Is the inflation tide turning for central banks?

Not quite. Stubbornness in core inflation, strong consumer spending on services, and tight labor markets mean it may be too soon for central banks to declare victory over inflation.

On July 12, as data on consumer prices in the United States trickled in, there was palpable excitement in financial markets.1 Inflation,2 which had shot up to as much as 9.1% a year back, fell to 3% in June.3 With price pressures declining, the question that some were asking was whether monetary policy will reverse course? It didn’t turn out that way. For just as Chairman Powell had hinted back in June,4 the Federal Open Market Committee (FOMC) raised rates by another 25 basis points (bps) in end-July.5 That’s hardly surprising for many economists tracking inflation in the United States and Europe. While inflation has been going down as supply chains bottlenecks ease and energy prices decline, core inflation—which excludes energy and food prices—hasn’t declined at the same pace. That’s the measure of inflation that central banks want to bring down to target levels.

Central banks in the West, however, face a tough choice.6 Do they keep hiking interest rates to bring down core inflation? Or they wait to see the impact of previous hikes, as monetary policy works with a lag? Any further tightening also poses risks for banking, financial services, and real estate. In emerging economies, it’s a mixed bag. Some central banks like in India and Brazil have seen headline inflation fall to desired levels and, hence, have paused rate hikes. Yet, they have reasons to worry. More rate hikes in the West would widen interest-rate differentials, which in turn may lead to capital outflow and currency depreciation. Nevertheless, as price pressures ease in these economies, they may be tempted to take the first steps to ease monetary policy this year and shift their focus from inflation to growth.

