Analysis

2015 Global Health Care Sector Outlook

Common goals, competing priorities

Across the globe, governments, health care delivery systems, insurers, and consumers are engaged in a persistent tug-of-war between competing priorities: meeting the increasing demand for health care services and reducing the rising cost of those services.

This report examines the current issues impacting the global health care sector, provides a snapshot of activity in a number of geographic markets, and suggests considerations for stakeholders as they look ahead to 2015.

Overview

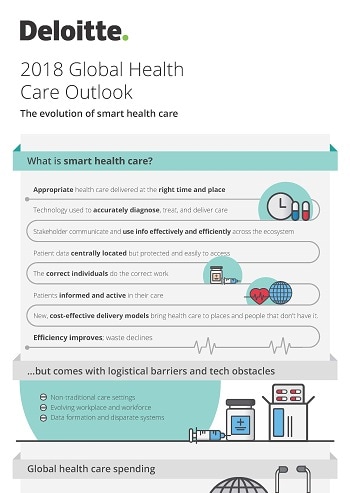

With the ever-evolving policies, processes, and capabilities and the given magnitude and complexity impacting the sector, smart health care is not going to come easy. Clinicians, usually, have difficulty coordinating appointments and procedures, sharing test results, and involving patients in their treatment plan. In other words, care providers may be working hard but are they working “smart”? How is health care moving the barriers of the hospital walls? This 2018 outlook reviews the current state of the global health care sector; explores trends and issues impacting health care providers, governments, other payers, and patients; and suggests considerations for stakeholders as they seek to deliver high-quality, cost-efficient, and smart health care.

Global health care sector issues in 2018

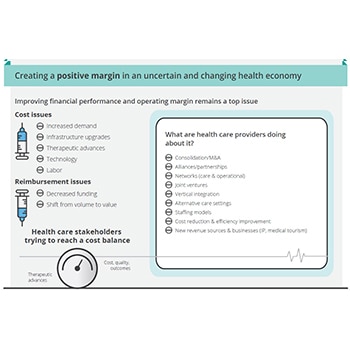

Creating a positive margin in an uncertain and changing health economy

Public and private health systems have been facing revenue pressures and declining margins for years. The trend is expected to persist as increasing demand, infrastructure upgrades, and therapeutic and technology advancements strain the already limited financial resources. As a result, spending is expected to be driven by aging and growing populations, developing market expansion, clinical and technology advances, and rising labor costs. As health care costs increase though, affordability and insurance coverage remain problematic. Health care providers are also collaborating to gain competitive advantage.

Key takeaway

Health care stakeholders are pursuing new cost reduction measures, such as developing alternative staffing models, shifting patients to outpatient services, and reducing administrative and supply costs. In addition, they are exploring new revenue sources such as intellectual property (IP) capitalization, investing in JVs, commercializing their foreign assets, and launching new companies and philanthropic organizations.

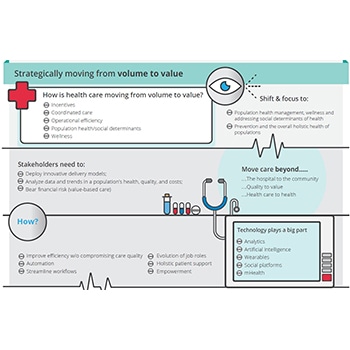

Strategically moving from volume to value

The health care industry is participating in risk-bearing, coordinated care models and continues to move away from the traditional fee-for-service (FFS) system. Stakeholders are moving from volume to value through reform policies, programs promoting operational efficiency, technology use, population health management, wellness, and addressing the social determinants of health.

Key takeaway

A successful transition to value-based care requires that market players and consumers move beyond transaction-based treatment to the holistic health of populations; from treatment to prevention/wellness; and from individual to population health. Health care providers can also look at deploying innovative care delivery models based on data and analytics.

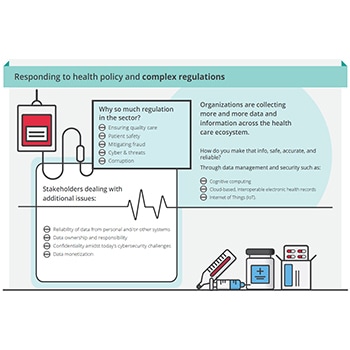

Responding to health policy and complex regulations

Health systems worldwide share overarching health policy and regulatory goals—ensuring quality care and patient safety, mitigating fraud and cyber threats. Digital health care technology solutions addressing better diagnostics and more personalized therapeutic tools are leading to the challenge of data protection.

The trends in data management and security include cognitive computing, cloud-based, interoperable electronic health records, and Internet of Things (IoT). Cybersecurity and data risk management continue to be front and center, especially with patients taking a more active control of their health, and wanting access and reliability to their data.

