{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Does monetary tightening in advanced economies spell trouble for emerging markets? has been saved

Cover image by: Jaime Austin

Interest rates in advanced economies are rising sharply as central banks fight higher inflation rates than they’ve seen in decades.1 On September 21, 2022, the US Federal Reserve (Fed) raised its key policy rate for the fifth time in the year.2 The European Central Bank (ECB) has raised its deposit facility rate by a total of 125 basis points (bps) in 2022, after keeping it below zero for nearly eight years. And the Bank of England is pursuing aggressive monetary tightening as well, with more hikes likely over the near term.

Emerging economies too are battling inflation with interest rate hikes of their own.3 But unlike their counterparts in advanced economies, many have an additional worry: Many foreign investors are withdrawing capital from emerging economies to invest it in higher-yield holdings closer to home. An acceleration in these capital outflows could spell trouble for affected countries, potentially leading to greater sovereign risks, depreciating currencies, deteriorating balances of payments, a higher cost of borrowing, and a fall in domestic investor wealth—fertile ground for reduced GDP growth, if not an outright contraction.

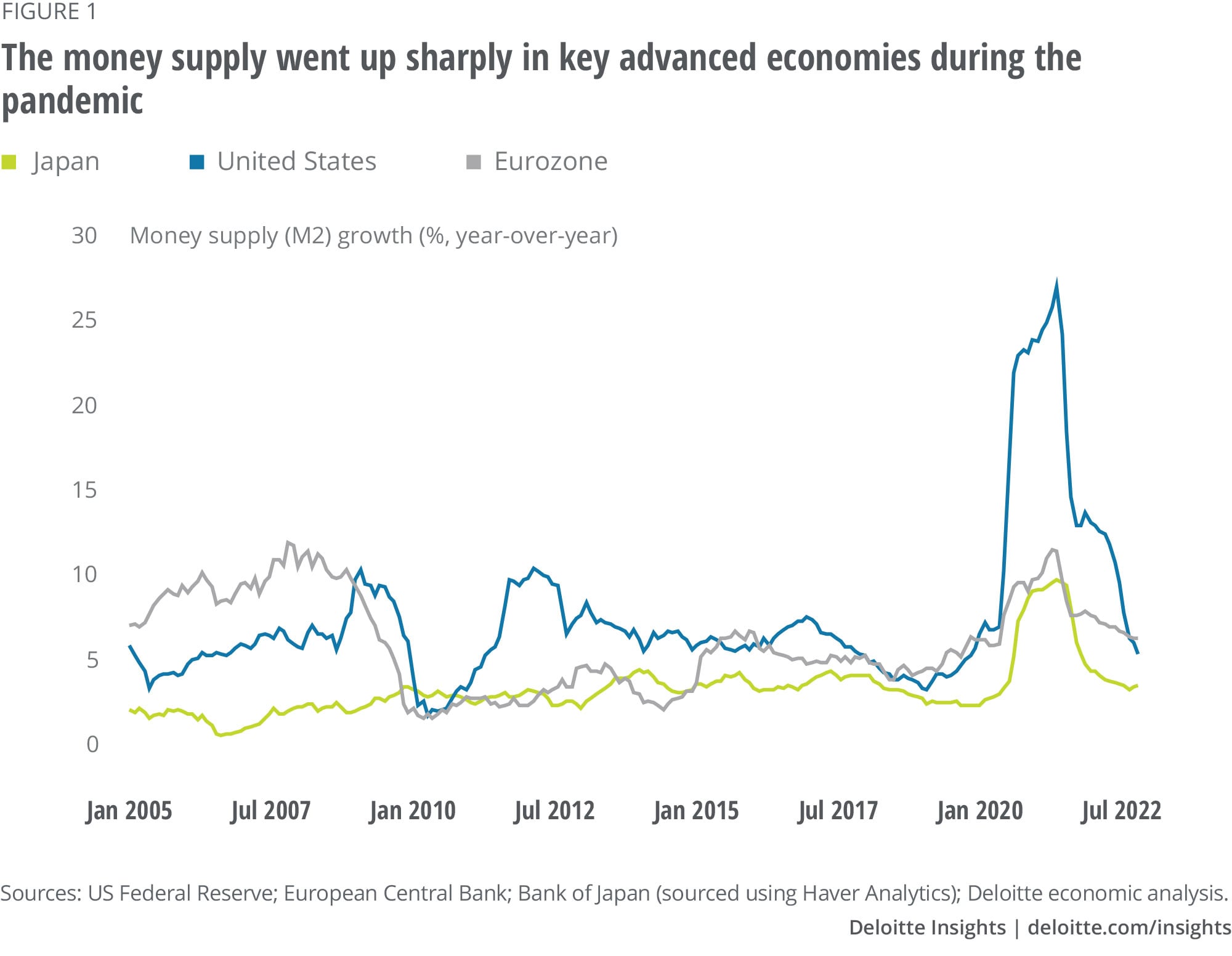

Today’s risk of capital outflows from emerging economies follows an influx of capital over a period of rapid quantitative easing (QE) by the world’s major central banks, which created very high liquidity in advanced economies. In the United States, the Fed’s assets surged by US$4.6 trillion in just two years from March 2020;4 in contrast, in its response to the Great Recession, the Fed’s assets went up by only US$3.5 trillion in the seven years from 2008 to 2014. In the Eurozone, the ECB implemented an 1,850-billion-euro pandemic emergency purchase program in 2020, expanding on the accommodative monetary policy and asset purchases it had practiced since the threat of a sovereign debt crisis in 2014.5

The result of these and similar policies was that the money supply6 shot up in key advanced economies during 2020–2021 (figure 1), spurring foreign investors toward emerging economies as they sought higher returns in equities and debt instruments.

