and 2012, combo solutions that also integrate GPS have increasingly gained traction in 2013.

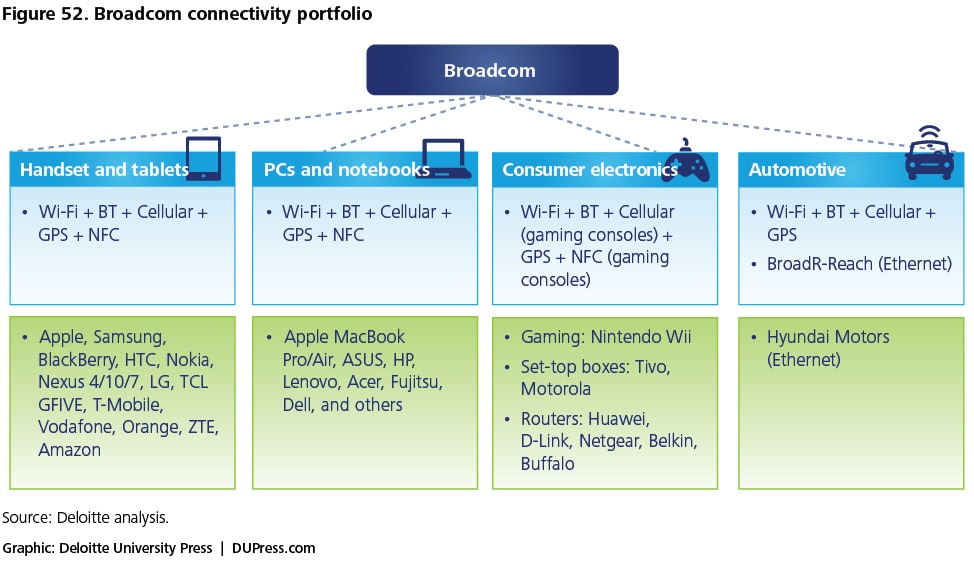

Broadcom continues to lead the wireless connectivity market, leveraging its mobile phone combo chip solutions that integrate Wi-Fi, Bluetooth, and FM on a single chip (see figure 25). The company also introduced a Bluetooth + GPS + FM combo chip solution and remains well positioned to benefit from the tablet trend, being the incumbent supplier for Apple’s iPad platform (as well as the major supplier for the iPad’s touchscreen controller). Innovation in connectivity solutions remains the firm’s strong suit, and this, combined with its forward-looking position on integrating near field communications (NFC) technology into more combo chip solutions, will act as a catalyst for its top-line growth objectives.46 Other major vendors, including Qualcomm and MediaTek, also launched combo chip sets in 2012, such as a quad-combo chip that integrates GPS, Bluetooth, Wi-Fi, and FM.47

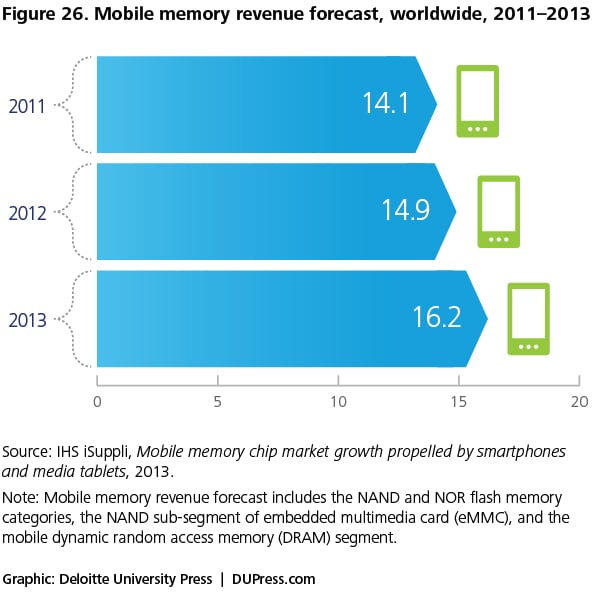

Mobile memory end market snapshot

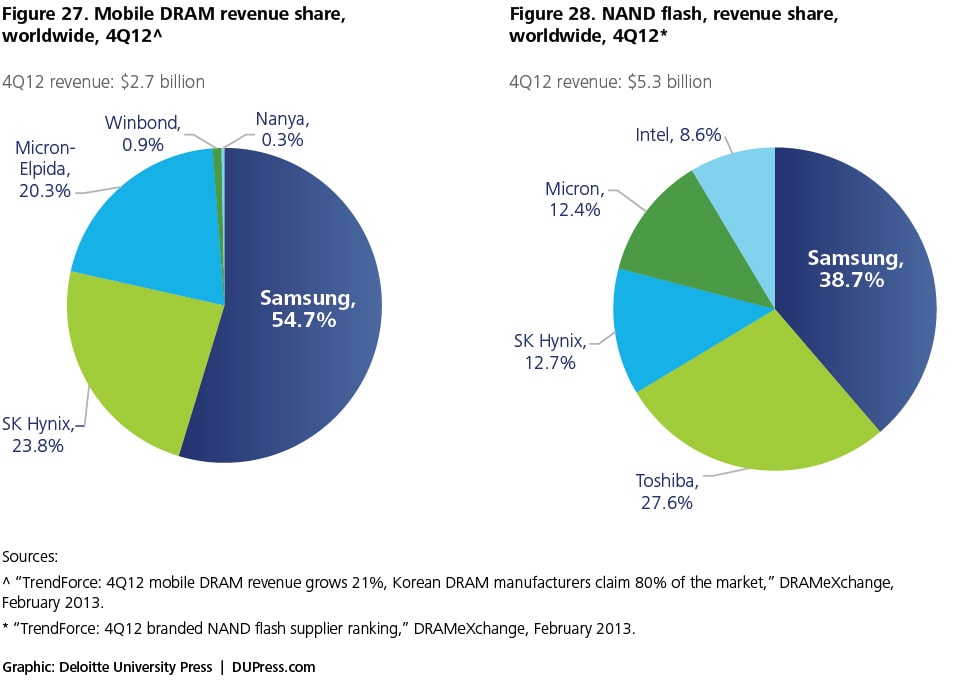

Smartphone and tablet adoption are enabling a revival of DRAM and NAND demand and boosting the memory market in the process. As both device categories increasingly combine content consumption with content creation, software applications requiring substantial memory capability are on the rise. Gaming and video are two content-rich growth categories for mobile applications that are set to continue their upward growth curve through 2015. As a result, strong growth is projected in both the DRAM and NAND markets in the short term as smartphone technology trickles down into lower-end device categories and the emergence of more powerful tablets and “superphones”48 begins to take hold (see figure 26). In terms of market leadership, Samsung remains dominant in both memory markets, leveraging its leading technology innovation and economies of scale (see figures 27 and 28).

