Russia’s invasion of Ukraine is causing significant global economic disruption, adding further stress to a global economy that continues to struggle with the legacies of the COVID-19 pandemic and the supply chain problems and inflation it has provoked.

The International Monetary Fund said this autumn that one-third of the world economy would probably contract this year or the next as prices rise and real incomes shrink.1 That challenging outlook is reflected in the responses in Deloitte’s European CFO Survey for Autumn 2022.

Since 2015, the survey has given voice twice a year to approximately 1,500 CFOs from across Europe. This article provides an overview of current economic trends, CFOs’ hiring and investment intentions, their views on business transformation as well as critical business risks and strategic priorities and the factors they currently consider vital to success.

We also ask CFOs for their expectations about medium-term prospects. In addition, each survey contains a specific set of questions about current business issues.

This edition focuses on inflation and specifically CFOs’ opinions on the prospects for the annual inflation rate in their country and the strategies they are undertaking to mitigate the impact of high inflation.

The responses provided reflect record levels of business uncertainty – the most extreme since the survey's inception. There are, however, some bright spots amid the gloom. European CFOs are still optimistic about their revenues and intend to keep hiring, and they expect average inflation will drop to a somewhat more manageable level of 6.10 per cent in the euro area and 4.11 per cent in the non-euro area towards the end of 2023.

Although it makes for sobering reading, we hope the views set out in this article will nourish your thinking and help provide a good basis for your business plans. Please contact one of our Deloitte leaders to discuss any aspects of our findings.

Executive summary

- The Deloitte European Chief Financial Officers (CFOs) Survey for Autumn 2022 reveals that CFOs see the impacts of the invasion of Ukraine as going from bad to worse. Russia’s invasion in February has caused enormous difficulties for businesses and economies around the globe, with severe disruption to energy availability, especially for natural gas, surging energy prices and persistently high consumer price inflation.