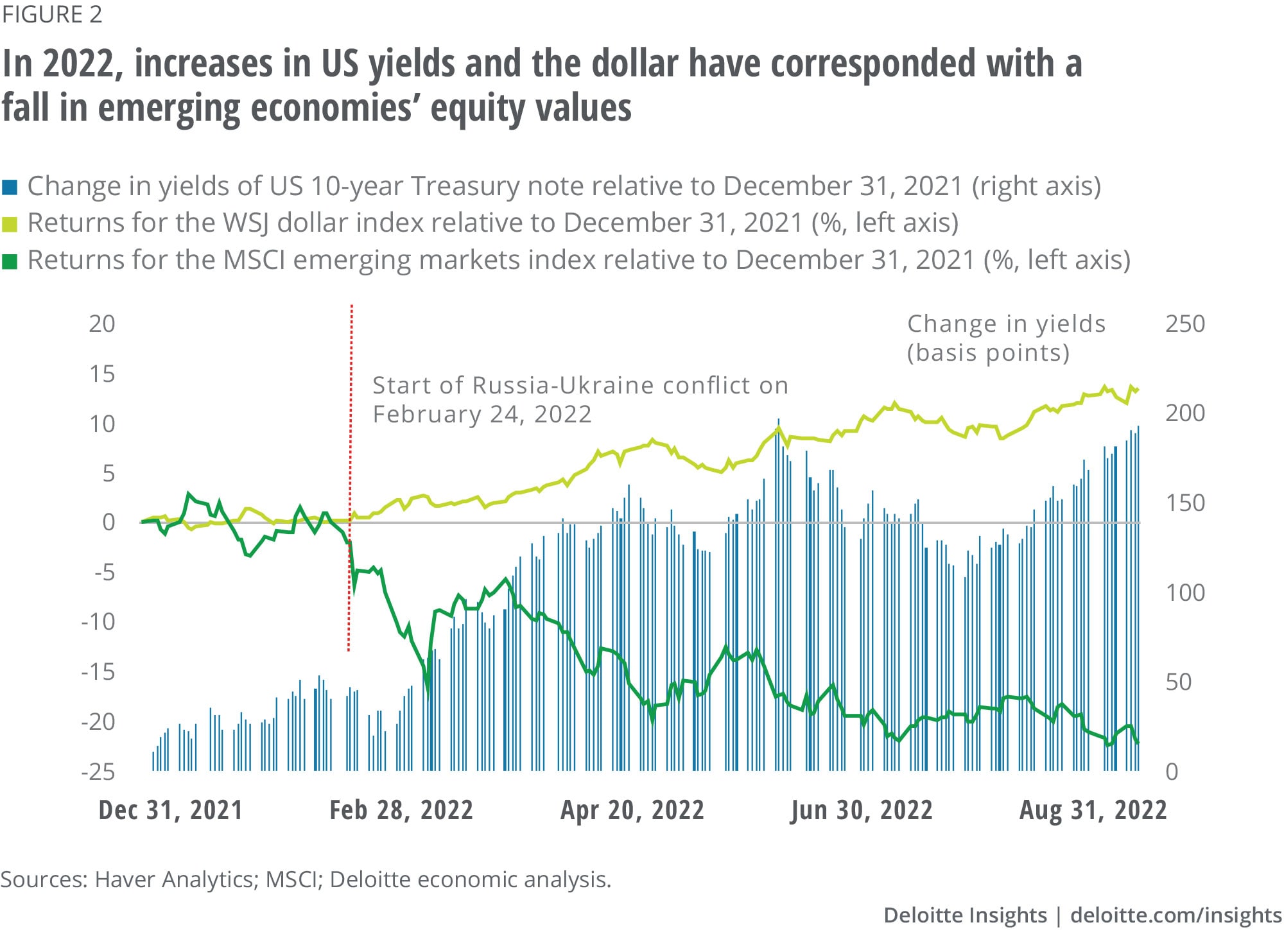

That’s changed a bit in recent times. In the five months leading up to July 2022, foreign portfolio investments (FPIs) have started to flow out of emerging economies, recording a net decline.7 These investments are unlikely to be replaced anytime soon: The Institute for International Finance predicts a 42% decrease in portfolio inflows to emerging economies for the year.8 Concurrent gains in the US dollar index aren’t helping, since it is driving up the cost of foreign funds and interest payments on external debt. Equities have also dropped steeply in emerging economies (figure 2), further encouraging foreign investors to withdraw.

