{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Foreign reserves to the rescue for Asian currencies has been saved

Cover image by: Meena Sonar

A key learning from the Asian Financial Crisis of 1997 was the need to build a war chest of foreign reserves that can be deployed in times of sharp capital outflows to defend domestic currencies.1 Ever since, many Asian economies have built up foreign reserves and deployed them effectively at times of economic volatility.2 Be it the global financial crisis of 2007–2008, the “taper tantrum” of 2013,3 or COVID-19 in 2020, Asian central banks have found these reserves handy to tide over currency fluctuations and shore up confidence in their countries’ external balances.

This year, as central banks in the West tighten monetary policy at a pace unheard of in the past three decades, Asia’s policymakers are once again turning to their reserves amid sharp capital outflows.4 Yet the use of reserves is more a short-term intervention and not something that can be used extensively over a long time. Prudence therefore may be necessary, given that global economic uncertainty amid surging inflation, rising cost of borrowing, and an armed conflict raging at the edge of Europe.

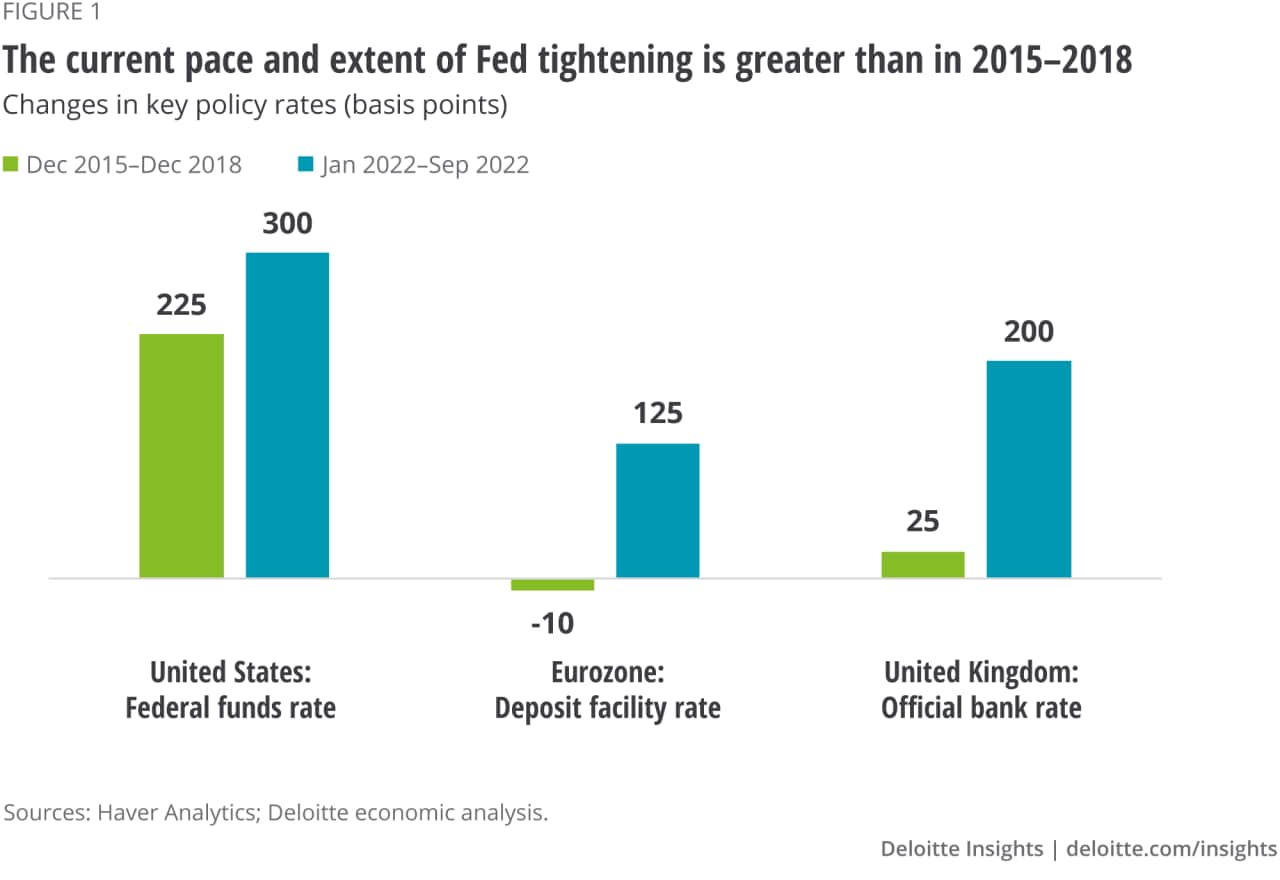

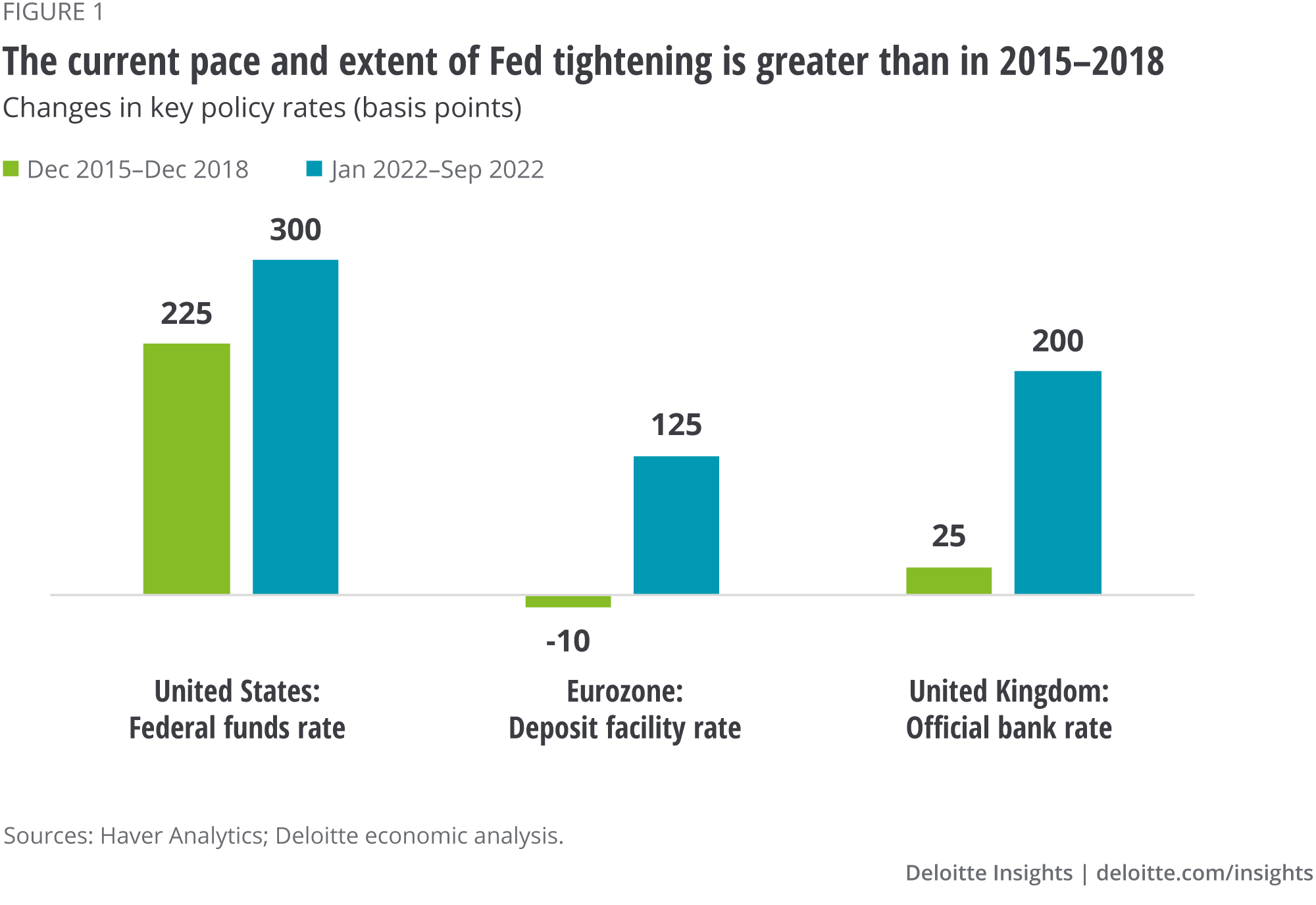

The speed and scale of interest-rate hikes by central banks in the West are something new for Asian economies. During its previous period of monetary tightening, from December 2015 to December 2018, the United States Federal Reserve (Fed) raised interest rates by 225 basis points (bps). In contrast, since January 2022—in seven months alone—the Fed has hiked interest rates by 300 bps. Moreover, while previous hikes took place in increments of 25 bps, in 2022, there were three hikes of 75 bps each and one of 50 bps. And that’s not the end of it. Going by the latest minutes from the Federal Open Market Committee, more hikes are on their way, especially as inflation remains high and core inflation remains much above the Fed’s 2% target.5 The Fed is not alone in raising rates aggressively. In Europe, both the European Central Bank and the Bank of England have tightened policy sharply this year compared to the prepandemic period (figure 1).

