Artikel

Leader: Now is the time to act on Basel 3.1 implementation

Basel 3.1 is expected to be adopted in 2023 in the EU and applied from the 1st of January 2025. This blog provides an overview of the changes in the newest Basel reform, when it will come into force and how it impacts Nordic banks.

Explore Content

- Evolution of the Basel framework

- what changes in Basel 3.1

- Implementation of Basel 3.1 – deadline for EU set for early 2025

- The impact of Basel 3.1 in the Nordics

This is the first of six blogs we publish from the “Basel 3.1 – Nordics ready!”. The series covers various aspects of Basel 3.1 with a focus on considerations for banks in the Nordic region, including minimum capital requirements, the regulatory landscape, the strategic and operational considerations, and how to implement Basel 3.1 for the long term, in the Nordics.

Explore other related articles

1. Now is the time to act on Basel 3.1 implementation

2. Capital requirement calculations under Basel 3.1

3. Deloitte CRR III Survey results

4. The Basel 3.1 impact on strategy and operations in the Nordics

Key takeaways

- Basel 3.1 refines the standardised approach by adjusting and introducing new risk weights for different types of exposure classes.

- Basel 3.1 significantly reduces the potential for capital reduction using IRB models due to the new RWA output floor. This is a key change in the new reform and financial institutions need to review their risk model landscape and capital planning accordingly.

- The phase-in implementation of Basel 3.1 will most likely start in 2025 in the EU.

- While the EU ‘banking package’ (CRD6 / CRR3) is not yet finalized, it will likely deviate from the Basel accords on some parts.

- The current estimate for finalisation date for the package is end of 2023.

- The Nordic regulators have not confirmed their implementation plans, although these are anticipated to be aligned to the EU timeline.

- The capital impact of Basel 3.1 is expected to be greater for Nordic banks than at a global level due to higher concentration of low-risk mortgage portfolios and active use of the IRB approach.

Evolution of the Basel framework

The Basel framework has continuously evolved over the last 3 decades to ensure proper capital and risk management by financial institutions. The Basel Committee of Banking Supervision (BCBS) is responsible for developing and setting the Basel accords, to increase financial stability by increasing transparency and quality of bank supervision worldwide. Since its inception (in 1974) the BCBS has published a number of different iterations of the Basel accords.