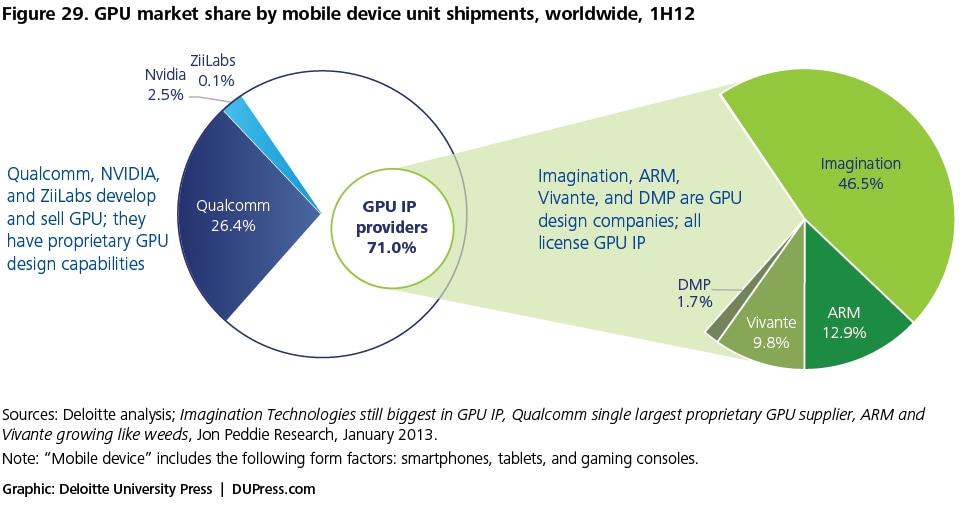

GPU end market snapshot

In line with the other semiconductor end markets, the GPU market continues to see increased demand resulting from robust smartphone and tablet adoption. With both device categories utilizing GPUs to enable functions such as advanced gaming capabilities, user interface capabilities, and browser acceleration, growth in this market is projected to continue to climb. Innovation trends include increasing functionality, with some of the latest chips including augmented reality capability and high-performance image and video processing functionalities.

On the competitive landscape front, Imagination Technologies continues to hold a leading position in the global mobile GPU market, with a 46.5 percent unit shipment share (see figure 29). The company’s GPU offerings are the preferred solution for most of the major smartphone and tablet vendors, including Apple and Samsung. Many system-on-chip (SoC) vendors, including TI and Intel, also license Imagination’s GPU intellectual property for their own integrated processor platforms.

Qualcomm is the leading mobile device GPU vendor (see figure 29), primarily due to its integration strategy of positioning its Adreno GPU chip as part of the Snapdragon platform, which is one of the leading integrated mobile device processor platforms in the market. In the overall mobile GPU market, Qualcomm currently ranks second, behind Imagination Technologies.

In the mobile GPU IP market, ARM is the No. 2 GPU design vendor, after Imagination (see figure 29). Companies, including Samsung, ST-Ericsson, and Broadcom, continue to license ARM’s GPU IP for their integrated SoCs. Meanwhile, NVIDIA, a relatively small player in the overall mobile device GPU market, continues to build out its integrated processor offerings, focusing heavily on leveraging its leading-edge capability in graphics. The firm’s proprietary GPU GeForce chip is now integrated across its range of Tegra mobile processor platforms.

Growth trends in the end markets

Across the end markets, several technology trends stand out as a bellwether to future revenue growth.

Integrated platforms

One of the major technology trends that continue to impact the industry is the move toward integrated processors. These are chips that combine multiple functionality on a single chip platform—typically consisting of memory and graphics functionality combined with processor capability. The benefits of this approach are primarily performance- and cost-related, allowing vendors to theoretically lower costs for customers by integrating application, graphics, and baseband processors that share memory and power capabilities. As such, the move toward integration in mobile devices is rapidly gaining traction across the tablet and smartphone sectors. Major OEMs such as Broadcom, Qualcomm, Nvidia, and TI are prominent in pushing the technology out to a wide customer base that is eager for low-cost and power-efficient solutions.

From a market perspective, upticks in smartphone adoption, particularly in emerging markets, will again fuel growth in integrated platforms. As multi-core CPUs make headway into entry-level smartphones, power consumption and cost will likely become key elements. Consequently, the trickle-down effect of technology reference design reuse in markets such as China will likely ensure that a wave of low-end, affordable smartphone designs hits the emerging markets 2013 onward. Additionally, with LTE forecast to have a big impact on driving adoption, demand for power-efficient handsets with integrated platforms such as Snapdragon and Tegra is expected to continue to climb.

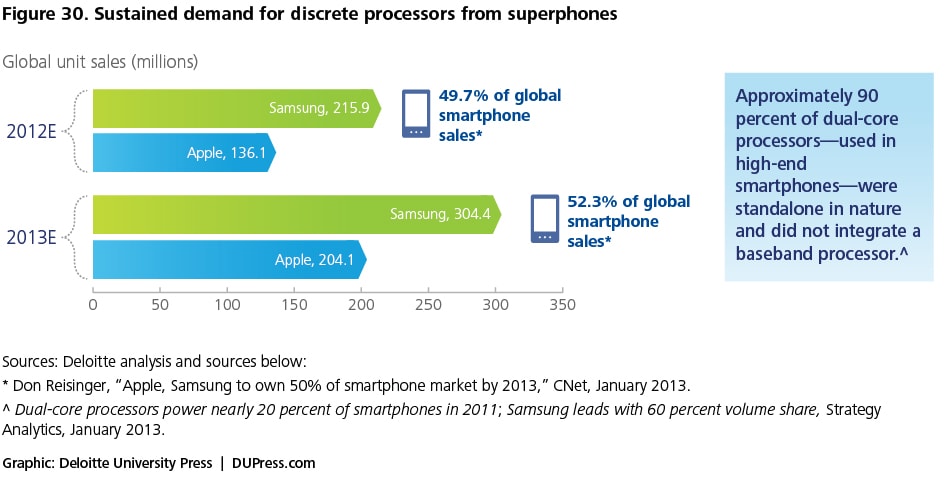

Superphones need more power

Parallel to the shift toward integrated chipsets, albeit at a reduced level, is the predicted sustained demand in the discrete semiconductor end market to serve the emerging superphone mobile device category. These chips, which are used in several electronic applications—most importantly, in managing electric power—will likely see steady revenue growth through 2014 due to sustained demand for advanced functionality in high-end devices. Smartphone vendors such as Apple and Samsung (with the iPhone and Galaxy devices, respectively) currently use discrete chips for the flexibility of customizing the chip design across multiple devices and form factors (see figure 30).

Multi-core processor demand rises

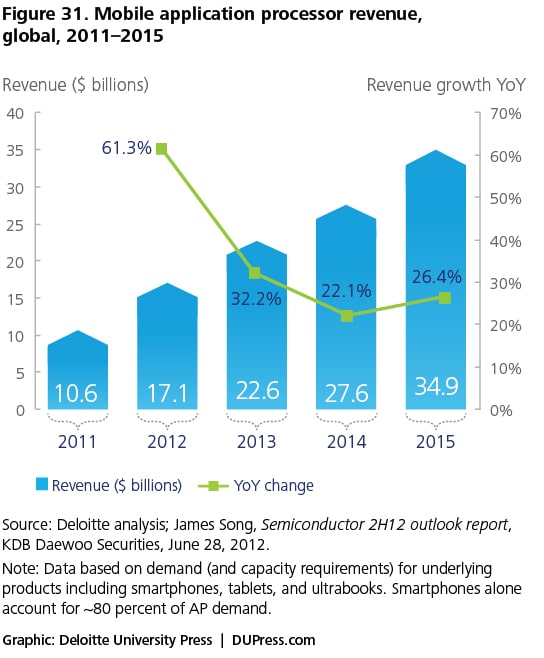

Recently, the smartphone category has also seen a rise in the use of dual-core and quad-core processors, which helps lower the number of application processors required on a single wafer. Typically, a single wafer can be comprised of over 1,260 single-core processors, which is reduced to approximately 560 with a dual-core processor and to approximately 370 on a quad-core processor.49 Given the increasing consumer demand for high-end smartphones with multi-core processors, Apple and Samsung use both dual- and quad-core processors in their devices. As such, application processor vendors are likely to continue to ramp up capacity and expand their investments in this area steadily through 2015 (see figures 30 and 31).