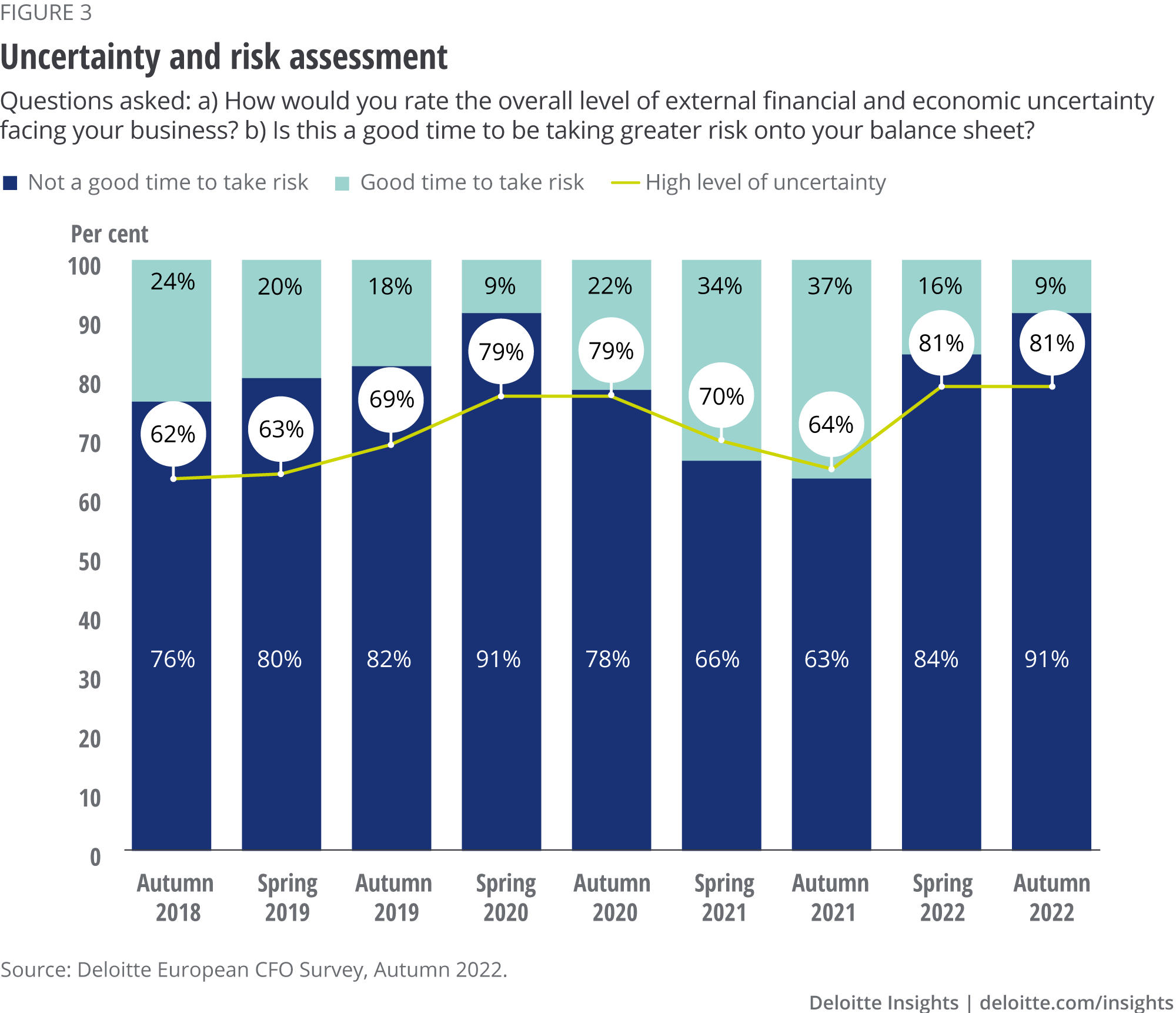

- The level of financial and economic uncertainty recorded by the European CFO Survey reached an all-time high in spring 2022, immediately after the Russian invasion of Ukraine. This survey sets a new record.

