Artikel

Deloitte CRR III Survey results reveal how prepared banks are for Basel 3.1

The Deloitte CRR III Survey assesses the state of 52 participating banks, including 10 banks from the Nordic region. The participants, including members of the risk, capital management and finance teams in banks, expect the adjustments required to implement CRR III to go beyond an update to the calculation of Risk Weighted Assests (RWAs) and regulatory reporting engines. Broader strategic implications and/or significant adjustments to the IT environment need to be addressed, in addition to achieving compliance. However, as compliance with the requirements is mandatory, with implementation activities needing to intensify in 2023, for banks to achieve a high quality, fit for purpose and timely outcome.

This is the third publication in the “Basel 3.1 – Nordics ready!” blog series. The series covers aspects of Basel 3.1 where bank management teams in the Nordic region are focused, including minimum capital requirements, the regulatory landscape, the strategic and operational considerations, and how to implement Basel 3.1 for the long term.

Explore other related articles

1. Now is the time to act on Basel 3.1 implementation

2. Capital requirement calculations under Basel 3.1

3. Deloitte CRR III Survey results

4. The Basel 3.1 impact on strategy and operations in the Nordics

Overall, our CRR III Survey shows that at the time results were collected (mid-2022), most banks had not started implementation projects, with plans in place to kick-off implementation projects no later than 2023. The new Basel 3.1 rules are expected to result in greater complexity, so management teams should be conscious of balancing the benefits of a later start to implementation activities (e.g. greater regulatory clarity) with the reduced time available to understand and mitigate the drivers of the expected changes associated with a shorter implementation project timeline.

The full CRR III Survey results are available for download to the right.

Key takeaways

Survey design and data basis

- Our survey assesses the state of preparation for Basel 3.1 in banks, with participants from 52 institutions from 14 different countries, including 10 banks from the five Nordic countries.

- The banks participating apply a range of regulatory capital approaches, with 22 of the institutions exclusively using standardised approaches and 30 institutions applying internal models to determine the minimum capital requirements (for at least one risk type).

Capital impact and drivers

- Expected change in RWAs resulting from Basel 3.1 remain in line with previous supervisory findings and impact studies, with most participants expecting significant increases in the minimum capital requirements.

- The output floor is expected to drive the most significant impact, primarily for real estate lending (where the difference between the risk weights in standardised approaches and internal models is largest), followed by corporate lending and unsecured consumer lending portfolios.

- The RWA impact of Basel 3.1 changes for banks applying the Standardised Approach (for credit risk) varies depending on I) the portfolio structure, ii) external rating coverage and iii) collateralisation in the real estate.

- The RWA impact of Basel 3.1 changes for the internal models appear to be comparatively modest, with changes driven by updates to the regulatory Loss Given Default (LGD) in the foundation approach (lower RWA) and the input floors (higher RWA).

Strategic impact of future capital requirements

- The variation in RWA calculation changes mean that management teams will have to reassess the capital effectiveness of each product and/or business area, with more than 60% of the respondents expecting capital planning and pricing actions, and about two-thirds indicating that they intend to conduct an RWA optimisation exercise