Looking further out, growing demand for faster applications in mobile devices will potentially lead to increased demand for multi-core processors, which have faster processing speeds and lower energy consumption compared with single-core processors. Additionally, multi-core processors enable higher performance while supporting parallel execution of multiple applications.

Moore’s Law propels another wave of shrinking

The race to boost chip performance through shrinking components continues unabated. With the industry now transitioning to sub-22 nm linewidths and 3D transistors, the push by companies such as Intel, Qualcomm, and Samsung to develop chips on smaller nodes is noteworthy. Intel, in particular, has an aggressive R&D pipeline, which will likely see the company become the first vendor to develop chips for PCs on a 14-nm linewidth in 2013. By 2019, the company plans to introduce chips on a 5- nm node.50

Meanwhile, foundries such as TSMC and UMC—while trailing Intel—plan to introduce 16-nm/20-nm/22-nm chips for PCs during 2013–14. For mobile devices, a slight lag is present, with vendors instead aiming to introduce smaller (sub-22-nm) processors 2014– 15 onward.51

Semiconductor manufacturers are also exploring producing chips on larger 450-mm size wafers, which will improve production scale and boost fixed-cost savings. Intel and TSMC were the first to announce separate plans to pilot production on 450-mm wafers. Intel, in particular, signaled its intent in this area by signing an agreement to invest roughly $1 billion in backend equipment provider ASML’s 450-mm wafer and R&D programs.52 The significant capital investment required by both chip vendors and backend equipment providers will likely push the move toward 450-mm wafers out to 2017.53

Mobile device memory is on the uptick as advanced functionalities demand increased digital storage

As the level of mobile gaming becomes more sophisticated, increased memory capacity is required to handle more advanced tasks, which in turn is driving DRAM demand in the end markets. Activities such as multitasking, media encoding/decoding, and data synchronization in advanced mobile computing devices, all require higher memory.54 Handset DRAM density increased from 2.3 GB in 2Q10 to 5.8 GB in 2Q12. In media tablets, mobile DRAM density increased from 2.0 GB to 8.3 GB over the same period.55

NAND flash storage capacity is also on the rise as smartphone and tablet users voraciously consume content such as digital music, video, images, and books. For instance, three variants of Apple iPhone 5 smartphones were launched with different NAND flash memory features—16 GB, 32 GB, and 64 GB.

Growth trends in vertical industries

Several industry verticals, where mobile technology adoption is rapidly advancing, are also providing semiconductor companies with new routes for mobile-focused growth. Companies such as Qualcomm have dedicated strategies in place to take advantage of opportunities across the Internet of Things landscape. Increasing application complexity, consolidation of multiple subsystems, and rising demand for wired and wireless connectivity features are all contributing to semiconductor growth opportunities in the automotive, health care, energy, and retail industries.

Mobile growth in the automotive industry

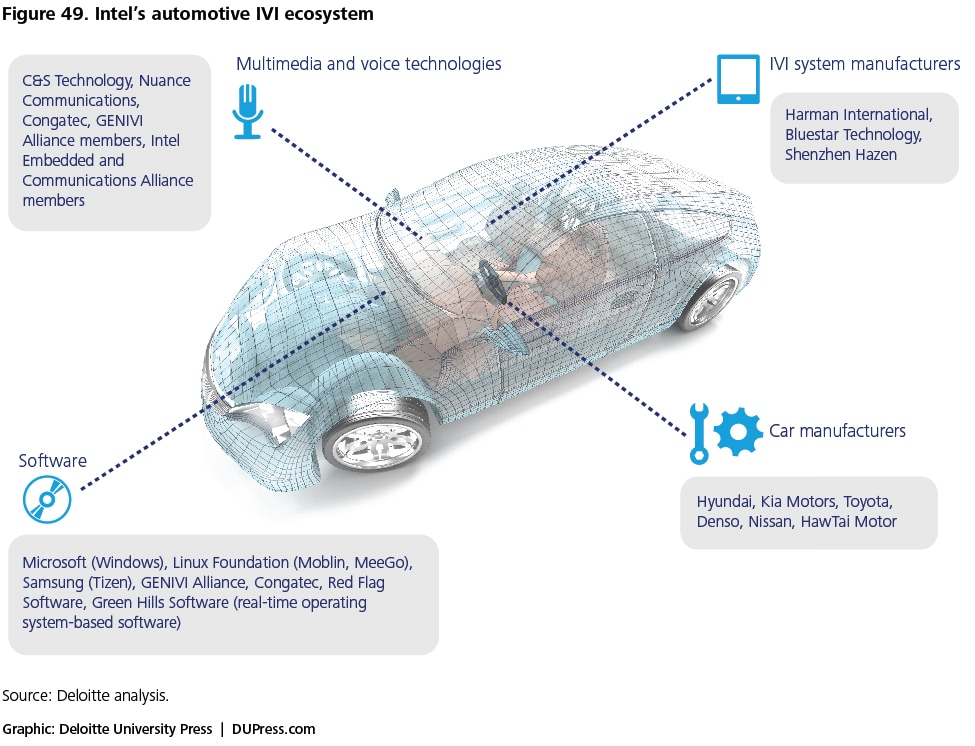

The automotive industry has made great strides over the last three years to rapidly adopt wireless technology across a range of consumer and enterprise products and services. With in-vehicle electronics growing in complexity and demand, three categories for semiconductor connectivity growth currently stand out: in-vehicle infotainment (IVI), telematics, and insurance services.