Emerging economies have faced capital outflows before. The “taper tantrum” of 2013, when the Fed announced that it would reduce QE,9 saw a significant drop in FPI, as did 2016–2018 when the Fed hiked rates after seven years of record lows. Both times, however, emerging economies rode out the storm with relatively little harm.10 Many had growth fundamentals in their favor, and they used their foreign reserves effectively to counter weakness in their currencies. In fact, taken together, emerging and developing economies actually grew from 4.4% to 4.7% per year over 2016–2018.11

But this time, things seem very different. Global commodity prices, including food,12 are much higher than in the last bout of Fed tightening, and Russia’s invasion of Ukraine has only made it worse. Rising commodity prices, in turn, are spurring inflation to new heights globally. In August 2022, for example, inflation in the United States stood at 8.3% compared with 0–3% between 2016 and 2018, and other parts of the world are suffering high price pressures as well. Third, the Fed, ECB, and other major central banks are responding with faster and larger interest rate hikes than in previous rounds of tightening, not only drawing investment out of emerging economies but also causing their currencies to depreciate. Finally, emergency spending during the pandemic has left governments in many emerging economies with high debt and deficit levels at a time when high interest rates at home and abroad are making borrowing very expensive.

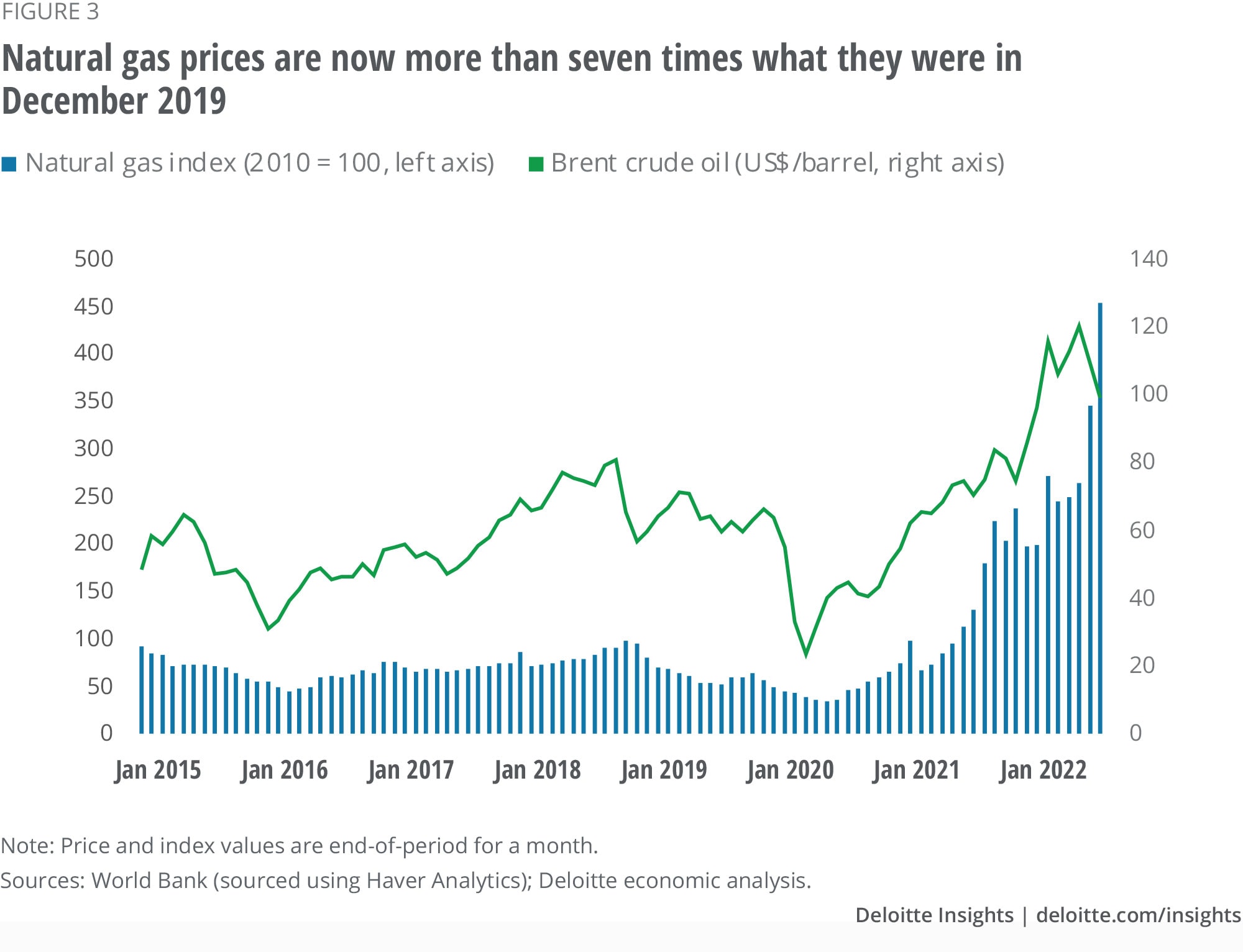

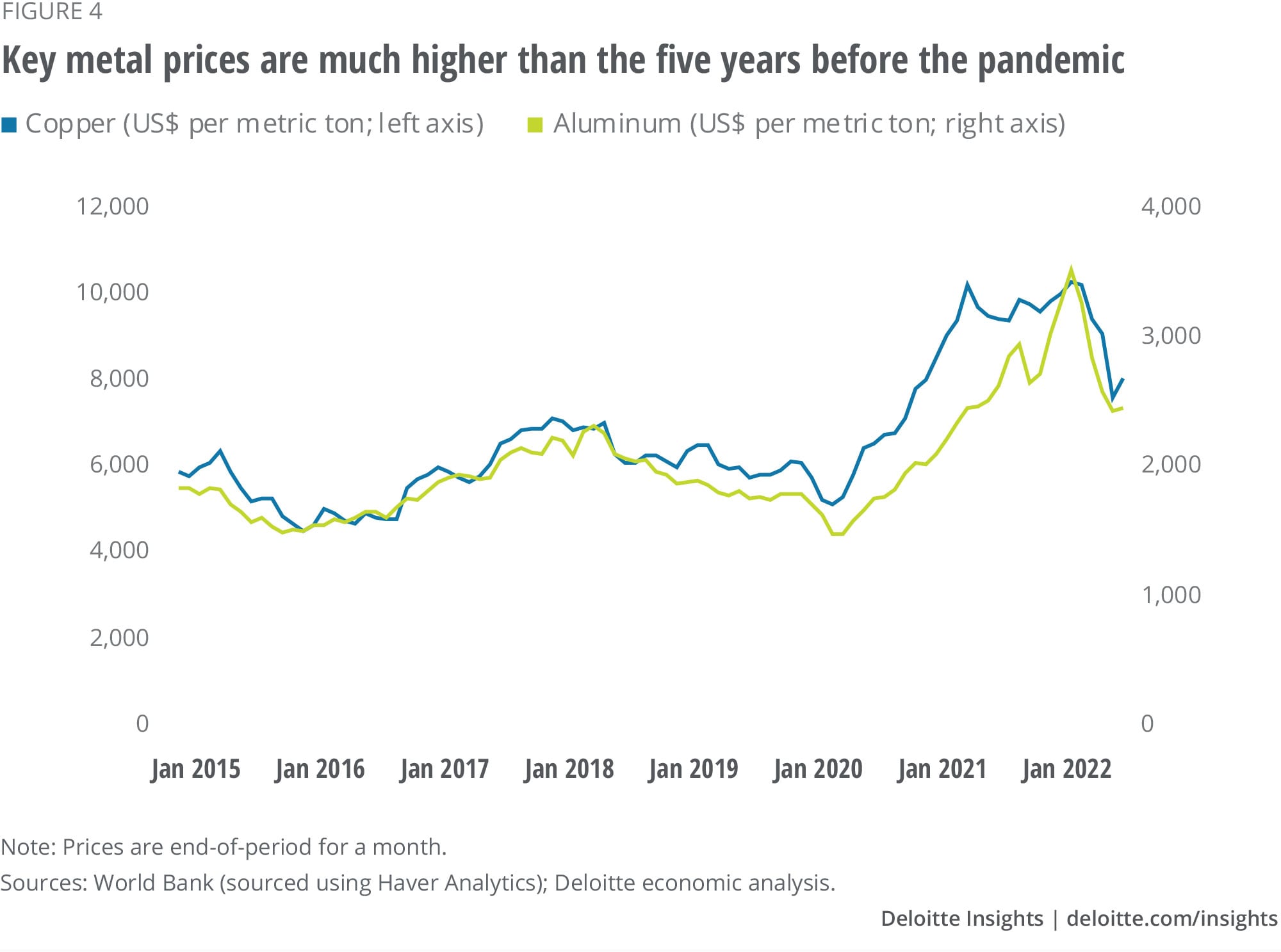

A great many commodities, from food to natural gas to metals, cost substantially more today than they did before the pandemic. This creates a drag on economies everywhere, but the effects on emerging economies, where most consumers and enterprises have less to spend, can be especially acute.

The largest human impact may be from the spiraling price of food. In August 2022, the Food and Agriculture Organization (FAO) food price index showed that global food prices were up 27% from prepandemic levels—and that was after a drop from an all-time high in March.13 High food prices could push up the number of people suffering from hunger and malnutrition. According to the FAO, 828 million people were affected by hunger in 2021—an increase of 150 million since 2019 (right before the pandemic). Rising food prices and disruptions to food supplies due to Russia’s invasion of Ukraine likely made it even worse in 2022.14

Natural gas prices, as measured by the World Bank’s commodity markets index, are also rising, and are now more than seven times what they were just before the pandemic (figure 3).15 Russia’s invasion of Ukraine, the subsequent sanctions on Russia, and cuts in Russian gas deliveries to the European Union have played an obvious part.16 Metal prices too are surging—figure 4 shows the increase in copper and aluminum prices this year.17