Two key contributors to inflation have eased in recent times

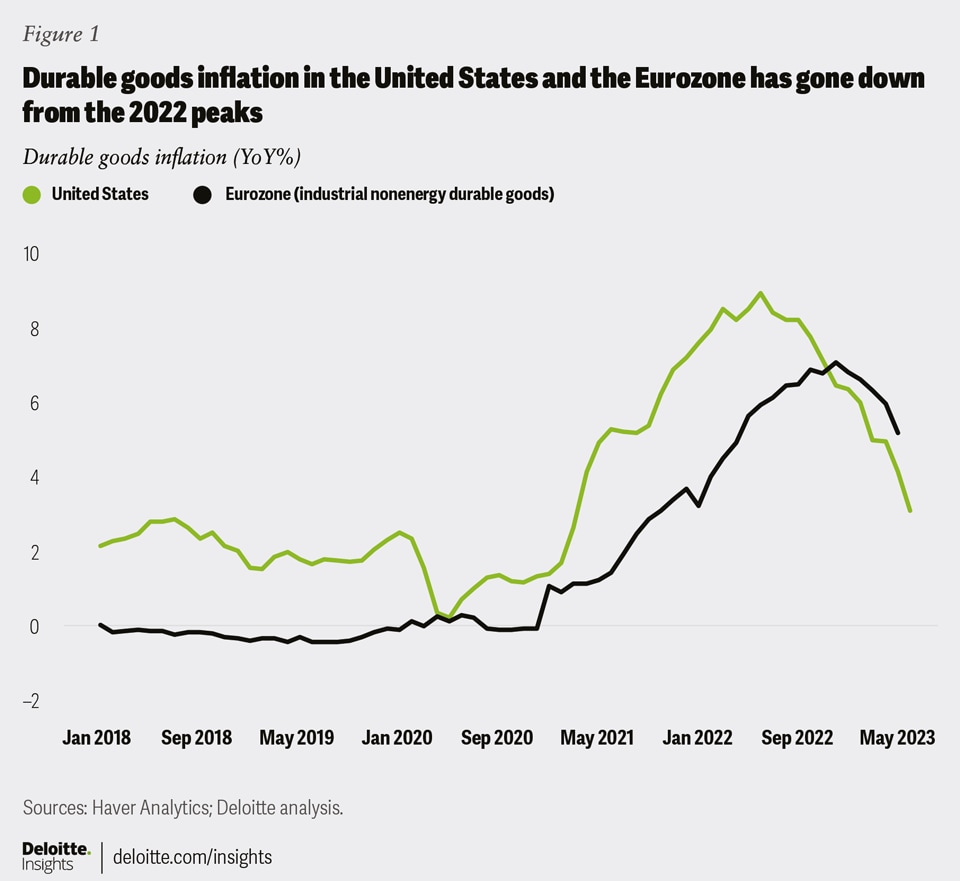

The first push to consumer prices between 2020 and 2022 came from supply chain constraints. Well-oiled global supply chains suddenly developed cracks as COVID-19 spread across the world in 2020. The issue intensified next year as production couldn’t keep with rising consumer demand for durable goods.7 For example, the Federal Reserve Bank of New York’s global supply chain pressure index kept going up through 2021 before finally peaking by the end of the year.8 Durable goods inflation, as a result, went up sharply between 2021 and 2022. Thankfully, supply chain pressures have eased considerably in recent quarters. Sharp decline in virus cases and widespread vaccinations starting in 2021 have helped. Also, consumer spending is now steadily shifting from durable goods to services.9 No wonder then, that, durable goods inflation has gone down in recent months (figure 1).