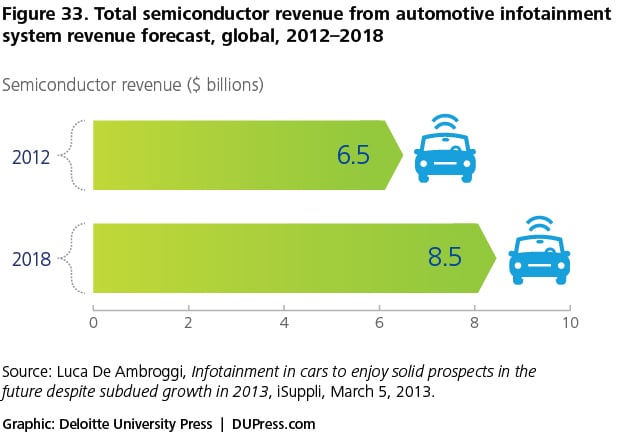

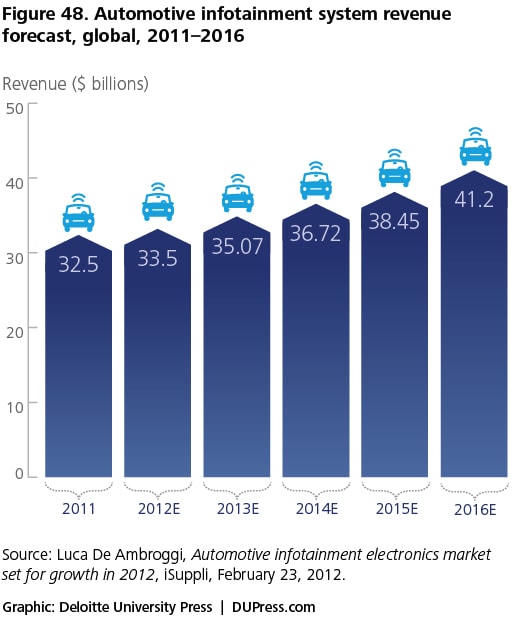

The semiconductor revenue opportunity from in-car infotainment, which is by far the biggest automotive growth channel, is estimated to reach $8.54 billion by 2018 (see figure 33).56 Propelled by a surge in the integration of infotainment and wireless connectivity solutions that will power the likes of next-generation location and navigation systems, telematics, and connectivity, this section of the market is expected to grow 3–7 percent annually over the next five years. This will subsequently provide companies such as Intel, Qualcomm, Nvidia, and Broadcom opportunities to significantly expand their embedded market footprint.57 In the telematics category, connectivity systems to assist vehicle diagnostics for maintenance purposes are among other services, such as fleet vehicle management and roadside assistance, that are converging with advanced driver insurance systems in products such as pay-as-you-go driver insurance and driver-based insurance mapping.

In many instances, it is apparent that mobile operating system platforms are continually being enhanced in all areas of wireless automotive and integrated closely with today’s mobile semiconductor platforms.

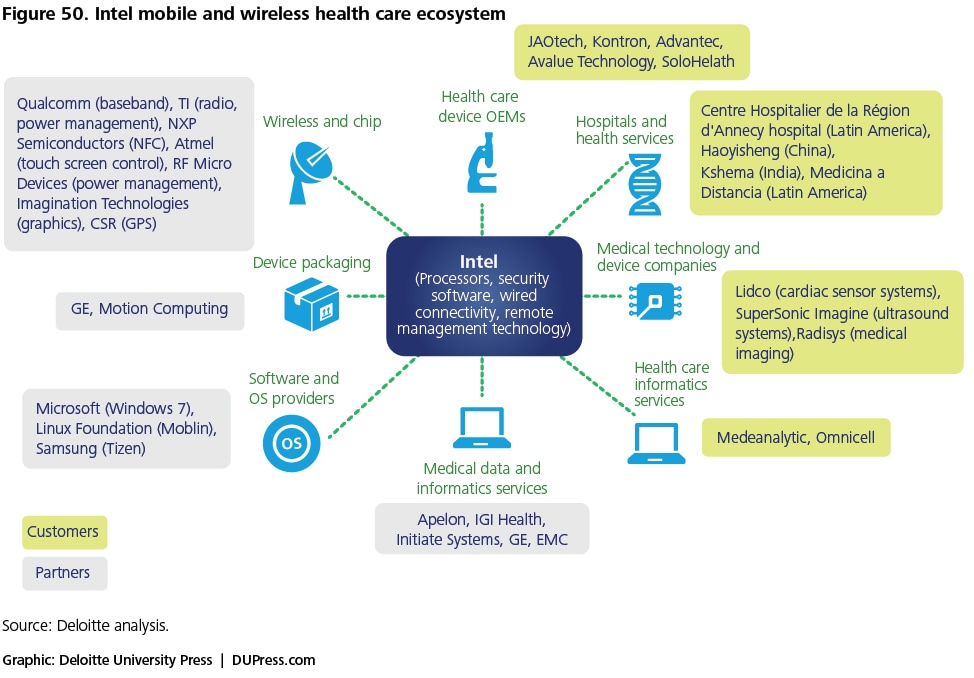

mHealth markets set to soar

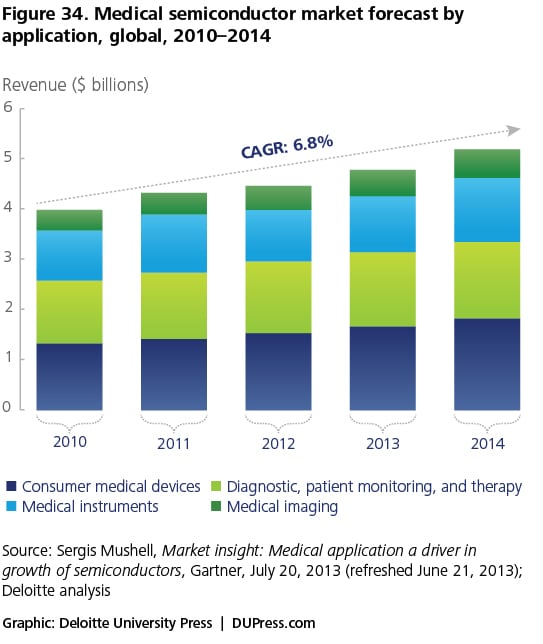

As previously discussed, the US health care sector is witnessing increased adoption of mobile and wireless technology, with the global mobile health (mHealth) market forecast to be worth $11.8 billion by 2018.58 Within this fast-growing embedded segment, the consumer medical device market is expected to be a leading connectivity growth opportunity for semiconductor companies.

Key drivers for this expected growth are the recent health care reforms in the United States, such as the Affordable Care Act and the Health Insurance Portability and Accountability Act (HIPAA), which are aimed at reducing health care costs, improving care quality, and increasing general public access to health care. These reforms, together with an aging population, are driving the need to reduce the cost of treatment, thus fueling demand for remote patient treatment and monitoring. Within this niche market, device OEMs are utilizing semiconductor processor platforms to enable advanced functionality in areas such as diagnostics and therapy. In turn, this is helping fuel US wireless health monitoring device revenues, which are estimated to grow to $22.2 billion in 2015.59 Alongside this market, use of embedded medical monitoring devices is anticipated to grow to 170 million devices by 2017.60

At present, Intel has a technology lead in the medical device platform market through the widespread use of its Atom processor, but it faces increasing competition from arch rival ARM.61 Current challenges to sustained growth in this market are mainly with regard to fragmentation in wireless connectivity standards, which will challenge medical device vendors. Emerging standards are wide and varied and include IEEE 802.15.6, Bluetooth Low Energy (LE), Wi-Fi, and Zigbee.62 In contrast, the portable health care device platform market is less fragmented, with two main platforms: the Intel Atom-based Qseven Computer-on-Module (COM), which supports Windows and Linux platforms, and the ARM-based Ultra Low Power COM (ULP-COM), which supports Android and Linux. Support for multiple connection protocols is crucial to the adoption of portable health care devices.63