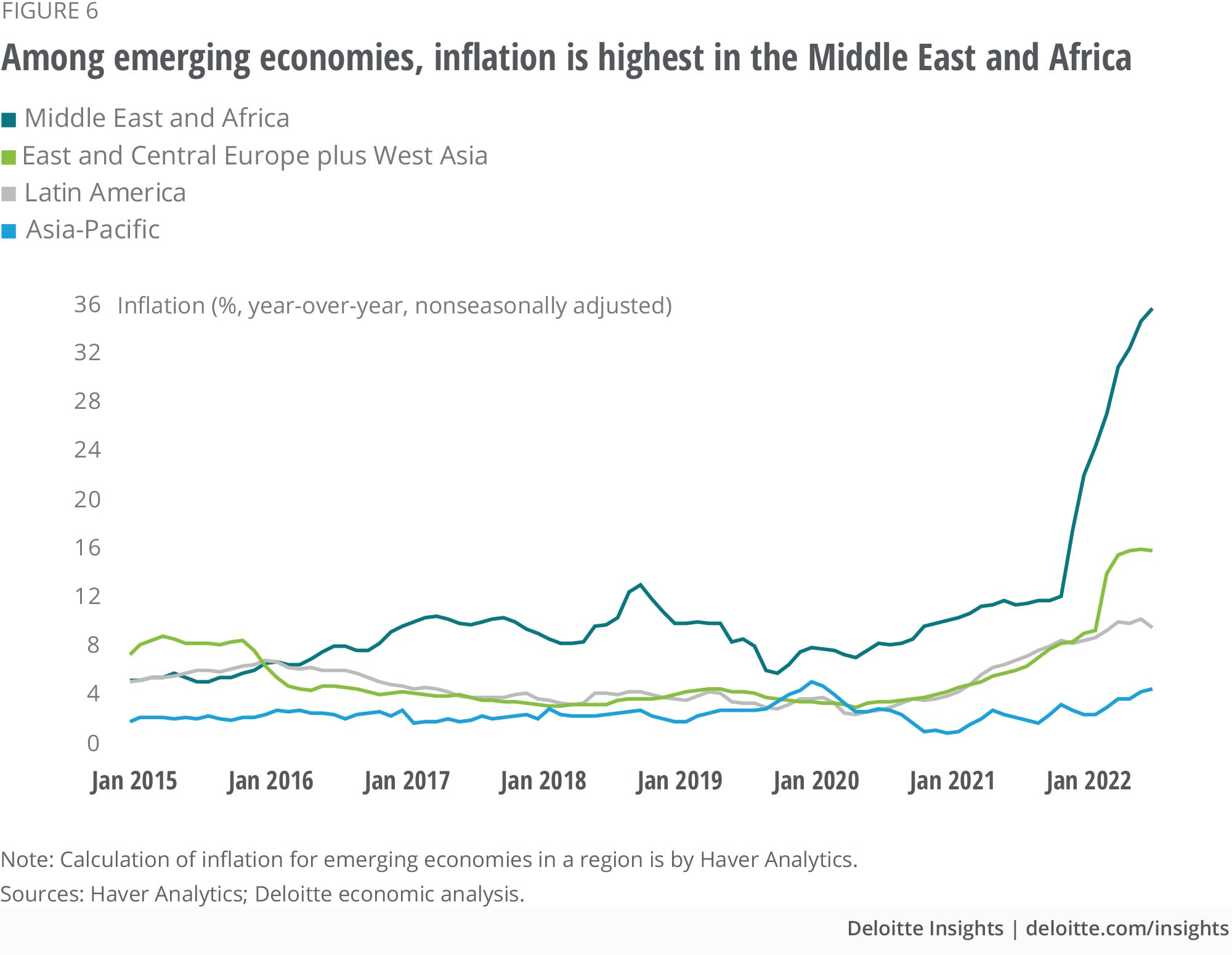

Partly due to high commodity prices, the world is facing far higher price pressures now than it did prior to the pandemic, with inflation rampant in both advanced and emerging economies (figure 5). In 2022, inflation in the United States has been higher than at any time in the past 40 years; inflation in the United Kingdom reached 10.1% in July, while in the Eurozone, it nearly doubled to 9.1% in August 2022 from the end of 2021. Meanwhile, inflation in emerging economies now averages 11%, compared with 3.1–4.2% over 2016–2018.18 Inflation is highest in emerging economies in the Middle East and Africa (figure 6), and despite the deceptively low figure for Asia-Pacific as a whole—largely because of China’s low inflation rate due to slow growth in aggregate demand—it has increased for many countries in that region as well.