Key takeaway

Holistic approaches to investments in people, processes, and technology will be key to regulatory compliance. A thorough assessment by health care businesses to understand how recent and upcoming policy changes will impact organizational priorities is an imperative. Care providers also need to explore strategies to build second-line defenses to reduce their administrative, financial, and reputational exposure.

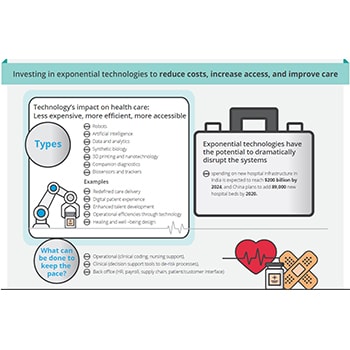

Investing in exponential technologies to reduce costs, increase access, and improve care

Exponential technologies are driving less expensive, more efficient, and more accessible care delivery on a global scale. A few trends which impact care delivery are

- Exponentials will reshape health care by impacting areas such as synthetic biology, 3D printing and nanotechnology, and companion diagnostics amongst others.

- Hospitals of the future are being built through redefined care delivery, digital and AI technologies, and enhanced talent development.

Key takeaway

Organizations may meet some of the objectives of care delivery through digitization of the health care system. At the outset, keeping pace with rapid technology developments is likely to require massive investments in electronic patient records, eHealth/mHealth, interoperability, and big data amongst others. Organizations should consider strategic investments in people, processes, and premises enabled by digital technologies.

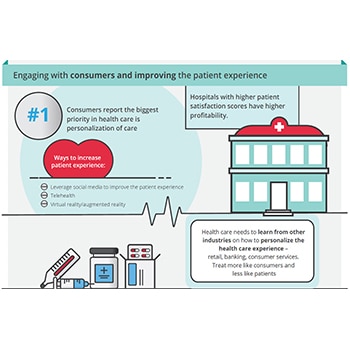

Engaging with consumers and improving the patient experience

Hospitals can provide more personalized care through better engagement with consumers and elevate patient experience by using digital solutions to aid omni-channel patient access, including customer apps, patient portals, personalized digital information kits, and self-check-in kiosks. Other digital channels, and tools to enhance provider-consumer interactions include:

- Leveraging social media to improve patient experience

- Telehealth

- Virtual reality/augmented reality

Key takeaway

Health care organizations should consider extending their focus beyond price and quality of care to creating a customer-centered relationship. Health care has an opportunity to learn from other industries (consumer products, financial services, and hospitality, as examples) how to more effectively target, serve, communicate with, and retain customers and patients.

Shaping the workforce of the future

Workforce challenges in the health care industry, such as staffing shortages in hospital specialties and nursing shortages are evident across the globe. Compounding the problem is a scarcity of next-generation skills to guide and support the transformation to becoming patient-centric, insight-driven, and value-focused organizations. When planning for the future of work, health care organizations will need to assess the physical proximity, automation level, and talent category.

The global health care sector outlook for 2015 is mixed. Treatment advancements and government initiatives to increase access to care should drive sector expansion but pressure to reduce costs is escalating. Growing populations and consumer wealth are increasing demand for health care services but aging societies and chronic diseases are forcing health payers to make difficult decisions on benefit levels. In the midst of this tug-of-war, many historic business models and operating processes will no longer suffice. Read on to learn more about trends impacting the global health care sector in 2015 and suggested considerations for stakeholders. Four major trends are anticipated to impact stakeholders along the global health care value chain in 2015: cost, adapting to market forces, transformation and digital innovation, and regulations and compliance.

Key takeaway

Digital technology, robotics, and other automated tools have enormous potential to resolve current and future health care workforce pain points. Health care providers should embrace strategies where talent can collaborate with technology to improve efficiency instead of competing against each other.

Visit our 2018 Life Sciences Outlook to learn more about the trends and issues impacting the life sciences sector.

Access previous versions

Review or download previous health care sector outlooks.

2017 global health care sector outlook

2016 global health care sector outlook

Global health care sector trends in 2015:

1、Cost: Cost is the biggest health care issue facing most countries in 2015. Pressure to contain costs and demonstrate value is coming from all sides.

2、Adapting to market forces: Five forces are requiring providers and health plans to rethink traditional business models to better address shifting or emerging health care challenges and opportunities: (1) Increasing role of government; (2) Scales to prosper; (3) Competition for talent; (4) Improving access to care; (5) Consumerism.

3、Transformation & digital innovation: Adoption of new digital HIT advances such as electronic health records, mHealth, telemedicine and predictive analytics is transforming the way physicians, payers, patients, and other health care stakeholders interact.

4、Regulations & Compliance: The global health care regulatory landscape is complex and evolving. The primary driver is patient health and safety; however authorities’ approaches to protecting patients can vary widely from country to country.

Recommendations

The digital hospital of the future

In 10 years, technology may change the face of global health care delivery