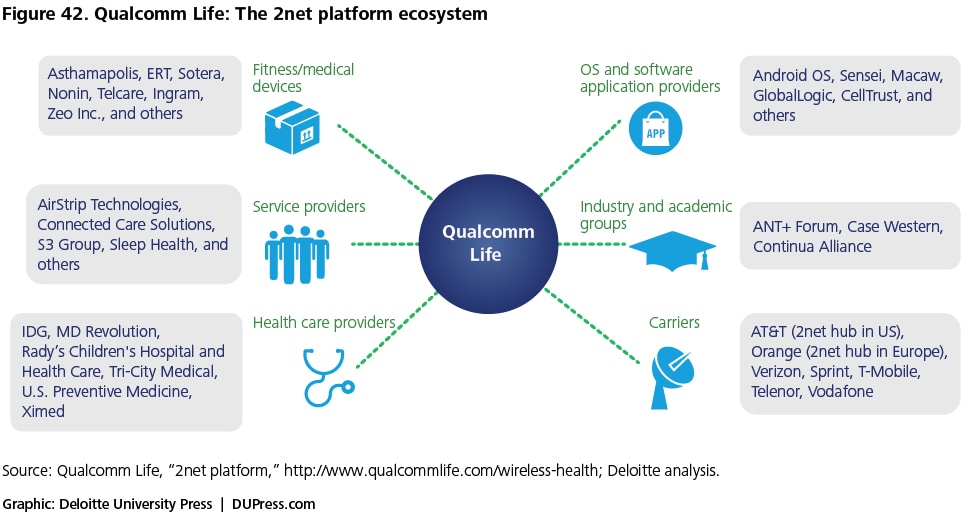

Intel is also collaborating with GE in a joint venture to develop mobile health care devices.64 Qualcomm, through its subsidiary Qualcomm Life, has also created a presence in this market with its 2net platform,65 a cloud-based platform designed to provide wireless connectivity, data management, and services for chronic disease management and a channel to share medical information. More than 161 partners and collaborators have currently integrated or are considering integration with the 2net platform.66

Smart energy leading the way

Innovation in the energy sector is occurring at a rapid rate. In particular, the emergence of smart grid networks across the United States is perhaps the leading value proposition for exploiting wireless M2M technology. At the broadest level, these networks provide means of tracking energy utilization, mainly in the form of smart grid metering, for two-way communication between consumers and the electricity grid in real time. This enables significant energy and cost-saving features not possible with today’ s grid.67

Growth opportunities are significant: Recent analyst projections suggest the US smart grid market will grow from $21.4 billion in 2009 to $42.8 billion in 2014.68 By 2014, 88 percent of this market is projected to be comprised of device and hardware manufacturers, software developers, and communications equipment providers. Within these sub-sectors, double-digit growth forecasts are not uncommon. In parallel, the total smart grid communications market is forecast to experience tremendous market growth with a projected CAGR of 17 percent through 2015. The total market size in 2015 is projected to reach almost $1.6 billion.69The market is divided between wired (with a CAGR of 10 percent) and wireless communications (with a CAGR of 26 percent). Currently the market size of wired communications is larger, but wireless communications will surpass it by 2015 and prove a larger market as more investments are made.70 Other forecasts suggest that the smart grid infrastructure market, including grid automation upgrades as well as smart metering, represents yet another golden opportunity that will likely attract $200 billion in worldwide investment from 2008 to 2015.71 It is across these infrastructure and components markets that semiconductor companies could be well placed to make an impact.

Pathways to competitiveness in this sector can often emerge from participating in various ecosystems that are forming in a number of overlapping industries, bringing together a wide variety of M2M value chain players. From power generation through energy distribution and management, communications infrastructure, and future applications development, the scope and complexity of these ecosystems is growing. Leading semiconductor companies competing in these networks include Qualcomm, which has a number of strategic alliances in place, including an equity stake in Consert Inc., a smart grid technology provider.72 Qualcomm technology is also deployed in 241,000 cellular embedded smart meters as part of Texas New Mexico Power’s smart grid network.73

Smart homes on the rise

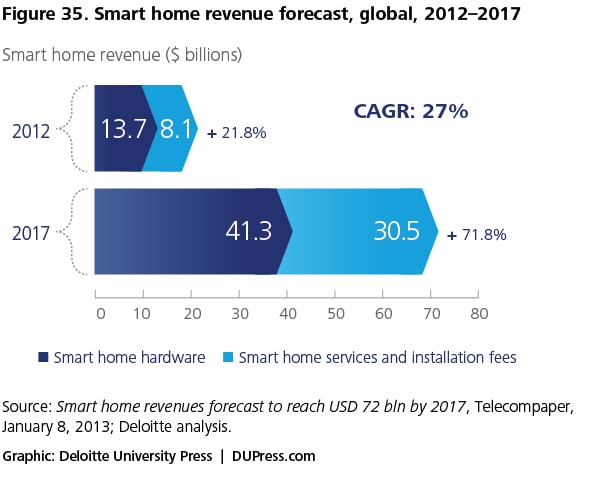

The impact of smart home74 technology adoption is picking up speed, and semiconductor companies are well placed to capitalize on it. Recent analyst projections suggest global smart home revenues are estimated to reach $72 billion by 2017, with new ecosystems focusing on the development of systems and devices for smart home entertainment, computing, monitoring and control, and even health (see figure 35).75 Market trends to watch in this area include the emergence of app-based home automation solutions; adoption of multiple, and seamless, connectivity options within the home; and a general shift in consumer discrete content viewing to a content-as-a-service model. All of these trends will offer semiconductor companies opportunities to develop and utilize new platform chip technologies in a multitude of home connectivity solutions and consumer devices.

Companies already making inroads into this market include Qualcomm, which has multiple wireless and wireline products as well as software solutions that enable smart home connectivity,76 and Samsung, which has introduced AllShare, a digital content sharing platform for smart home use. Samsung has also launched Smart View, a software application that links its Smart TVs with its own brand of mobile devices, enabling users to stream live TV and other content. Also part of the firm’s platform strategy is a home energy management (HEM) solution that integrates smart appliances, smart TVs, thermostats, mobile devices, solar panels, and smart meters.

Mobile payments finally set to take off?