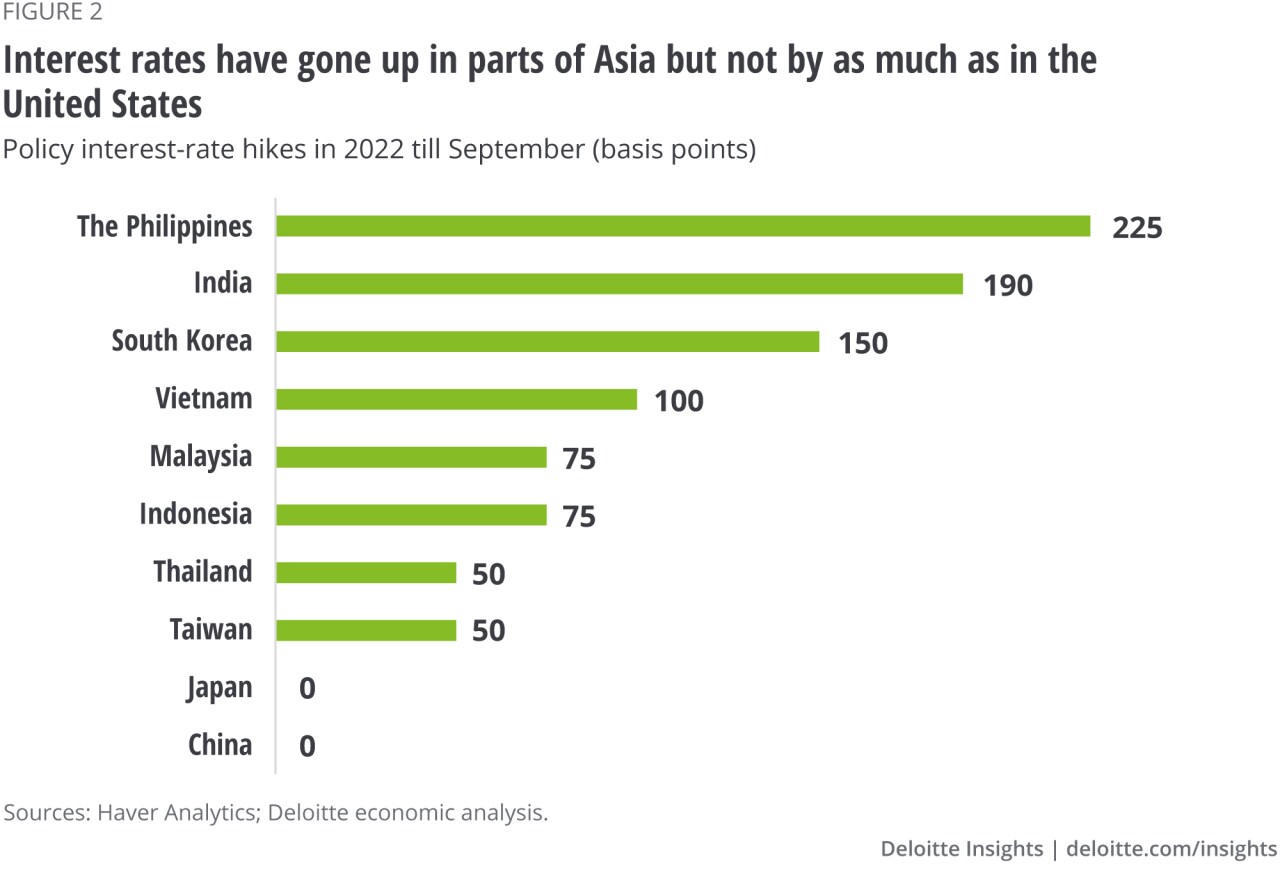

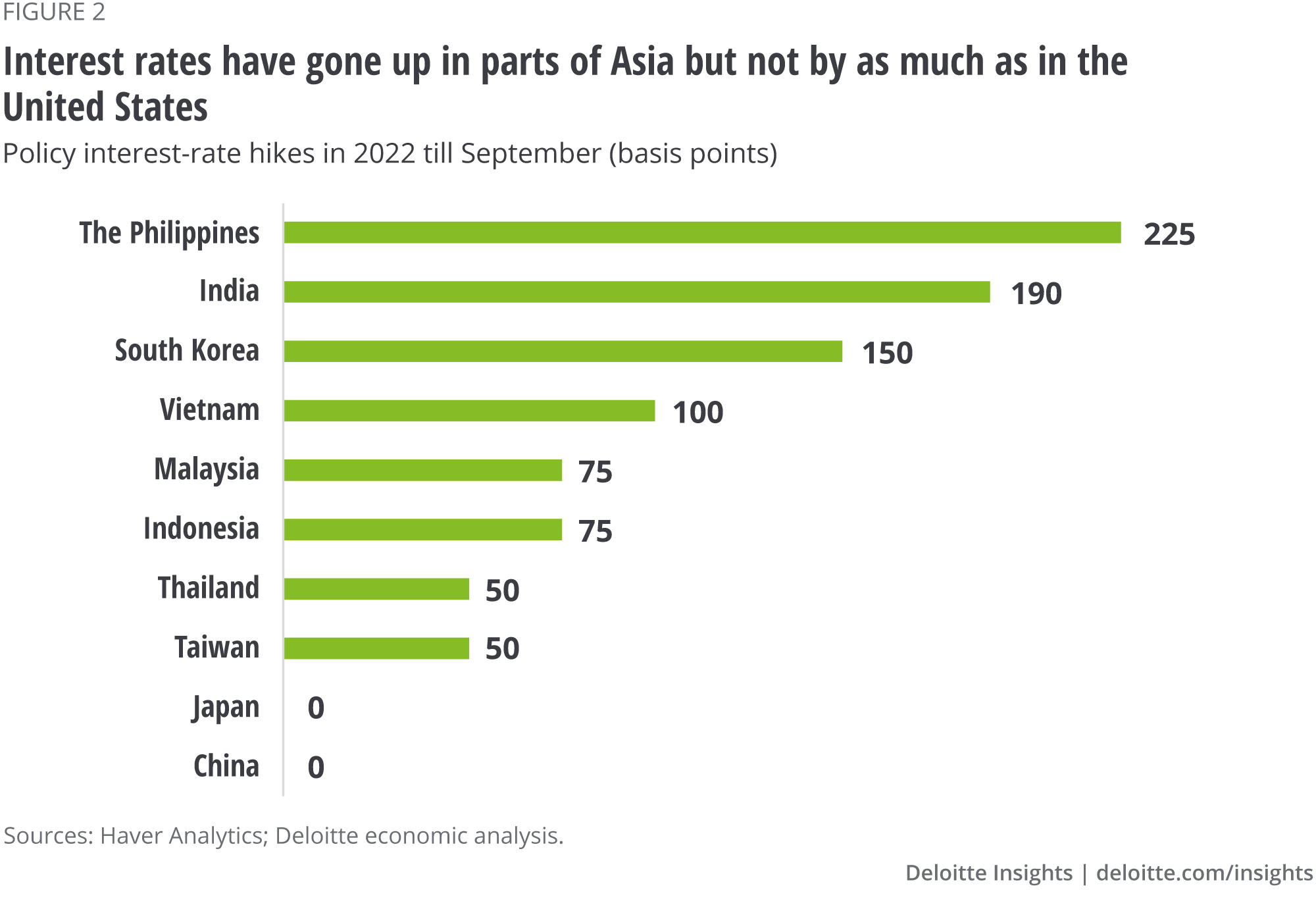

The pace of rate hikes in the West has meant that their interest-rate differentials with key Asian economies has gone up. This is despite monetary tightening in many Asian economies to thwart rising domestic inflation. A quick comparison between figures 1 and 2 shows that the rise in policy interest rates, if any, in key Asian economies has been lower than corresponding hikes by the Fed this year. Among major economic hubs in Asia, only Singapore has hiked rates by more than the Fed, reflecting the Monetary Authority of Singapore’s focused efforts to thwart inflation and retain confidence in one of the world’s leading trade and investment hubs.6

As the West’s interest-rate differentials with Asia go up and global economic uncertainty rises due to the war in Ukraine and fears of a global economic slowdown, foreign portfolio investments (FPIs) into Asia, especially to emerging economies, have either been slowing or reversing since early 2022. Figure 3 shows the dip in net inflows (or net liabilities) in portfolio accounts of the balance of payments of key economies in Asia between Q4 2021 and Q2 2022; the dip is the strongest in the first and second quarters of this year in China and India. According to the Institute of International Finance (IIF), in the five months leading up to July 2022, FPIs have started to flow out of emerging economies, recording a net decline.7 These investments are unlikely to be replaced anytime soon: The IIF predicts a 42% decrease in portfolio inflows to emerging economies for the year.8