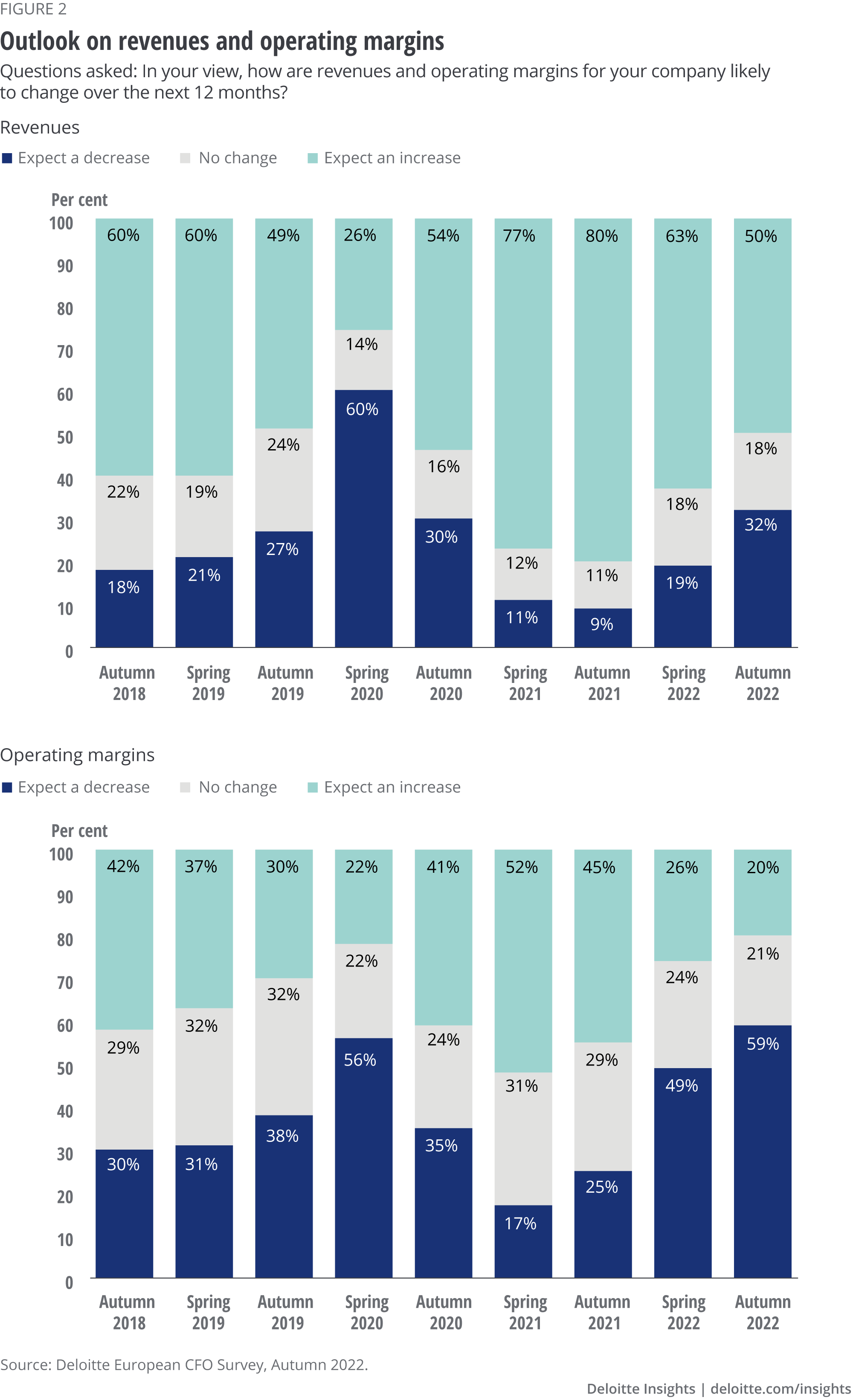

- CFOs are very pessimistic about the financial prospects for their companies and sectors, and particularly for operating margins and capital expenditures (CAPEX). However, CFOs are more optimistic about revenues and their hiring intentions, although they continue to experience unusual difficulty finding employees with the skills they need.