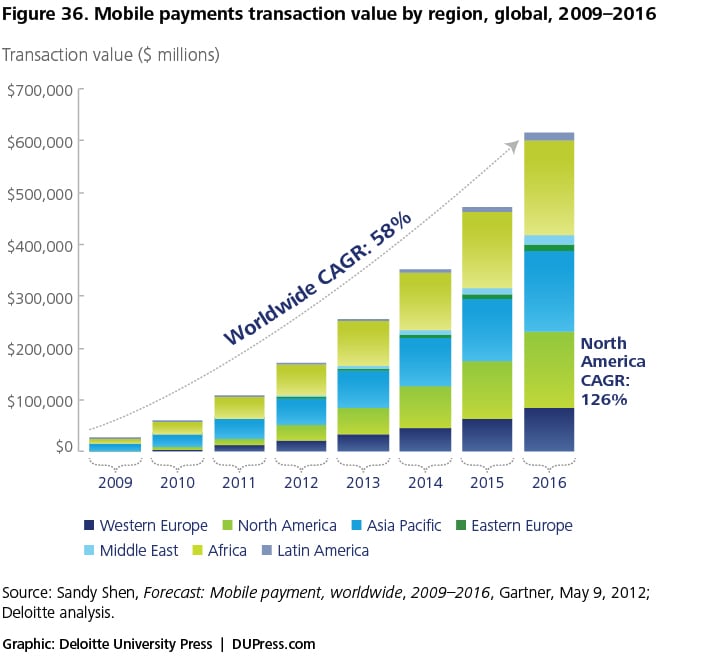

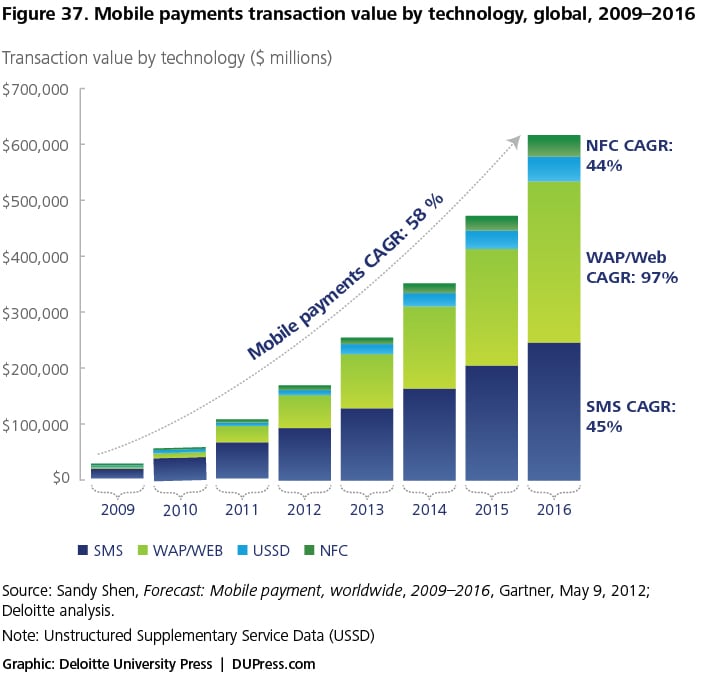

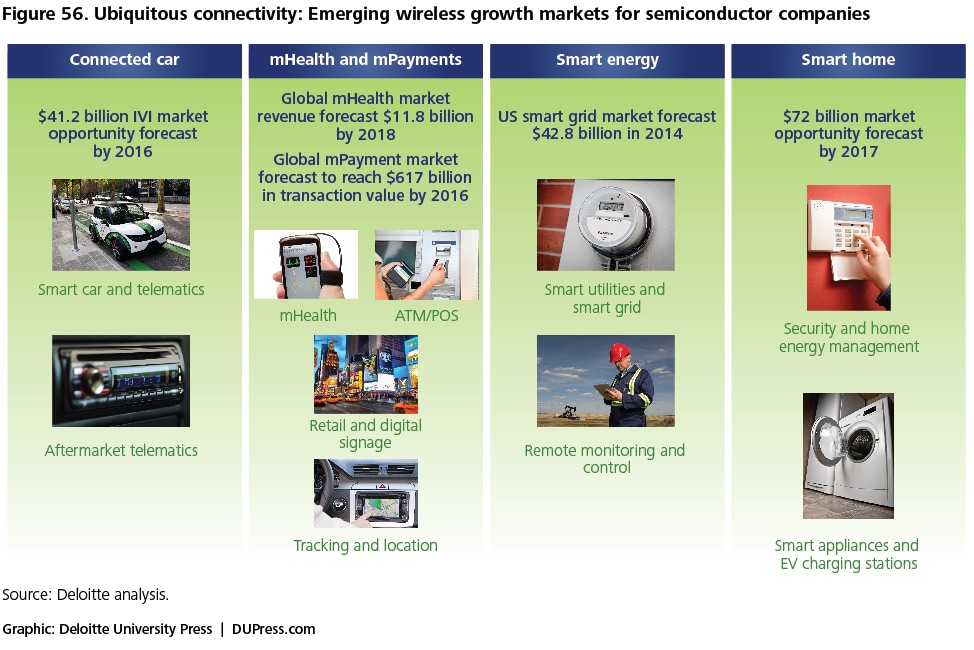

In the world of mobile technology-enabled commerce, mobile payments technology has been the headline grabber for a number of years now. With the adoption of NFC77 technology steadily rising in the United States and global consumer markets, analysts predict that the market for mobile payments will reach $617 billion in transaction value by 2016, with the North American market predicted to grow at a CAGR of 126 percent during 2009–2016 (see figure 36).78

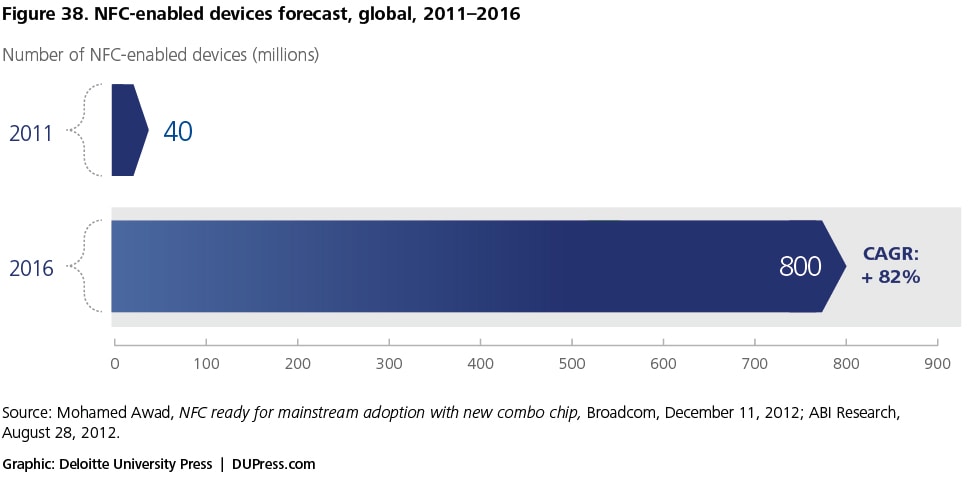

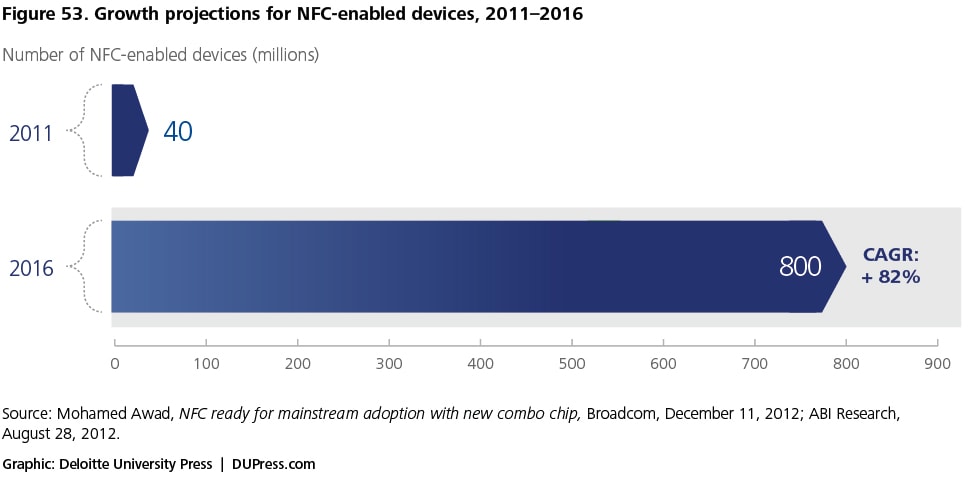

Growth opportunities for semiconductor companies in the area of mobile payments will primarily depend on the scale of adoption of NFC technology and integrated NFC chipsets. In addition to payment technology, NFC is also used for data share functions, interactive gaming, mobile advertising, ticketing, transportation, and wireless streaming. In terms of penetration, nearly 40 million NFC-enabled devices were shipped in 2011, and the market is expected to grow at a CAGR of 82 percent and reach 800 million by 2016 (see figure 38).79 It is estimated that over 50 percent of NFC-enabled devices will be smartphones and 25 percent will be consumer electronic devices. Companies developing NFC chip platforms include NXP, Inside Secure, TI, Broadcom, Qualcomm, and Intel. Many of these chipsets will be integrated into devices such as PCs/notebooks, routers, and gaming consoles.