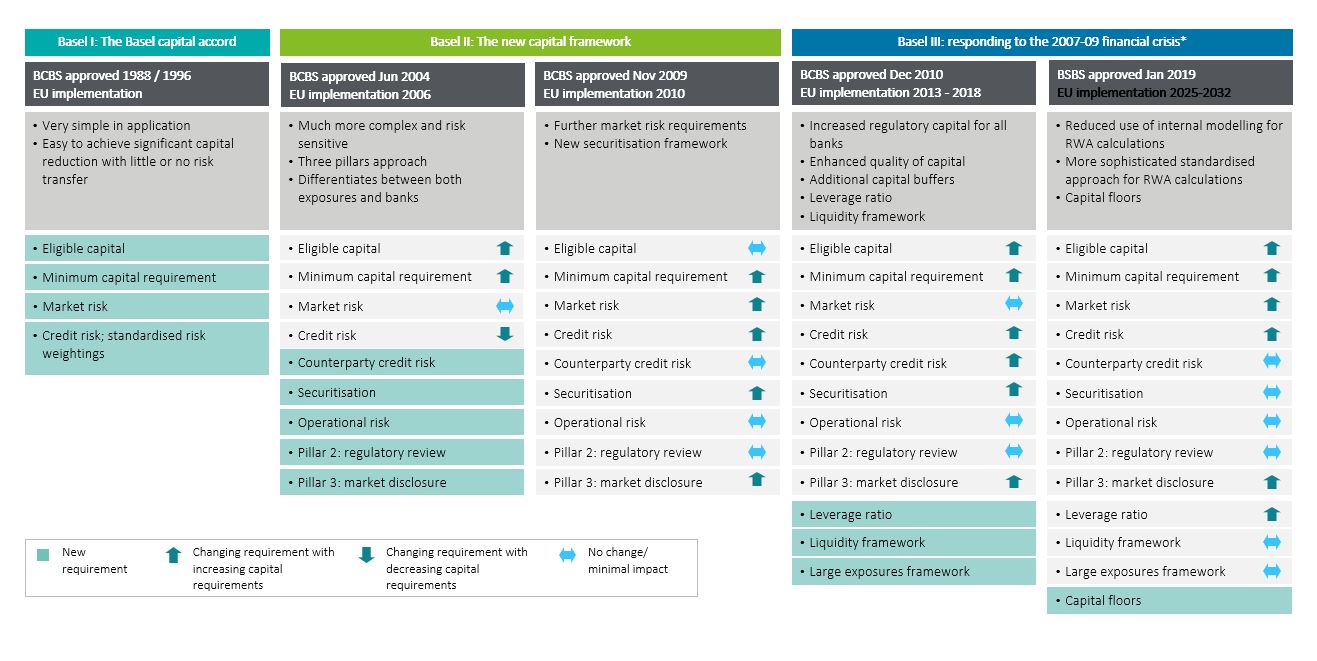

The Basel I capital framework was a simple framework which provided the foundation for later Basel accord iterations. Perhaps the most significant aspect of Basel I was the introduction of the minimum capital ratio to risk-weighted assets (RWA) of 8%. The capital ratio was designed to create global consistency across the different jurisdictions and remains a strong foundation of the framework. In Basel II the capital framework became more complex and risk sensitive with the three pillars approach and internal rating based (IRB) approach to measuring minimum capital requirements introduced – both still in use. The Basel II reform introduced additional market risk requirements and a new securitization framework. Basel III was developed in response to the 2007–2009 financial crisis. It includes an increase to minimum regulatory capital requirements for all banks, enhanced required quality of capital, additional capital buffers and a leverage ratio and new liquidity framework.

Image 1. Overview of how the Basel framework has developed over multiple decades, increasing in scope and sophistication over time.

Introducing a more sophisticated standardised approach and output floor – what changes in Basel 3.1?

Basel 3.1 introduces changes to how to calculate capital requirements for all risk types, for both standard and internal models and will mean higher capital needs for most banks. Previous Basel accords gave banks significant freedom in calculating RWA, particularly under the IRB approaches. This has led to a high variability in capital requirements calculated by banks. The high variability has raised concerns with regulators and market participants about the viability of RWA reporting. Basel 3.1 is designed to simplify and reduce variability in RWA calculations across different banks and jurisdictions, by reducing the variability in IRB capital requirements and introducing a more sophisticated standardised approach for RWA calculations.

The new reform introduce a capital floor, in which the RWA derived through the IRB approaches must be at least 72.5% of the RWA derived from the standardised approach . Furthermore, the scope of exposures which can be included in Advanced-IRB (A-IRB) is more limited. For real estate exposures, the more sophisticated standardised approach introduces credit risk RWAs that depend on the collateralisation, more specifically Loan-to-Value (LTV) at origination. Similarly for corporate exposures, the standardised approach introduces separate RWAs based on external credit ratings (for BBB+ to BBB-) and a specific risk weight for SMEs.

Basel 3.1 revises the leverage ratio framework, with changes made to the way total exposure is calculated and the introduction of a leverage ratio buffer for global systemically important banks (G-SIBs). In operational risk the new reform includes recalibration and simplification components, looking to drive consistency across the industry, particularly regarding the identification and recognition of prior operational losses. This is achieved by removing the advanced measurement approaches (AMA) for operational risk and replacing the existing three standardised approaches, with a single standardised approach. The refined CVA framework aims to enhance risk sensitivity by removing the internal modelled approach and aligning to the revised market risk framework. Market risk is covered in a separate but linked framework for market risk (FRTB), which was revised by BCBS in 2019, and in practice, is included in the full implementation package of Basel 3.1.