High worldwide inflation raises three primary concerns for emerging economies. First, as we have seen, advanced economies are aggressively tightening their monetary policies, attracting investment away from emerging economies. Second, these capital outflows put pressure on emerging economies’ currencies, pushing up imported inflation and contributing to a vicious cycle of rising prices and depreciating currencies. Finally, inflation inhibits real income growth and poverty alleviation, two areas where emerging economies have made great strides over the last 40 years. According to the World Bank, high inflation and geopolitical tensions, together with the pandemic, will force an additional 75–95 million people worldwide into poverty in 2022.19

The speed and scale of interest rate hikes by central banks in advanced economies is something new for emerging economies. During the Fed’s prior period of monetary tightening starting in December 2015, it raised interest rates a little at a time over a time frame of years. In contrast, since January 2022, the Fed has hiked rates by 300 bps—more than the 225 bps increase between December 2015 and December 2018—in just seven months. Moreover, while the previous hikes took place in increments of 25 bps each, 2022’s hikes included three of 75 bps and one worth 50 bps.

Such large and frequent increases make it difficult for emerging economies’ central banks to defend their currencies as their value diminishes in the face of increasing capital outflows. While emerging economies have been quick to draw down foreign reserves to preserve currency stability, doing so over a long period may not be sustainable. In India, the Reserve Bank of India’s efforts to defend the rupee has cost US$80 billion in foreign reserves since August 2021, leaving it with reserves of US$561 billion.20 Other countries, such as Argentina, with relatively low foreign reserves don’t even have that luxury.

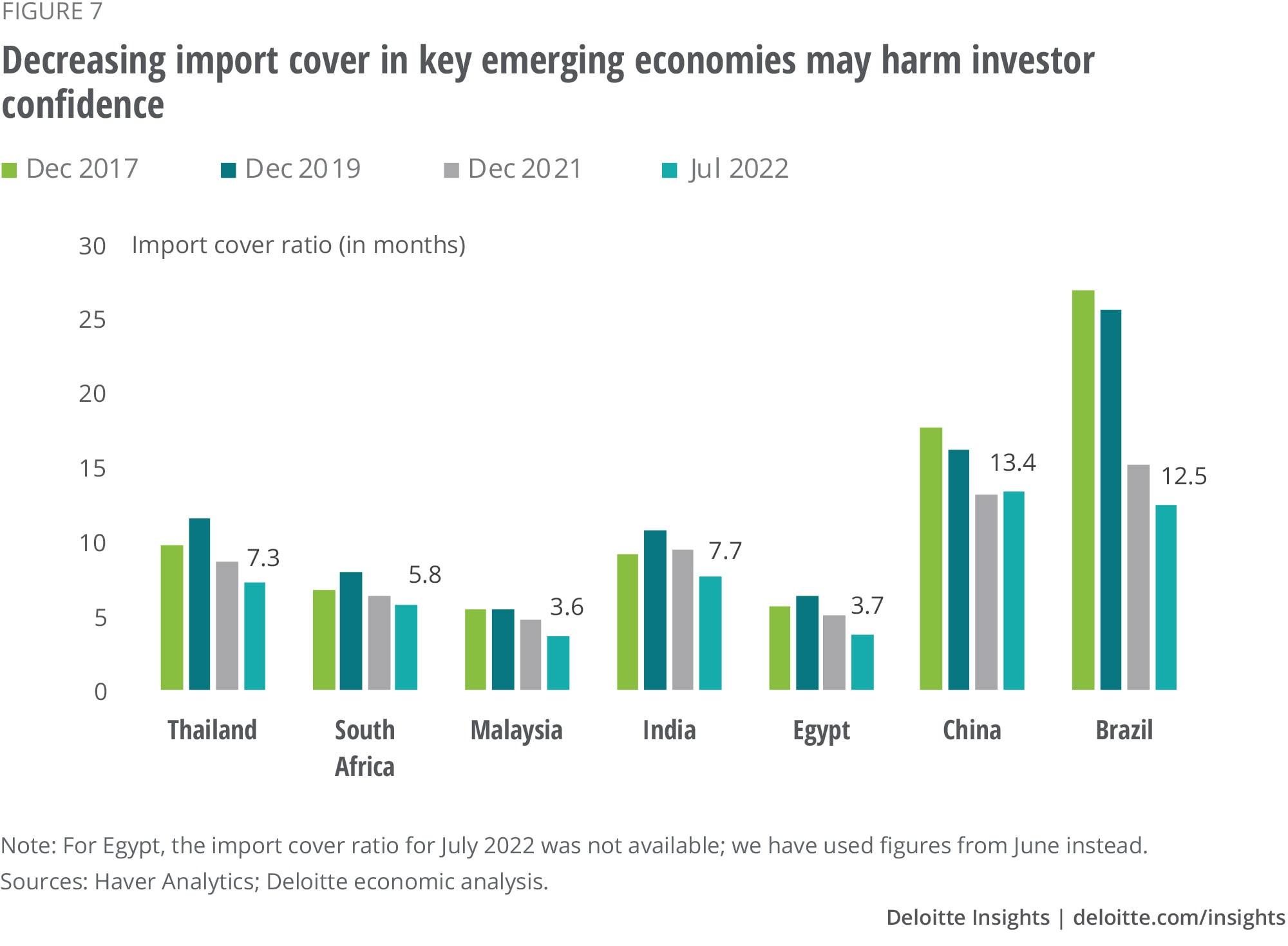

Using up reserves quickly can also decrease a country’s import cover, which is defined as the number of months of imports a country can pay for using existing foreign reserves (figure 7). Import cover declines are especially worrisome for commodity importers as it could raise trade and current account deficits and thereby encourage further currency depreciation and losses in investor confidence. An example is Sri Lanka’s situation in July 2022, when it didn’t have enough foreign reserves to pay for fuel imports. With inflation soaring, fuel shortages rampant, and the value of its currency plummeting, the country finally defaulted on its external debt for the first time in its history.21