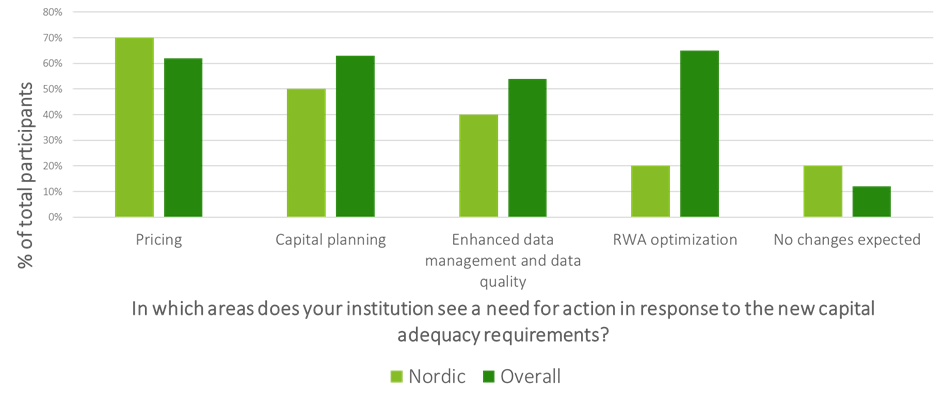

- Nordic participants are primarily focused on pricing and the majority have not yet considered RWA optimization (shown in Figure 1). This is likely due to strong capital ratios in the region currently but may also be an effect of optimization being constrained by local regulatory floors.

Figure 1: Expected areas where action is needed in response to the new capital adequacy requirements split by Nordic and overall respondents.

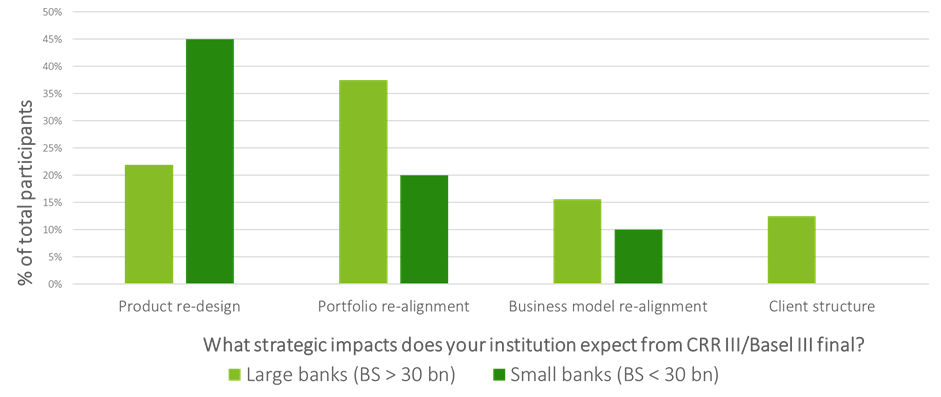

- Approximately 30% of the respondents expect that adjustments in product design (particularly smaller banks) and/or some level of portfolio realignment (a focus for larger banks) will be necessary to ensure integration of the capital requirements into product calculations is appropriate (summarized in Figure 2). This is reasonable consistent with the focus stated by Nordic banks.

Figure 2: Expected strategies split by the total assets of the respondent

- More than 50% of banks stated that they need to improve data management and/or data quality connected to RWA optimisation, with the data required for more favourable recognition of transactions, often not available or outdated.

Implementation of the new rules

- Projects will require structural adjustments to the IT environment.

- New reporting solutions need to be adopted, with one out in seven banks expecting a fundamental change being required to risk and finance data and/or the reporting IT infrastructure whilst a similar number expect to change their entire reporting solution.

- 25% of the participants foresee major challenges and expects significant effort in the implementation of the new standardised approach for credit risk, especially future capital requirement for real estate exposures and the newly introduced due diligence process for the use of external ratings.

Benefits from IRB

- The current choice of regulatory approaches may no longer be ideal, with the survey highlighting that the expected IRB coverage ratios will change. The use of internal model approach are in some instances, more attractive for mono-line lenders which are currently using the standardised approach for credit risk.

- Due to the output floor and the cost of compliance, many IRBA banks in our sample are currently considering reverting from the IRBA to the standardised approach for targeted portfolios (or in the entirety). Portfolios with scarce defaults are difficult to model and achieve regulatory approval (e.g., central governments/central banks, public sector entities or financial institutions) so will likely revert to the standardised approach.

We will continue our blog series with a focus on the strategic and operational considerations related to Basel 3.1 as well as an overview of the regulatory landscape in the Nordics. Stay also tuned for the publication of our white paper “To be or not to be IRB” in the coming weeks. If you have any questions or challenges to discuss about these topics, please do contact us.

Deloitte CRR III Survey