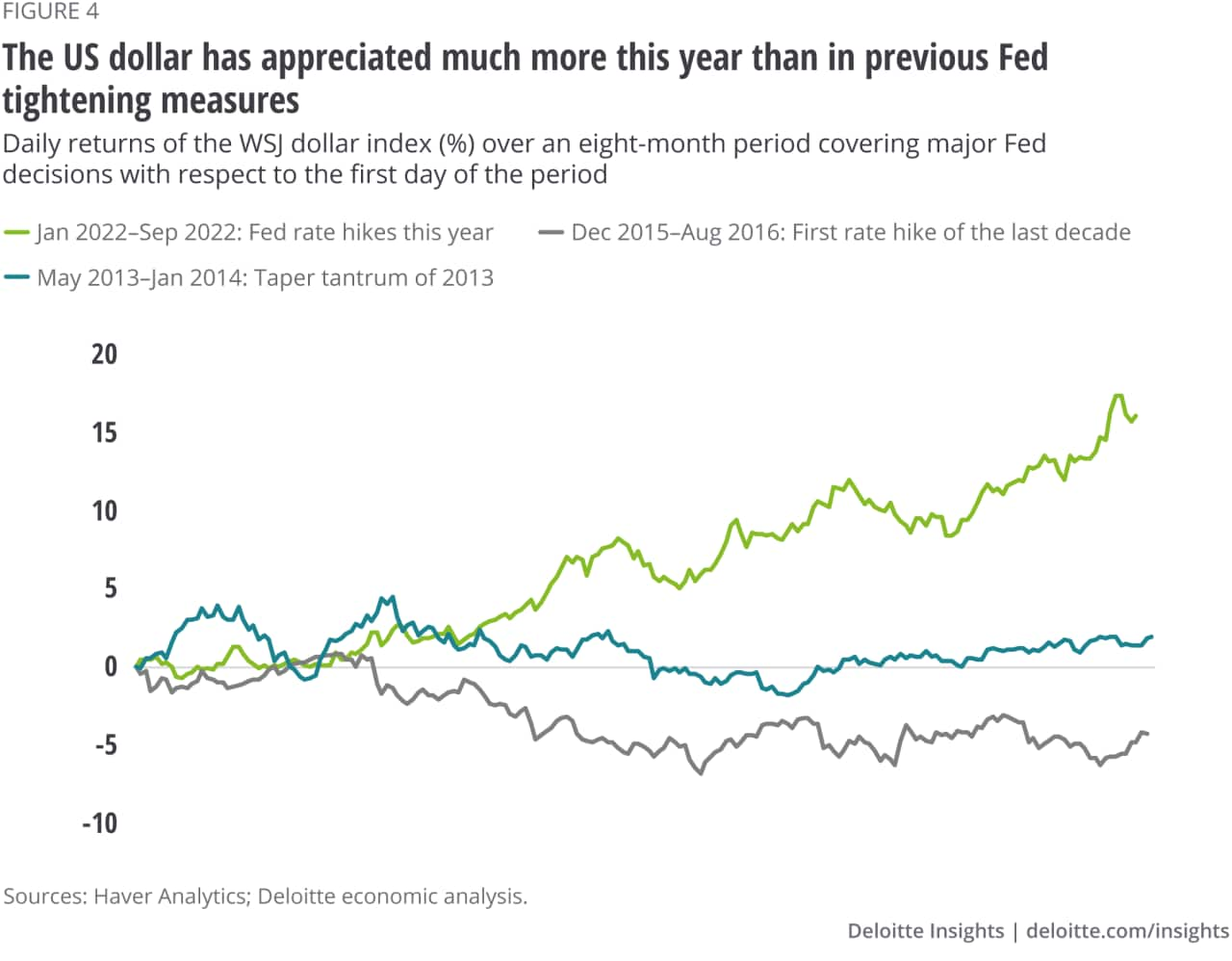

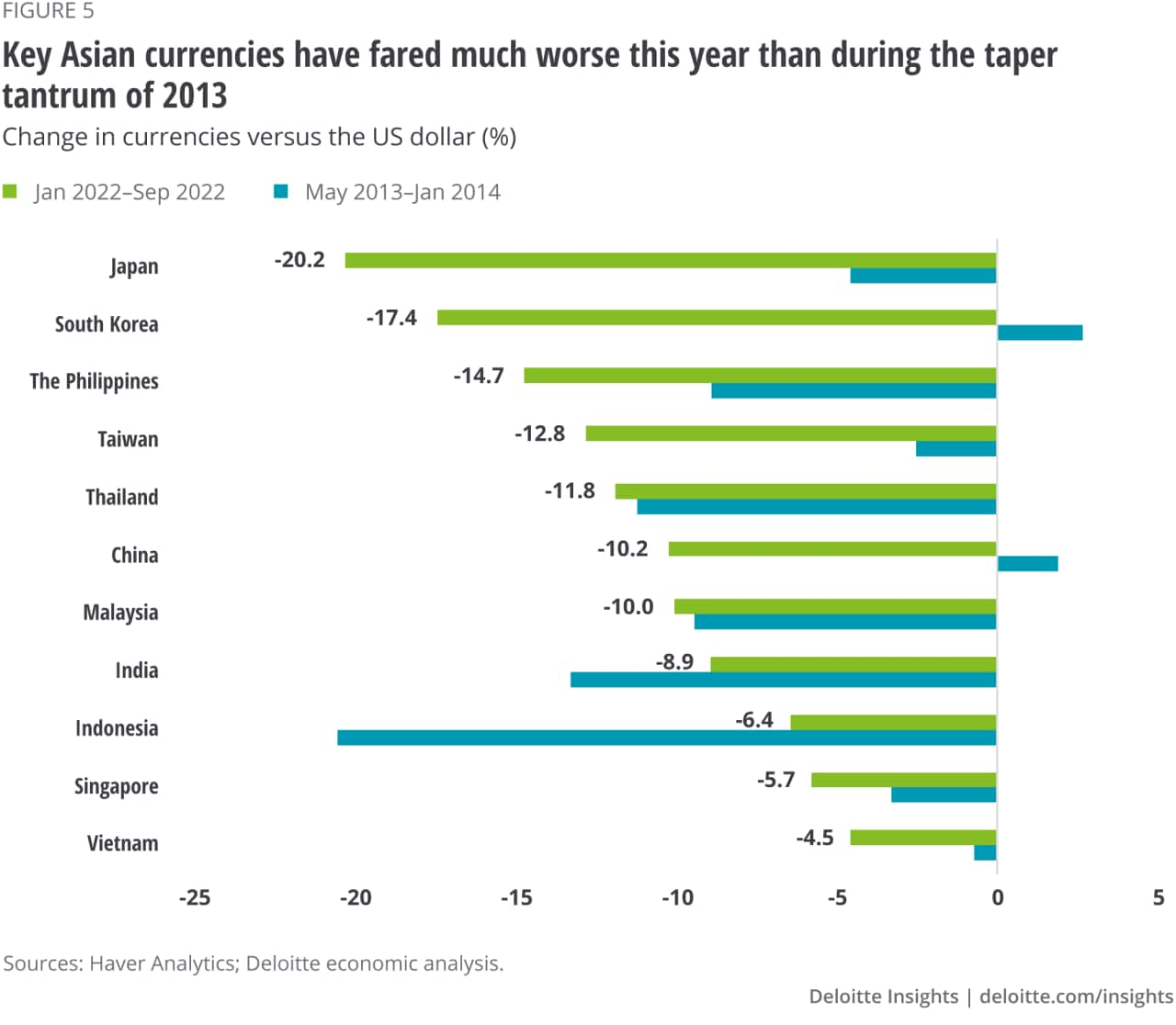

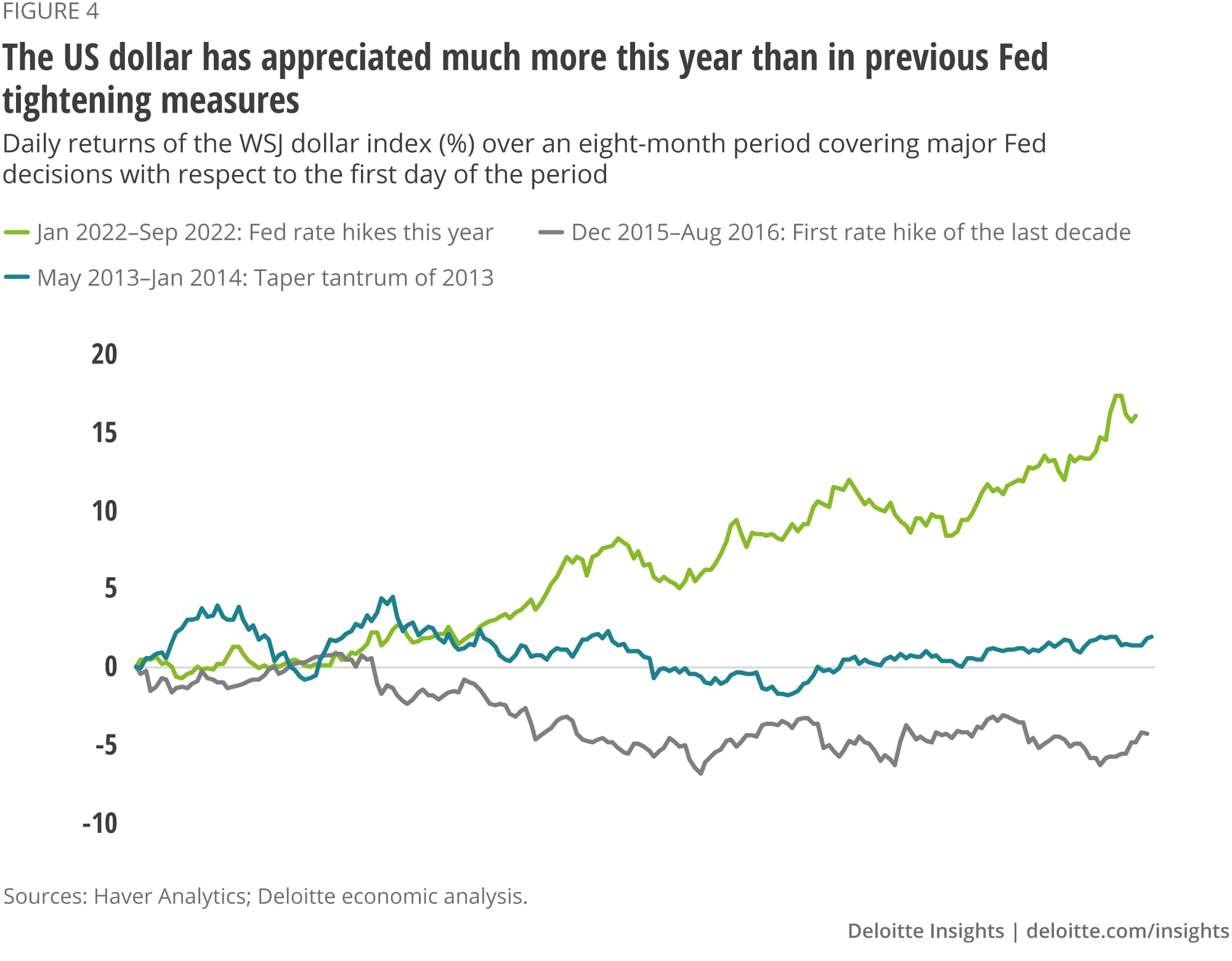

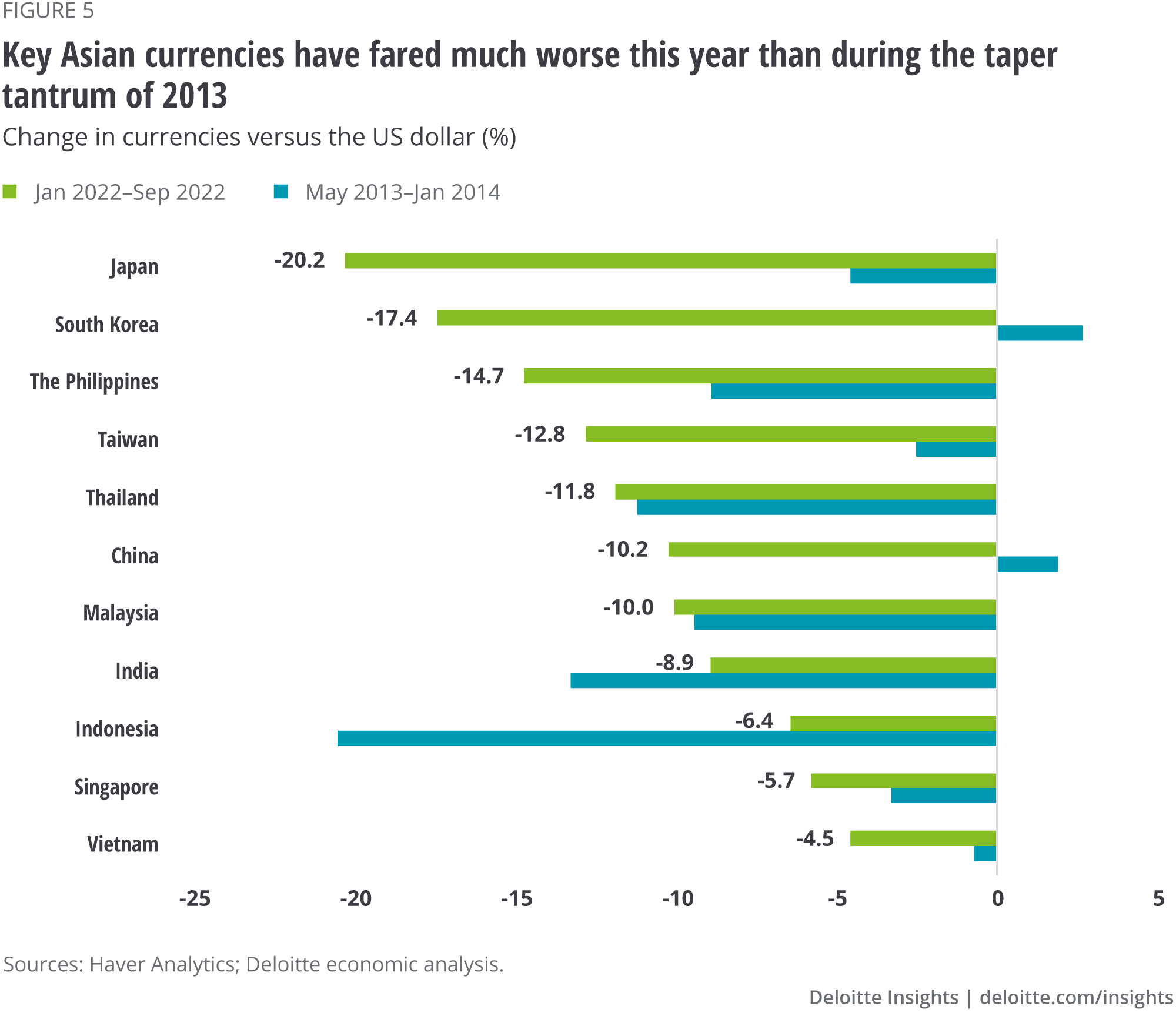

The mix of portfolio outflows from Asia and high interest rates in the United States has meant that the US dollar has enjoyed a strong burst of appreciation. By the end of September this year, the WSJ dollar index9 was up by 16.1%, much higher than prior periods of Fed action since 2010. In terms of the degree of appreciation, only the taper tantrum of 2013 compares to the bout of dollar surge this year (figure 4). But even during the taper tantrum, the surge in the value of the dollar faded after four months, whereas this year, it shows no sign of declining. No wonder then, that, Asian currencies have suffered, as figure 5 shows. It’s not just emerging economies in the region that are bearing the brunt. The Japanese yen and the South Korean won have fared worse than key emerging economy currencies. By the end of September, the yen was down 20.2% against the US dollar compared to December 2021, while the won had fallen by about 17.4% during this period. Figure 5 also reveals that most major Asian currencies are faring much worse this year than during the taper tantrum of 2013.