Implementation of Basel 3.1 – deadline for EU set for early 2025

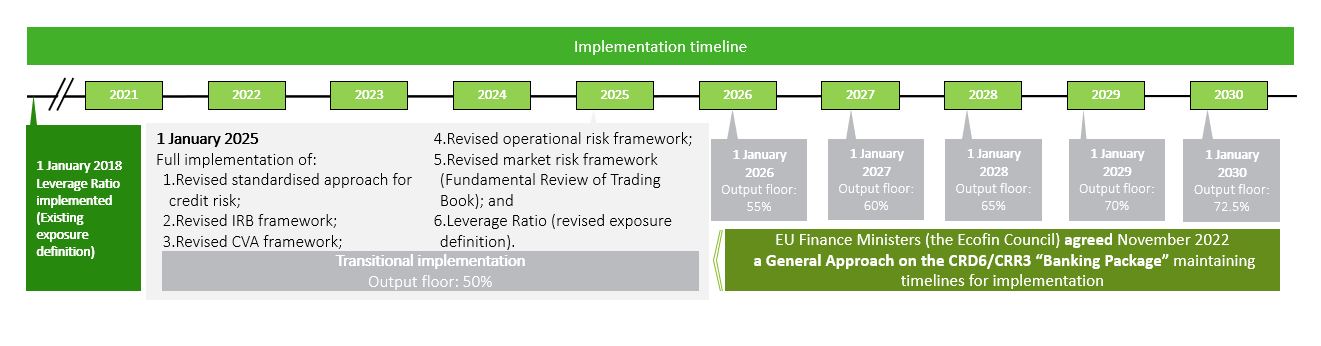

The Basel 3.1 expected implementation deadline in the EU is the 1st of January 2025 which Nordic prudential regulators is anticipated to align with. BCBS approved Basel 3.1 in 2019 and targeted implementation to start on the 1st of January 2023. The European authorities will enforce Basel 3.1 in the banking package (CRR3/CRD6) which initially was scheduled for the beginning of 2023 but was postponed to the beginning of 2025, in response to the COVID19 pandemic. Thus, the expected implementation timeline in the EU is 2025 with a phase-in period lasting until 2032. Other major jurisdictions (such as the UK and the US) are also expected to start implementation in 2025. CRR3 / CRD6 are anticipated to be finalized at the end of 2023, which leaves banks only just over a year before the 2025 implementation to ensure compliance with the new legislation. However, no major changes are expected in the final version to be published later this year and banks have already started to take actions in, among others, their model risk management, data management and financial (capital and liquidity management) planning to prepare for the new reform.

At EU level, Basel 3.1 is not implemented directly into European legislation. In fact, there are some significant divergences in the EU Commission’s and EU Council’s proposed packages compared to the Basel III reform, such as lower capital requirements for some low-risk exposures to residential mortgages under the IRB modelled approaches. Further discussion of the modifications proposed by the Commission is discussed in Implementing Basel 3.1 in the EU: Delay, Defer, Diverge – and more.

Image 2. EU implementation timeline of Basel III reform through CRD6 and CRR3

The Nordic prudential regulators have not confirmed their implementation plans once the European legislation is finalised, although these are anticipated to be aligned with the EU timelines, consistent with the European Central Bank (ECB) and European Banking Authority (EBA). However, local implementation timelines will depend on local legislative processes, which may cause a delay on the effective date.

The impact of Basel 3.1 in the Nordics

The capital impact is expected in the Nordic banks to be higher than other jurisdictions due to higher concentration of low-risk mortgage portfolios and active use of the IRB approach. The impact of Basel 3.1 will vary significantly due to regional differences in banks’ adoption and use of IRB approaches. Like many European banks, the Nordic banks have been active users of the IRB approach and thus the reduced capital benefits of being IRB will impact the Nordic banks more than the average bank on a global level. Capital requirements will especially increase for low-risk A-IRB portfolios due to the new capital floor. On the other hand, in the Nordics, some standardised portfolios will see a reduction in capital requirements driven by the loan-to-value (LTV) driven approach in the refined standardised approach for real estate exposures. However, the overall impact for Nordic banks will be higher capital requirements on average.