Despite the bullish forecasts, challenges exist with NFC reaching scale in predicted adoption. In the United States, the mobile payments landscape continues to be marked with uncertainty as competing platforms, ecosystems, and technology standards remain in flux, with major players such as Google, Visa, AT&T, and Verizon pushing ahead in developing their own proprietary consumer platform solutions. Until collaboration and integration occur across the mobile payments value chain, NFC payment transaction values are likely to remain flat in the United States and global markets.80

For chipset manufacturers, a broader outlook on NFC utilization beyond smartphone payment applications will be critical while the mobile payments infrastructure develops to facilitate widespread consumer adoption.

Keys to unlocking growth: Democratize or die!

Not all the smart people work for us. We need to work with smart people inside and outside our company.—Henry Chesbrough, 2003

H aving defined the mobile semiconductor landscape and assessed the most likely industries and end markets for mobile semiconductor growth, in this section we switch our focus to the enterprise and explore the strategies, tactics, and resources used by successful semiconductor firms competing in mobile. Unsurprisingly, the tactics used by these companies for exploiting growth opportunities vary according to the specific industry, product technology, and market offering. However, our research did reveal a number of common threads across the core components of the leading companies’ innovation strategies. Specifically, elements from the open innovation and platform leadership playbooks are thought to be key in pursuing breakthrough innovation in each company analyzed.81 This is enabling the emergence of democratized pathways to growth, allowing companies to look beyond the four walls of their organizations to secure new knowledge and new partners for collaboration. In doing so, company boundaries are becoming permeable and the process for developing mobile technology-based innovation is increasingly distributed and dispersed across geographies and talent demographics.

Open innovation—a decade old and still evolving

A decade has passed since Henry Chesbrough, the Berkeley professor often considered the leading academic on open innovation, laid the foundations for what many think is the dominant model in innovation strategy today. Since then, open innovation has allowed companies from an increasingly wide variety of industries the chance to explore the advantages of cooperation and collaboration and kick-start their previously stagnant innovation process. Even more significant are the risks associated with not pursuing open innovation. Evidence is mounting that firms that do not enter into collaborative knowledge sharing can, as a consequence, expect to shrink their knowledge base over the long term, lose their ability to partner with other organizations, and ultimately stymie their entire innovation capability82—all of which could be bad news for those seeking growth in new mobile markets.

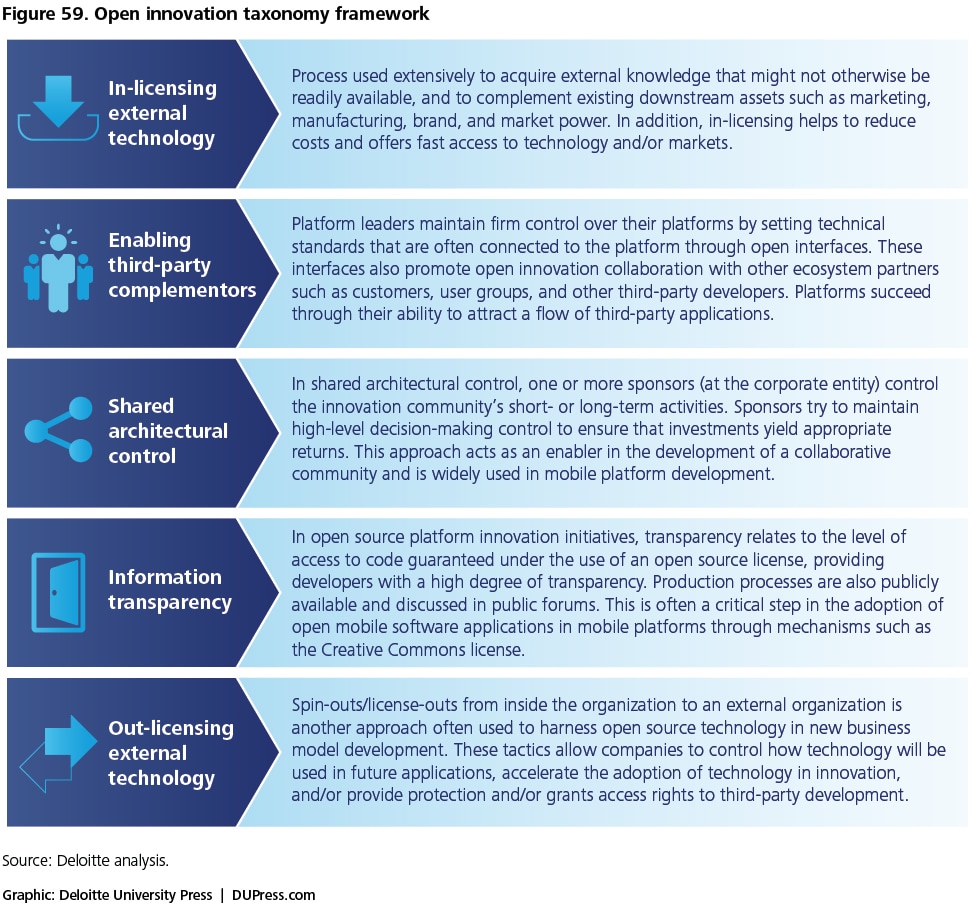

As more companies shift from the traditional closed model of innovation and embrace an open approach, gone are the days of relying on R&D to be kept in-house. No longer do firms need to depend on the old ways of using internal resources to closely guard the development of intellectual property until new products or services are launched in the market. Open innovation is, in many ways, the antithesis of this approach, helping companies look beyond their boundaries to seek and utilize flows of knowledge, both inbound and outbound, to accelerate internal innovation and expand markets for external innovation.83 And as the model becomes more widely used, management research on the topic is increasingly focused on understanding the “mechanics” of execution.84 Consequently, current approaches to making open innovation work tend to fall into three broad process categories: outside-in, inside-out, and hybrid.85

The outside-in process

The most common approach to implementing open innovation is through a series of activities that can be characterized as outside-in processes.86 Here, the objective is to improve the company’s knowledge base primarily to stimulate and enhance the process of innovation. This is usually done by integrating and interacting with external sources of new knowledge such as those in the immediate competitive landscape, including suppliers, clients, customers, and competitors. Other external sources can also include research institutes and non-customers and suppliers from completely different industries. It is here that the importance of developing an astute innovation networking strategy is paramount, with the ability to expand networks into supporting ecosystems that integrate disparate communities now recognized as a core skill.

The inside-out process

The inside-out approach to open innovation concerns the routes by which firms can capture value by bringing ideas to the market, trading in intellectual property, and transferring technologies to the external market for further development.87 Those companies that emphasize an inside-out process as their core open innovation approach primarily look to shift the exploitation of their intellectual property beyond the firm’s boundaries through licensing mechanisms that are often used to spread technology and ideas to other companies and other industries. Value is often generated and captured by using IP licensing royalty fees, making agreements with other firms in joint ventures, and developing spin-off companies, all of which can allow firms utilizing these tactics to collectively generate more overall value from innovation. The focus on new business model innovation in new markets via corporate venturing is also an outlet for larger multinational companies that have the resources to pursue such strategies.

