Article

COVID-19: IFRS 9 Impairment and the Certificates of the Emergency Situation

20 March 2020

No forward-looking model could have predicted the features of COVID-19 medical situation and its implications. Moreover, not even after the COVID-19 medical situation was recognized as pandemic, it is not clear how the situation will evolve considering that different measures are taken across the globe.

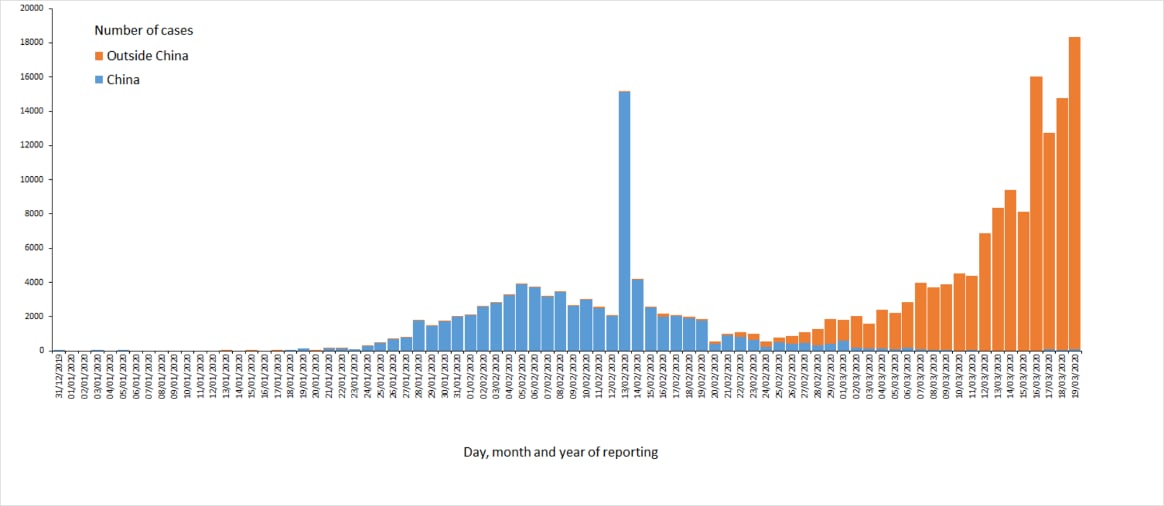

We see China reporting very positive outlook every day, and very steep increase in cases across Europe, America, Africa, Oceania, although measures are being taken and there’s more knowledge related to the way of contamination and prevention compared to the beginning of the medical situation.

Source: https://www.ecdc.europa.eu/en/geographical-distribution-2019-ncov-cases

Before the virus extension, the expected models for the recognition of expected losses on financial assets were built considering the relationship between macro-economic indicators and the expected loss prediction elements. In the absence of models that can predict the propagation of the recessions in different economic sectors under the specific COVID-19 situation, the financial institutions will continue to use existing IFRS 9 macro-models until tailored prediction models are developed.

Various scenarios will have to be considered about the length of the quarantine period needed to get the virus under control, how soon the activities will be retaken, where the production will be positioned, how consumer demand will be like after the situation settles or finds an equilibrium. Several sectors will take more time to recover, while others will need to transform or reinvent themselves.

China is one step ahead the rest of the world controlling the medical situation according to official reporting, but it is difficult to anticipate how improved medical status will be reflected in the economy considering cross-country and cross-continental economical dependencies. In addition, given the fact that in the rest of the world, the medical situation does not show signs of resolution, further restrictions will be imposed.

Governments around the world are taking economic and fiscal measures to limit the impact of the restrictions stemming from the pandemic, National Banks are considering or have already taken financial measures for strengthening the capital and liquidity positions of the banks while supporting at the same time the joint effort to protect the economy.

In Romania, companies in transport, tourism, horeca, event organizing, publicity, private education and adjacent activities, clothing, shoes and leather industry and public services, which are strongly affected by COVID-19, will be entitled to receive fiscal facilities, ask for concessions in the relation with the leasing, banking and financial institutions or any other public institution, renegotiate certain contracts under the condition they obtain from the Ministry of Economy the Certificate of the Emergency Situation. The Certificate can be further used by the financial institutions to predict the expected loss impact, and most important, to allow them to consider special treatment in case of moratorium by force of law and to exclude them from classification as default and non-performing exposures.

Similar measures are and will be taken across the world, impressive funds are disbursed to limit the impact and it is of utmost importance to find levels of control to avoid abuse and excessive use of aid measures where they are not justified or ultimately necessary.

Contact