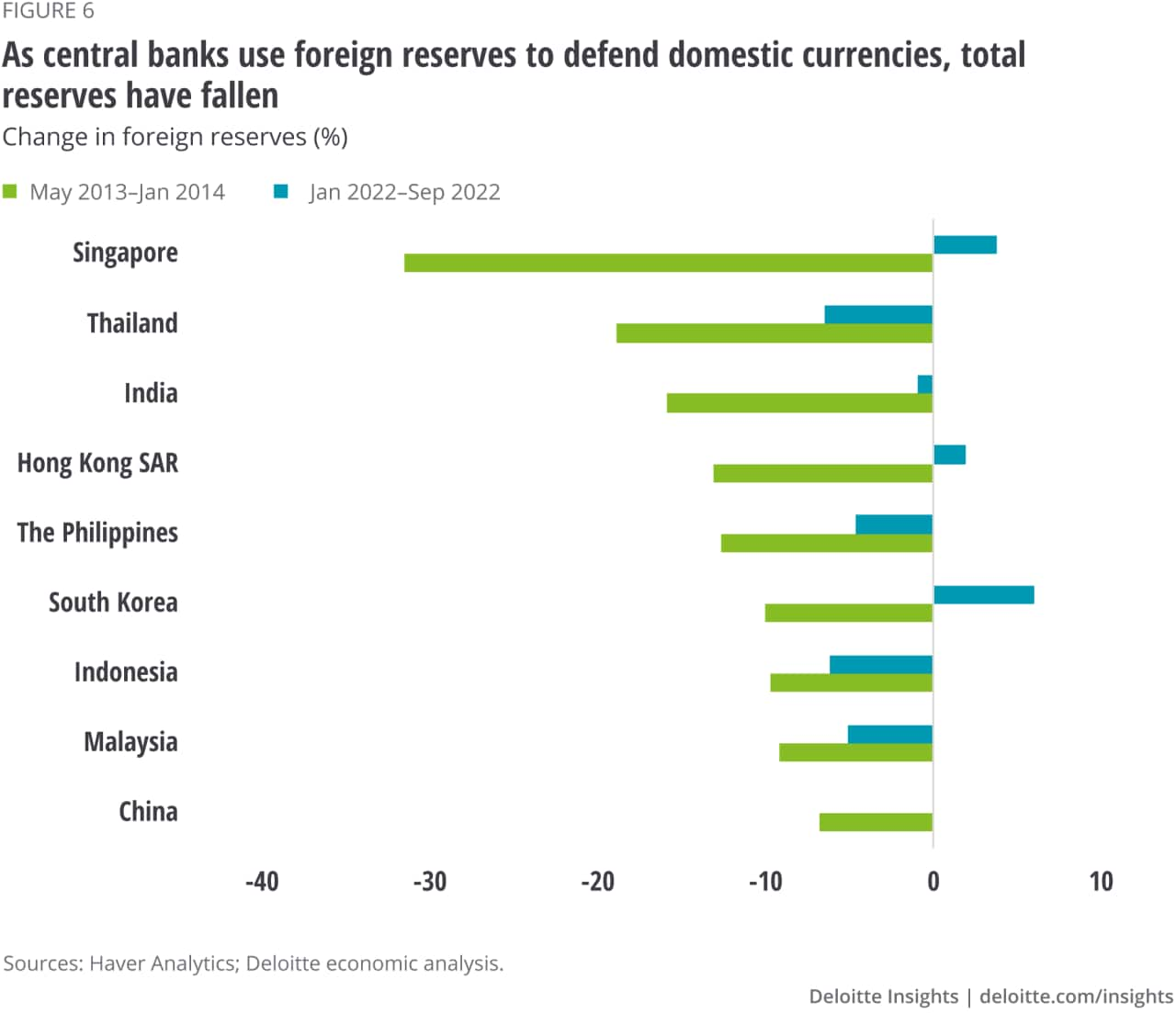

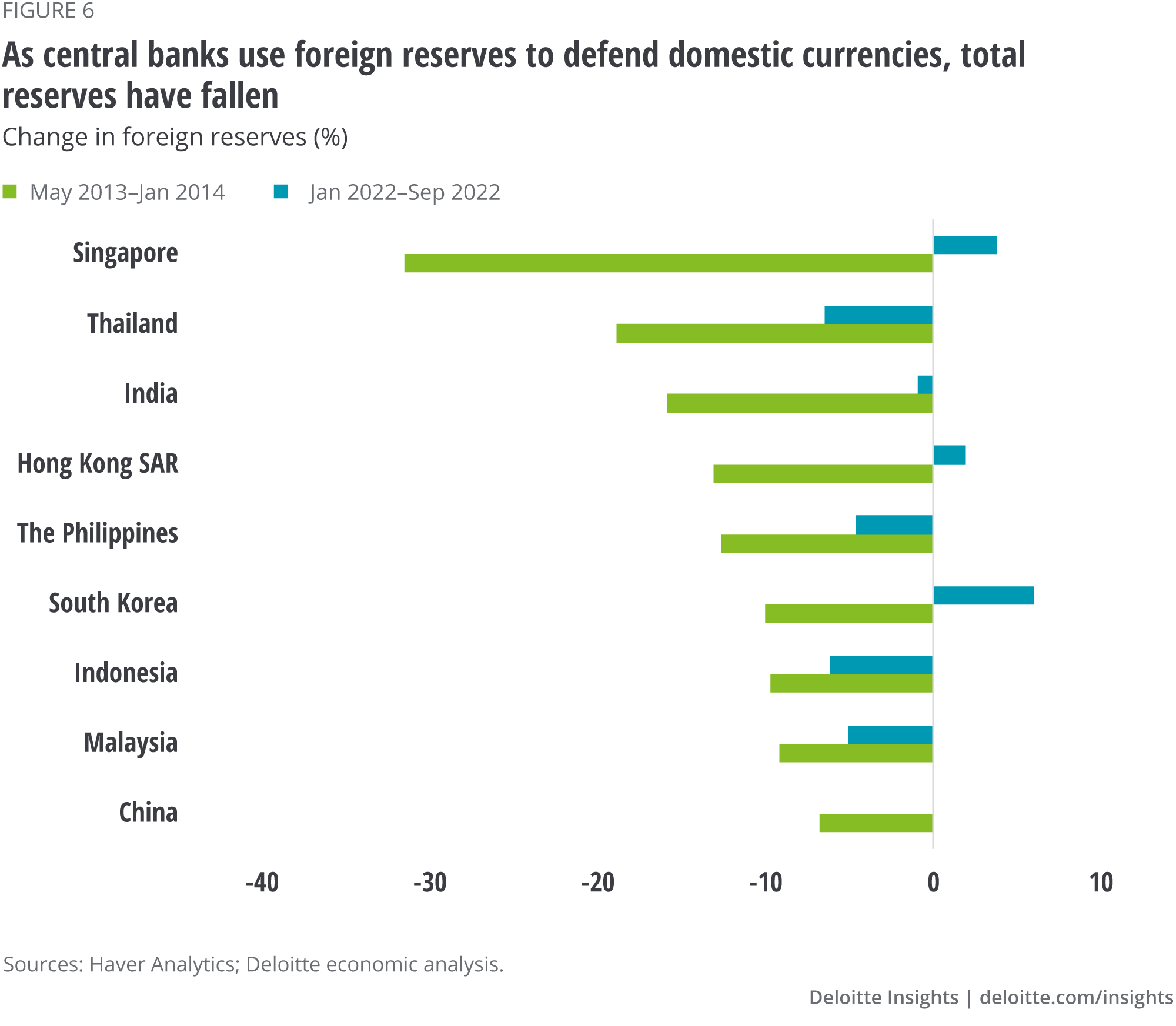

Asian currencies would have fared worse had reserves not turned up for defense. In India, for example, foreign reserves have fallen by more than US$100 billion or 15.9% since December 2021 till September this year as the Reserve Bank of India (RBI) has tried to defend the Indian rupee.10 Indeed, if not for such intervention, the rupee’s depreciation would have been higher than the 8.9% decline till September this year compared to the end of 2021. India is not alone in the region to deploy reserves to bolster domestic currencies. Figure 6 shows the decline in reserves for major economies in Asia since December 2021 as countries use their reserves to shore up weakening currencies against a rampant dollar. It is, however, important to note that not all this decline in reserves is due to its use in defending currencies; part of the dip in the dollar value of reserves is also due to the decline in the value of other currencies like the euro and the pound that make up total foreign reserves of countries.