{kind=link}

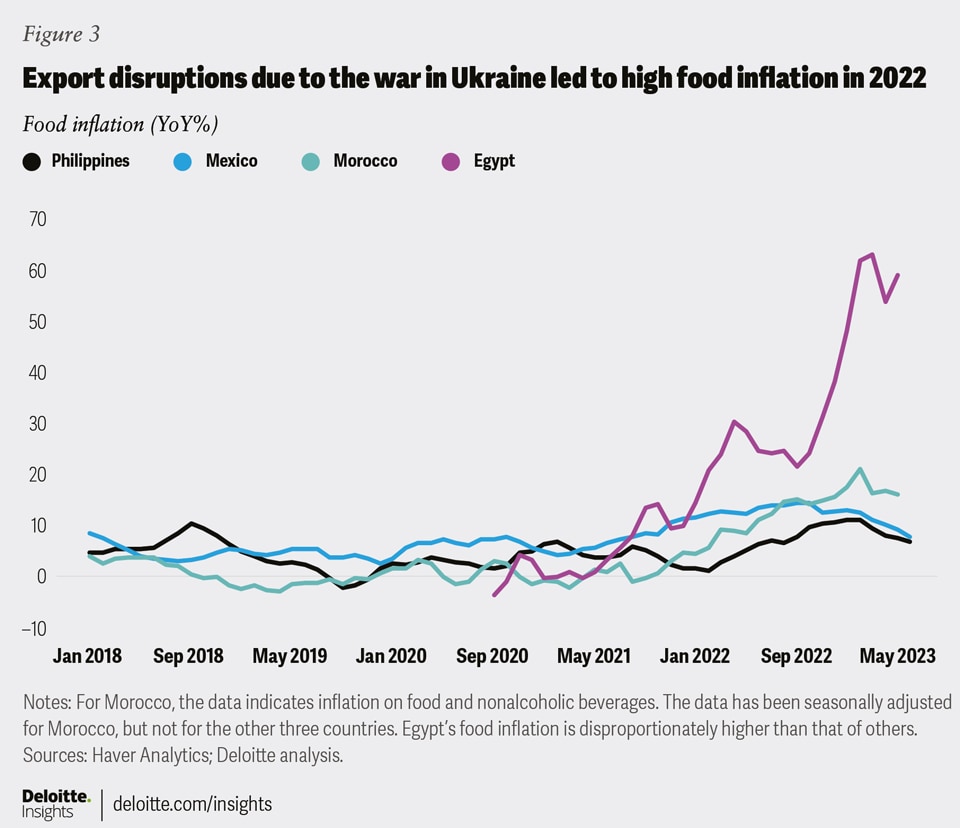

Commodities was the next big contributor to inflation in 2022. Energy prices shot up last year due to Russia’s invasion of Ukraine and subsequent sanctions by the West on Russia’s energy trade. The price of Brent crude surged 40% between January and June of last year. The spike in natural gas prices was even higher—by August 2022, natural gas prices were up 131% from January.10 For Europe, which had long enjoyed relatively cheaper Russian energy, the search for alternative suppliers came at a higher cost (figure 2), compared to advanced economies outside the continent.11 Ukraine and Russia are also major grain producers and therefore, export disruptions pushed up global food prices.12 This twin surge in energy and food producers hit major importers the most, especially in emerging and developing economies (figure 3). Energy and food inflation have, however, eased since their peaks of 2022. The decline in energy prices has been greater, given their sharp peaks in 2022.

{kind=link}

{kind=link}

Central banks have cracked down aggressively on inflation

By early 2022 many central banks realized that price pressures had become more broad-based than before the Russia-Ukraine war. Monetary policy response, therefore, was swift and strong in many countries. In the United States, the Federal Reserve (Fed) has hiked its key policy rate by 525 bps so far since March 2022. The pace and scale of this tightening is the highest since 1982. The Fed, however, isn’t alone. The Bank of England (BOE) has hiked rates by 515 bps since December 2021 while in the Eurozone, the refinancing rate is now at its highest since 2008. Central banks in Latin America also moved fast to stem inflation. In Brazil, the central bank started tightening policy from March 2021; by August 2022, it had hiked its key policy rate by 1175 bps. In Mexico, policy rates have gone up by 725 bps. In Asia too, central banks upped the ante against inflation, but the pace is slower than their counterparts in Latin America and the West (figure 4).

{kind=link}

Thankfully, most of the monetary tightening measures are showing results. Demand growth has slowed in recent quarters. Germany entered a technical recession in Q1 2023 and growth also slowed in the United States and France. India, too, despite outshining other economies in terms of growth, slowed in the second half of FY 2022–2023. Slowing demand, in turn, is weighing on consumer price growth. Figure 5 shows that headline inflation has been steadily edging lower from the peaks seen in 2022.

{kind=link}

Not all central banks have tightened policy

There are a few notable exceptions though to global monetary tightening. Japan, which had long suffered from deflationary pressure, is now witnessing strong growth in prices relative to the past few decades. Yet, the Bank of Japan views current price pressures as transitory—unless there is evidence of sustainable wage growth—thereby not warranting any rate hikes.13 In China, a delayed reopening of the economy has kept inflation low till now; it was 0.2% in May.14 Instead, there is greater focus on stimulating credit growth and rebooting the economy. So, instead of any worries about inflation, the People’s Bank of China (PBOC) has loosened policy to boost liquidity in the banking system and lower cost of certain forms of credit.15 In Turkey, monetary policy started running counter to orthodox policies in 2021. Even as inflation was surging—it went up to as much as 85.5% by October 2022—and the lira was fast depreciating, the Central Bank of Turkey (CBT) resorted to easing monetary policy from mid-2021. With confidence in monetary policy fast declining and no end in sight to high inflation, the CBT has finally reversed policy—it hiked its key policy rate by 650 bps in June, although markets were expecting a steeper hike.16

Elevated core inflation is keeping some central banks worried

In the United States and Europe, labor markets are still strong despite strong monetary tightening. That is keeping wage growth high, thereby raising worries about the probability of a “wage-push” inflation. In the United Kingdom, average weekly wages went up by 7.3% year over year in the three months to May even as headline inflation averaged 8.7% over that period. Similarly, in the United States, jobs growth is still healthy at 278,000 on average per month this year with the unemployment rate low at 3.6%. This is potentially keeping consumer spending strong, adding to the upward pressure on prices. It is unlikely that without some softening in labor markets, demand growth—and hence inflation—will slow.