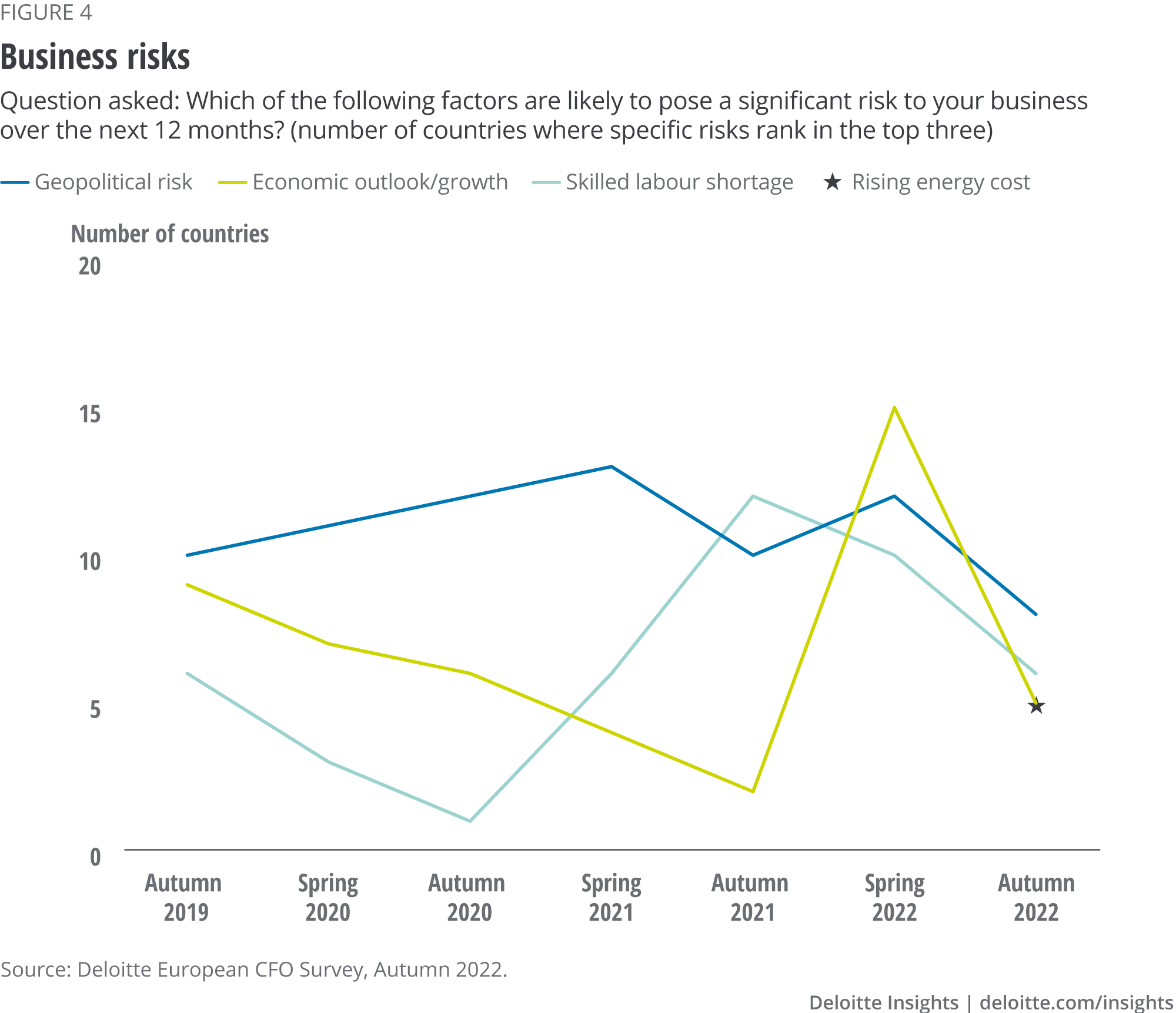

- European CFOs identify weak economic growth, a shortage of skilled labour and rising energy costs as the three factors likely to hold the most significant risk for their businesses over the next year. Also, economic and geopolitical uncertainty, coupled with high and still rising interest rates, has led to a sharp pullback in risk-taking by European CFOs across all sectors.