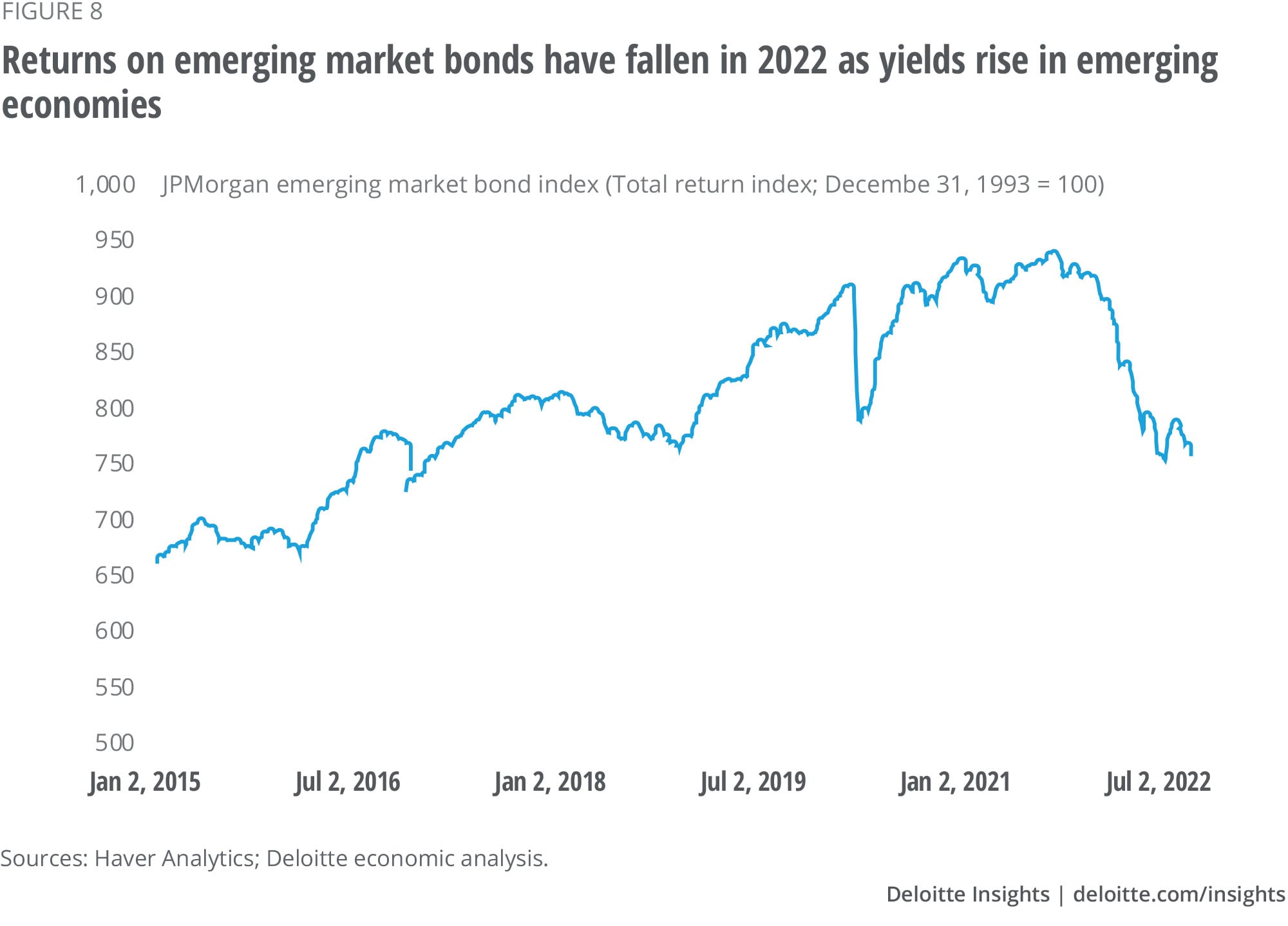

For emerging economies, advanced economies’ high interest rates and the US dollar’s appreciation have raised the cost of foreign funds and interest payments on external debt. Unfortunately, would-be borrowers may not be able to turn to domestic lenders either, as borrowing costs in emerging economies have also been rising. One reason is that emerging economies’ central banks are also tightening their monetary policies. A second is that FPI outflows from emerging economies’ bonds are denting demand, creating lower prices and higher yields.22 The JPMorgan emerging market bond Index has declined precipitously this year (figure 8), more than in prior periods of contraction.23