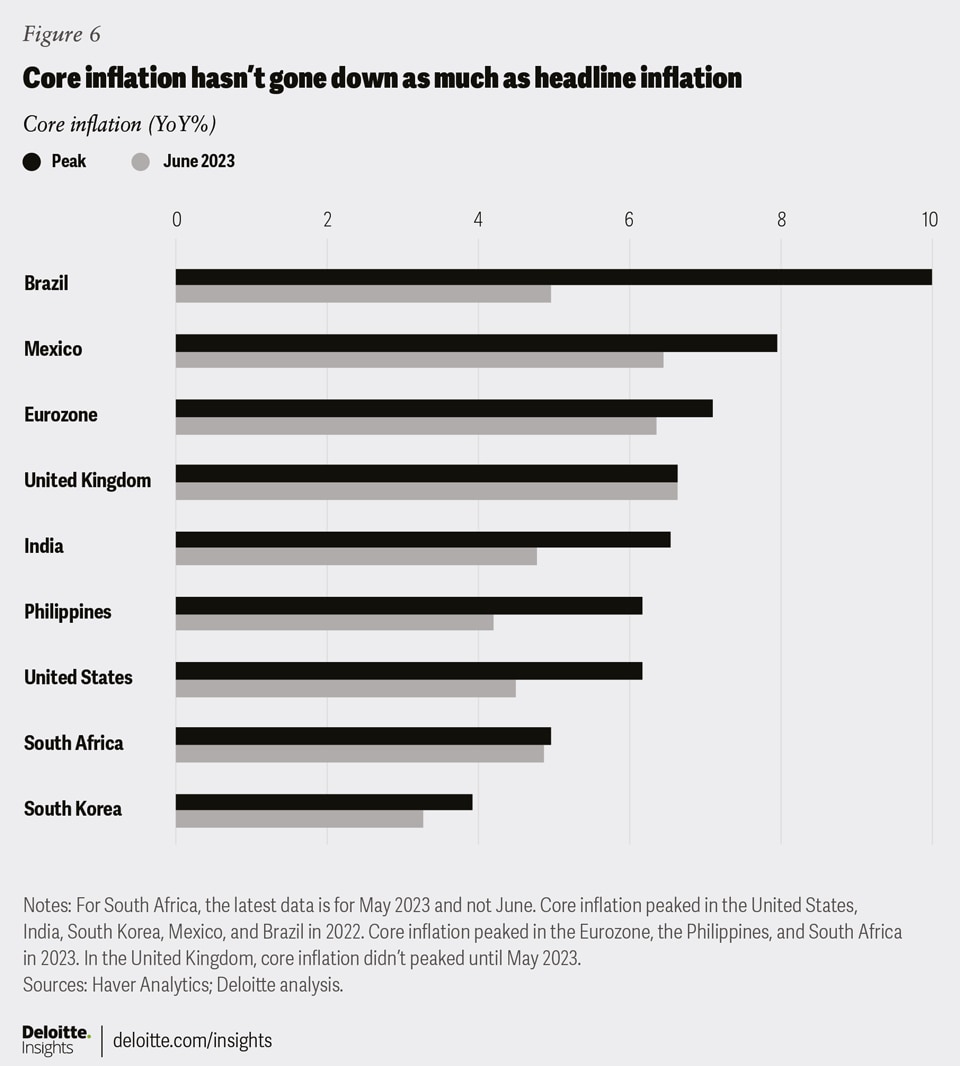

Second, consumer spending is shifting back to services from goods due to pent-up demand. Consequently, services inflation has gone up across major economies. In the Eurozone, inflation on recreation and personal care has steadily increased since mid-2021 to 7.7% in May. So, just as goods inflation eases in the region, services inflation has shot up. The trend is same in the United States where rising rent-related inflation is also pushing services inflation up. Services inflation, in turn, is keeping core inflation elevated (figure 6). In the United Kingdom, core inflation at 7.1% is now at its highest since 1992.17 Even in countries like India and Brazil where inflation has eased more compared to the West, core inflation hasn’t declined as much as headline inflation. Central banks are unlikely to breathe easy till core inflation is back to target levels.