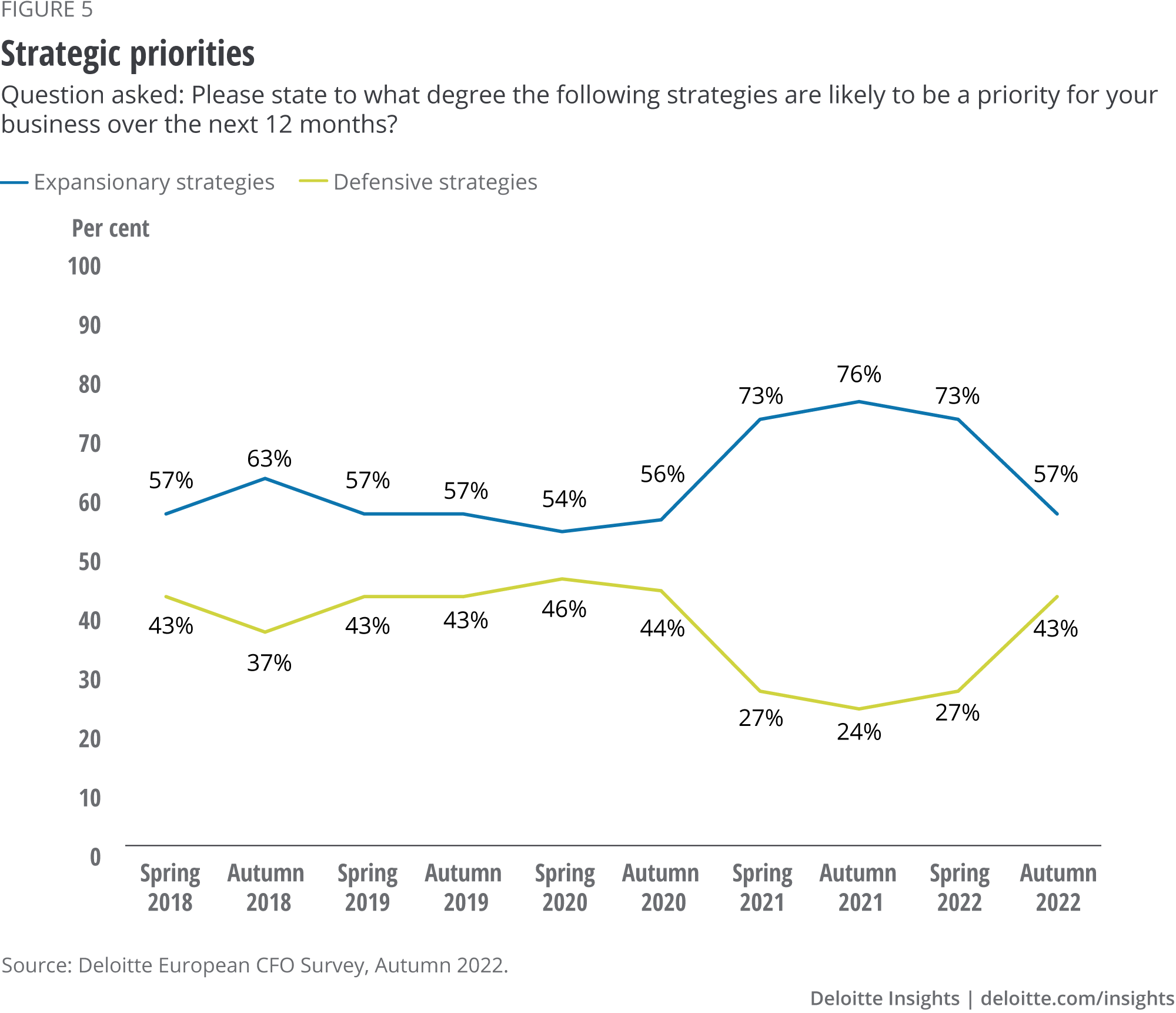

- European CFOs are growing more defensive as they seek to steer their businesses through the harsh economic environment. In particular, they are prioritising cost reduction as the number one strategy for the next year.

- Inflation is running at levels not seen since the 1980s, but European CFOs expect that the average inflation rate will ease to around 6.10 per cent in the euro area and 4.11 per cent in the non-euro area by the end of 2023. Companies are seeking to cushion the impact of inflation by passing on the costs to customers. CFOs in some countries are also prioritising the improvement of cash flow management and greater energy efficiency or focusing on higher-margin markets, products and services.

Financial outlook becomes even grimmer

CFOs have become more pessimistic about the financial prospects for their companies and sectors as high inflation, lower growth and tight monetary policy make themselves felt.