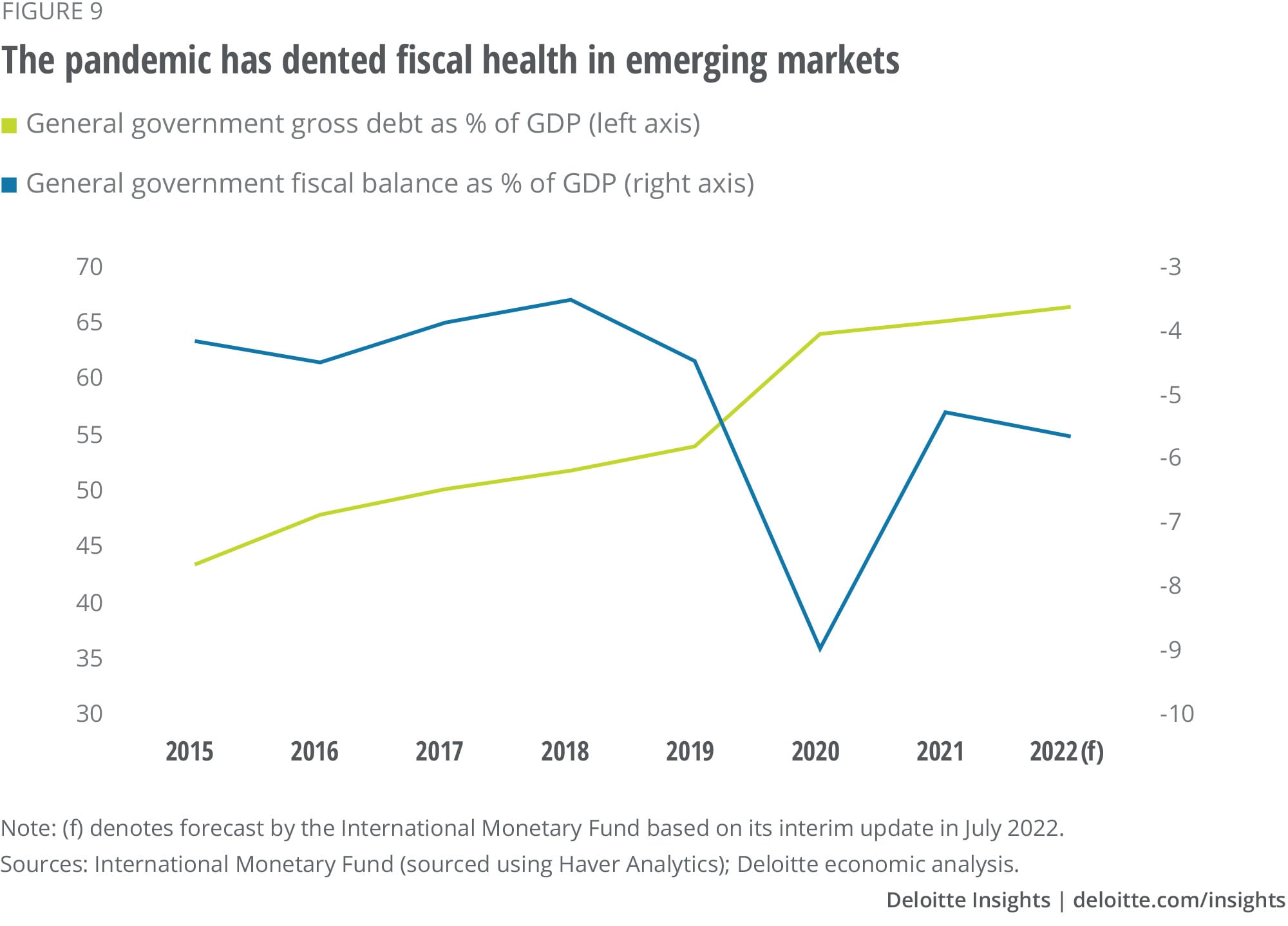

Rising borrowing costs are especially worrisome for governments in emerging economies, where two years of pandemic-induced government spending, coupled with falling revenues as economies contracted, have pushed up debt and deficit levels (figure 9). Nor does the path to fiscal consolidation look easier in the coming year, as global uncertainty, inflation, and rising borrowing costs mean that the wheels of domestic economic growth are likely to roll more slowly than anyone would like.24

So, is it all gloom and doom for emerging economies? Certainly not. Some have built sizeable foreign reserves and reformed their economies to prevent crises such as what occurred in Asia in 1997 and Russia in 1998. Commodity exporters such as Brazil and Indonesia are benefiting from high global prices. In Asia, inflation is still low in China, growth in India is picking up as consumer spending gains strength, and tourism is making a comeback in Thailand and Malaysia. External obligations too have dropped this year after surging in 2020. According to the IMF, the external-debt-to-GDP ratio for emerging and developing economies fell to 30.7% in 2021 from 32.6% in 2020.25

Many emerging economies may, therefore, defy expectations of any sharp economic slowdown. What they may require is some steely resolve to control domestic inflation, consolidate government finances, and install reforms to enhance global competitiveness. Such measures may cause short-term pain, but they could go a long way in attracting long-term foreign investments, setting the stage for strong, sustainable economic growth in the years ahead.