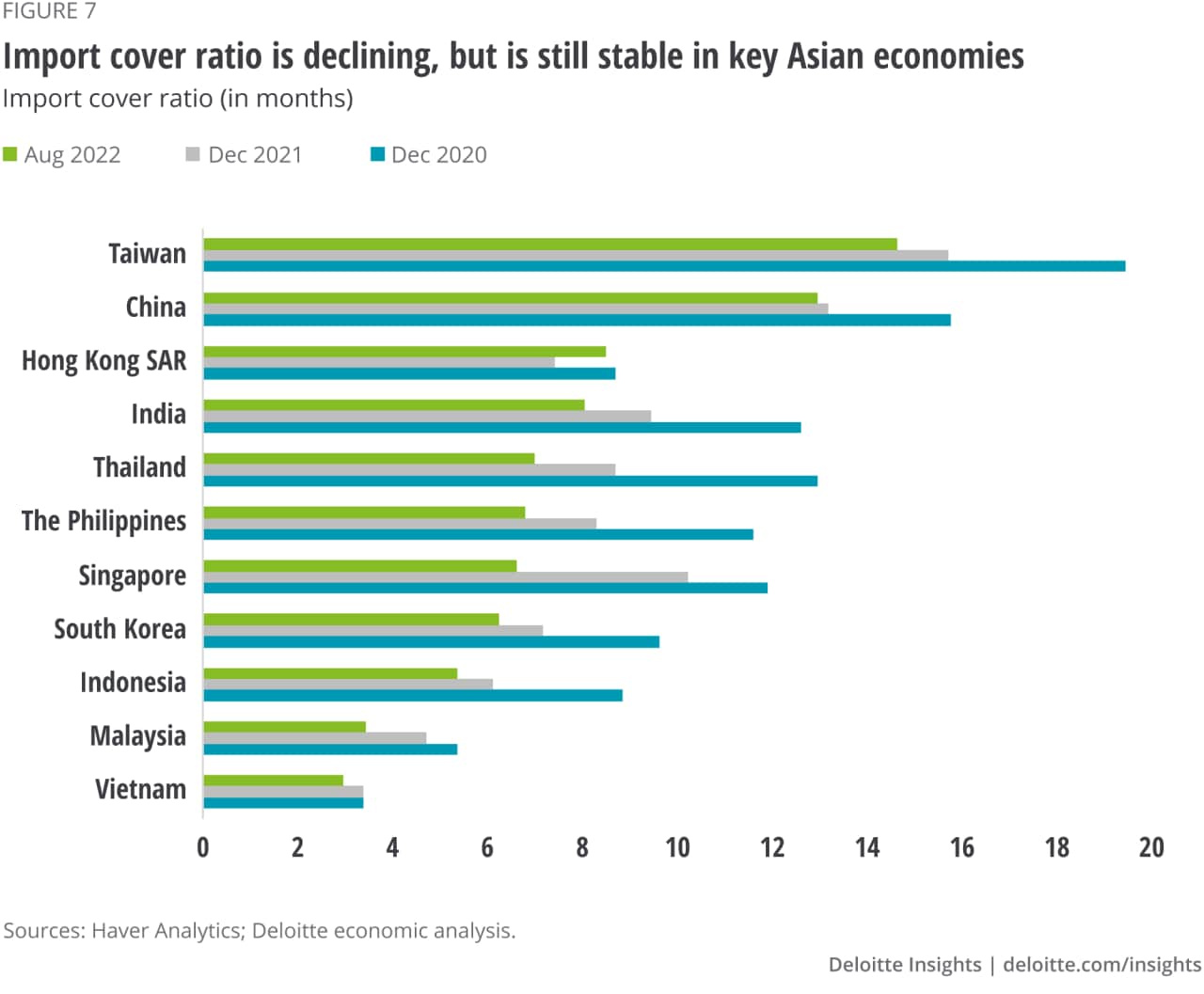

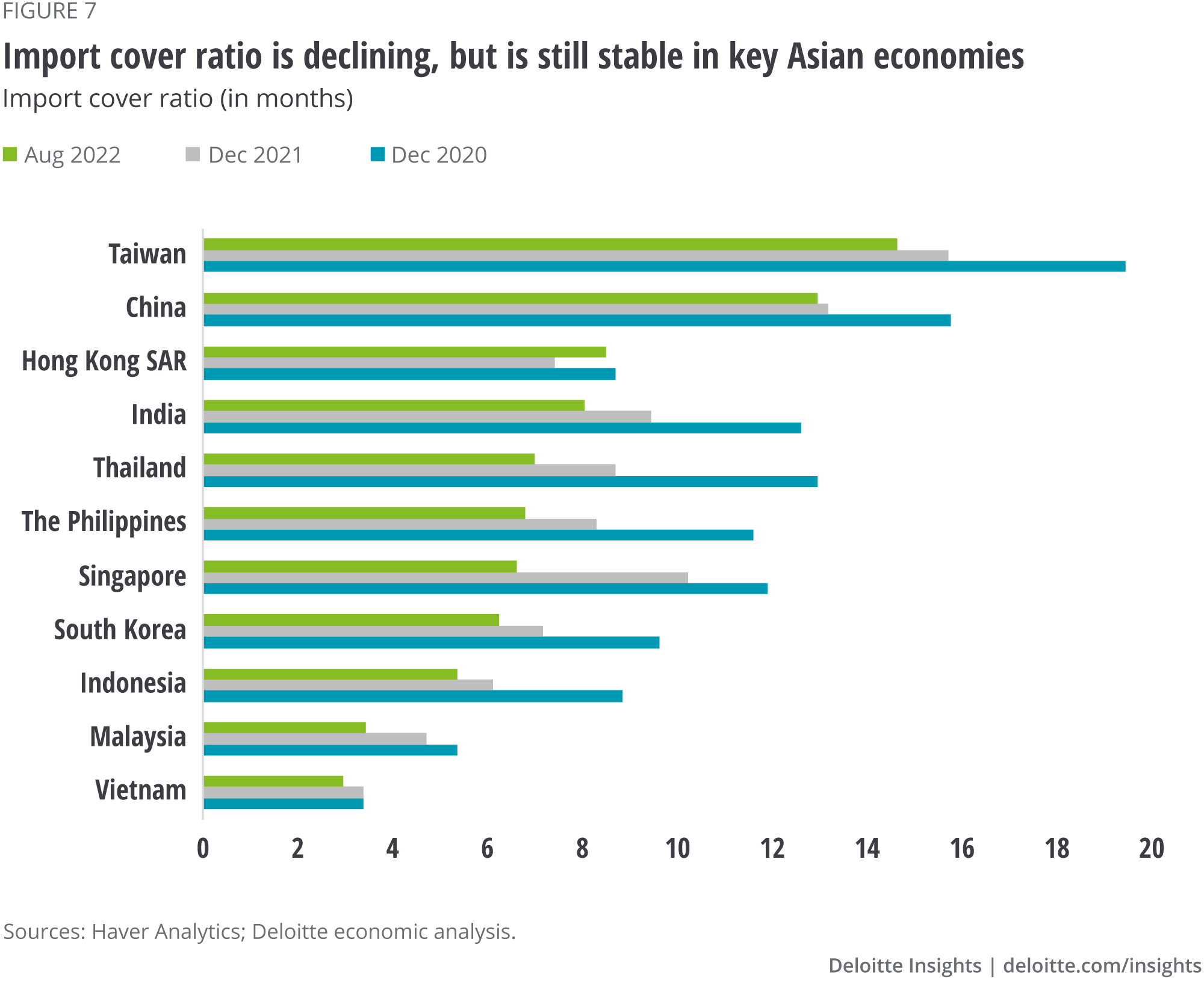

Using up reserves quickly can, however, decrease a country’s import cover—defined as the number of months of imports a country can pay for using existing foreign reserves (figure 7). Import cover is a key measure of a country’s ability to survive a sudden decline in foreign inflows, export earnings, or worse, a financial crisis. The decline in import cover is especially worrisome for countries suffering from stress in fiscal finances and large external balances; high global commodity prices will only make things worse for net commodity importers. Sri Lanka’s example this year is a cautionary tale for many. In July 2022, the country didn’t have enough foreign exchange to pay for imports and service its external debt. With inflation soaring, fuel shortages rampant, and the value of its currency plummeting, the country finally defaulted on its external debt for the first time in its history.11

What about other Asian economies? Do they need to worry? Thankfully, for now, key economies can afford to keep using reserves in the near term to bolster currencies as they have sufficient reserves at hand. Thailand, for example, may have used up 17.9% of its reserves but still has seven months of import cover. India, which has used reserves to stabilize the rupee, still has US$532 billion worth of reserves to deploy. Moreover, not all countries are using up reserves at a fast pace. The Bank of Japan, for example, has used reserves selectivity to stabilize the yen even as it keeps monetary policy loose.12 And as figure 7 shows, import cover may have declined for key economies in Asia but continue to remain healthy.

Nevertheless, extensive use of reserves over the long term may not be effective as reserves are more of a rainy-day fund. Getting inflation back in control, reigning in fiscal deficits, and enhancing competitiveness to push up potential economic growth will likely do more to bolster global investors’ confidence over the long term. After all, that’s how Asia has emerged stronger from periods of crisis in the previous century.

John Reed, Andy Lin, and Chloe Cornish, “India’s foreign reserves dwindle but currency defense still strong,” Financial Times, October 5, 2022.

View in ArticleCover image by: Meena Sonar