The hybrid (or coupled) process

A hybrid (or coupled) open innovation process focuses on combining aspects of the outside-in approach to secure new knowledge with tactics from the inside-out process to bring ideas to the market. Here, co-creation between usually complementary partners via network alliances, joint ventures, and other vehicles for cooperation is combined with commercialization tactics to develop and exploit innovation.88 Many of the approaches used in this process stem from lessons learned in areas such as open source software development where communities of self-organizing peers evolve to enable product development. These approaches can involve integrating early adopters of technology (also known as lead users), consumers, and universities and research institutes. Partnering with innovation intermediaries such as InnoCentive and crowdsourcing solutions using digital platforms are also examples of deploying a hybrid process in an open innovation strategy. These last two approaches are evidence that developments in social media technologies are enabling companies to interact with an unprecedented variety of partners, drawing them into the heart of their open innovation strategies in all stages of product design, development, and adoption in the market.

Our study on semiconductor companies pursuing mobile technology-based growth synthesized these three process categories into a single framework for analysis. This framework acts as a “lens” through which to view the tactics being used for innovation in each company across a wide range of industries. A notable research finding is the predominant use of platform leadership strategies in pursuing top-line mobile growth.

Platform leadership—at the core of mobile business model innovation

Underpinning many of the critical steps in a company’s open innovation playbook is the use of a broader platform leadership strategy designed to quickly develop and deploy mobile technology platforms and gain traction in emerging mobile growth areas. From a competitive perspective, a number of dominant platform leaders—companies adept at developing and deploying mobile platforms designed to rally other new and established players (usually around particular operating system [OS] technologies) and collaborate on new products and services—have emerged, and they continue to make significant gains in emerging mobile growth areas.89

Platform leaders control the development of a core product or service that usually emerges from a broader technology platform, the growth of which is also under the platform leader’s control.90 Success in this area often relies on the ability to nurture ecosystems of complementors91—firms that support and build/expand the platform to provide greater value for customers. Astute leverage of networks of complementors and the subsequent adoption of the platform by users can lead to large-scale network effects that can then be exploited in the platform’s commercialization phase. The personal computer and video game industries are good examples of where core technology platforms (for example, the Windows platform and the Microsoft Xbox gaming platform) were expanded by networks of developers and supported by the subsequent innovative efforts of complementors who made these platforms a market success.92

Examples of open innovation and platform leadership crossover are increasingly evident in the telecom and mobile sectors, where both strategies are used across industry value chains to gain access to new knowledge and technologies. This is often done via new network partnerships structured to develop product and service platforms that are then used to forge new markets and increase competitiveness. For instance, network carriers are beginning to simultaneously use open innovation and platform leadership strategies to attract partners and customers toward the development of new wireless technology platforms. AT&T, for example, has recently embarked on its high-profile “foundry” strategy designed to boost its venturing capability by orchestrating ecosystems that create new ideas, stimulate product innovation, and provide start-up companies with partnerships to market.93Tactics used often draw on the “collaborative community” approach in which participants in open innovation networks build cooperative relationships in environments where intellectual property (IP) rights are not threatened. This is a key element of network building, aimed at increasing knowledge flows, idea generation, and the adoption of new product platforms in a relatively IP-friendly environment. More competitive approaches are also common in which network partners that compete with each other are driven by the need to maximize value capture through “co-opetition”—in other words, competing in efforts to support the development of a common platform for the benefit of the broader network. In these instances, the formation, adoption, and expansion of network partnerships into supporting ecosystems is thought to be a key step in the process of generating and capturing platform value.94

In today’s mobile world, operating systems such as Google’s Android, the Windows phone, and Apple’s iOS are some of the most prominent stand-alone platforms that help drive industry-wide innovation.95 Each of these platforms successfully integrates separately developed technologies and attracts other third parties to add their own product innovations. Here, the parallels between the emergence of the open mobile era and the evolution of the personal computer (PC) industry are evident. The explosive growth of the PC industry over the last two decades could not have occurred without a broad supporting cast of various companies’ products. Operating systems combined with hardware such as keyboards, monitors, and disk drives, along with software applications and developer kits, all helped fuel the stellar growth of the PC industry. The same evolution can be forecast for the mobile industry.96 The mobile OS platform will likely become a core technology architecture around which layers of hardware and software will be integrated by platform developers and ecosystems of complementors.

Companies looking to boost business model innovation by becoming platform leaders in this area should first leverage network effects to increase the number of people using the platform product. Doing so can lead to more opportunities and incentives for complementor firms to introduce complementary products and services that may assist in growing the platform.97

Understanding the elements of platform leadership

In this study, we define a platform as simply a company’s technological building block of separate, interlinked components. These components can be either hardware or software—or both—which can be further developed and/or added to by third-party developers and, in some instances, competitors. Products can be thought of as platforms when they consist of one component or a subsystem of an evolving technological system. Platforms are normally functionally interdependent with most of the other components of the overall system, which ultimately drives consumer demand. Many proprietary platforms consist of an architecture of related standards, controlled by one or more sponsoring firms. In a mobile computing context, architectural standards could typically encompass a number of processors, an OS, and associated peripherals.

Platform leadership has a number of core elements, some of which overlap with open innovation. For instance, both approaches utilize ecosystems, which can be thought of as stand-alone networks of interlinked companies working cooperatively and competitively to co-evolve capabilities around innovation. Moreover, in the context of “platform ecosystems,” firms may collaborate through a common set of technology standards, creating a base architecture as a platform. Other key elements of platform leadership include:

Platform sponsorship: Platform leaders drive innovation in their industry, motivating others to form communities to supply innovation and support their core product platforms. Companies adept at platform leadership wield tremendous influence and help shape the evolution of their industries. Firms looking to become platform leaders should attack the big challenges in their fields and try to solve industry-wide business problems that affect a large number of firms. To become a leader, companies should then effectively “sponsor” the development of the platform and take on the role of curating, coordinating, and mobilizing co-development networks with partner firms.

Community building: Platform leadership often requires a comprehensive approach to network and ecosystem building to support the development and commercialization of the platform. Leaders facilitate a community of complementors to supply add-on products and services that create momentum around the platform. Companies need to develop supporting innovation communities that reconfigure talent, resources, and capabilities to serve and feed the platforms. Often, these networks, which can be dispersed and drawn together across disparate geographies, mimic the mechanisms of the open source development model, which has traditionally linked self-organizing talent quickly and efficiently to develop code. The same process is now being used to boost product and service innovation focused on enhancing the platform that coordinates their activities.

Platform interface design: The concept of modularity (the ability to separate technical components of the platform) in platform design is an important element of platform leadership. Modularity allows leaders to combine technical innovation with business model innovation, boosting the potential for commercial exploitation while sustaining control over platform integration. Modularity in platform interface design promotes outsourcing in collaborative development, provided that the platform’s architecture and interfaces are appropriately designed to allow users and the supporting ecosystem of innovation communities to develop new product complements. A robust technology and intellectual property plan should also be in place to guide decisions on managing the platform technology interfaces. At this stage, companies should decide how much modularity is required in the technology architecture in order to enhance the core platform technology’s ease of use and compatibility across multiple product generations. Many of the semiconductor industry’s leading products are based on platforms with enhanced modularity built in. From a historical perspective, Qualcomm’s integrated CDMA chip sets were an early example of modular architecture that was used to great effect across a wide range of the wireless industry’s products and services.