{kind=link}

Finally, in emerging and developing economies, central banks are likely worried about external events as well. In India, headline inflation is now back to the Reserve Bank of India’s (RBI’s) 2–6% target range. While the RBI has paused its rate hikes, it is worried about the threat of El Nino on agricultural output this year and hence, food prices.18 Emerging and developing economies’ central banks will likely be wary that any further tightening in the West might create interest-rate differentials with their own economies. That may put lead to capital outflows—as has often happened19—resulting in depreciation of domestic currencies. A weaker currency leads to higher imported inflation and may require exchange-rate stabilization through central banks’ use of their foreign exchange reserves20 or in some cases, like Turkey, more rate hikes. Central banks in major food importing nations will also be hoping that the recent spike in wheat prices after Russia walked out of the Black Sea grain deal in July21 will be short-lived and won’t contribute to sharp increases in food inflation in the near- to medium-term.

Central banks will be wary of risks from rate hikes

Tightening monetary policy further is not without risks. Rising interest rates have dented mark-to-market values of assets in banks’ balance sheets, as happened in regional banks in the United States in the first half of this year. Things would have got worse had it not been for timely intervention by the authorities, thereby leading to a reversal of risk spreads. High mortgage rates have also weighed on the housing market and put more pressure on already-stretching household budgets. The BOE has predicted that nearly 2 million households will see monthly increase in mortgage payments worth GBP 200-499.22 There are other risks emerging, especially in commercial real estate as remote and hybrid work patterns lower demand for office spaces. Banking and financial services’ exposure to commercial real estate is, therefore, worrying.23

