2018 InsurTech investment trends and insights has been saved

Analysis

2018 InsurTech investment trends and insights

Part of the FinTech investment series: InsurTech by the numbers

Even though startup activity in insurance has slowed, InsurTech will continue to play a major role in shaping the future of the industry. How can insurers adapt to these changing times and better leverage InsurTech to speed up innovation and digital transformation?

Explore Content

- Declining investments in InsurTech startups

- Shifting investment strategies

- Fueling digital evolution

- Explore our interactive tool

- Get in touch

Declining investments in InsurTech startups

The insurance industry has reached an inflection point: Rather than spreading their money across a large number of new InsurTechs just getting off the ground, many investors have started channeling more capital into proven entities, often in late-stage and follow-on funding rounds.

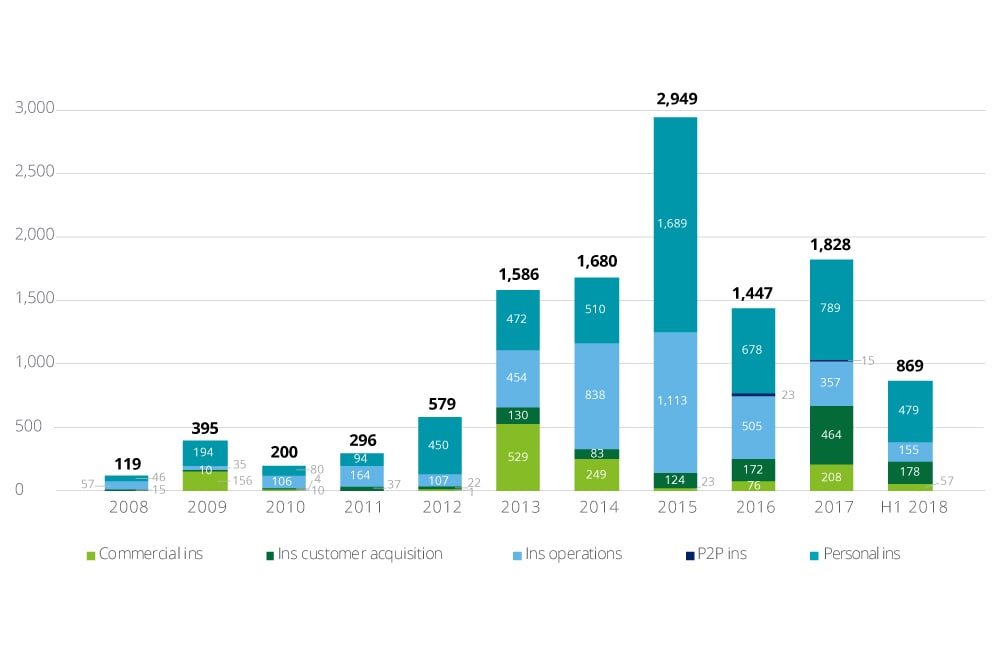

InsurTech startup activity came to a veritable standstill in the first half of 2018. This downward trend began last year, with 2017 seeing the launch of only 88 InsurTechs—half the number recorded in 2015 and 2016.

Startup momentum took longer to peter out for InsurTech, perhaps because insurance activity peaked later than in other financial services industries. The number of new InsurTechs kept rising in both 2015 and 2016, at a time when startup activity in the other financial sectors had already started dropping from its high point.

However, the dramatic decline in startup activity doesn't mean the InsurTech gold rush of the past decade is coming to an end. On the contrary, money continues to pour in, with InsurTech investment of $869 million in the first half of 2018 on track to at least equal the $1.82 billion in funds raised last year, which was the industry's second-highest level of financing.

Shifting investment strategies

On a micro level, while new launches may be fewer and farther between at the moment, InsurTech investment activity is expected to remain robust as investors shift their attention to maturing entities. More established InsurTechs will likely focus on gearing up their solutions to scale, but we may yet see a second wave of new startups not too far down the road in areas where innovation has lagged.

For instance, we expect to see significant action ahead in small- and middle-market commercial insurance, as personal insurance innovations in customer acquisitions, operations, telematic sensors, and analytics are adapted for business insurance applications.

On the other side of the industry, life insurance and annuities are generating far less InsurTech activity than among their property and casualty counterparts. But we believe that is likely to change as life insurers seek to streamline products, simplify underwriting, and advance self-service distribution systems. Life insurers, for example, will likely tap InsurTech insights to broaden accelerated underwriting capabilities with the help of advanced analytics and established ongoing wellness relationships with policyholders.

At the same time, we think that annuity writers could potentially benefit from more intuitive and interactive InsurTech tools that help consumers navigate and manage these often-complex products, as well as understand their long-term value versus alternative investment options.

Fueling digital evolution

InsurTechs are looking to carve their own niche in the emerging digital insurance marketplace by catering to evolving customer needs and rising expectations. Many incumbents are often helping to finance experiments by InsurTechs—which would at first appear to be competitors—in part to likely learn about the digital marketplace and perhaps complement their own more traditional business models.

Yet a majority of InsurTechs aren't seeking to compete with, let alone displace, incumbents. Instead, most are being launched to help solve legacy insurer problems across the organization, from general operations inefficiencies to enhancing underwriting, distribution, and claims functions. Insurers can leverage InsurTechs to speed up innovation and the digital evolution, integrating the newcomers' next-generation technical capabilities and entrepreneurial culture to become the digital insurers of the future.

InsurTechs could ultimately accelerate the transition of incumbents to become more customer-centric, data-driven, and multi-platform-based. InsurTech innovation can help stitch together capabilities across the insurance value chain so carriers are better able to meet the needs of consumers, agents, and brokers.

By collaborating with InsurTechs, we think traditional insurers may be able to more quickly and efficiently innovate in their approaches and operations to take advantage of four strategic options made possible through digital transformation:

- Delivering ahead of customer expectations

- Accessing new markets and segments

- Shifting from purely underwriting risk to providing more comprehensive well-being (in terms of physical and financial security)

- Reimagining the operating model to generate higher profitability

Four strategic options made possible through digital transformation:

- Delivering ahead of customer expectations

- Accessing new markets and segments

- Shifting from purely underwriting risk to providing more comprehensive well-being (in terms of physical and financial security)

- Reimagining the operating model to generate higher profitability

Where might insurers go from here?

To learn more about this next wave of InsurTech investment, download our full report.

Want to take a closer look at fintech activity? Explore our interactive tool.

Get in touch

Recommendations

The fintech revolution

A catalyst for change