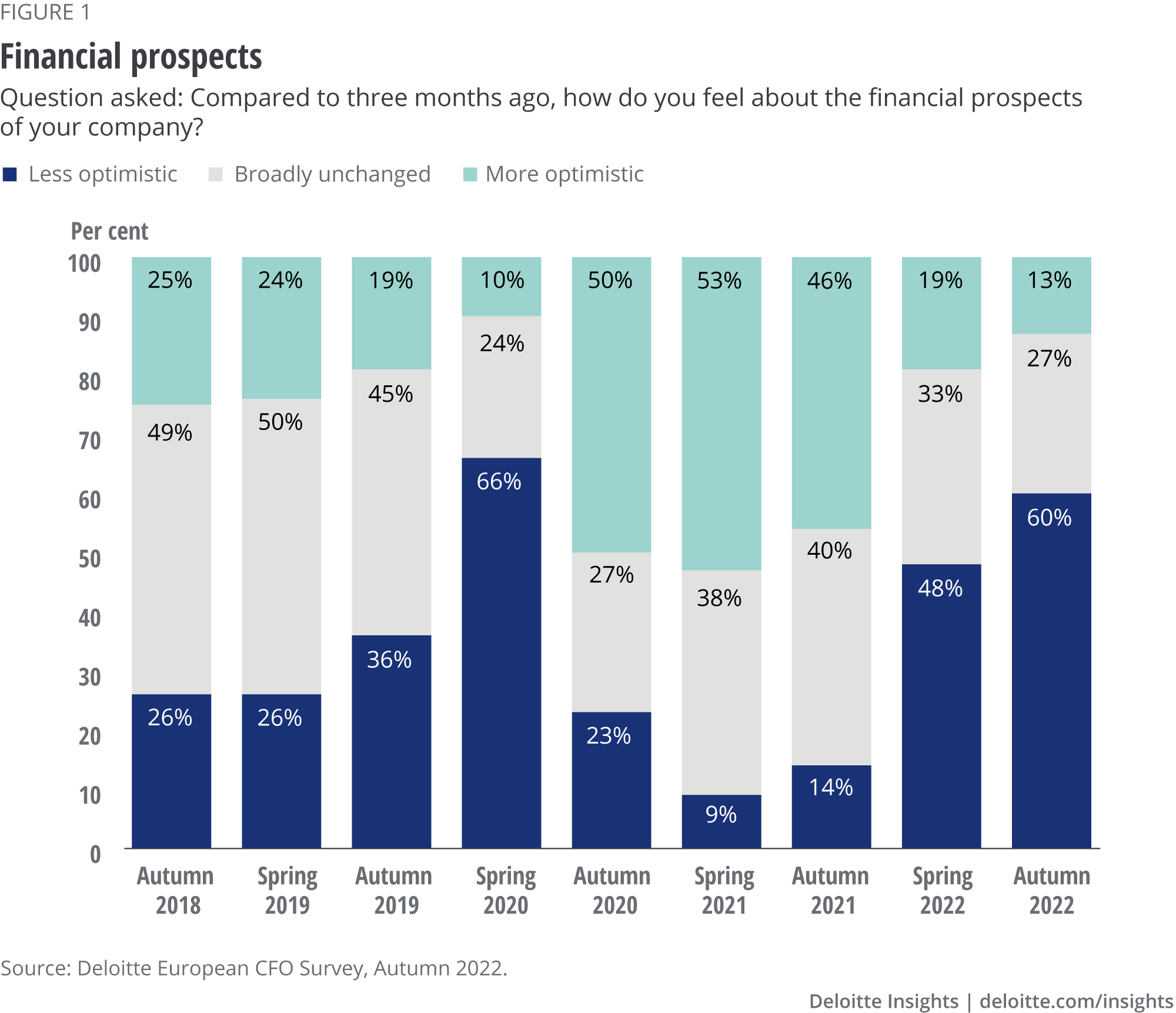

The mood among European CFOs became grim immediately after the Russian invasion of Ukraine in February 2022 but has plummeted even further as the conflict has dragged on. More than half (60 per cent) of the CFOs say they are less optimistic about their company's financial prospects in the next 12 months. Only 13 per cent describe themselves as optimistic.

Overall, the net balance for financial prospects declined from –29 per cent in the spring of 2022 to –47per cent in the autumn of 2022, almost reaching the depths observed during the early months of COVID-19 lockdowns.

The steep decline can be attributed to the severe disruption caused by the war in Ukraine, which has dimmed the prospects for a post-pandemic economic recovery.

The global economy continues to be weakened by the war through trade disruptions, pressure on food commodity prices and energy price shocks, all of which contribute to rising inflation. In addition, rapid monetary tightening by central banks in response to the high inflation is making the outlook for the European economy still worse.

The same sentiments prevail in the euro area and outside it. In the euro area, CFOs in Germany (72 per cent) and Spain (70 per cent) are the most pessimistic about their financial prospects. In non-euro countries, CFOs from Norway (60 per cent) and the UK (57 per cent) are the most pessimistic.

The sector results reflect the tone of the survey overall and continue the trends noted in the spring of 2022. All sectors have become less optimistic about their financial prospects. CFOs in life sciences are the most pessimistic, with the proportion of CFOs in this sector saying they are less optimistic doubling from 37 per cent in the spring of 2022 to 77 per cent in the autumn of 2022.

CFOs in the automotive sector, still reeling from the semiconductor chip shortage and other supply chain issues, report the lowest business confidence. Nearly two-thirds of the sector are less optimistic. Not one CFO in this sector said they are optimistic about the financial outlook.

By contrast, almost a quarter (24 per cent) of CFOs in the tourism and travel sector say they are more optimistic about their financial prospects in the next 12 months as they are expecting a promising tourism season ahead.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}