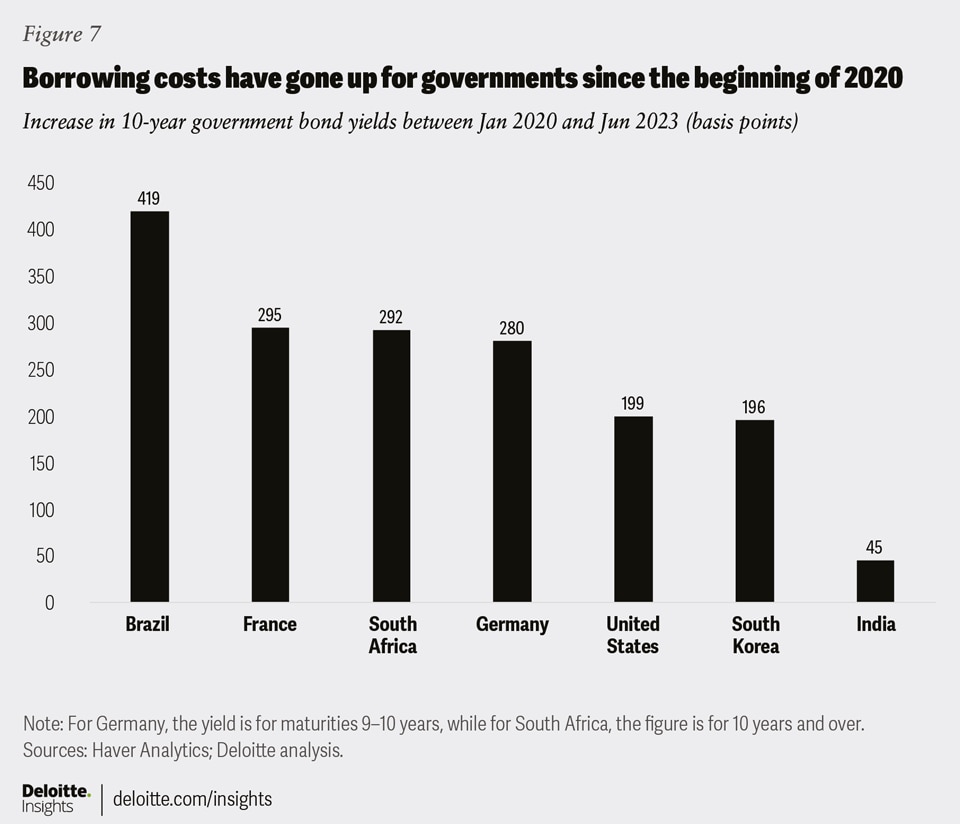

For governments, higher interest rates mean a rise in debt-servicing costs. Government debt soared during the pandemic due to revenue losses, public-health costs, and support for households and businesses. Estimates by the International Monetary Fund (IMF) suggest that general government debt in advanced economies in 2022 was about 8.5 percentage points higher than prepandemic levels.24 The debt-to-GDP ratio has also gone up sharply for emerging economies.25 While debt has gone up, so have interest rates (figure 7). In the United States, for example, the Congressional Budget Office estimates that the interest rate on the US public debt will rise to 2.9% in 2024 from 2.2% in 2022.26 Such rise in debt-servicing costs holds worries for long-term debt sustainability. This is more so for countries with high debt, low potential GDP growth, and structural deficiencies aggravated by COVID-19. In recent times, countries like Egypt and Pakistan had to tap international agencies for help while Sri Lanka was faced with no option but to default on its debt.27

{kind=link}

Rate cuts are unlikely in the United States and Europe this year

The stubbornness in core inflation, strong consumer spending on services, and tight labor markets mean that it’s too soon for central banks in the West to declare victory over inflation. While the Fed’s July hike may well be its last for now—unless inflation reverses its downward course28—it is unlikely that any monetary easing will happen this year.29 The economy too has held up well despite strong interest-rate hikes, thereby blunting any immediate requirement for rate cuts. Deloitte economists, in their baseline scenario (60% probability), expect the economy to avoid a recession in 2023–2024.30 GDP growth, however, is expected to slow to 1.4% this year and 1.3% in 2024 from 2.1% in 2022. In such a scenario, any easing is unlikely till the second half of 2024.

In the United Kingdom, both the BOE and the government acknowledge the risks of a wage-price spiral with core inflation (at 7.1% in May) at its highest level since 199231 and wages still rising. No wonder then, that, in June, the BOE raised its policy rate by 50 bps—higher than what financial markets were expecting32—and then followed it up with another hike of 25 bps in August.33 The BOE is not expected to pause without a tangible shift in wage and consumer price growth. In the Eurozone, too, more rate hikes are likely on their way as the European Central Bank (ECB) staff now expect core inflation to be higher this year and in 2024 due to a tight labor market.34 In July, the ECB hiked its refinancing rate again by 25 bps to 4.25% and they have kept open the possibility of further hikes this year should core inflation continue to remain elevated.35

Monetary policy easing may come sooner in emerging economies

For key emerging economies where inflation has dropped faster than advanced economies, a wait-and-watch approach has helped so far. Central banks have preferred to see the impact of previous rate hikes on core inflation as monetary policy works with a lag of six to nine months. This has also allowed them to gauge how the policy cycle evolves in the West, especially in the United States. This stance, however, may change in the coming months.

In Brazil, inflation fell again in June to 3.2%—the lowest since September 2020—with core inflation also declining during the month to 5.3%. Declining inflation had already set the stage for a policy-rate cut this year unless the current disinflationary process in the country reverses due to either internal or external shocks.36 And that’s exactly what happened in August when the Banco Central do Brasil (BCB) cut its key policy rate by 50 bps.37 In Asia, inflation has eased in Indonesia and India. In June, core inflation in Indonesia fell again to 2.6% in Indonesia, while headline inflation declined to 3.5%, both core and headline inflation are now within the Bank of Indonesia (BOI’s) target range of 2–4%. It is likely that in the absence of any dent to its currency (unlike last year), the BOI may cut rates by Q4 2023 to boost economic growth. In India, too, if seasonal agricultural factors do not impact inflation and the Fed’s tightening cycle stops, some easing is likely later this year. While in China, with the PBOC expecting inflation to stay low or even decline in the near term,38 monetary policy will remain engaged on growth. The only major exception to these trends could be Turkey where the CBT has still a long way to go to curtail inflation, bolster the lira, and regain market confidence.39